The IRS has released tax data covering the first 30 weeks of the tax season, providing a glimpse of how individual taxpayers fared in 2019, the second taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. year under the Tax Cuts and Jobs Act (TCJA). The preliminary data provides aggregate information by income group on a range of topics, including sources of income as well as deductions and credits taken by taxpayers.

It is important to note that this data represents about 95 percent of filers and excludes those that requested a six-month filing extension. For this reason, the data represents about 82 percent of total tax liability that will be reported on individual income tax returns filed for tax year 2019.

In a previous piece, we outlined how the TCJA reduced effective tax rates and increased use of the standard deduction, among other changes, for all income groups in 2018 compared to 2017. When we account for the 2019 data, a similar trend emerges.

Tax Liability

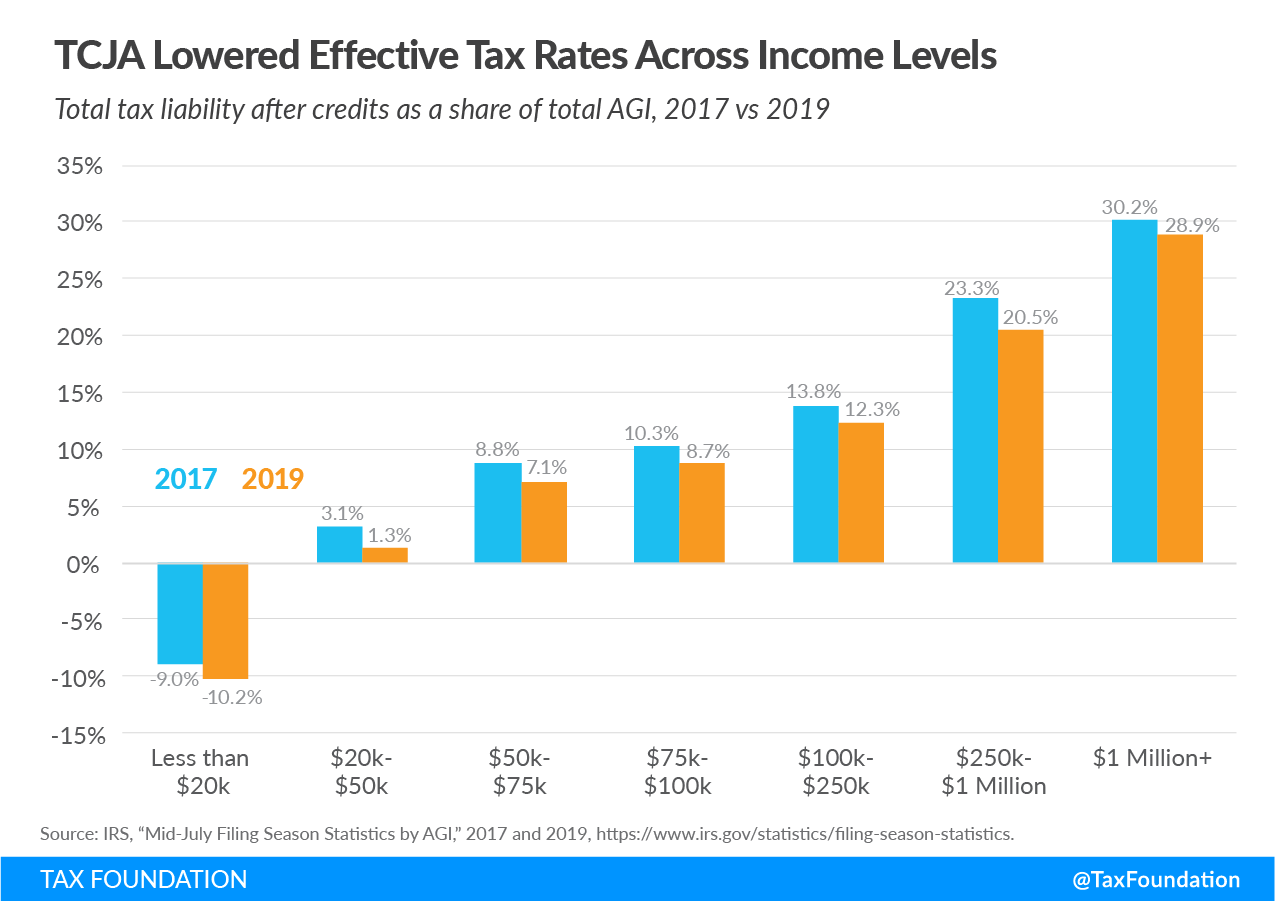

As illustrated below, the TCJA reduced effective tax rates, or total tax liability divided by an income group’s total adjusted gross incomeFor individuals, gross income is the total of all income received from any source before taxes or deductions. It includes wages, salaries, tips, interest, dividends, capital gains, rental income, alimony, pensions, and other forms of income. For businesses, gross income (or gross profit) is the sum of total receipts or sales minus the cost of goods sold (COGS)—the direct costs of producing goods, for all filing groups in 2019 compared to 2017. Even though taxpayers in each income group saw a tax cut on average, individual circumstances vary.

Taxpayers making less than $20,000 experienced negative effective tax rates due to refundable tax credits including the Additional Child Tax Credit (ACTC) and Earned Income Tax Credit (EITC). Refundable tax credits allow taxpayers to receive a refund from the government when the amount of credit they are owed surpasses their tax liability.

