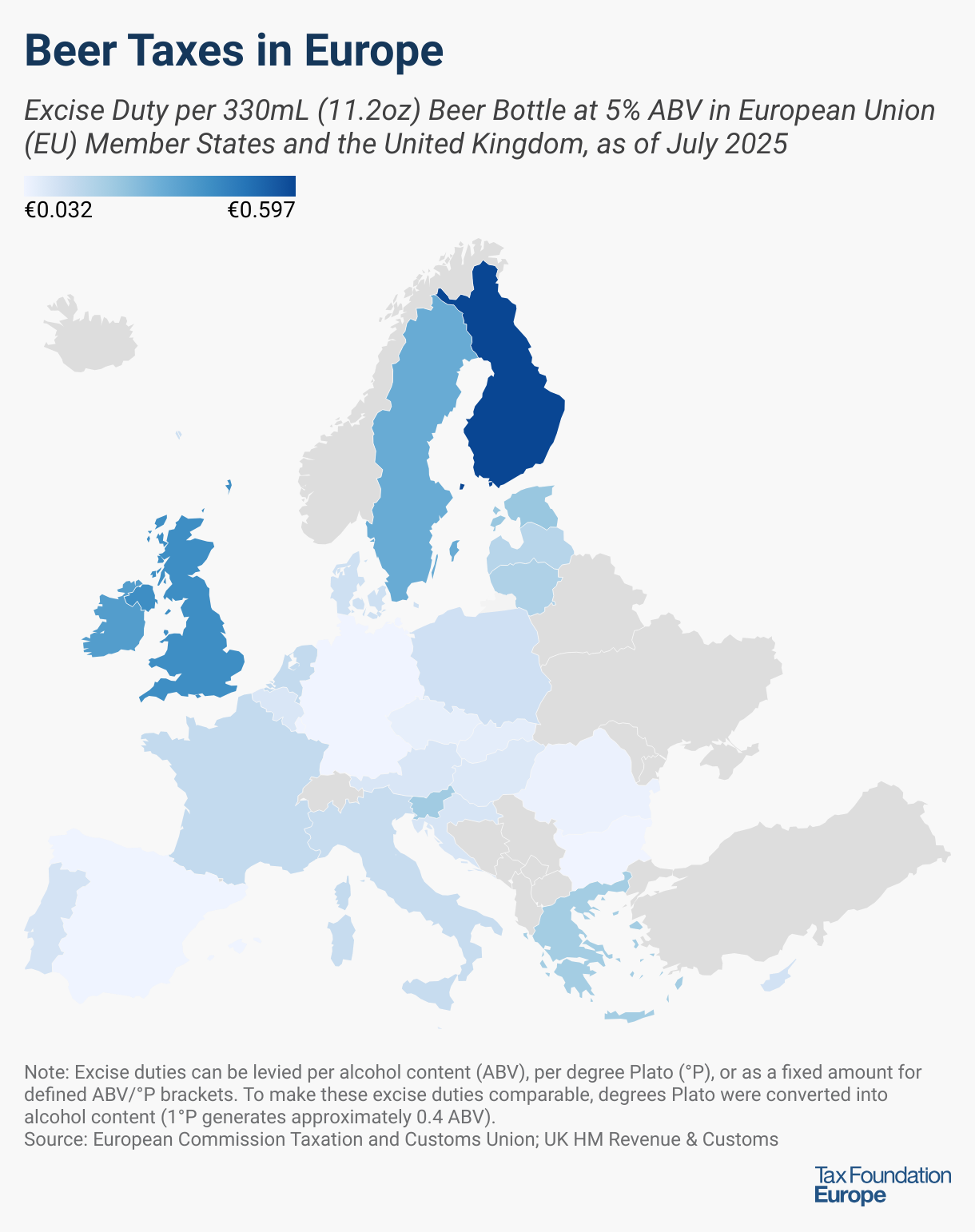

With much of the continent celebrating Oktoberfest, it is a great time to examine beer taxes across Europe. Hefty beer taxes increase the price consumers pay for their libations.

