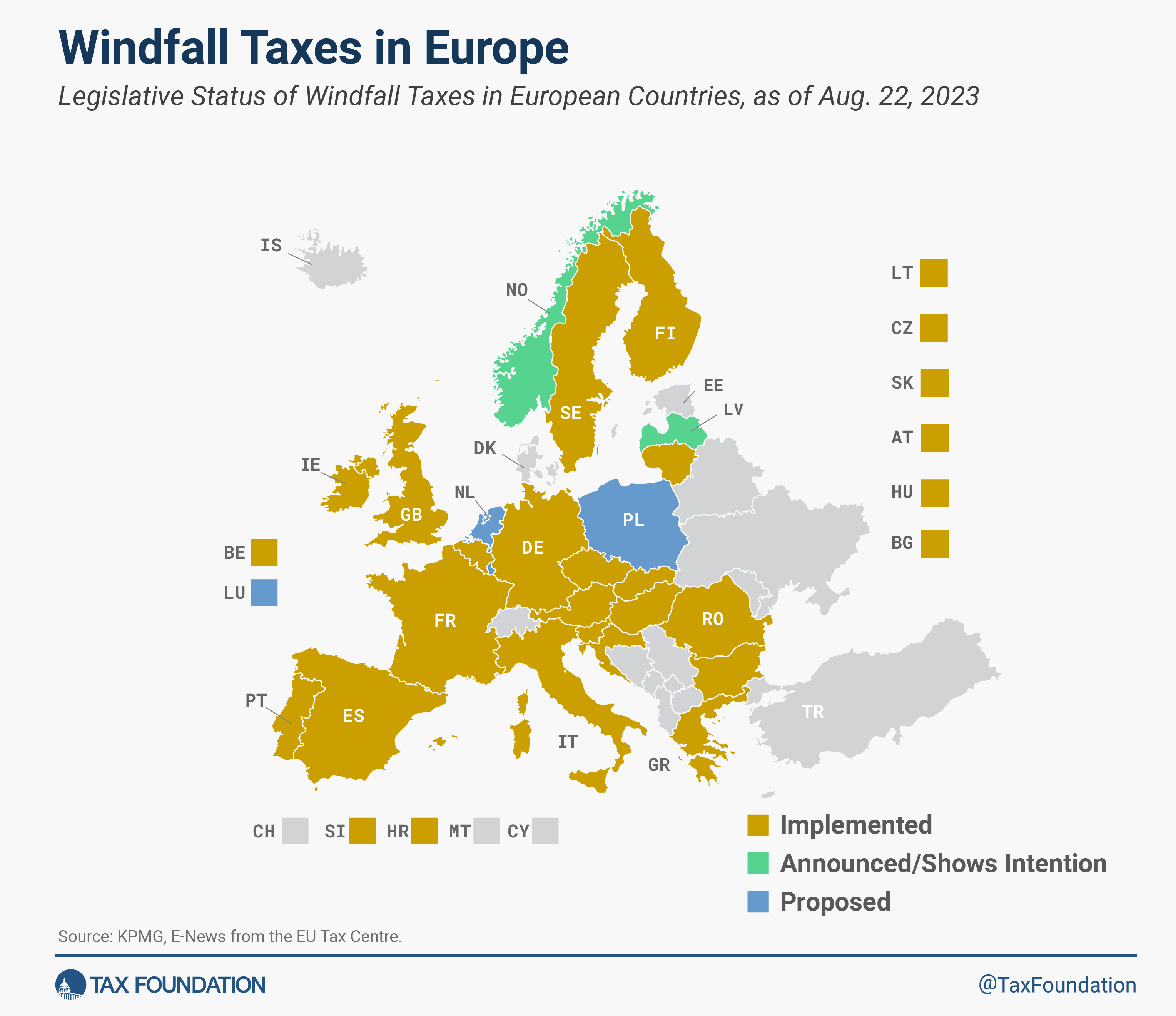

As energy prices have declined, European countries have switched the focus of their windfall profits taxes—a one-time taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. levied on a company or industry when economic conditions result in large, unexpected profits—from energy providers to the banking and financial sector.

As early as March 2022, the European Commission recommended that Member States temporarily impose windfall profits taxes on all energy providers in its REPowerEU communication. The Commission suggested such measures should be technologically neutral, not retroactive, and designed in a way that does not affect wholesale electricity prices or long-term price trends. In October 2022, the Council of the European Union agreed to impose an EU-wide windfall profits taxA windfall profits tax is a one-time surtax levied on a company or industry when economic conditions result in large and unexpected profits. Historically, such taxes have targeted oil and energy companies when costs have risen, especially from war or other crises., or “solidarity contribution,” on fossil fuel companies (oil, gas, coal, and refining sectors), though with a different design than the Commission’s recommendations. At the same time, a cap was set on market revenues for electricity generators that use infra-marginal technologies to produce electricity, such as renewables, nuclear, and lignite.

