Key Findings

- Most state sales taxA sales tax is levied on retail sales of goods and services and, ideally, should apply to all final consumption with few exemptions. Many governments exempt goods like groceries; base broadening, such as including groceries, could keep rates lower. A sales tax should exempt business-to-business transactions which, when taxed, cause tax pyramiding. bases are smaller than ideal. The median state sales tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. only includes 23 percent of personal income. Sales taxes should taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. all final personal consumption.

- States frequently exempt consumer goods, such as clothing and groceries, but these blanket exemptions are ineffective ways to lessen the regressive nature of sales taxes.

- Due to historical accident, most states do not tax services in a notable way.

- States should expand their state sales taxes to include consumer purchases of both goods and services. However, states should exempt business-to-business transactions.

- Expanding sales tax bases improves neutrality. Newly generated revenues can then be used to finance general fund programs or other tax reforms, including paying down reductions in the sales tax rate.

- If states are still concerned about the somewhat regressive nature of sales taxes, several policy options are more effective tools than blanket exemptions. Grocery tax credits, expanded Earned Income Tax Credits, or an increased standard deductionThe standard deduction reduces a taxpayer’s taxable income by a set amount determined by the government. It was nearly doubled for all classes of filers by the 2017 Tax Cuts and Jobs Act (TCJA) as an incentive for taxpayers not to itemize deductions when filing their federal income taxes. in an income tax would provide assistance without introducing the same degree of economic distortions.

Introduction

Since the creation of the modern sales tax in 1930, state sales tax bases have been narrower than ideal. Economic theory says that sales taxes should apply to all final personal consumption, yet partly due to historic accident and partly due to policy efforts to exempt some goods, the median state sales tax base covers only 23 percent of final personal income. The narrow tax bases undermine neutrality, favoring one product or industry over another.

States have experimented with broadening their sales taxes, but most efforts have been piecemeal and frequently involved additional taxation of business-to-business transactions. Meaningful base broadening, however, remains a worthwhile endeavor, as base expansion allows for greater tax neutrality and revenue stability, and can be paired with more targeted relief for low-income households.

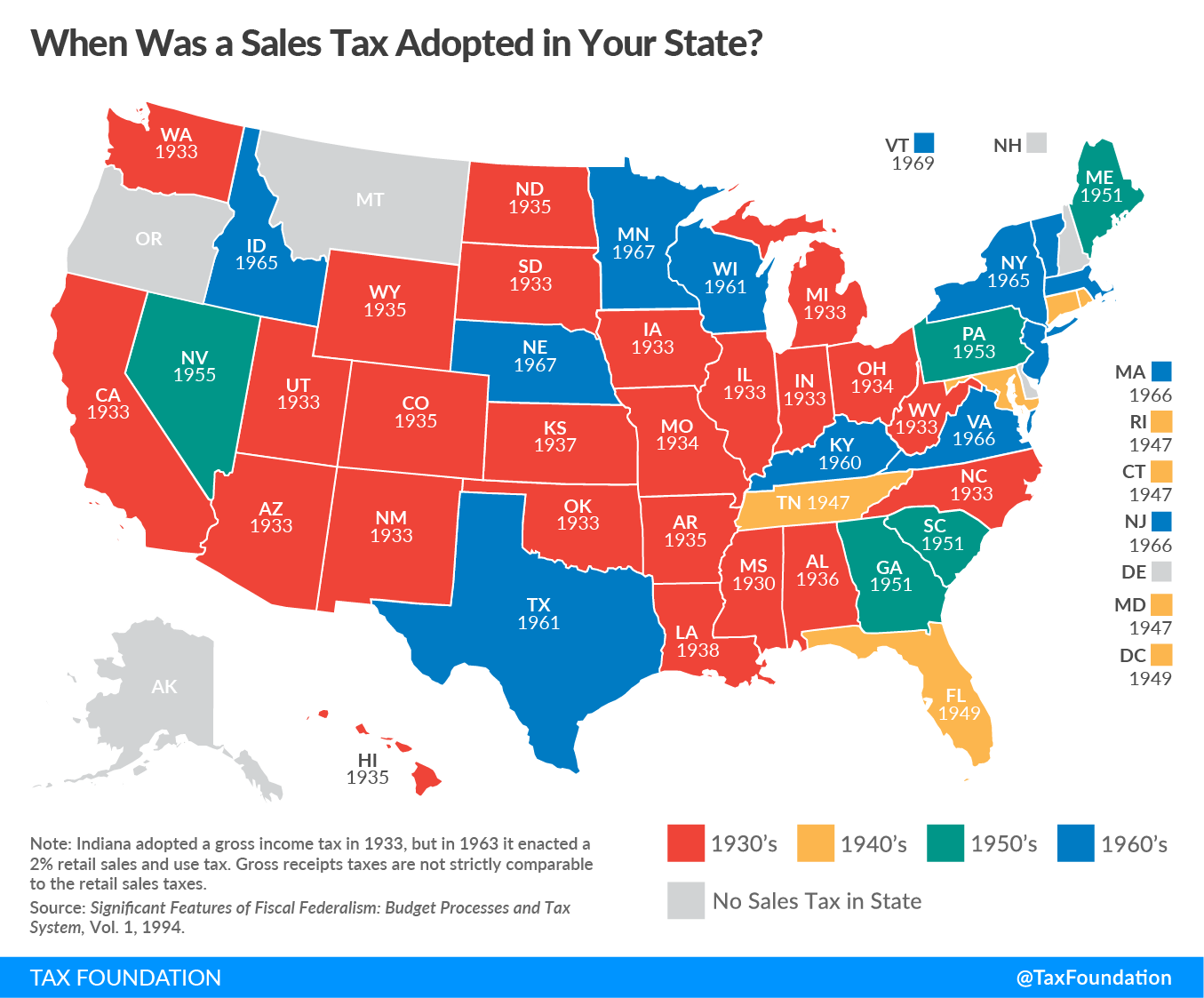

State Adoption of Sales Taxes

In 1930, Mississippi became the first state to adopt a general sales tax.[2] In the decade that followed, 23 other states followed suit (see map below) as the Great Depression disrupted state and local economies. In 1927, property taxes made up 20 percent of state government revenue and 82 percent of local government revenue. In total, two-thirds of all state and local government revenue came from property taxes. However, from 1929 to 1936, property taxA property tax is primarily levied on immovable property like land and buildings, as well as on tangible personal property that is movable, like vehicles and equipment. Property taxes are the single largest source of state and local revenue in the U.S. and help fund schools, roads, police, and other services. assessments fell substantially, approximately a 20 percent decline. The decline in property values, combined with deteriorating farm prices and high industrial unemployment, reduced property tax collections.[3] At the same time, individual and corporate income taxes became less productive. These revenue constraints were coupled with increased spending mandates from the federal government. Participation in new government programs required investments by states.[4]