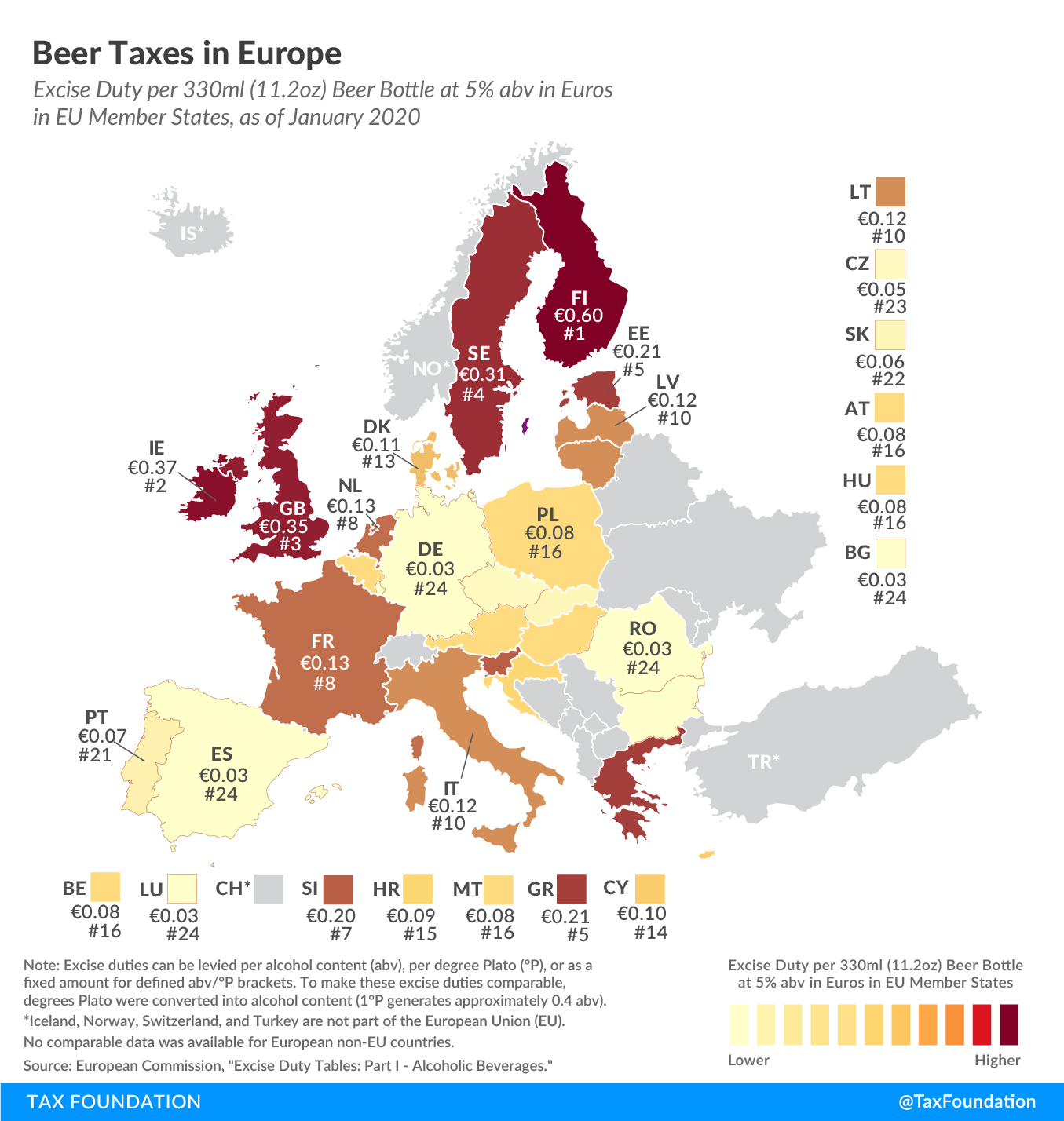

The EU requires Member States to levy an excise duty on beer of at least €1.87 per 100 liters (26.4 gallons) and degree of alcohol content. For a standard bottle of 330 mL (11.2 oz) of 5 percent alcohol content beer, this translates to a minimum taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. of €0.0309 ($0.0364). Only a few Member States remain near this minimum rate; most countries choose to levy much higher duties on beer.