The EU anticipated that the two policies would jointly raise about €140 billion, of which €25 billion would be revenues from oil and gas companies collected through the solidarity contribution. The revenue would then be used to partially offset households’ high energy bills “in a non-selective and transparent measure supporting all final consumers.”

According to the 2025 European Commission report on the solidarity contribution, between 2022 and 2023, 16 of the 27 Member States applied the solidarity contribution, while eight adopted an equivalent national measure. Three countries—Luxembourg, Latvia, and Malta—reported that they do not have in-scope companies. Although the revenue collected for fiscal years 2022 and 2023—€26.15 billion—slightly exceeds the €25 billion estimate, the figures show notable discrepancies. Apart from the three countries that reported no companies in scope, three others—Finland, Lithuania, and Sweden—reported, for now, zero revenues from this policy to the European Commission, and there is no other data publicly available. Cyprus never adopted the regulation. Additionally, since Croatia applied the windfall tax to all sectors in the economy, it hasn’t reported any revenues from this policy specifically.

Therefore, out of the 27 EU Member States, only 19 have revenue data available on the solidarity contribution or an equivalent measure. Furthermore, the Commission's report reveals that the revenues from the solidarity contribution accounted for just 7 percent of the total cost of the energy support measures implemented by Member States, which amounted to €340 billion.

Although no longer a part of the EU, in 2022, the British government also implemented a windfall profits tax that exclusively targets companies engaged in oil and gas extraction.

As energy prices have declined and capital costs have risen, however, the profits of oil, gas, and coal sectors have dropped as well. In response, some countries have begun shifting the scope of the windfall tax from energy producers or oil and gas companies to the banking and financial sector. Currently, the Czech Republic, Hungary, Lithuania, Romania, Slovakia, and Spain have extended the scope of the windfall profits taxes to cover these sectors.

The windfall taxes in Europe differ significantly in their structures and their tax rates (ranging from 2 percent in Romania to 60 percent in the Czech Republic and Lithuania).

2025 Data

2024

2023

2022

Expand or Collapse Table

Windfall Profits Taxes in Force in European Countries, as of 1 September 2025

| Country | Tax Rate | Scope | Base | Status |

|---|---|---|---|---|

| Czech Republic | 60% | Companies in the energy and fossil fuel sectors with a total annual turnover in 2021 of at least CZK 2 billion (EUR 82 million) and a current total annual net turnover of at least CZK 50 million (EUR 2 million). | Profit margin exceeding 120% of the average profit of 2018, 2019, 2020, and 2021. | In Force (Applicable for three years: 2023, 2024, and 2025. Currently, there is a proposal in the 2026 budget that would substitute the banking tax with a 30 percent CIT rate on the banking sector). |

| Banks with a current net interest income of at least CZK 50 million (EUR 2 million) and a net interest income in 2021 of at least CZK 6 billion (EUR 246 million). | ||||

| Hungary | 18% | Credit and financial institutions | Up to the taxable amount of HUF 20 billion (EUR 51 million), a 7 percent tax applies, while an 18 percent rate will apply on the excess. | In Force (The first one was introduced as early as 1 July 2022; most were applicable for three years: 2022, 2023, and 2024. While windfall taxes on telecommunications companies, pharmaceutical companies, airlines, and energy suppliers ended in 2024, the bank tax stays in effect through 2025). |

| Lithuania | 60% | Credit institutions | 50% of the net interest income (interest income minus interest expenses) that exceeds the average net interest income of the previous four years. | In Force (Applicable initially for two years, 2023 and 2024, the tax has been extended through2025). |

| Poland | Proposed (On August 13, 2025, the Minister of Finance and Economy announced that the government will soon present the framework for new legislation introducing a tax on windfall profits in the banking sector. The Minister indicated that the revenues from this source could reach PLN 1.5-2 billion in 2026. | |||

| Romania | 2% | Banks | Net revenue. | In Force (Introduced for two years, 2024 and 2025. The tax will become permanent in 2026, when the rate will drop to 2%). |

| Slovakia | 30% | Banks | Banking profits. The windfall tax, together with the regular corporate tax, will raise the effective tax rate for the banking sector to 45% in 2024. By 2027, the effective tax rate will drop to 33% since the tax rate will be cut by 5 percentage points per year between 2025 and 2027. | In Force (Applicable for four years from 2024 to 2027. The tax rate will be cut by 5 percentage points per year to 15% in 2027). |