Filing Methods

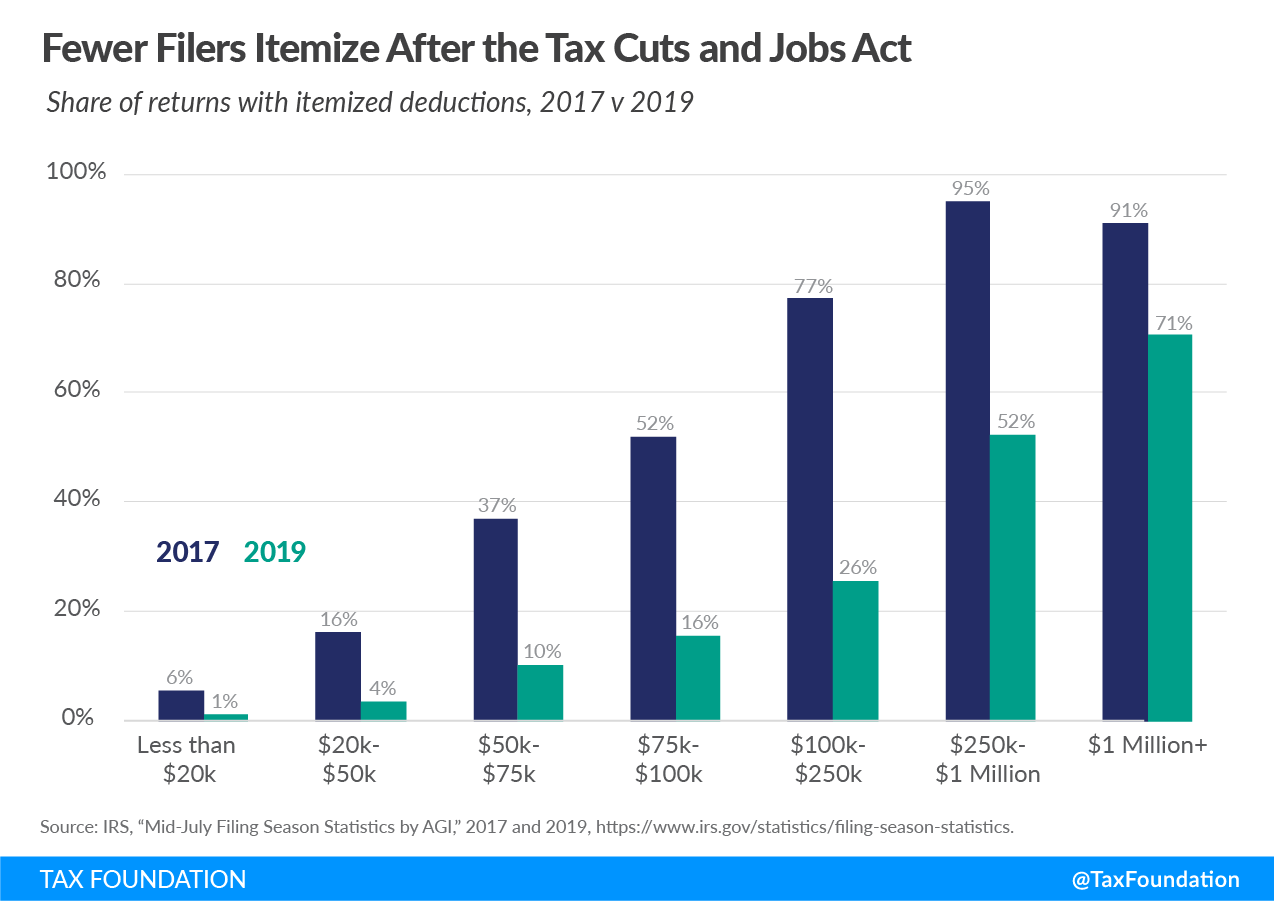

One of the most significant changes introduced by the TCJA was the expansion of the standard deductionThe standard deduction reduces a taxpayer’s taxable income by a set amount determined by the government. Taxpayers who take the standard deduction cannot also itemize their deductions; it serves as an alternative.. The TCJA also directly limited or eliminated a number of itemized deductions. As the chart below shows, the share of taxpayers who itemized went down across income levels. According to the returns filed through the first 30 weeks of the year, 9.6 percent of filers chose to itemize their deductions on their 2019 tax returns.