Some countries vary their volume-based tax rate in proportion to alcohol content, and other countries set one rate for a range of alcohol content in beer. To allow for comparison, we convert the different rates to euros and apply those rates to a standard bottle of beer. EU countries also levy a value-added tax (VAT) as a percentage of the sales price, which is separate from the excise taxes and not included in the map.

The significant disparities in beer tax rates among EU Member States are representative of the wide range in the global tax treatment of alcohol. Finland levies the highest tax of €0.597 ($0.704) per 330 mL bottle of beer, followed by the United Kingdom at €0.419 ($0.494) and Ireland at €0.372 ($0.439). Bulgaria levies the lowest tax of €0.0316 ($0.0373) per bottle of beer, followed by Germany at €0.0325 ($0.0383) and Luxembourg at €0.0327 ($0.0386).

2025 Data

2024

2023

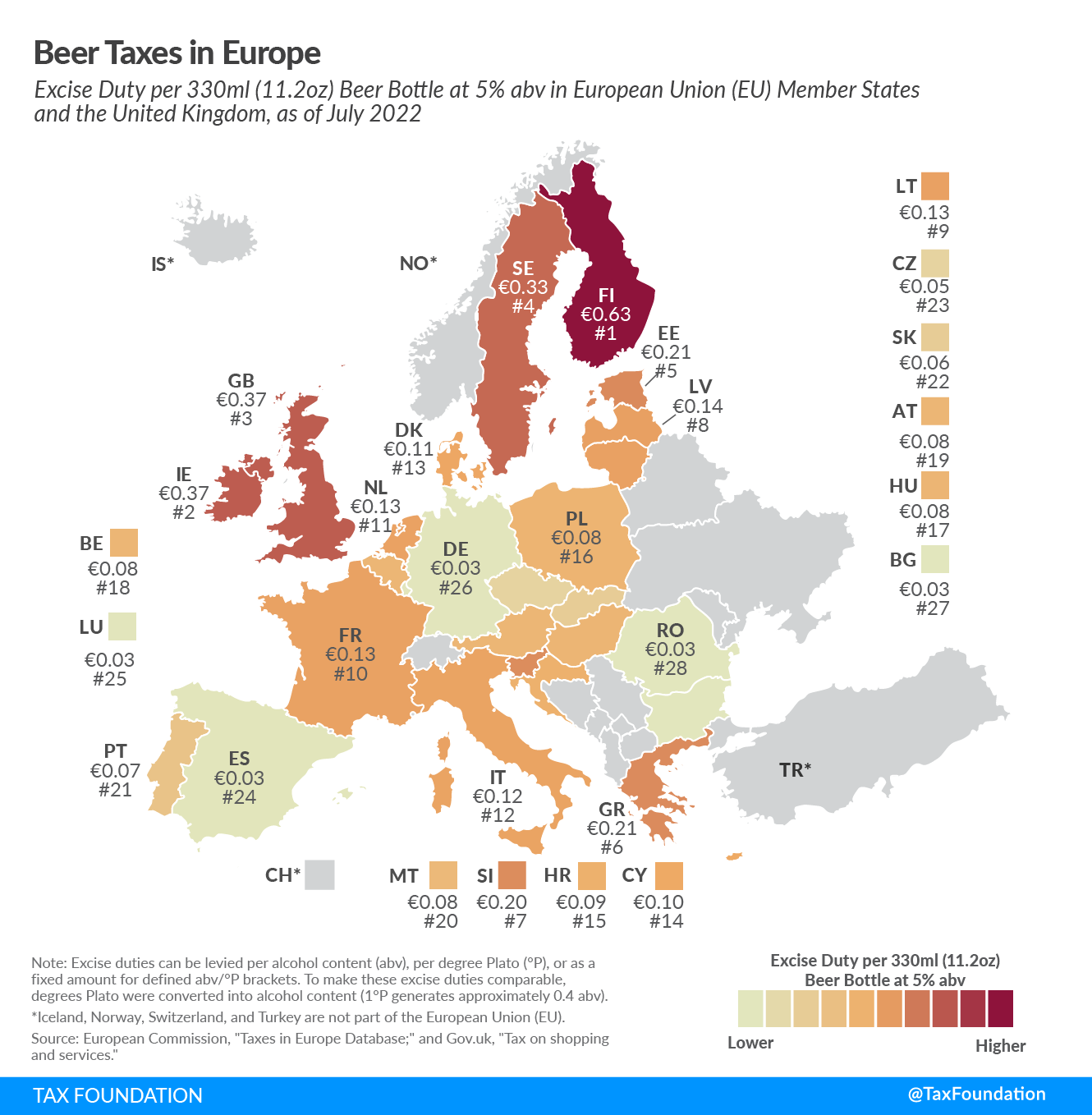

2022

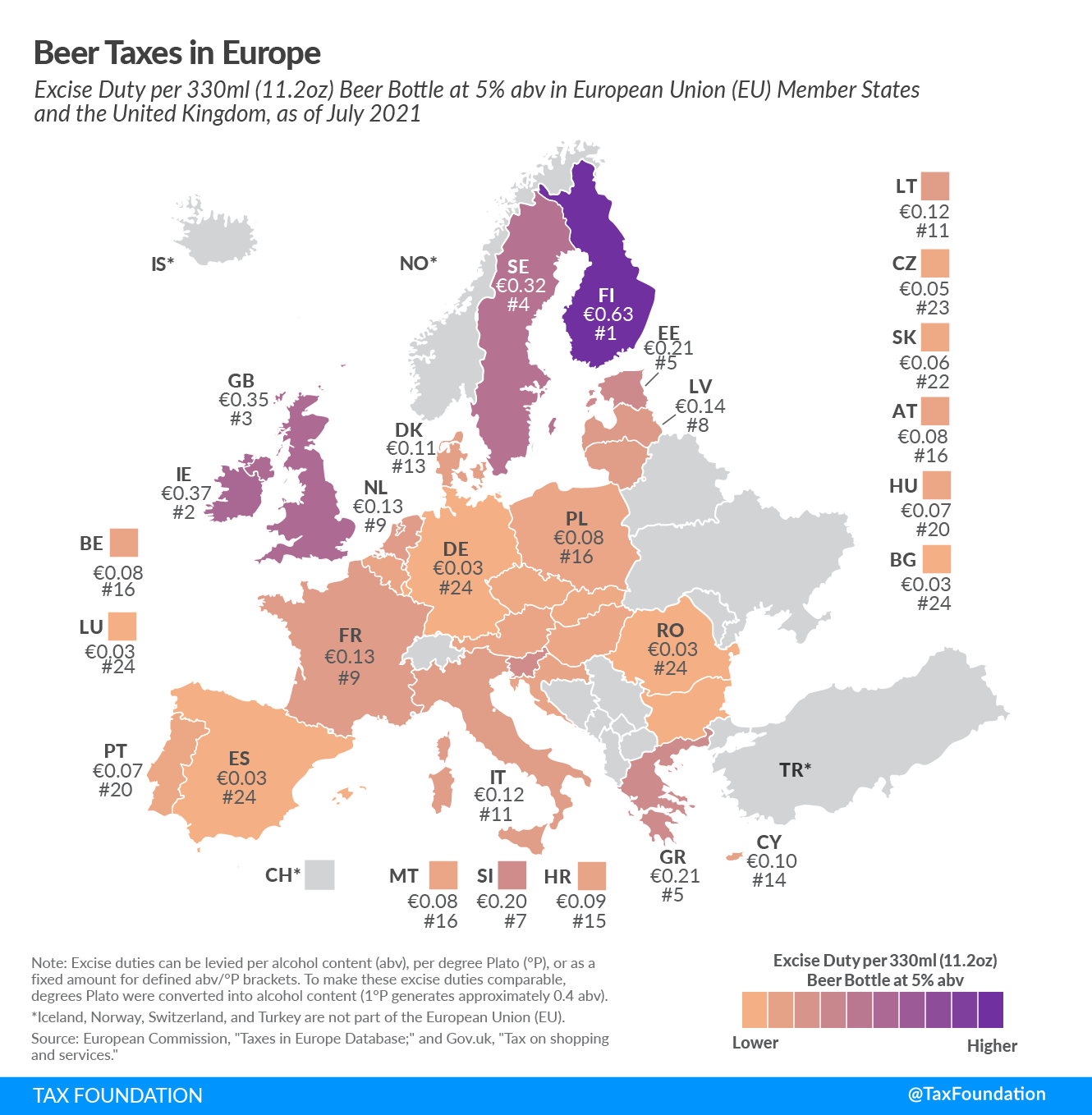

2021

2020

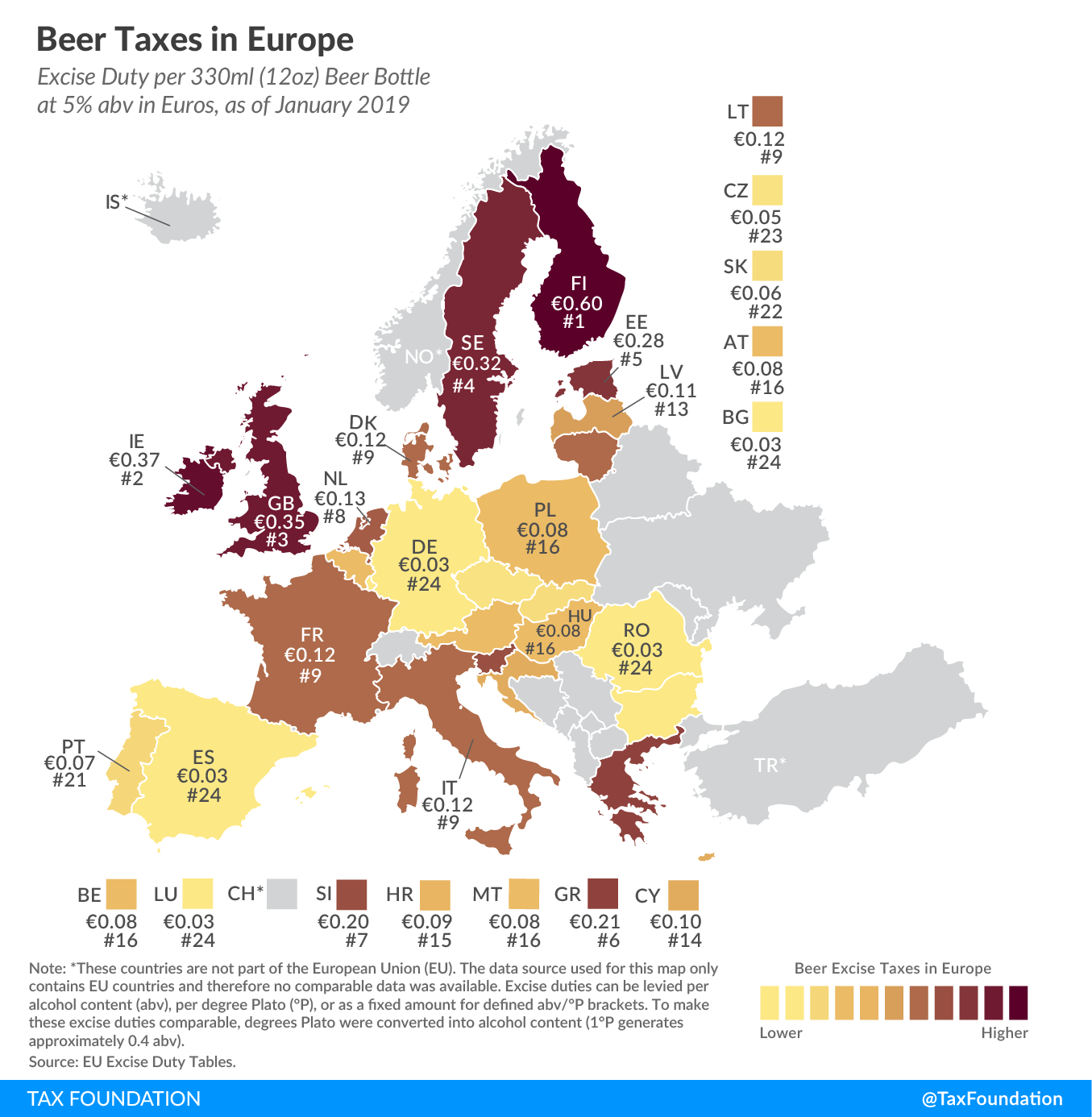

2019

Expand or Collapse Table

Beer Taxes in Europe, 2025