States began to look for alternative sources of revenue to fund government services and began turning to the sales tax. “The sales tax,” as John Due and John Mikesell have noted, “with its low rate, large yield, and relatively painless collection, was especially attractive.”[5]

State Sales Tax Bases are too Narrow

Currently, 45 states impose a sales tax. Only Alaska, Delaware, Montana, New Hampshire, and Oregon forgo a sales tax.[6] When states began to levy a sales tax in the 1930s, the tax applied to tangible personal property, items such as clothing, home appliances, and furniture, among other taxable goods.[7]

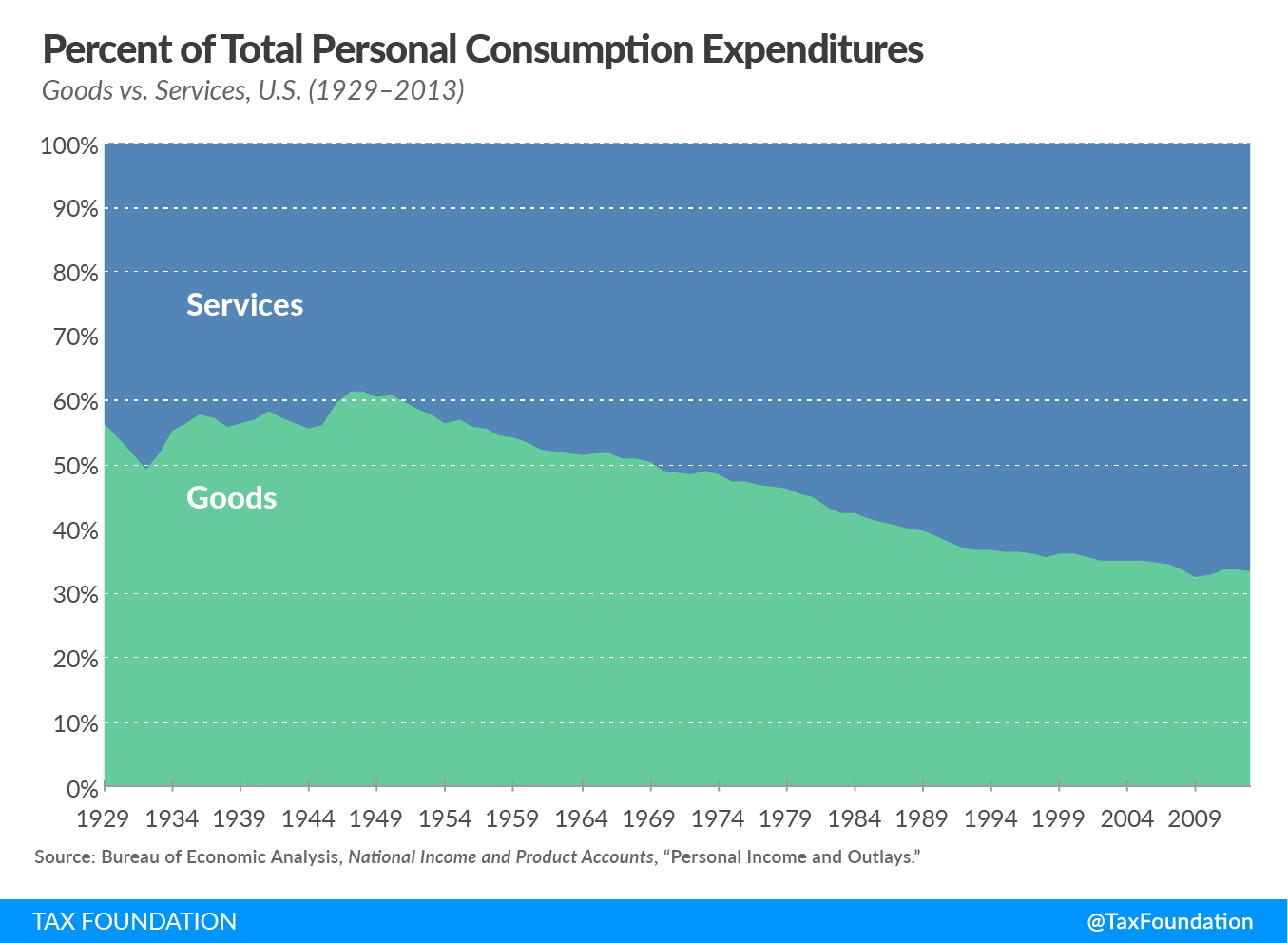

This made the tax relatively easy to administer. It also produced sufficient revenue, as the economy largely consisted of manufacturing and tangible goods. Over time, however, the U.S. economy has changed from a manufacturing-based economy to a service-based economy. Americans are purchasing more services than goods as a percentage of their consumption. In the first quarter of 2017, services accounted for approximately 68 percent of personal consumption expenditures in the United States.[8] Despite the transformation in the economy, states have responded slowly to updating their sales tax bases.

