Tracking the Impact of the Trump Tariffs & Trade War

The Trump tariffs have not meaningfully altered the trade balance and amount to an average tax increase per US household of $700 in 2026.

55 min readThe Tax Foundation is the world’s leading independent tax policy 501(c)(3) nonprofit. For over 85 years, our mission has remained the same: to improve lives through tax policies that lead to greater economic growth and opportunity.

Our Center for Federal Tax Policy, Center for State Tax Policy, and Center for Global Tax Policy each produce timely and high-quality research and analysis that influences the debate toward economically principled tax policies. Our experts are continuously analyzing the day’s most relevant tax policy topics and are relied upon routinely for presentations, testimony, and media appearances on tax issues spanning every level of government.

Likewise, providing journalists, taxpayers, and policymakers with basic data on taxes and spending has been a cornerstone of the Tax Foundation’s educational mission since its founding. As we wrote in our first edition of Facts & Figures in 1941, “Facts give a broader perspective; facts dissipate predilections and prejudices…[and are] an important step to meet the challenge presented by the broad problems of public finance.”

The Trump tariffs have not meaningfully altered the trade balance and amount to an average tax increase per US household of $700 in 2026.

55 min read

How will recent federal tax changes affect you?

4 min read

The State Tax Competitiveness Index enables policymakers, taxpayers, and business leaders to gauge how their states’ tax systems compare. While there are many ways to show how much state governments collect in taxes, the Index evaluates how well states structure their tax systems and provides a road map for improvement.

122 min read

Lawmakers can constrain the growth of property taxes without creating new problems. But the details matter.

Our experts explain how this major tax legislation may affect you and how policymakers can better improve the tax code.

24 min read

For Congress, work on the One Big Beautiful Bill Act is done. But in state capitols, the work has not yet begun. Many of the tax changes in the federal reconciliation act flow through to state tax codes—automatically in some states, and subject to an update in states’ Internal Revenue Code conformity date in others.

39 min read

As a rule, an individual’s income can be taxed both by the state in which the taxpayer resides and by the state in which the taxpayer’s income is earned.

52 min read

Notably, the OBBBA makes permanent the individual tax changes first put in place by the TCJA, which avoids a tax hike on an estimated 62 percent of tax filers in 2026.

4 min read

Facts & Figures serves as a one-stop state tax data resource that compares all 50 states on over 40 measures of tax rates, collections, burdens, and more.

2 min read

While there are many factors that affect a country’s economic performance, taxes play an important role. A well-structured tax code is easy for taxpayers to comply with and can promote economic development while raising sufficient revenue for a government’s priorities.

93 min read

New IRS data shows the US federal income tax system continues to be progressive as high-income taxpayers pay the highest average income tax rates. Average tax rates for all income groups remain lower after the Tax Cuts and Jobs Act (TCJA).

6 min read

The variety of approaches to taxation among European countries creates a need to evaluate these systems relative to each other. For that purpose, we have developed the European Tax Policy Scorecard—a relative comparison of European countries’ tax systems.

55 min readDesigning tax policy in a way that sustainably finances government activities while minimizing distortions is important for supporting a productive economy.

5 min read

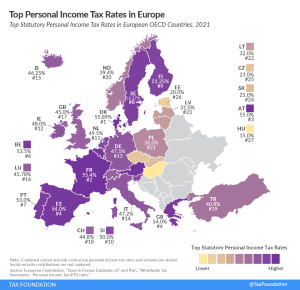

Denmark (55.9 percent), France (55.4 percent), and Austria (55 percent) have the highest top statutory personal income tax rates among European OECD countries.

2 min read

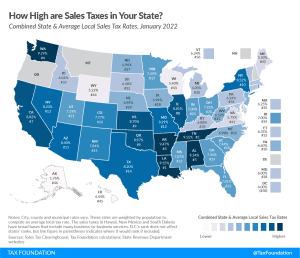

While many factors influence business location and investment decisions, sales taxes are something within policymakers’ control that can have immediate impacts.

12 min read

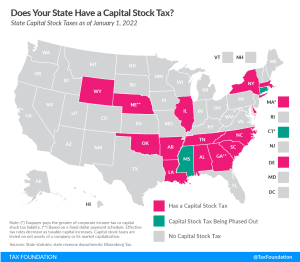

States can better position themselves for success by moving away from economically-damaging taxes like the capital stock tax.

