VAT Rates in Europe, 2024

3 min readBy:More than 170 countries worldwide—including all major European countries —levy a value-added taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. (VAT) on goods and services. As today’s tax map shows, EU Member States’ VAT rates vary across countries, though they’re somewhat harmonized by the EU.

The VAT is a consumption taxA consumption tax is typically levied on the purchase of goods or services and is paid directly or indirectly by the consumer in the form of retail sales taxes, excise taxes, tariffs, value-added taxes (VAT), or income taxes where all savings are tax-deductible. assessed on the value added in each production stage of a good or service. Every business along the value chain receives a tax creditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income rather than the taxpayer’s tax bill directly. for the VAT already paid. The end consumer does not, making it a tax on final consumption.

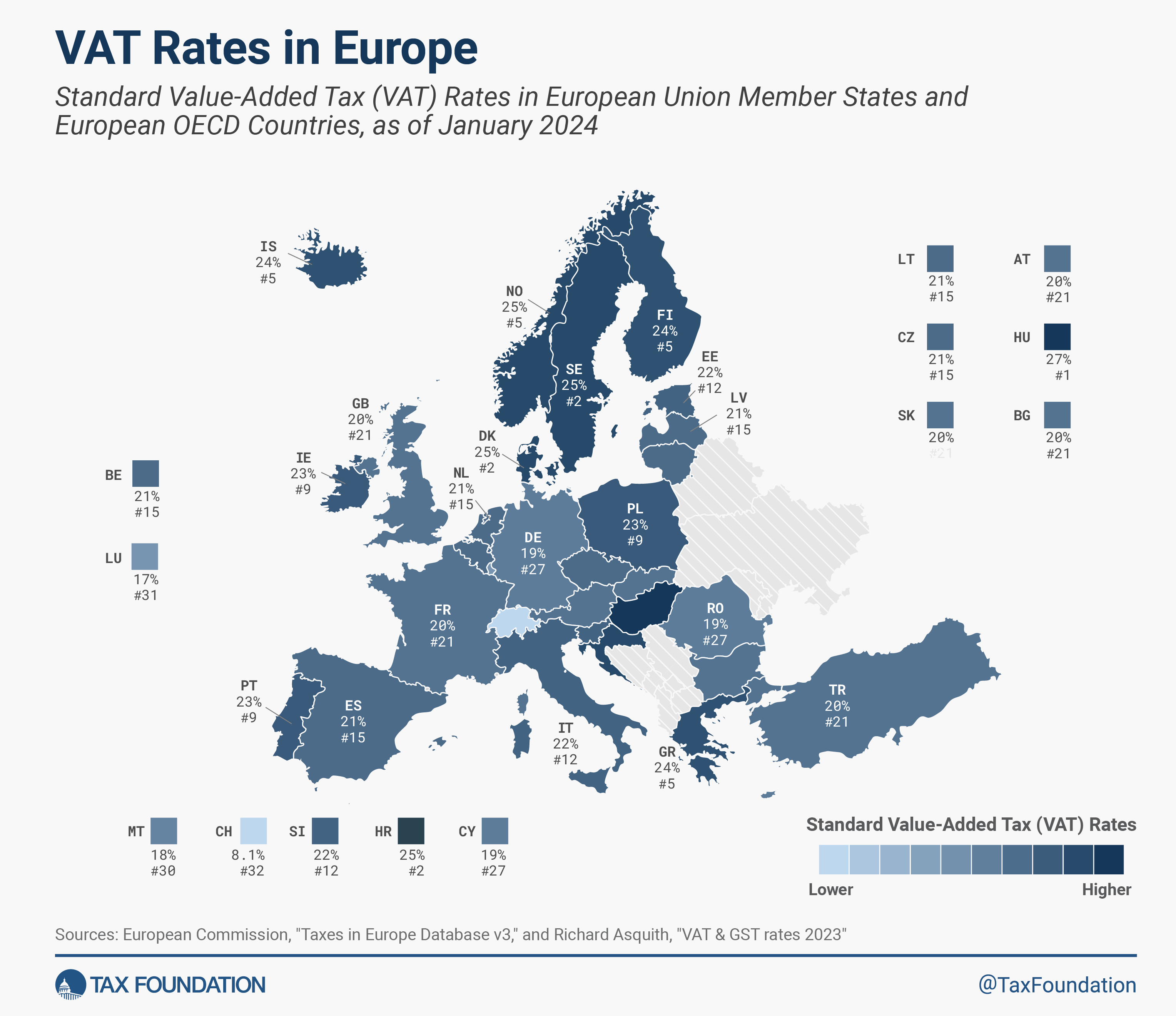

The EU countries with the highest standard VAT rates are Hungary (27 percent), Croatia, Denmark, and Sweden (all at 25 percent). Luxembourg levies the lowest standard VAT rate at 17 percent, followed by Malta (18 percent), Cyprus, Germany, and Romania (all at 19 percent). The EU’s average standard VAT rate is 21.6 percent, more than six percentage points higher than the minimum standard VAT rate required by EU regulation.