Tax Returns and Withholding

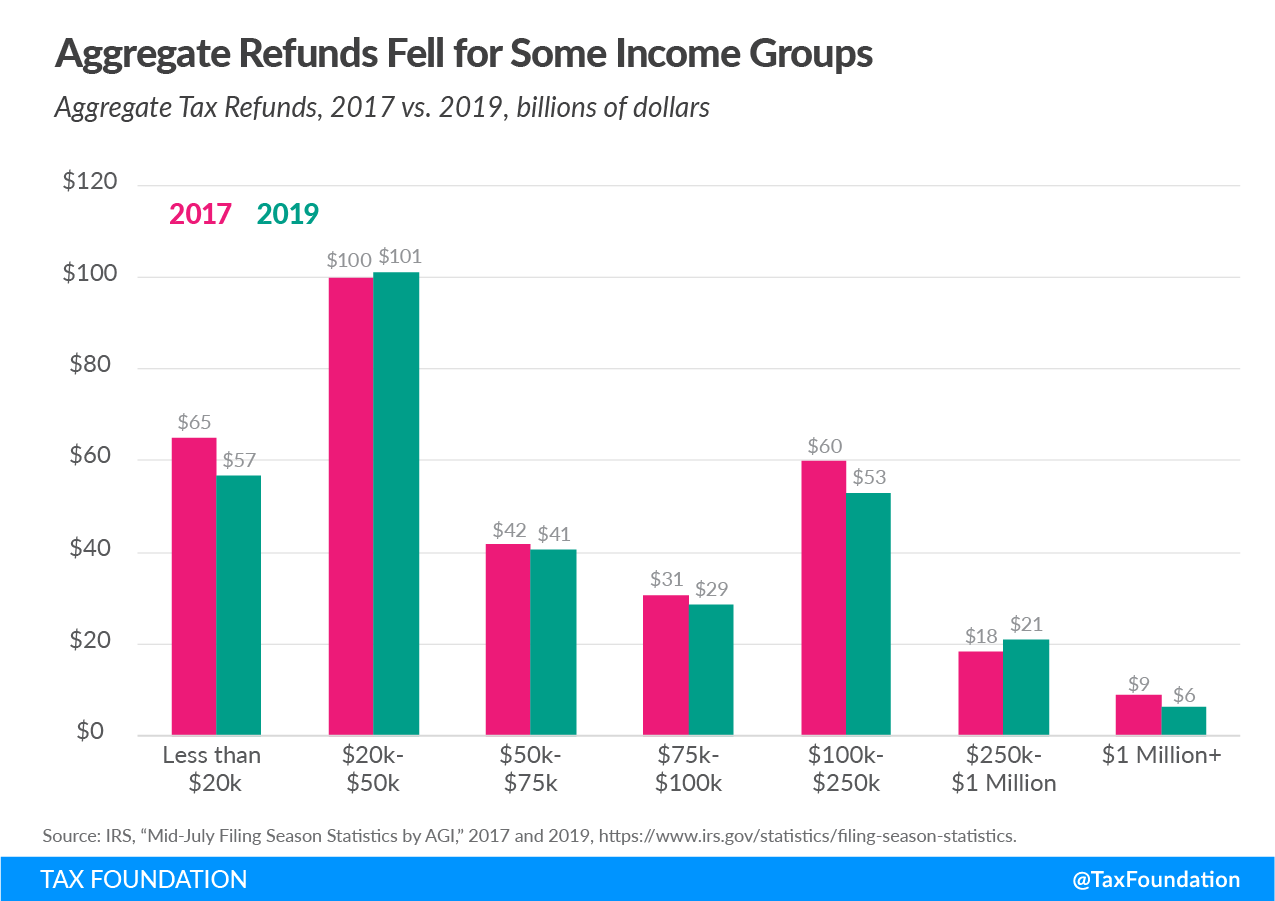

Tax filing season brings up many questions for taxpayers, such as, “How big will my tax refund be?” or, “Will I have a balance due when I file taxes this year?” Changes to withholdingWithholding is the income an employer takes out of an employee’s paycheck and remits to the federal, state, and/or local government. It is calculated based on the amount of income earned, the taxpayer’s filing status, the number of allowances claimed, and any additional amount the employee requests. tables in the aftermath of the TCJA resulted in lower-than-expected refunds, but it is important to remember that decreased tax refunds do not necessarily translate to increased tax liabilities.

The chart below shows the aggregate amount of refunds returned to taxpayers in each income group through the 30th week of the filing season in 2017 and 2019. While total refunds in 2019 fell for some income groups relative to 2017, effective tax rates dropped across all income groups over the same period. This pattern is similar to tax year 2018, when aggregate refunds also fell for most income groups.

Child Tax CreditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income rather than the taxpayer’s tax bill directly.