The economic transition to a service-based economy is not the only reason sales tax bases are shrinking. This trend has accelerated as states exempted a variety of household goods to mitigate the perceived regressivity of the sales tax. Together, these two long-term trends have led to improper sales tax bases. The median state’s sales tax base only includes 23 percent of a state’s personal income.[9]

| Source: Professor Emeritus John Mikesell, Indiana University | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (a) The sales tax in Hawaii, New Mexico, North Dakota, and South Dakota have broad bases that include many business-to-business transactions. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| State | Sales Tax Breadth | Rank | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| U.S. Median | 23% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Ala. | 35% | 23 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Alaska | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Ariz. | 41% | 11 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Ark. | 43% | 8 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Calif. | 28% | 35 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Colo. | 35% | 26 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Conn. | 26% | 37 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Del. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fla. | 40% | 12 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Ga. | 32% | 32 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Hawaii (a) | 104% | 1 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Idaho | 38% | 14 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Ill. | 23% | 43 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Ind. | 40% | 13 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Iowa | 35% | 22 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Kan. | 36% | 19 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Ky. | 36% | 20 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| La. | 37% | 18 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Maine | 41% | 10 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Md. | 26% | 39 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Mass. | 22% | 45 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Mich. | 36% | 20 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Minn. | 33% | 31 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Miss. | 47% | 7 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Mo. | 31% | 34 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Mont. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Neb. | 35% | 24 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Nev. | 49% | 6 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| N.H. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| N.J. | 24% | 42 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| N.M. (a) | 59% | 5 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| N.Y. | 27% | 36 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| N.C. | 34% | 29 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| N.D. (a) | 73% | 2 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Ohio | 35% | 24 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Okla. | 34% | 29 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Ore. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Pa. | 26% | 39 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| R.I. | 26% | 38 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| S.C. | 32% | 33 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| S.D. (a) | 65% | 3 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Tenn. | 34% | 28 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Texas | 42% | 9 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Utah | 34% | 27 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Vt. | 25% | 41 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Va. | 23% | 44 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wash. | 38% | 15 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| W.Va. | 37% | 16 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wis. | 37% | 16 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wyo. | 62% | 4 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Commonly Exempted Goods

Despite goods representing a declining share of the economy, they remain an important component of consumption, representing 32 percent of total personal consumption.[10] While services have in large part been exempt from taxation due to historic reasons, goods are frequently exempt from sales tax bases due to proactive exemptions issued by state legislatures. This is frequently due to perception of the regressive nature of the sales tax.

Proponents of exempting consumption goods point out that the sales tax is regressive. They argue that low-income households spend a larger portion of their income on these goods, and therefore, there is an inherent inequity in taxing necessities.[11] It is unfair to tax basic needs, per their argument. While it is true that such a tax would be regressive, that does not mean that exemptions are the correct policy choice. These arguments sometimes presuppose that sales taxes should only apply to luxury goods, not necessities, but again, this is a political argument, not one of economics.[12]

These arguments also tend to overestimate the extent to which sales taxes are regressive. In the short term, sales tax are regressive, but economic research shows that over a lifetime, the sales tax is “only slightly regressive.”[13] According to Laird Graeser, “… individuals adjust their spending patterns to approximate their long-term economic power and consumer proportionately to this long-term expectation of income.…Assuming that all consumption is taxed equally, lifetime consumption taxes are proportional to lifetime income.”[14] Even so, states frequently “address regressivity issues by modifying their sales tax base.”[15

The common exempted goods in the United States include: clothing, groceries, and prescription drugs.[16] Twenty-five states and the District of Columbia exempted two or more of these goods in 2017 (see Table 2). These goods represent a significant portion of a state tax base. Louisiana estimates that its sales tax exemptionA tax exemption excludes certain income, revenue, or even taxpayers from tax altogether. For example, nonprofits that fulfill certain requirements are granted tax-exempt status by the Internal Revenue Service (IRS), preventing them from having to pay income tax. for groceries cost the state $424 million in fiscal year 2016, while its exemption for prescription drugs costed $358 million for the same fiscal year.[17] Arkansas, which still taxes groceries at 1.5 percent, lost an estimated $197 million in fiscal year 2012, the most recent year for which data are available.[18]

| Groceries | Clothing | Prescription Medication | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Source: 2018 State Business Tax Climate Index | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Alabama | Taxable | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Alaska | No Sales Tax | No Sales Tax | No Sales Tax | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Arizona | Exempt | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Arkansas | 1.50% | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| California | Exempt | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Colorado | Exempt | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Connecticut | Exempt | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Delaware | No Sales Tax | No Sales Tax | No Sales Tax | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Florida | Exempt | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Georgia | Exempt | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Hawaii | Taxable | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Idaho | Taxable | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Illinois | 1.00% | Taxable | 1.00% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Indiana | Exempt | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Iowa | Exempt | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Kansas | Taxable | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Kentucky | Exempt | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Louisiana | Exempt | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Maine | Exempt | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Maryland | Exempt | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Massachusetts | Exempt | Exempt | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Michigan | Exempt | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Minnesota | Exempt | Exempt | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Mississippi | Taxable | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Missouri | 1.225% | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Montana | No Sales Tax | No Sales Tax | No Sales Tax | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Nebraska | Exempt | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Nevada | Exempt | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| New Hampshire | No Sales Tax | No Sales Tax | No Sales Tax | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| New Jersey | Exempt | Exempt | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| New Mexico | Exempt | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| New York | Exempt | Exempt | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| North Carolina | Exempt | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| North Dakota | Exempt | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Ohio | Exempt | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Oklahoma | Taxable | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Oregon | No Sales Tax | No Sales Tax | No Sales Tax | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Pennsylvania | Exempt | Exempt | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Rhode Island | Exempt | Exempt | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| South Carolina | Exempt | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| South Dakota | Taxable | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Tennessee | 5.00% | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Texas | Exempt | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Utah | 1.75% | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Vermont | Exempt | Exempt | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Virginia | 2.50% | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Washington | Exempt | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| West Virginia | Exempt | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wisconsin | Exempt | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wyoming | Exempt | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| District of Columbia | Exempt | Taxable | Exempt | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Exemptions can force odd choices for consumers. New York’s clothing exemption only applies to clothing or footwear costing less than $110. This creates an incentive to purchase an item that is slightly less than $110 rather than one that is slightly above $110, regardless of the consumer’s preference for one item or the other.[19]