Excise Duty per 330ml (11.2oz) Beer Bottle at 5% abv in European Union (EU) Member States and the United Kingdom, as of July 2025

| Country | Excise Duty on 330 mL of 5% ABV Beer | Rank |

|---|---|---|

| Austria | € 0.0825 | 19 |

| Belgium | € 0.0827 | 18 |

| Bulgaria | € 0.0316 | 28 |

| Croatia | € 0.0876 | 17 |

| Cyprus | € 0.0990 | 15 |

| Czech Republic | € 0.0522 | 23 |

| Denmark | € 0.1078 | 13 |

| Estonia | € 0.2310 | 5 |

| Finland | € 0.5973 | 1 |

| France | € 0.1337 | 11 |

| Germany | € 0.0325 | 27 |

| Greece | € 0.2063 | 7 |

| Hungary | € 0.0776 | 20 |

| Ireland | € 0.3721 | 3 |

| Italy | € 0.1233 | 12 |

| Latvia | € 0.1617 | 9 |

| Lithuania | € 0.1810 | 8 |

| Luxembourg | € 0.0327 | 26 |

| Malta | € 0.0759 | 21 |

| Netherlands | € 0.1340 | 10 |

| Poland | € 0.1051 | 14 |

| Portugal | € 0.0955 | 16 |

| Romania | € 0.0439 | 24 |

| Slovakia | € 0.0592 | 22 |

| Slovenia | € 0.2137 | 6 |

| Spain | € 0.0329 | 25 |

| Sweden | € 0.3247 | 4 |

| United Kingdom | € 0.4187 | 2 |

Source: European Commission Taxation and Customs Union; UK HM Revenue & Customs.