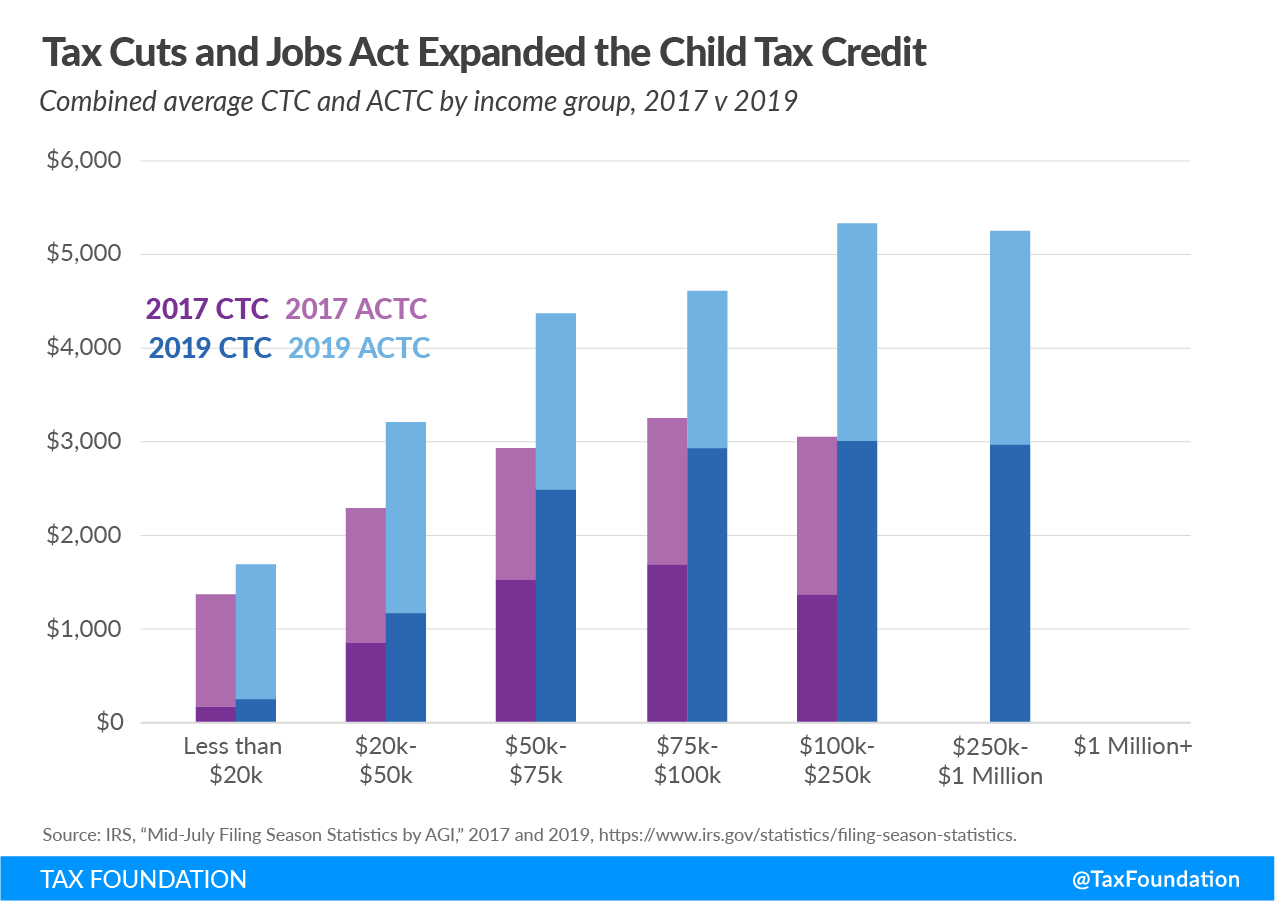

The TCJA increased what parents receive from the Child Tax Credit (CTC). The maximum credit amount increased from $1,000 to $2,000 per child and the refundability threshold increased from $1,000 to $1,400. (The refundable portion of the CTC is referred to as the Additional Child Tax Credit (ACTC).) Additionally, the income level eligibility for the credit increased from $110,000 to $400,000 for married filers ($75,000 to $200,000 for single filers) while the earned income threshold for the ACTC decreased from $3,000 to $2,500. Overall, these changes meant that more filers were eligible for a larger credit.

As shown in the chart below, the average combined benefit from the CTC and ACTC rose across all income groups (excluding higher earners who are ineligible for the credit) from 2017 to 2019. Due to the higher income phaseouts, high-income taxpayers saw significantly greater benefits from the credit in 2019 than in 2017. This change and the larger standard deduction helped offset the effects of suspending the personal exemption within the individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source.