But sales tax exemptions can extend far behind clothing, groceries, and prescription drugs. Many states exempt flags, newspapers, and magazines from the sales tax, items that are far from being considered necessities. Pennsylvania even exempts youth sports programs.[20] A number of states in recent years have moved to exempt feminine hygiene products from sales taxes.[21] States can also engage in short-term sales tax exemptions, known as sales tax holidays. In 2017, 16 states held sales tax holidays, [22] ranging from back to school holidays to ones for hurricane preparedness in Florida. Sales tax holidays involve political gimmicks, and favor one industry or product over another.[23]

States also tend to exempt items which are subject to additional excise taxes, such as gasoline or cigarettes. Only four states, Hawaii, Illinois, Indiana, and Michigan, completely include gasoline in their sales tax base.[24] It is often stated that these products are exempt from the sales tax base because of concerns over double taxationDouble taxation is when taxes are paid twice on the same dollar of income, regardless of whether that’s corporate or individual income. ; however, this argument falls flat. These taxes have two separate purposes. Gasoline, along with other items, is indeed final personal consumption, and it should be taxed accordingly. It can also then be true that gasoline is a good proxy for road usage, and an excise taxAn excise tax is a tax imposed on a specific good or activity. Excise taxes are commonly levied on cigarettes, alcoholic beverages, soda, gasoline, insurance premiums, amusement activities, and betting, and typically make up a relatively small and volatile portion of state and local and, to a lesser extent, federal tax collections. to fund general transportation expenditures is necessary. But the presence of an excise tax does not negate that gasoline should be subject to a general sales tax. If the total tax burden is deemed too high, the preferred approach is to lower the excise tax, not to exempt the item from the general sales tax.[25]

Services

While several states have made forays in this direction, such as Florida’s brief attempt in 1986,[26] most states do not broadly tax personal services in their sales tax base. The lack of sales tax on services is one of “historical accident, not logic.”[27] As John Due described, “Acquisition of services by households constitute consumption expenditure in the same fashion as the purchase of commodities; there is no basic difference between the two that warrants different tax treatment.”[28]

Not taxing services, similar to exempting goods, introduces distortions into consumer decisions. Imagine that a state taxes the purchase of appliances, but does not tax repair services.[29] This encourages the consumer to repair the current appliance, rather than purchase a new one. There are obviously many reasons why someone could decide that repairing an appliance is preferable to purchasing new, but now the sales tax treatment has given repair companies a competitive advantage over appliance retailers.[30] The tax code should not favor the repair industry over the retailing industry.

Table 3 shows four selected personal services and whether they are taxable in each state.

| Source: 2018 State Business Tax Climate Index | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Dry Cleaning | Fitness | Barber | Veterinary | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Alabama | Exempt | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Alaska | No Sales Tax | No Sales Tax | No Sales Tax | No Sales Tax | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Arizona | Exempt | Taxable | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Arkansas | Taxable | Taxable | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| California | Exempt | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Colorado | Exempt | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Connecticut | Exempt | Taxable | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Delaware | No Sales Tax | No Sales Tax | No Sales Tax | No Sales Tax | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Florida | Exempt | Taxable | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Georgia | Exempt | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Hawaii | Taxable | Taxable | Taxable | Taxable | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Idaho | Exempt | Taxable | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Illinois | Exempt | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Indiana | Exempt | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Iowa | Taxable | Taxable | Taxable | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Kansas | Taxable | Taxable | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Kentucky | Exempt | Taxable | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Louisiana | Taxable | Taxable | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Maine | Taxable | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Maryland | Taxable | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Massachusetts | Exempt | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Michigan | Taxable | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Minnesota | Taxable | Taxable | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Mississippi | Taxable | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Missouri | Exempt | Taxable | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Montana | No Sales Tax | No Sales Tax | No Sales Tax | No Sales Tax | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Nebraska | Exempt | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Nevada | Exempt | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| New Hampshire | No Sales Tax | No Sales Tax | No Sales Tax | No Sales Tax | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| New Jersey | Exempt | Taxable | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| New Mexico | Taxable | Taxable | Taxable | Taxable | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| New York | Exempt | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| North Carolina | Taxable | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| North Dakota | Exempt | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Ohio | Taxable | Taxable | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Oklahoma | Exempt | Taxable | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Oregon | No Sales Tax | No Sales Tax | No Sales Tax | No Sales Tax | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Pennsylvania | Exempt | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Rhode Island | Exempt | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| South Carolina | Taxable | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| South Dakota | Taxable | Taxable | Taxable | Taxable | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Tennessee | Taxable | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Texas | Taxable | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Utah | Taxable | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Vermont | Exempt | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Virginia | Exempt | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Washington | Taxable | Taxable | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| West Virginia | Taxable | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wisconsin | Taxable | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wyoming | Taxable | Exempt | Exempt | Exempt | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| District of Columbia | Taxable | Taxable | Exempt | Taxable | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Benefits of Broadening the Base

An overly narrow sales tax base introduces a number of problems. Sales taxes are not neutral across consumer purchases, and they are not as effective at raising revenue as they could be. Furthermore, exempting items is also not an ideal way to address regressivity. Base broadeningBase broadening is the expansion of the amount of economic activity subject to tax, usually by eliminating exemptions, exclusions, deductions, credits, and other preferences. Narrow tax bases are non-neutral, favoring one product or industry over another, and can undermine revenue stability. fixes these issues, and also reduces tax administration costs. However, all base broadening must provide exemptions for business-to-business transactions.

The presence of exemptions creates demand for further exemptions as political interests organize to demand more exemptions. Broadening the tax base sends a strong signal in the opposite direction.

Improved Neutrality

The overall goal of expanding the sales tax base is increased neutrality within the tax code. Consumers are likely to shift towards untaxed purchases, regardless of their actual preferences. Ideally, the sales tax would apply to all consumer transactions, as to not bias consumer behavior.[31]

Investment can also be misappropriated due to sales tax exemptions. Firms or industries might see increased demand, encouraging further expansion through capital expenditures.

