Windfall Profit Taxes in Europe, 2022

9 min readBy:As energy prices continue to rise, more European countries have been looking at windfall profit taxes—a one-time taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. levied on a company or industry when economic conditions result in large, unexpected profits—to fund relief measures for consumers. As early as March 8, the European Commission recommended in its REPowerEU communication that member states temporarily impose windfall taxes on all energy providers. The Commission suggested such measures be technologically neutral, not retroactive, and designed in a way that doesn’t affect wholesale electricity prices and long-term price trends.

According to statistics from the International Energy Agency, the Commission estimated these measures could yield up to €200 billion in 2022. The revenue could then be used to partially offset households’ high energy bills “in a non-selective and transparent measure supporting all final consumers.”

Countries like Romania and Spain already implemented a temporary mechanism in 2021 to cut excess revenues of energy companies that benefit from higher energy and gas wholesale prices.

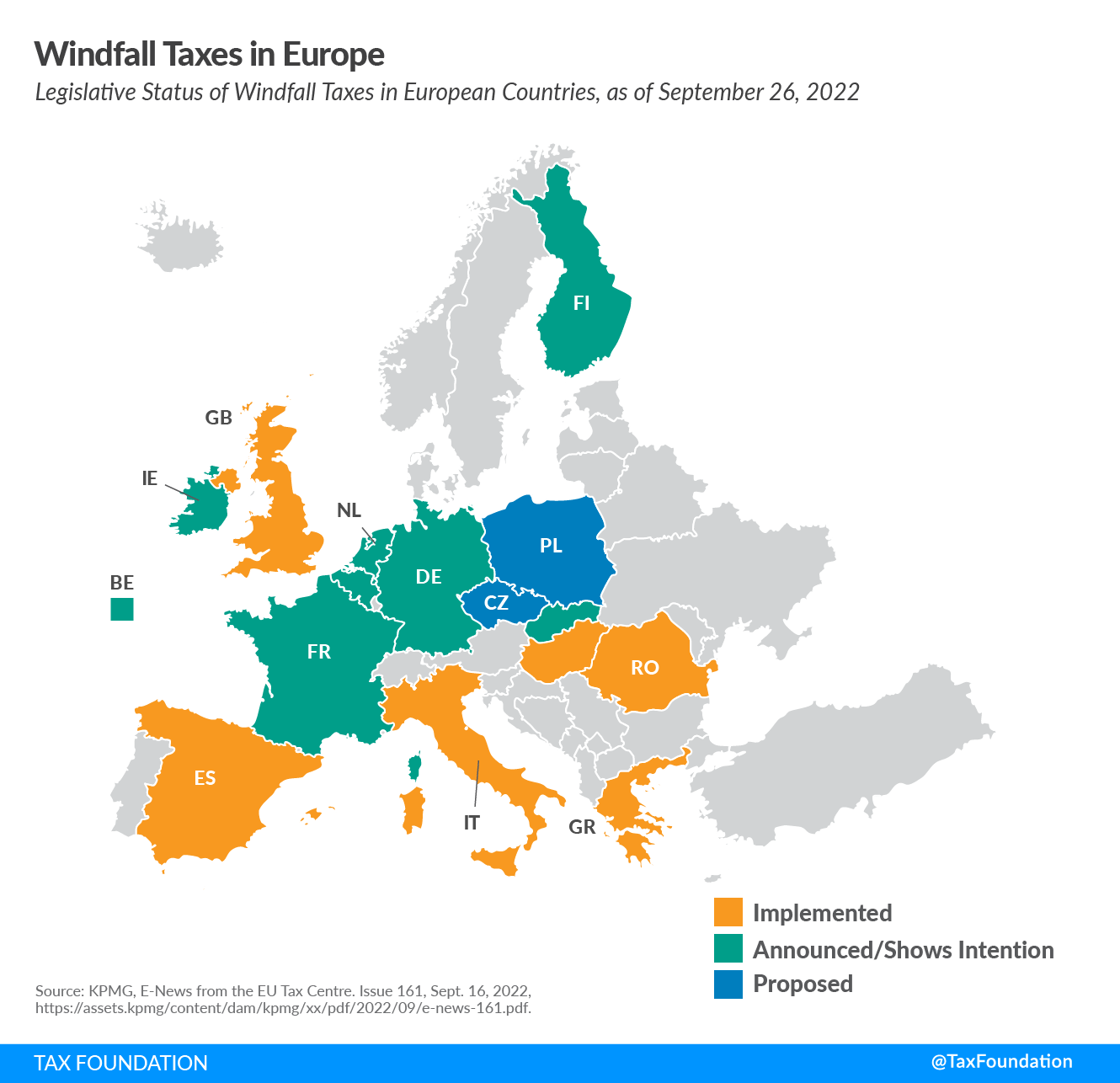

Six months after the Commission’s recommendation and continued energy price increases, 15 European countries have either announced, proposed, or implemented windfall profit taxes.

Greece, Hungary, Italy, Romania, Spain, and the United Kingdom have implemented a windfall tax. The Czech Republic and Poland have published proposals to enact a windfall tax and Spain published a proposal to enact a second windfall tax because the first one was diluted by a series of exclusions that left many energy providers out of its scope. Belgium, Finland, Germany, Ireland, Netherlands, and Slovakia have either officially announced or shown intentions to implement a windfall tax. France is, for now, the only country that voted down a windfall tax proposal.

The proposed and implemented windfall taxes differ significantly in their tax rates (e.g., Greece’s is up to 90 percent) and their structures. Additionally, many of the proposed and enacted measures are not proper windfall profit taxes—they go beyond merely taxing windfall profits.

In most countries with windfall taxes, the tax base is not designed in a way that exclusively captures the windfall profits generated by the spikes in energy and oil prices. In Romania and Spain, for instance, a tax on electricity sold over an arbitrarily determined price or on total sales is not a tax on profits at all—it resembles more of an excise tax. On the other hand, Italy’s windfall profit tax (the Incremental Added-Value) could be influenced by a variety of factors, including mergers and acquisitions, which are not linked to price changes.