| Spain | 3.5% to 7% | Financial institutions | Bank’s net interest income and net fees if the net income from these sources exceeded EUR 750 million. Financial institutions with a taxable base between EUR 750 million and EUR 1.5 billion will be subject to a 3.5% tax rate, while those with up to EUR 3 billion of qualifying income will pay tax at 4.8%. Banks with up to EUR 5 billion of net interest income and fees will pay a 6% tax, while financial institutions with amounts over that threshold will be subject to tax at 7%. The tax enacted in December 2024 includes a special deduction aimed at supporting banks with low profitability. | In Force (In December 2022, two windfall taxes on the banking sector and energy companies were approved. Applicable for two years: 2023 and 2024. As of December 2024, the windfall tax on the banking sector was extended through the 2026 fiscal year. Previously, in September 2021, Spain approved a temporary mechanism that was in force until 31 December 2022. The mechanism consisted of a temporary reduction in the remuneration of electricity production activities to reduce windfall profits earned due to higher gas and carbon prices. The tax was payable if the gas price was higher than EUR 20/MWh. However, later on, a series of exclusions were approved, and many energy providers were left outside the scope of the mechanism). |

| United Kingdom | 38% (35% up to 1 November 2024) | Oil and gas companies operating in the UK and the UK Continental Shelf. | On the same profits that are already subject to the UK’s oil and gas 40% headline tax, generating an effective tax rate of 78%. | In Force (Approved on 11 July 2022, applicable to profits generated on or after 26 May 2022, up to 31 March 2030. Jeremy Hunt raised the tax from 25% to 35% in January 2023 and, in the 2024 budget announcement, stated that it would remain in place until March 2029. However, with the new labor government, the tax was extended for one more year to March 2030 and the rate was increased to 38% starting from 1 November 2024). |

Data compiled by Cristina Enache

Additionally, many of the proposed and enacted measures are not proper windfall profits taxes—they go beyond merely taxing windfall profits. For oil and gas companies, European countries followed the windfall tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. definition from the EU’s regulation as the difference between the current profits and the profits generated over a baseline period. Nevertheless, these incremental profits are not necessarily excess or supernormal returns, and a windfall tax could translate into double taxationDouble taxation is when taxes are paid twice on the same dollar of income, regardless of whether that’s corporate or individual income. of regular profits.

In some countries with windfall taxes, the tax base is not designed in a way that exclusively captures the windfall profits generated by the spikes in energy and oil prices. A tax on electricity sold over an arbitrarily determined price (as most European countries implemented) or on total sales (as in Spain) resembles more of an excise taxAn excise tax is a tax imposed on a specific good or activity. Excise taxes are commonly levied on cigarettes, alcoholic beverages, soda, gasoline, insurance premiums, amusement activities, and betting, and typically make up a relatively small and volatile portion of state and local and, to a lesser extent, federal tax collections..

In the banking sector, the windfall tax not only reduces the amount of available capital but also restricts banks’ capacity to respond to an unforeseeable financial crisis. It might also scare bank investors, thus raising the cost of capital and hindering long-term economic growth. Additionally, in the event of a recessionA recession is a significant and sustained decline in the economy. Typically, a recession lasts longer than six months, but recovery from a recession can take a few years., a rise in loan defaults would negatively impact bank profits. The European Central Bank (ECB) objected to Spain's, Lithuania's, and Italy's windfall taxes on banks as they could reduce credit supply and banks’ resilience in an economic downturn.

Although the EU regulation clearly states that windfall profits taxes should be a temporary mechanism, and “the duration of the measure should be limited and tied to a specific crisis situation,” the Czech Republic, Hungary, and Lithuania have extended it until 2025, Spain has extended it until 2026, and Slovakia has extended it until 2027. The United Kingdom, which implemented a windfall profits tax on fossil fuel companies in 2022, extended its application to 2030, and Romania’s windfall tax on banks was made permanent. The other countries terminated the tax as planned.

The flawed design of these windfall profits taxes has created problems in countries that implemented them. European Parliament research finds that, historically, windfall taxes have negatively affected investment. Additionally, the Spanish and British taxes have threatened and continue to threaten domestic renewable energy investments.

While some of these windfall taxes have achieved their revenue goals, they have distorted the market by penalizing domestic production, reducing investment in green energy, and punitively targeting certain industries without a sound tax base. Policymakers should consider repealing windfall taxes altogether and instead focus on principled tax policy reforms that generate stable revenue over time.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

SubscribeAbout the Author

Cristina Enache writes on the economics of tax policy and is the author of the Spanish Regional Tax Competitiveness Index. She was formerly the Director of Research at Civismo, an economic research organization based in Spain. She also served as head of research at Institución Futuro, a regional think tank based in Navarra in northern Spain. She is also currently Secretary-General at the World Taxpayers Associations and General Manager of the Spanish Taxpayers Union, which she joined in 2016.