Lower Rates and Greater Revenue Stability

Narrower bases also limit the ability to collect necessary revenues. A broader sales tax base provides the opportunity for additional revenue, because there is a larger basket of goods and services to tax. In contrast, exempting items from the sales tax base means that the tax rate on taxable items must be higher than it would otherwise be. Pennsylvania’s sales tax exemptions on groceries, prescription drugs, and clothing totaled $3.2 billion in fiscal year 2016, compared to the $10 billion in total sales tax collections for the state. The sales tax on all the remaining taxable items must be significantly higher to offset the $3.2 billion in exempted purchases. These are obviously not the only sales tax exemptions in Pennsylvania; adding all of Pennsylvania’s exemptions would result in an even greater imbalance. Tax rates in Pennsylvania are notably higher to generate the $10 billion in revenue than they could be if the base was expanded to include these previously exempted transactions.

Additionally, narrow sales tax bases hinder a key feature of consumption taxes: revenue stability. Sales tax revenue collections are currently dominated by large purchases, such as appliances, furniture, or motor vehicles, all types of items where purchases slow during times of economic weakness. Expanding the sales tax base to include items deemed to be essential, such as food and clothing, limits the volatility of collections. Even during recessions, these basic necessities would be purchased, though the items purchased might vary slightly, for instance, away from expensive cuts of meat like steak to less expensive like ground beef. Carving away the base introduces more volatility to revenue collections.

Not the Ideal Way to Offset Regressivity

Blanket exemptions are also blunt instruments for ameliorating regressivity, which as discussed previously is often overstated. Exempting all grocery items, while sold as a help to low-income taxpayers, benefits all consumers, regardless of their income level. Arguably, the exemption actually benefits higher-income individuals more than lower-income individuals as their total grocery spending will be higher. These families might “spend substantial amounts on expensive cuts of meat, fresh fruit out of season, exotic seafoods, and other items.”[32] Households that shop at more expensive grocery chains or buy more expensive items benefit disproportionately from the exemption.[33]

Additional research has found that broadening sales tax bases and using the new revenues to reduce rates is actually less regressive than the status quo. For instance, a study by the Minnesota Department of Revenue found that an expanded base and lower rate of 5 percent (down from 6.5 percent) would be less regressive than their current structure.[34]

Funding Other Tax Reforms

Additionally, sales tax base broadening can be used to fund other tax reforms. Expanding the sales tax base increases revenue, providing the funds necessary to offset tax changes in other areas. For instance, North Carolina’s tax reform in 2013 lowered and flattened its individual income tax, and lowered corporate income tax. The changes were in part financed with a broadened sales tax base that included admissions charges to live entertainment, movies, and certain attractions.

The District of Columbia followed a similar path. Its tax reform package in 2014 included an expansion of the sales tax to include gym memberships, among other items.[35] These sales tax base expansions helped finance cuts to the individual and corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. and an expanded Earned Income Tax Credit (EITC).

Simplifying Tax Administration

Broadening the sales tax base also eases tax administration.[36] Much time and effort is spent trying to distinguish between taxable and nontaxable items, leading to complex and complicated questions on how to define various items.

Many states, for example, do not tax groceries, but do tax candy and soda. But what are the defining features of candy?[37] This quickly becomes a difficult question. In many states, the inclusion of flour makes an item food and therefore exempt, while candy without flour would be taxable. The presence of sweeteners could make something candy too. New Jersey includes sweetened chocolate chips in its tax base, but excludes unsweetened chocolate chips.[38]

The Wisconsin Department of Revenue released a guidance document in 2010 discussing the various tests for determining whether an ice cream cake was subject to the sales tax.[39] Taxability hinges on several key questions, such as whether the retailer provides utensils and if there are multiple food items, like fudge and a cake layer, in the ice cream cake. These kinds of tax structures create unnecessary compliance costs for businesses and for the state.

Now, all of this is not to say that expanding the sales tax base is without challenge. Questions regarding situsing[40], particularly around services, are important, but broader bases reduce the costs of tax administration.[41]