In other countries, the tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. is calculated as the difference between the current profits and the profits generated over a baseline period. Nevertheless, these incremental profits are not necessarily excess or supernormal returns and a windfall tax could translate into double taxation of regular profits.

The flawed design of these windfall profit taxes has already created problems in countries that implemented them. While the constitutionality of Italy’s windfall tax is questioned, the country hardly collected €2 billion out of the €11 billion expected revenue. In Poland, as companies are already struggling with higher energy costs, business associations warned that this measure would “lead to an uncontrolled wave of bankruptcies that will hit the Polish economy.” In Spain, after the announcement of a possible EU-wide windfall tax, the country’s government vowed to adjust the two new windfall tax proposals, already heavily criticized by the targeted sectors, to the EU design.

It’s unlikely these implemented and proposed windfall taxes will achieve their goals of addressing high gas and energy prices and raising additional revenues. They would more likely raise prices, penalize domestic production, and punitively target certain industries without a sound tax base. Although an EU-wide windfall tax is not a good option, it does not have as many problems as the current proposed and implemented windfall profit taxes.

| Country | Tax Rate | Scope | Base | Status |

|---|---|---|---|---|

| Belgium (BE) | 38% | Nuclear plant | Profit margin from the exploitation of nuclear power stations. | Announced/Shows Intention (Extend windfall profit tax beyond existing nuclear levy paid annually by Engie’s and Electricite de France’s Belgian subsidiaries.) |

| Czech Republic (CZ) | 40%, 50%, or 60% | Electricity producers, the banking sector, and, possibly, fuel production and distribution companies. However, it will not apply to the sale of fuel to end consumers. | The difference between the current year’s tax base and the average tax base for the preceding five-year period. | Proposed (The government released a working paper to be used in negotiations and for drafting the bill. Not a retroactive tax; expected to be effective from 2023.) |

| Finland (FI) | Electric, gas, and oil companies. | Announced/Shows Intention (During the announcement of the 2023 budget proposal the Finance Minister showed his intention to impose a new windfall tax on certain energy companies. The budget proposal was supposed to be presented to the Finnish Parliament on September 19, 2022.) | ||

