Ahead of President Joe Biden’s speech in Pittsburgh on Wednesday evening, the White House has released a fact sheet on the proposed American Jobs Plan to fund additional spending on infrastructure and R&D. The proposal’s taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. increases on corporations are among the most harmful options to pay for the increased spending. While the President’s plan emphasizes making goods in America, the tax increases will raise the cost of production in the U.S, erode American competitiveness, and slow our economic recovery.

The American Jobs Plan (Biden infrastructure plan) would raise taxes on corporations in several ways:

-

Increase the federal corporate tax rate from 21 percent to 28 percent and tighten inversion regulations.

-

Raise the tax on Global Intangible Low Tax Income (GILTI) to 21 percent, calculate it on a country-by-country basis, and eliminate the exemption of a 10 percent return on tangible investment abroad (QBAI).

-

Impose a 15 percent minimum tax on corporate book income, which would be levied on a firm’s financial profits instead of taxable income for firms with revenue over $100 million.

-

Repeal the Foreign-Derived Intangible Income (FDII) deduction, which incentivizes firms to move intellectual property (IP) into the U.S.

-

Provide a tax creditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income rather than the taxpayer’s tax bill directly. for certain onshoring activity and deny expense deductions on jobs that were offshored.

-

Increase corporate tax enforcement.

-

Eliminate certain deductions and credits for the fossil fuel industry.

The tax proposals in the American Jobs Plan (Biden infrastructure plan) rely on mistaken assumptions about how corporate taxes work, how corporations respond, and how workers are affected. Here are the facts:

-

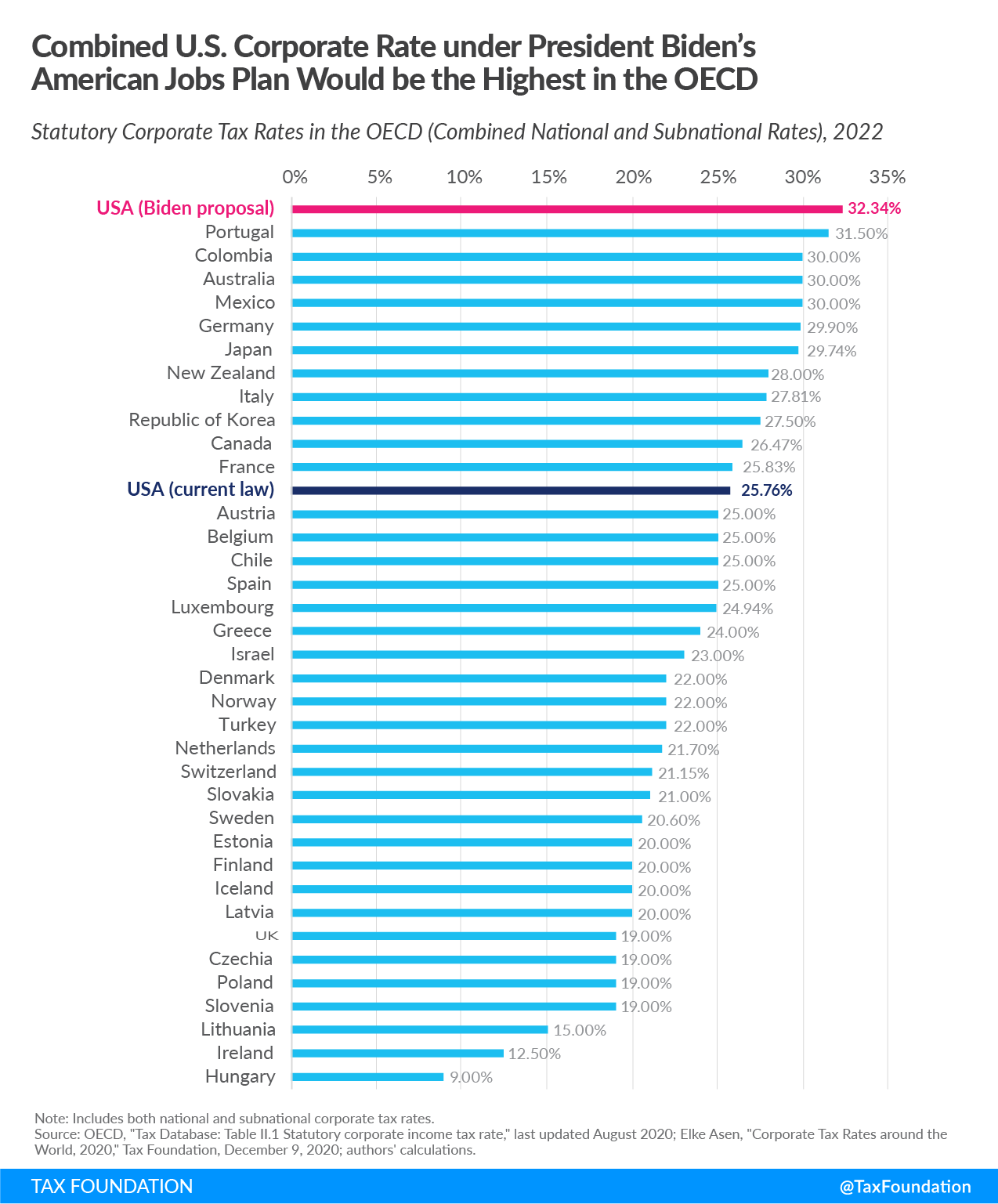

An increase in the federal corporate tax rate to 28 percent would raise the U.S. federal-state combined tax rate to 32.34 percent, higher than every country in the OECD, the G7, and all our major trade partners and competitors including China. This would harm U.S. economic competitiveness and diminish our role in the world.

-

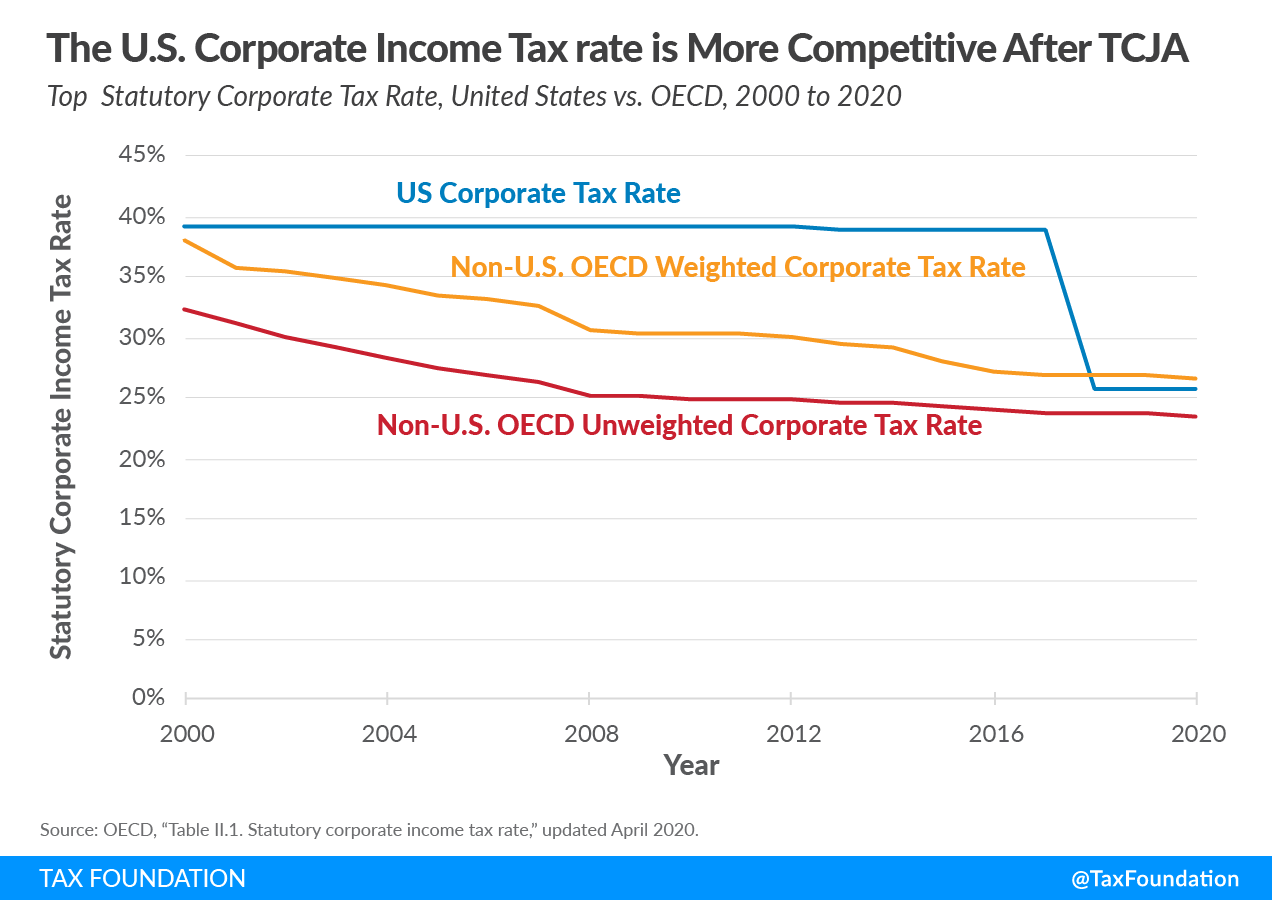

When the U.S. last had the highest corporate tax rate in the OECD, prior to tax reform in 2017 with the Tax Cuts and Jobs Act (TCJA), the U.S. experienced several years of economic malaise, including chronically low levels of investment, productivity, and wage growth, as well as major distortions and avoidance schemes in the corporate sector. This included corporate inversions to lower-tax countries, migration out of the corporate sector and into the noncorporate sector, and a decline in business dynamism. This is why the U.S. lowered the corporate tax rate, to compete with other countries around the world that lowered theirs long ago.