Business-to-Business Transactions

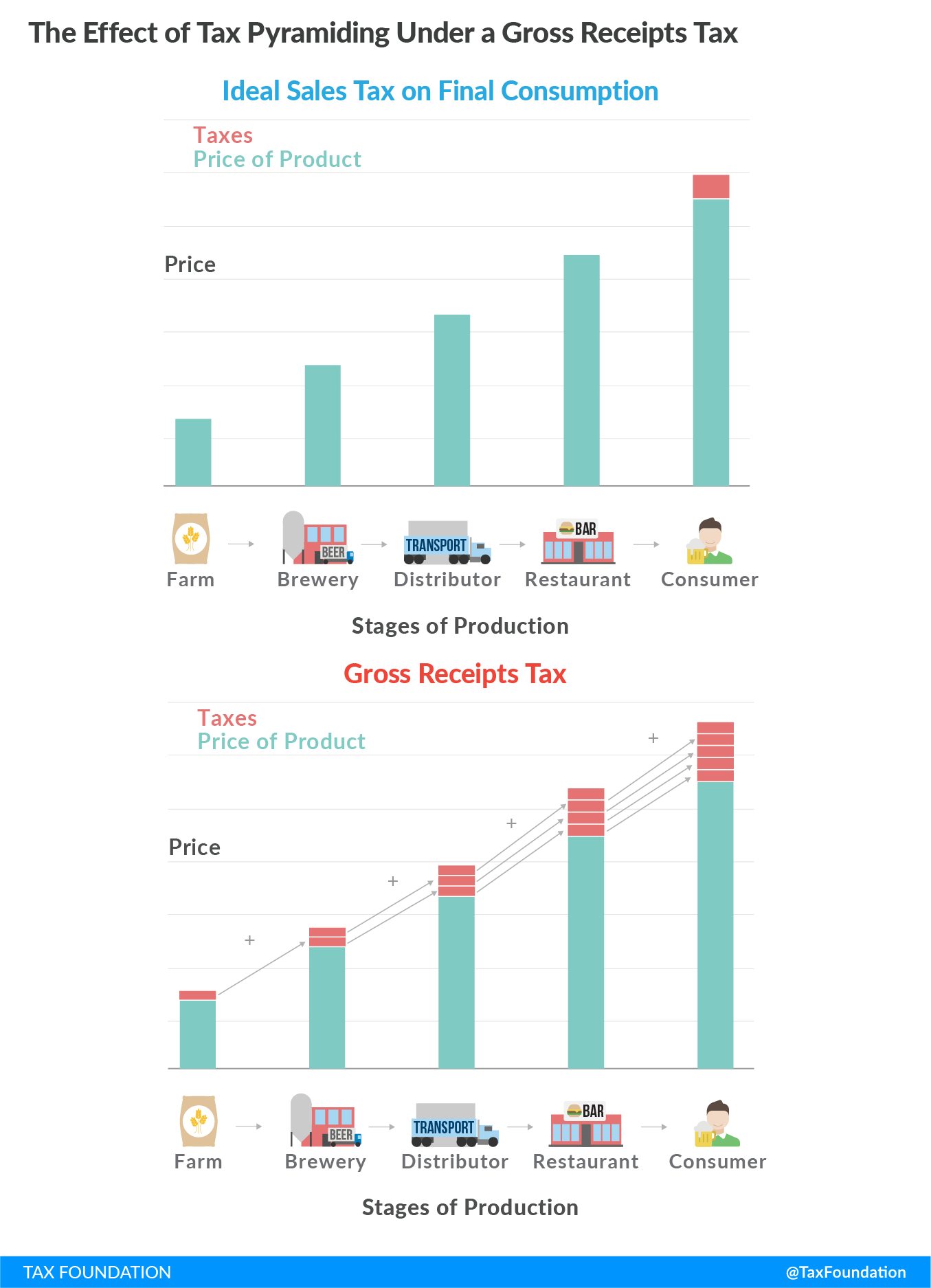

While all final consumption, both goods and services, should be taxed within a sales tax, it is crucial that consumption by businesses should be exempted.[42] This is not due to a preference for businesses over the general public, but rather an attempt to avoid “tax pyramidingTax pyramiding occurs when the same final good or service is taxed multiple times along the production process. This yields vastly different effective tax rates depending on the length of the supply chain and disproportionately harms low-margin firms. Gross receipts taxes are a prime example of tax pyramiding in action. .”[43]

By taxing inputs, goods or services, the price of the final product becomes more expensive; taxes are assessed multiple times as the goods or services come to market, increasing costs and yielding higher prices for consumers. Firms would pass the burden of the tax forward to their customers to manage their profit margins, and the multiple layers of sales taxes on inputs would turn the state sales tax into a gross receipts tax.

But passing the tax forward isn’t always possible. In firms or industries with strong price competition, firms would be hesitant to pass costs directly to consumers. In some cases, such as products with suggested manufacturers’ retailing pricing and national pricing strategies, the retailer is strictly prohibited from passing the costs forward.[44] In those instances, the firm instead might shift the increased costs to labor, perhaps by cutting hour and benefits or limiting overall hiring.

It also introduces a number of biases. Items with longer production cycles bear a disproportionate share of the tax. Firms may choose to streamline the production process so that everything is made in-house. In this way, they would not be subject to the sales tax on business purchases, creating an incentive for vertical integration.

At its most extreme, taxing all business inputs converts a sales tax into a gross receipts taxGross receipts taxes are applied to a company’s gross sales, without deductions for a firm’s business expenses, like compensation, costs of goods sold, and overhead costs. Unlike a sales tax, a gross receipts tax is assessed on businesses and applies to transactions at every stage of the production process, leading to tax pyramiding. .[45] However, most states exist somewhere in between a purely personal consumption-based sales tax and a gross receipts tax. According to data from the Council on State Taxation, firms paid $150 billion in general sales taxes on inputs in fiscal year 2015.[46] Care must be given to ensure that any base broadening does not unintentionally include business-to-business transactions.

Addressing Equity Concerns

As discussed, sales tax exemptions are frequently rooted in concerns over the regressive nature of sales taxes. However, limiting tax bases through blanket exemption is a problematic approach in terms of both neutrality and administration. There are several preferred ways to ameliorate regressivity without providing broad exemptions in a sales tax code.

Expanding to Services

Expanding sales tax bases to services is one way to broaden the tax base in a relatively progressive fashion.[47] Consumption of many personal services, such as cosmetic and beauty services, fitness, pet grooming and veterinary services, and landscaping, among others, skews towards the higher end of the income scale. Including personal services would increase tax neutrality, while providing for increased revenue, allowing the state to reduce the overall tax rate.

Earned Income Tax CreditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income rather than the taxpayer’s tax bill directly.

Tax credits could protect low-income households without preventing a broad base sales tax structure. One option for states is to increase the Earned Income Tax Credit (EITC) for low-income households. Currently, 26 states and the District of Columbia have their own EITC, in addition to the federal one. Twenty-two of these states make the credits fully refundable if the amount exceeds taxes owed.[48] Providing an EITC would also eliminate nonneutralities introduced by exemptions, while providing an offset to any regressive effects of the sales tax.

Grocery Tax Credit

Another option is to apply a grocery tax credit to offset the sales tax paid on food purchases, similar to those instituted in Oklahoma and Idaho. Residents in Idaho receive a tax credit of $100 to offset sales tax paid on groceries.[49] Oklahoma’s credit is $40 per year if the household income is below $20,000, or below $50,000 for those who have at least one dependent.[50] In both states the credit is refundable for those without income tax liability.

As noted previously, blanket food exemptions actually provide substantial tax cuts to high-income households as all their grocery purchases are also exempt. Food purchases would no longer be exempt from taxation, as they currently are in most states, which disproportionately benefits those with high food expenditures. A grocery tax credit is a more targeted approach.[51]

Increased Standard Deduction

Finally, states can always increase the standard deduction for their income taxes, for those filing single, married filing jointly, or head of households. An increase in the standard deduction has been a part of the successful tax reform packages North Carolina has enacted in the last few years, as a means to protect low-income households.