Among the five European OECD countries that are not part of the European Union—Iceland, Norway, Switzerland, Turkey, and the United Kingdom—only Switzerland levies a standard VAT rate below the EU minimum at a rate of 8.1 percent. In comparison, in the United States, combined state and local sales taxA sales tax is levied on retail sales of goods and services and, ideally, should apply to all final consumption with few exemptions. Many governments exempt goods like groceries; base broadening, such as including groceries, could keep rates lower. A sales tax should exempt business-to-business transactions which, when taxed, cause tax pyramiding. rates averaged only 6.6 percent in 2023.

Generally, consumption taxes are an economically efficient way of raising tax revenue. To minimize economic distortions, there is ideally only one standard rate that is levied on all final consumption, with as few exemptions as possible. However, EU countries levy reduced rates and exempt certain goods and services from the VAT.

One of the main reasons for reduced VAT rates and VAT-exempted goods/services is the promotion of equity, as lower-income households tend to spend a larger share of their incomes on goods and services such as food and public transportation. Other reasons include encouraging the consumption of “merit goods” (e.g., books), promoting local services (e.g., tourism), and correcting externalities (e.g., clean power).

However, evidence shows that reduced VAT rates and VAT exemptions are not necessarily effective in achieving these policy goals and can even be regressive in some instances. Such reduced rates and exemptions can lead to higher administrative and compliance costs and can create economic distortions. A recent study shows that scrapping VAT-reduced rates in EU countries will allow standard rates to drop under 15 percent. To address equity concerns, the OECD instead recommends measures that directly increase poorer households’ real incomes.

A few European countries have made changes to their VAT rates from last year. Estonia increased its standard rate from 20 percent to 22 percent. Luxembourg increased its standard rate from 16 to 17 percent and its reduced rates from 13 to 14 percent and from 7 to 8 percent, respectively. Switzerland increased its standard rate from 7.7 percent to 8.1 percent and its reduced rate from 3.7 to 3.8 percent. Turkey increased its standard VAT rate from 18 to 20 percent and its reduced rate from 8 to 10 percent. The Czech Republic has taken a step to reduce the complexity of its VAT system by consolidating its reduced rates of 10 and 15 percent into one reduced rate of 12 percent.

2024 VAT Rates in Europe, as of January 2024

| Country | Super-reduced Rate (%) | Reduced Rate (%) | Parking Rate (%) | Standard Rate (%) |

|---|---|---|---|---|

| Austria (AT) | - | 10 / 13 | 13 | 20 |

| Belgium (BE) | - | 6 / 12 | 12 | 21 |

| Bulgaria (BG) | - | 9 | - | 20 |

| Croatia (HR) | - | 5 / 13 | - | 25 |

| Cyprus (CY) | - | 5 / 9 | - | 19 |

| Czech Republic (CZ) | - | 12 | - | 21 |

| Denmark (DK) | - | - | - | 25 |

| Estonia (EE) | - | 9 | - | 22 |

| Finland (FI) | - | 10 /14 | - | 24 |

| France (FR) | 2.1 | 5.5 / 10 | - | 20 |

| Germany (DE) | - | 7 | - | 19 |

| Greece (GR) | - | 6 / 13 | - | 24 |

| Hungary (HU) | - | 5 / 18 | - | 27 |

| Iceland (IS) | - | 11 | - | 24 |

| Ireland (IE) | 4.8 | 9 / 13.5 | 13.5 | 23 |

| Italy (IT) | 4 | 5 / 10 | - | 22 |

| Latvia (LV) | - | 5 / 12 | - | 21 |

| Lithuania (LT) | - | 5 / 9 | - | 21 |

| Luxembourg (LU) | 3 | 8 | 14 | 17 |

| Malta (MT) | - | 5 / 7 | - | 18 |

| Netherlands (NL) | - | 9 | - | 21 |

| Norway (NO) | - | 12 / 15 | - | 25 |

| Poland (PL) | - | 5 / 8 | - | 23 |

| Portugal (PT) | - | 6 / 13 | 13 | 23 |

| Romania (RO) | - | 5 / 9 | - | 19 |

| Slovakia (SK) | 5 | 10 | - | 20 |

| Slovenia (SI) | - | 5 / 9.5 | - | 22 |

| Spain (ES) | 4 | 10 | - | 21 |

| Sweden (SE) | - | 6 / 12 | - | 25 |

| Switzerland (CH) | 2.6 / 3.8 | 8.1 | ||

| Turkey (TR) | 1 | 10 | - | 20 |

| United Kingdom (GB) | - | 5 | - | 20 |

Sources: European Union, “VAT rules and rates,”https://europa.eu/youreurope/business/taxation/vat/vat-rules-rates/index_en.htm#shortcut-5; European Commission, "Taxes in Europe Database v3," https://ec.europa.eu/taxation_customs/tedb/vatSearchForm.html; and Richard Asquith, "VAT & GST rates 2024," VATCalc, https://vatcalc.com/vat-rates/.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

SubscribeAbout the Author

Alex Mengden is an Economist at the Tax Foundation, where he focuses on international tax issues and tax policy in Europe. He holds a BA in philosophy and economics from the University of Bayreuth and an MSc in economics from the Ludwig Maximilian University of Munich.

Previous Versions

-

VAT Rates in Europe, 2023

4 min read -

VAT Rates in Europe, 2022

4 min read -

VAT Rates in Europe, 2021

4 min read -

VAT Rates in Europe, 2020

4 min read -

VAT Rates in Europe, 2019

4 min read