Data compiled by Adam Hoffer, Jacob Macumber-Rosin

Expand or Collapse Table

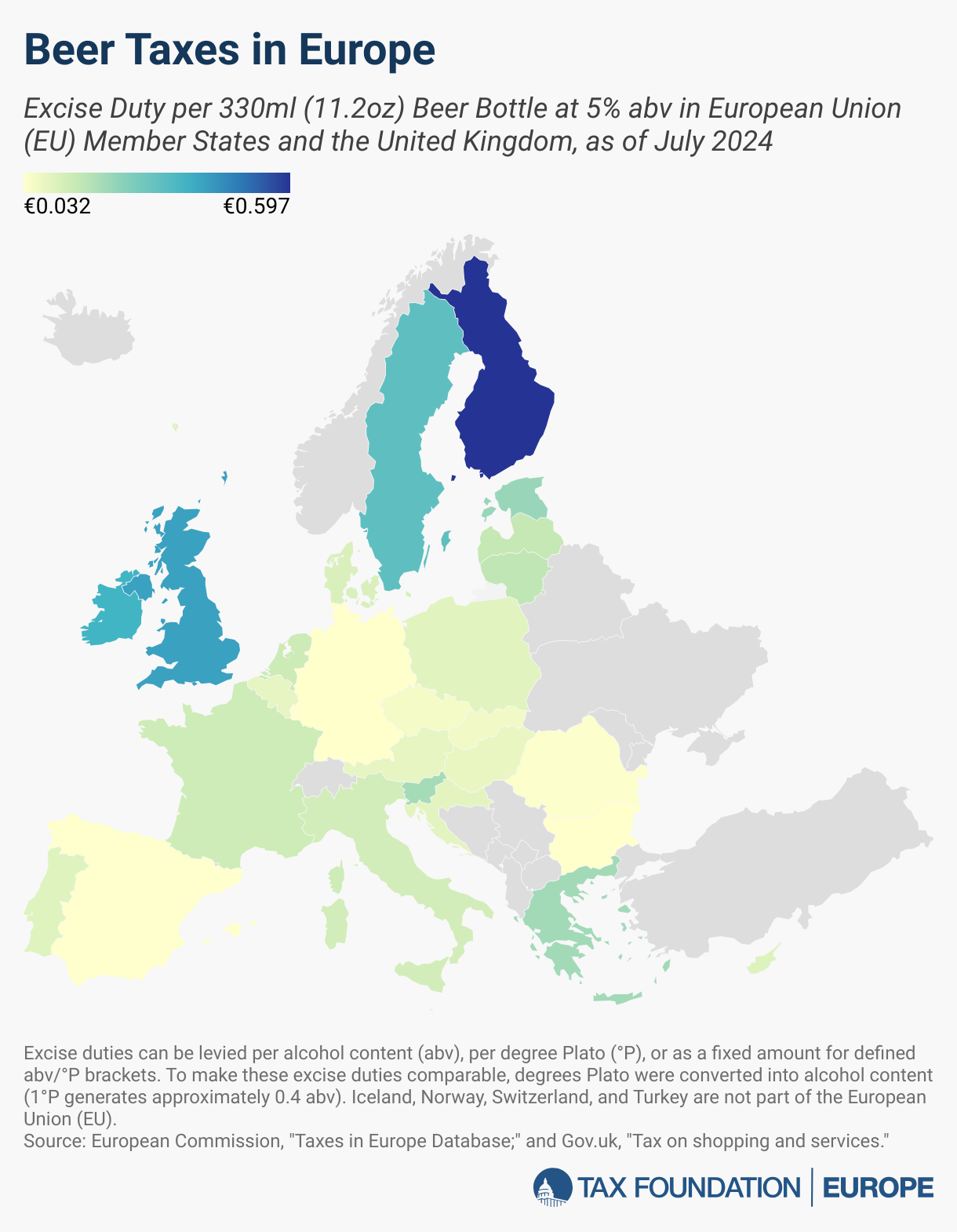

Beer Taxes in Europe, 2024

Excise Duty per 330ml (11.2oz) Beer Bottle at 5% abv in European Union (EU) Member States and the United Kingdom, as of July 2024

| Country | Excise Duty per 330ml (11.2oz) beer bottle and 5% abv in EUR | Ranking |