Impact of E-Commerce on Sales Taxes

The proliferation of internet retailing provides a challenge to states. As more individuals purchase items via online retailers, state sales tax collections have fallen as many retailers do not have sufficient nexus, traditionally defined as property or payroll, in a state to require the retailer to collect and remit sales taxes. Many online retailers fail to meet this standard, putting strain on state sales taxes.

The scope of the issue, however, is not immediately clear. Americans spent almost $400 billion online in 2016, or approximately 8 percent of all retail sales.[52] However, given narrow state sales tax bases, it’s not obvious that all these transactions would be taxable if they had been purchased in-person via a brick-and-mortar location. A 2009 study[53] estimated that state revenue collections would fall by $11 billion in 2012 due to internet purchases; however, their estimates seem too large based on state experiences.[54]

In 2017, Amazon, the largest online retailer, announced that it would start collecting sales tax on its purchases (excluding items sold via its Marketplace feature) in all states with a sales tax, likely increasing state sales tax collections, and limiting the amount of lost revenue.[55]

Conclusion

Partly due to historic accident and partly due to proactively carving up their tax base, state sales tax bases are exceedingly small, with the median state only taxing 23 percent of its personal income. The lack of a broad tax base introduces a number of distortions to the marketplace, influencing consumer behavior. Expanding state sales tax bases improves neutrality.

Frequently, sales tax base exemptions are presented as a way to make the tax code more progressive, but broad sales tax exemptions can actually benefit high-income households more than low-income households. States concerned about regressivity should consider other options than broad exemptions for entire classes of goods.

Sales taxes are key in a state revenue toolkit for numerous reasons, such as revenue yield and stability, and ease of administration, but if states continue to erode the base through exemptions, the effectiveness of sales taxes will be lessened. Expanding sales tax bases to services and removing previously-passed exemptions would allow states to improve the revenue collections and stability from their taxes, while improving neutrality. States should confront this challenge if they hope to retain this important feature in their revenue toolkits.

[1] The author thanks Isai Chavez for his research assistance and analysis.

[2] John F. Due and John L. Mikesell, Sales Taxation: State and Local Structure and Administration (Baltimore: The John Hopkins University Press, 1983), 2.

[3] Ronald Snell, “State Finance in the Great Depression,” National Conference of State Legislatures, March 2009, http://www.ncsl.org/print/fiscal/statefinancegreatdepression.pdf, 3.

[4] Robert D. Ebel and Christopher Zimmerman, “Sales Tax Trends and Issues,” in Sales Taxation: Critical Issues in Policy and Administration (Westport, CT: Praeger Publishers, 1992), 7-9.

[5] Due and Mikesell, Sales Taxation: State and Local Structure and Administration, 2.

[6] Morgan Scarboro, “Table 19. State and Local Sales Tax Rates” in Facts and Figures 2017, Tax Foundation/wp-content/uploads/2017/03/TF-Facts-Figures-2017-7-10-2017.pdf. Alaska has local sales taxes with average local rates of 1.76 percent, while Montana allows local sales taxes in resort areas.

[7] Ebel and Zimmerman, “Sales Tax Trends and Issues,” 16-17.

[8] Bureau of Economic Analysis, “Table 2.3.5. Personal Consumption Expenditures by Major Type of Product,” July 28, 2017.

[9] Morgan Scarboro, “Table 22. State Sales Tax Breadth,” in Facts & Figures 2017, Tax Foundation, /wp-content/uploads/2017/03/TF-Facts-Figures-2017-7-10-2017.pdf.

[10] Bureau of Economic Analysis, “Table 2.3.5. Personal Consumption Expenditures by Major Type of Product,” July 28, 2017.

[11] John F. Due and John L. Mikesell, Sales Taxation: State and Local Structure and Administration (Washington, D.C.: Urban Institute Press, 1994), 9.

[12] Economic theory actually goes even further. If true efficiency is the goal, necessities should be taxed at an even higher rate as their elasticities are higher, meaning higher costs are less likely to decrease consumption.

[13] Laird Graeser and Allen Murray, “Sales Tax on Services: State Trends,” in Sales Taxation: Critical Issues in Tax Policy and Administration (Westport, CT: Praeger Publishers, 1992), 101.

[14] Ibid.

[15] Graeser and Murray, in Sales Taxation: Critical Issues in Tax Policy and Administration, 81.

[16] Scott Drenkard, “Three Big Problems with Sales Taxes Today – and How to Fix Them,” Tax Foundation, February 10, 2017, https://taxfoundation.org/three-big-problems-sales-tax/.

[17] Louisiana Department of Revenue, “State of Louisiana Tax Exemption Budget, 2016-2017,” March 2017, http://revenue.louisiana.gov/Publications/TEB%20(1617)%20.pdf.

[18] Arkansas Department of Finance and Administration, “Exemptions from the 6% Arkansas Gross Receipts Tax and Compensating Use Tax,” April 2012, http://www.dfa.arkansas.gov/offices/exciseTax/salesanduse/Documents/SalesTaxExemptionsFY2011.pdf.

[19] New York State Department of Taxation and Finance, “Clothing and Footwear Exemption,” Tax Bulletin ST-122, March 10, 2014, https://www.tax.ny.gov/pubs_and_bulls/tg_bulletins/st/clothing_and_footwear.htm.

[20] Governor Tom Wolf, “2017-2018 Governor’s Executive Budget,” February 7, 2017, D-69, http://www.budget.pa.gov/PublicationsAndReports/CommonwealthBudget/Documents/2017-18%20Proposed%20Budget/2017-18%20Budget%20Document%20-%20Web.pdf.

[21] Nicole Kaeding, “Tampon Taxes: Do Feminine Hygiene Products Deserve a Sales Tax Exemption?” Tax Foundation, April 26, 2017, https://taxfoundation.org/tampon-taxes-sales-tax/.

[22] Joseph Bishop-Henchman and Scott Drenkard, “Sales Tax Holidays: Politically Expedient but Poor Tax Policy, 2017,” Tax Foundation, July 25, 2017, https://taxfoundation.org/sales-tax-holidays-2017/.

[23] Ibid.