3 min read

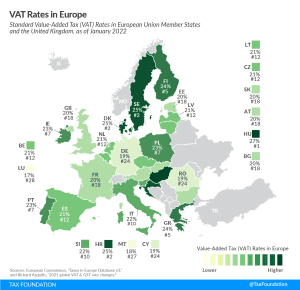

The VAT is a consumption tax assessed on the value added in each production stage of a good or service. Every business along the value chain receives a tax credit for the VAT already paid. The end consumer does not, making it a tax on final consumption.

4 min read

The latest IRS data shows that the U.S. federal individual income tax continued to be progressive, borne primarily by the highest income earners.

41 min read

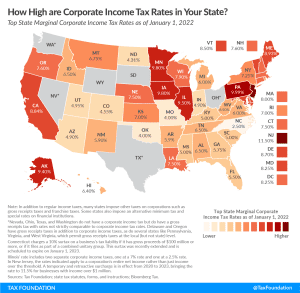

Forty-four states levy a corporate income tax. Rates range from 2.5 percent in North Carolina to 11.5 percent in New Jersey.

8 min read

Well-designed Net Operating Loss (NOL) provisions benefit the economy by smoothing business income, which mitigates entrepreneurial risk and helps firms survive economic downturns.

24 min read

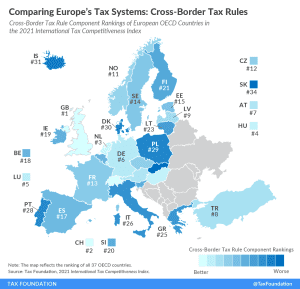

Cross-border tax rules define how income earned abroad and by foreign entities are taxed domestically, making them an important element of each country’s tax code.

3 min read

Twenty-one states and D.C. had significant tax changes take effect on January 1, including five states that cut individual income taxes and four states that saw corporate income tax rates decrease.

17 min read

States are unprepared for the ongoing shift to remote and flexible work arrangements, or for the industries and activities of today, to say nothing of tomorrow. In some states, moreover, existing tax provisions exacerbate the impact of high inflation and contribute to the supply chain crisis.

40 min read

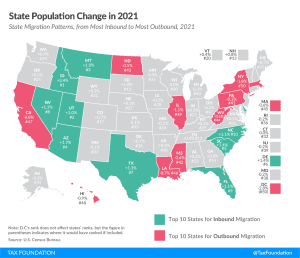

The pandemic has accelerated changes in the way we live and work, making it far easier for people to move—and they have. As states work to maintain their competitive advantage, they should pay attention to where people are moving, and try to understand why.

6 min read

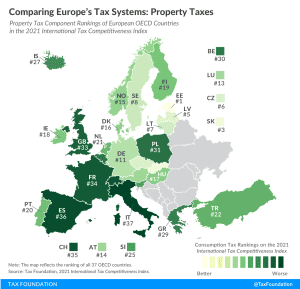

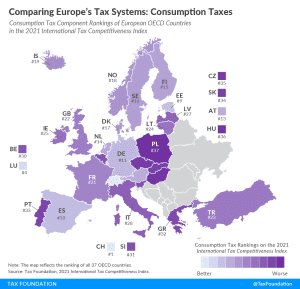

According to the 2021 International Tax Competitiveness Index, Switzerland has the best-structured consumption tax among OECD countries while Poland has the worst-structured consumption tax code.

2 min read

While there are many ways to show how much is collected in taxes by state governments, our State Business Tax Climate Index is designed to show how well states structure their tax systems and provides a road map for improvement.

169 min read

A new report shows that corporate tax rates around the world continue to level off. “We aren’t seeing a race to the bottom, we’re seeing a race toward the middle,” said Sean Bray, global policy analyst at the Tax Foundation.

24 min read

Learn more about the House Build Back Better Act, including the latest details and analysis of the Biden tax increases and reconciliation bill tax proposals.

15 min read

According to the 2021 International Tax Competitiveness Index, Switzerland has the best-structured consumption tax among OECD countries while Poland has the worst-structured consumption tax code.

2 min read

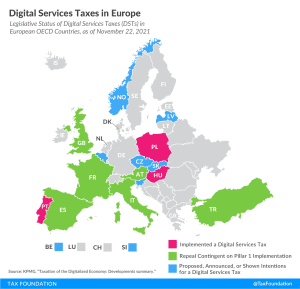

Despite ongoing multilateral negotiations in the OECD, about half of all European OECD countries have either announced, proposed, or implemented their own unilateral digital services tax.

7 min read