-

Whether we use corporate tax collections as a portion of GDP, average effective tax rates, or marginal tax rates, each measure shows that the U.S. effective corporate tax burden is close to or above the average compared to its OECD peers. Raising corporate income taxes would put the U.S. at a competitive disadvantage, whether one looks at statutory tax rates or effective corporate tax rates.

- Contrary to the proposal’s claims about a “race to the bottom” on corporate tax rates, reductions in corporate rates have plateaued for more than a decade. When the U.S. cut the federal statutory corporate rate from 35 percent to 21 percent in 2017, it was not leading a race to the bottom but moving to the average. The U.S. combined (state and federal) tax rate on corporate income is now 25.77 percent. The average corporate rate among countries in the OECD (excluding the U.S.) is 23.4 percent.

- Raising the federal corporate tax rate 7 percentage points would reduce the after-tax rate of return on corporate investment in America, resulting in less investment, less productivity, fewer jobs, and lower wages. We estimate that raising the federal corporate tax rate to 28 percent would reduce long-run economic output by 0.8 percent, eliminate 159,000 jobs, and reduce wages by 0.7 percent.

- Workers across the income scale would bear much of the tax increase. For example, the bottom 20 percent of earners would on average see a 1.5 percent drop in after-tax income in the long run.

- The design of the tax on U.S. companies’ foreign earnings known as GILTI does not incentivize offshoring.

- Critics of the design ignore the context of the policy, which includes the lower corporate tax rate and full expensing for short-lived assets. The tax burden on GILTI can be much higher than 10.5 percent since it is a second layer of tax in addition to foreign taxes. A company that chooses to invest abroad simply because of GILTI’s design would be ignoring the balance that the TCJA intended to create with real policies that incentivize investment in the U.S.

- The lower tax rate on companies that export to foreign markets was designed to make the U.S. an attractive place for businesses to hold their IP. Rather than develop their IP assets in the U.S. and then move them offshore, the design of FDII makes the U.S. an attractive place for holding IP. Just last week, Rob Portman (R-OH) referred to the fact that U.S. companies have brought back IP from offshore due to FDII.

- A minimum tax on corporate book incomeBook income is the amount of income corporations publicly report on their financial statements to shareholders. It provides a picture of a firm’s financial performance and follows Generally Accepted Accounting Practices (GAAP). While it is a useful measure for assessing financial performance, it is not useful for assessing tax liability. would make the tax code more complicated, as it would require corporations to use two tax bases to determine their tax liability. It would outsource key aspects of the corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. to the Financial Accounting Standards Board (FASB) or require policymakers to meddle in standards for financial accounting, reducing the value of financial income statements for corporate stakeholders.

- A minimum tax would also distort investment incentives when firms become liable for the minimum tax and reduce incentives to invest by clawing back provisions like the R&D tax credit and accelerated depreciation deductions. The tax would potentially undermine current-law investment incentives as well as those proposed by President Biden, such as the “Made in America” tax credit.

- The fact sheet argues that corporations face low effective tax rates in the U.S. One reason for that is because firms are investing in the United States (and can legally take a deduction for that investment). It would be a mistake to think such firms investing in the U.S. should pay corporate income taxes on that investment.

- There are real, legitimate reasons why a corporation should not be required to pay corporate income taxes in a particular year, such as deductions for accelerated depreciationDepreciation is a measurement of the “useful life” of a business asset, such as machinery or a factory, to determine the multiyear period over which the cost of that asset can be deducted from taxable income. Instead of allowing businesses to deduct the cost of investments immediately (i.e., full expensing), depreciation requires deductions to be taken over time, reducing their value and disco, R&D tax credits, and net operating loss (NOL) carryforwards.

- The American Jobs Plan would provide additional funding for the Internal Revenue Service (IRS) to increase auditing and enforcement. Instead of simplifying the tax code to help with compliance, however, the American Jobs Plan would significantly increase the complexity of the tax code by enacting policies like a minimum tax on book income that will further complicate enforcement.

- There are already guardrails in the existing tax system to check for compliance. For example, the Joint Committee on Taxation (JCT) must approve any tax refund for a C corporation that exceeds $5 million. The IRS routinely audits large corporations; for instance, in fiscal year 2019, it examined nearly 50 percent of large corporate returns with more than $20 billion in assets.

Rather than penalizing U.S. production and making the tax code more complex, Congress should consider ways to incentivize greater dynamism and domestic production through a competitive and simplified corporate tax system.

Related Resources

Launch Resource Center: President Biden’s Tax Proposals

Share this article