[24] Jared Walczak, Scott Drenkard, and Joseph Bishop-Henchman, 2018 State Business Tax Climate Index, Tax Foundation.

[25] Due and Mikesell, Sales Taxation, 1983, 77.

[26] James Francis, “The Florida Sales Tax on Services: What Really Went Wrong,” in The Unfinished Agenda for State Tax Reform, (Denver: National Conference of State Legislatures, 1988), 129-149.

[27] John F. Due, “Proposed Application of the Illinois Sales Tax to Services,” Illinois Business Review 44, no.3. (June 1987), 3.

[28] Due, “Proposed Application of the Illinois Sales Tax to Services,” 3.

[29] William F. Fox, “Sales Taxation of Services: Has its Time Come,” in Sales Taxation: Critical Issues in Tax Policy and Administration (Westport, CT: Praeger Publishers, 1992), 52.

[30] Ibid.

[31] Kaeding, “Tampon Taxes: Do Feminine Hygiene Products Deserve a Sales Tax Exemption.”

[32] Due and Mikesell, Sales Taxation, 1983, 68.

[33] The federal government also prohibits sales taxation of food items purchased with Supplemental Nutrition Assistance Program (food stamp) funds, meaning that truly low-income individuals are already exempted without broader grocery exemptions.

[34] John P. James, “Sales Tax on Services: A Tax Administrator’s Perspective,” in Sales Taxation: Critical Issues in Tax Policy and Administration (Westport, CT: Praeger Publishers, 1992), 69-70.

[35] Joseph Bishop-Henchman, “D.C. Council to Vote on Tax Reform Package Today,” Tax Foundation Blog, June 24, 2014, https://taxfoundation.org/dc-council-vote-tax-reform-package-today/.

[36] Due and Mikesell, Sales Taxation, 1983, 67.

[37] Scott Drenkard, “Overreaching on Obesity: Governments Consider New Taxes on Soda and Candy,” Tax Foundation, October 31, 2011, https://taxfoundation.org/overreaching-obesity-governments-consider-new-taxes-soda-and-candy/.

[38] New Jersey Division of Taxation, “New Jersey Sales Tax Guide: Bulletin S&U-4,” July 2017, 6, http://www.state.nj.us/treasury/taxation/pdf/pubs/sales/su4.pdf.

[39] Wisconsin Department of Revenue “Sales of Ice Cream Cakes and Similar Items,” November 8, 2010, https://www.revenue.wi.gov/Pages/TaxPro/news-2010-101108c.aspx.

[40] Situsing is the process for determining whether a transaction is taxable under a sales and use tax.

[41] Walter Hellerstein, “Sales Taxation of Services: An Overview of the Critical Issues,” in Sales Taxation: Critical Issues in Tax Policy and Administration (Westport, CT: Praeger Publishers, 1992), 45-46.

[42] Billy Hamilton and John L. Mikesell, “Sales Tax Policy During the Next Decade,” in Sales Taxation: Critical Issues in Tax Policy and Administration (Westport, CT: Praeger Publishers, 1992), 30.

[43] Patrick Fleenor and Andrew Chamberlain, “Tax Pyramiding: The Economic Consequences of Gross Receipts Taxes,” Tax Foundation, December 4, 2006, https://taxfoundation.org/tax-pyramiding-economic-consequences-gross-receipts-taxes/.

[44] Nicole Kaeding, “Yes, Really. Measure 97 Would Raise Prices,” Tax Foundation, July 28, 2016, https://taxfoundation.org/yes-really-initiative-petition-28-would-raise-prices/.

[45] For more reading on gross receipts taxes, see https://taxfoundation.org/state-tax/gross-receipts-and-margin-taxes/.

[46] Council on State Taxation and EY, “Total State and Local Business Taxes: State-by-State Estimates for Fiscal Year 2015,” Council on State Taxation, December 2016, http://www.cost.org/globalassets/cost/state-tax-resources-pdf-pages/cost-studies-articles-reports/fy15-state-and-local-business-tax-burden-study.pdf.

[47] Due and Mikesell, Sales Taxation, 1983, 89.

[48] Jessica Hathaway, “Tax Credits for Working Families: Earned Income Tax Credit (EITC),” National Council of State Legislatures (NCSL), April 5, 2017, http://www.ncsl.org/research/labor-and-employment/earned-income-tax-credits-for-working-families.aspx.

[49] Idaho Code, 63-3024A.

[50] Oklahoma Tax Commission, State of Oklahoma, “Tax ExpenditureTax expenditures are a departure from the “normal” tax code that lower the tax burden of individuals or businesses, through an exemption, deduction, credit, or preferential rate. Expenditures can result in significant revenue losses to the government and include provisions such as the earned income tax credit (EITC), child tax credit (CTC), deduction for employer health-care contributions, and tax-advantaged savings plans. Report 2015-2016,” 18, https://www.ok.gov/tax/documents/Tax%20Expenditure%20Report%202015-2016.pdf. The $50,000 income level also applies to those over the age of 65 or with a disability.

[51] Hamilton and Mikesell, “Sales Tax Policy During the Next Decade,” 34.

[52] Rebecca DeNale and Deanna Weidenhamer, “Quarterly Retail E-Commerce Sales 4th Quarter 2016,” U.S. Census Bureau News, February 17, 2017, https://www2.census.gov/retail/releases/historical/ecomm/16q4.pdf.

[53] Donald Bruce, William F. Fox, and LeAnn Luna, “State and Local Government Tax Revenue Losses from Electronic Commerce,” The University of Tennessee, April 13, 2009, http://cber.utk.edu/ecomm/ecom0409.pdf.

[54] Nicole Kaeding, Scott Drenkard, Jeremy Horpedahl, Joseph Bishop-Henchman, and Jared Walczak, “Arkansas: The Road Map to Tax Reform,” Tax Foundation, November 2016, 74-77, https://taxfoundation.org/arkansas-road-map-tax-reform/.

[55] Chris Isidore, “Amazon to start collecting state sales taxes everywhere,” CNN.com, March 29, 2017, http://money.cnn.com/2017/03/29/technology/amazon-sales-tax/index.html.

Share this article