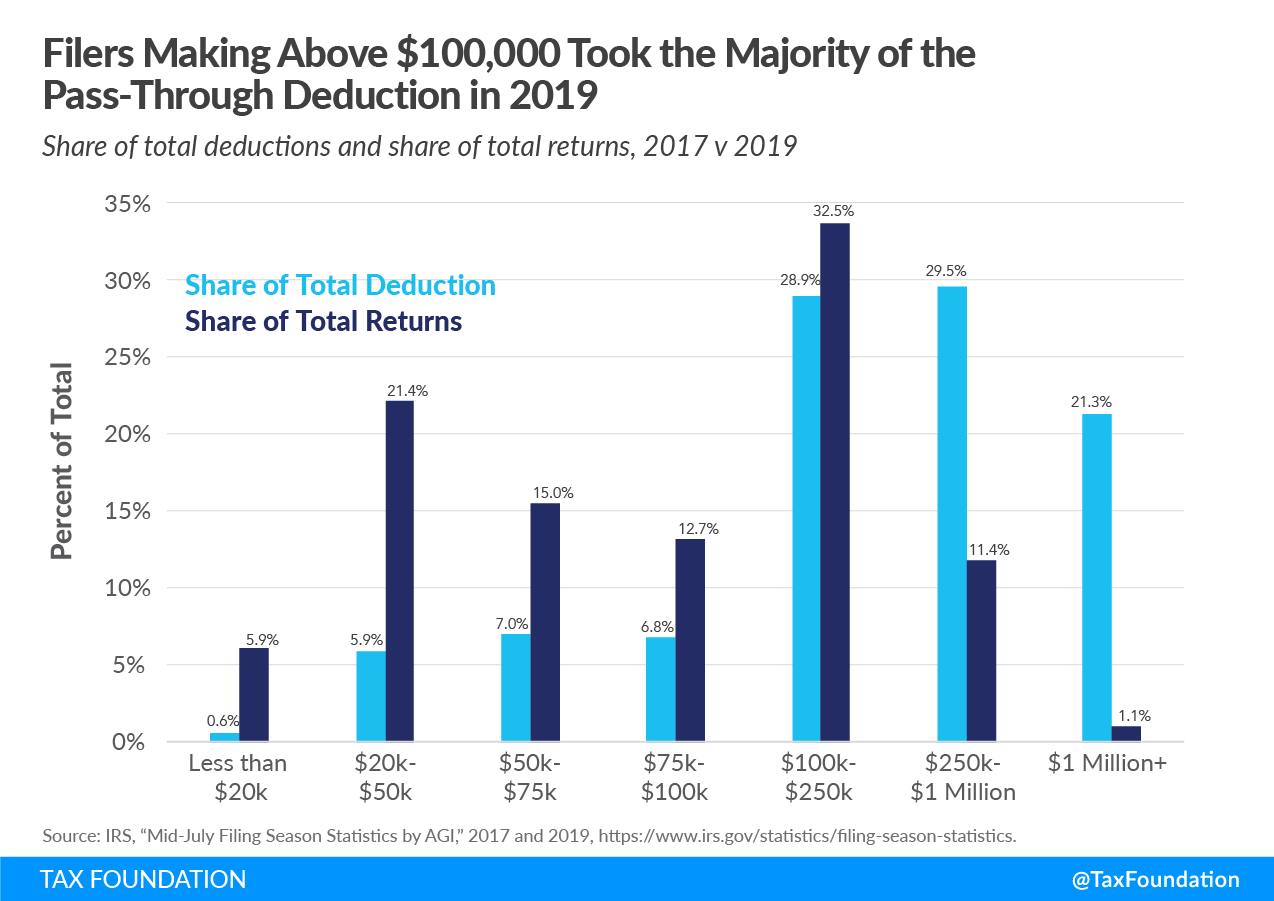

Section 199A Pass-through Deduction

The Tax Cuts and Jobs Act of 2017 created a deduction for households with income from pass-through businesses—companies such as partnerships, S corporations, and sole proprietorships, which are not subject to the corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax.. The pass-through deduction allows taxpayers to exclude up to 20 percent of their pass-through business income from federal income tax. Upper-income taxpayers are subject to several limits on the deduction, intended to prevent abuse, which are based on the economic sector of each business, the amount of business wages paid, and the original cost of business property.

As illustrated below, in tax year 2019, income groups of $100,000 and below accounted for 55 percent of the returns claiming the pass-through deduction, but only 20.3 percent of the benefits. Income groups above $100,000 accounted for 45 percent of returns claiming the pass-through deduction, but nearly 80 percent of the benefits.

Conclusion

The data continues to illustrate that the net effect of the Tax Cuts and Jobs Act was to reduce effective tax rates across income groups. In 2019, the TCJA again expanded the use of several deductions and credits, made the standard deduction more favorable than itemizing, and lowered taxes for most taxpayers.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

Subscribe