| France (FR) | Announced/Shows Intention (In July 2022 the National Assembly voted down a windfall tax proposal.) | |||

| Germany (DE) | Announced/Shows Intention (The Finance Minister pledges to reverse a mechanism that previously subsidized renewables via electricity bills while the ruling coalition backs the European Union proposal to tax windfall profits.) | |||

| Greece (GR) | 90% | Certain energy producers | The difference between the profit generated in a given month of the tax period and the profit for the corresponding month of the previous year (monthly basis). | Implemented (Introduced on May 2022; applies retroactively for the tax period between October 1, 2021, and June 30, 2022. It’s a one-time tax.) |

| Hungary (HU) | A variety of rates depending on the sector | Producers of petroleum products, renewable energy, pharmaceutical distributors, mining royalties, airline companies, credit, financial institutions, etc. | Varies by industry. | Implemented (Introduced on July 1, 2022; applicable to the 2021 and 2022 fiscal years, collected in 2022 and 2023.) |

| Ireland (IE) | Announced/Shows Intention (The Finance Ministry is working to quantify energy companies’ windfall gains to explore the potential of collecting a portion of these gains. Also, plans to implement the EU-wide measure if it works for Ireland.) | |||

| Italy (IT) | 25% | Importing, production, extraction, distribution, and sales of electricity, methane gas, natural gas, and oil products. Does not apply to companies organizing and managing platforms for the exchange of electricity, gas, environmental certificates, and fuels. | The difference between the added value for the period from October 1, 2021, to April 30, 2022, and the added value for the period from October 1, 2020, to April 30, 2021 (the incremental added value). The tax is not deductible for income tax purposes. | Implemented (Introduced on March 21, 2022. On May 2, 2022, the tax rate was increased from 10% to 25%. It’s a one-time tax.) |

| Netherlands (NL) | Companies extracting oil and gas. | Announced/Shows Intention (announced during the country’s budget day on September 20, 2022.) | ||

| Poland (PL) | 50% | All companies employing more than 250 people. | Profit margin exceeding the average profit of 2018, 2019, and 2020; banks would pay the levy based on ROA above the 3-year average. | Proposed (After discussion and governmental approval, the bill could be passed by the parliament in the following weeks.) |

| Romania (RO) | 80% | Energy producers, certain energy suppliers, and traders. | The average selling price of electricity in a month exceeds RON 450 (€91) per MWh; subject to certain exemptions. | Implemented (Applicable for the period from November 1, 2021, to March 31, 2022, and extended to March 31, 2023.) |

| Slovakia (SK) | 50% | Nuclear plants. | Announced/Shows Intention (In May 2022, plans to impose a 50% tax on profits from the sale of nuclear energy were dropped in exchange for a fixed electricity price.) | |

| Spain (ES) | 1.2% (energy companies) and 4.8% (banks) | Energy companies (gas, oil, and electricity) and banks | Sales of domestic power utilities (companies with an annual turnover exceeding €1 billion in 2019). Bank’s net interest income and net fees if the net income from these sources exceeded €800 million in 2019. | Implemented (In September 2021, Spain approved a temporal mechanism that is in force until December 31, 2022. The mechanism consists of a temporary reduction in the remuneration of electricity production activities to reduce windfall profits earned due to higher gas and carbon prices. The tax applies to facilities with a capacity of more than 10 MW and power plants not benefiting from public subsidies. The tax is payable if the gas price is higher than €20/MWh. The rate of the tax depends on the energy produced, the gas price, and the price of the energy produced by gas-powered plants. However, later on, a series of exclusions were approved and many energy providers were left outside the scope of the new mechanism. Proposed (In July 2022, the government submitted a new draft proposal with two new windfall taxes on the banking sector and energy companies. In September 2022, Spain vowed to adjust the new windfall tax if the EU proposal succeeds.) |

| United Kingdom (GB) | 25% | Oil and gas companies operating in the UK and the UK Continental Shelf | On the same profits that are already subject to the UK’s oil and gas 40 percent headline tax, generating an effective tax rate of 65 percent. However, the new legislation also introduces an “investment allowance” which, together with other reliefs already available, enables taxpayers to obtain relief of up to 91.25 pence in the pound when they reinvest profits in the UK oil and gas sector. | Implemented (Approved on July 11, 2022, applicable to profits generated on or after May 26, 2022, up to December 31, 2025. On September 8, 2022, the new Prime Minister announced that there will be no extension of the application of this previously introduced windfall profit tax.) |

| Sources:

KPMG, E-News from the EU Tax Centre. Issue 161, Sept. 16, 2022, https://assets.kpmg/content/dam/kpmg/xx/pdf/2022/09/e-news-161.pdf; KPMG, E-News from the EU Tax Centre, Issue 157, July 5, 2022, https://assets.kpmg/content/dam/kpmg/xx/pdf/2022/07/e-news-157.pdf; KPMG, “Czech Republic: Working paper on possible windfall tax,“ Sept. 13, 2022, https://danovky.cz/en/news/detail/1092; Bloomberg Tax, “French PM Leaves Door Open for Windfall Tax on ‘Super Profits’,” Aug. 28, 2022, https://news.bloombergtax.com/daily-tax-report-international/french-pm-leaves-door-open-for-windfall-tax-on-super-profits; Bloomberg Tax, “Germany Expects About $10 Billion From Energy Windfall Levy,” Sept. 14, 2022, https://news.bloombergtax.com/daily-tax-report-international/germany-expects-about-10-billion-from-energy-windfall-levy; Bloomberg Tax, “Dutch to Raise Wages, Corporate Tax to Ease Energy Crisis (2),” Sept.20, 2022, https://news.bloombergtax.com/daily-tax-report-international/dutch-present-16-billion-plan-to-ease-the-pain-of-energy-crisis; Bloomberg Tax, “Poland Proposes Windfall Tax Rate of 50%: Minister Sasin,” Sept. 25, 2022, https://news.bloombergtax.com/daily-tax-report-international/poland-proposes-windfall-tax-rate-of-50-minister-sasin; Bloomberg Tax, “Poland’s New Windfall Tax Could Affect All Large Companies: RP,” Sept. 26, 2022, https://news.bloombergtax.com/daily-tax-report-international/polands-new-windfall-tax-could-affect-all-large-companies-rp; Bloomberg Tax, “Slovakia to Drop Tax in Return for Fixed Electricity Price,” Feb. 16, 2022, https://news.bloombergtax.com/daily-tax-report/slovakia-to-drop-tax-in-return-for-fixed-electricity-price; Bloomberg Tax, “Belgium to Work Out Details of Energy Windfall Profit Taxation,” Aug.31, 2022, https://news.bloombergtax.com/daily-tax-report-international/belgium-to-work-out-details-of-energy-windfall-profit-taxation; Bloomberg Tax, “Spain Seeks 4.8% Tax on Banks To Beat Cost of Living Crisis (2),” July 28, 2022, https://news.bloombergtax.com/daily-tax-report-international/spain-seeks-4-8-tax-on-banks-to-counter-cost-of-living-crisis; PWC Hungary, “Government Decree on Extra-profit Tax,” July 1, 2022, https://www.pwc.com/hu/en/pressroom/2022/extra-profit.html; Taxnotes, “Ireland to Fund Cost-of-Living Package With Windfall Profits Tax,” Sept.23, 2022, https://www.taxnotes.com/tax-notes-today-international/individual-income-taxation/ireland-fund-cost-living-package-windfall-profits-tax/2022/09/23/7f61b; Taxnotes, “Italy Imposes 10 Percent Energy Windfall Profits Tax,” Mar. 22, 2022, https://www.taxnotes.com/tax-notes-today-international/corporate-taxation/italy-imposes-10-percent-energy-windfall-profits-tax/2022/03/22/7d9ff. |

||||

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

SubscribeAbout the Author

Cristina Enache writes on the economics of tax policy and is the author of the Spanish Regional Tax Competitiveness Index. She was formerly the Director of Research at Civismo, an economic research organization based in Spain. She also served as head of research at Institución Futuro, a regional think tank based in Navarra in northern Spain. She is also currently Secretary-General at the World Taxpayers Associations and General Manager of the Spanish Taxpayers Union, which she joined in 2016.