|---|---|---|

| Austria | € 0.0825 | 19 |

| Belgium | € 0.0827 | 18 |

| Bulgaria | € 0.0316 | 28 |

| Cyprus | € 0.0990 | 14 |

| Czech Republic | € 0.0540 | 23 |

| Germany | € 0.0325 | 27 |

| Denmark | € 0.1077 | 13 |

| Estonia | € 0.2201 | 5 |

| Spain | € 0.0329 | 25 |

| Finland | € 0.5973 | 1 |

| France | € 0.1313 | 11 |

| United Kingdom | € 0.4127 | 2 |

| Greece | € 0.2063 | 6 |

| Croatia | € 0.0876 | 17 |

| Hungary | € 0.0764 | 21 |

| Ireland | € 0.3721 | 3 |

| Italy | € 0.1233 | 12 |

| Lithuania | € 0.1561 | 8 |

| Luxembourg | € 0.0327 | 26 |

| Latvia | € 0.1485 | 9 |

| Malta | € 0.0796 | 20 |

| Netherlands | € 0.1340 | 10 |

| Poland | € 0.0928 | 16 |

| Portugal | € 0.0955 | 15 |

| Romania | € 0.0384 | 24 |

| Sweden | € 0.3247 | 4 |

| Slovenia | € 0.1997 | 7 |

| Slovakia | € 0.0592 | 22 |

Source: European Commission, "Taxes in Europe Database;" and Gov.uk, "Tax on shopping and services."

Data compiled by Adam Hoffer, Jacob Macumber-Rosin

Significant Changes from July 2024

- Lithuania increased the tax on a standard bottle of beer by €0.0249.

- Slovenia increased the tax on a standard bottle of beer by €0.0140.

- Latvia increased the tax on a standard bottle of beer by €0.0132.

- Poland increased the tax on a standard bottle of beer by €0.0123.

- Estonia increased the tax on a standard bottle of beer by €0.0109.

- Several other countries changed the tax by less than one eurocent with rate changes or changes to currency conversions to the euro.

The motivations for excise taxes on beer are straightforward. Governments tax beer and other alcohol both to discourage people from consuming alcohol and to generate revenues from a broadly consumed, but socially disdained, product. Beer taxes remain a blunt tool for reducing harm, however.

European tax treatment of alcohol varies even more widely than just the treatment of beer. Generally speaking, beer is taxed more heavily than wine, with several countries placing no excise taxAn excise tax is a tax imposed on a specific good or activity. Excise taxes are commonly levied on cigarettes, alcoholic beverages, soda, gasoline, insurance premiums, amusement activities, and betting, and typically make up a relatively small and volatile portion of state and local and, to a lesser extent, federal tax collections. on wine whatsoever. Alcohol in beer is taxed much lighter than alcohol in spirits, however.

Innovation in the alcohol industry has blurred existing categorical lines. Craft brewing, with a diverse flavor profile and wider range of alcohol content, revolutionized the beer industry, exponentially increasing the number of beers available to global consumers. Malt liquor, a higher-alcohol-content beer brewed with extra malt, by its own name is such a clear category stratifier. Many ready-to-drink cocktails are distilled spirits drinks, but after combining the spirit with a mixer, the final product available to purchase has an alcohol content closer to a beer than a bottle of liquor.

Beer in the EU is generally already taxed by alcohol content, whether by percent alcohol or degree Plato, but other categories of alcohol are not. As the alcohol product landscape continues to develop, the treatment of those categories is likely to become more complex, inefficient, and costly to administer and comply with.

Modernizing alcohol taxation by discarding clunky categorical systems for a tax levied on alcohol content would equalize the treatment of different types of alcohol while making the tax system more efficient and more transparent.

Beer taxes already tend to be levied per degree of alcohol content in Europe, and the wide range of rates reflect different governments’ outlooks on shaping consumer behavior, public health, and revenue generation via tax policy.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

SubscribeAbout the Authors

Adam Hoffer is the Director of Excise Tax Policy at the Tax Foundation. Dr. Hoffer earned his PhD in Economics from West Virginia University and his undergraduate degree from Washington & Jefferson College.

Jacob Macumber-Rosin is an Excise Tax Policy Analyst with the Tax Foundation. Jacob holds a BS in economics (politics and the economy) as well as a BS in civic and economic thought and leadership from Arizona State University.