Net Operating Loss Carryforward and Carryback Provisions in Europe, 2021

7 min readBy:Loss carryover provisions allow businesses to either deduct current year losses against future profits (carryforwards) or current year losses against past profits (carrybacks). Many companies have investment projects with different risk profiles and operate in industries that fluctuate greatly with the business cycle. Carryover provisions help businesses “smooth” their risk and income, making the tax code more neutral across investments and over time.

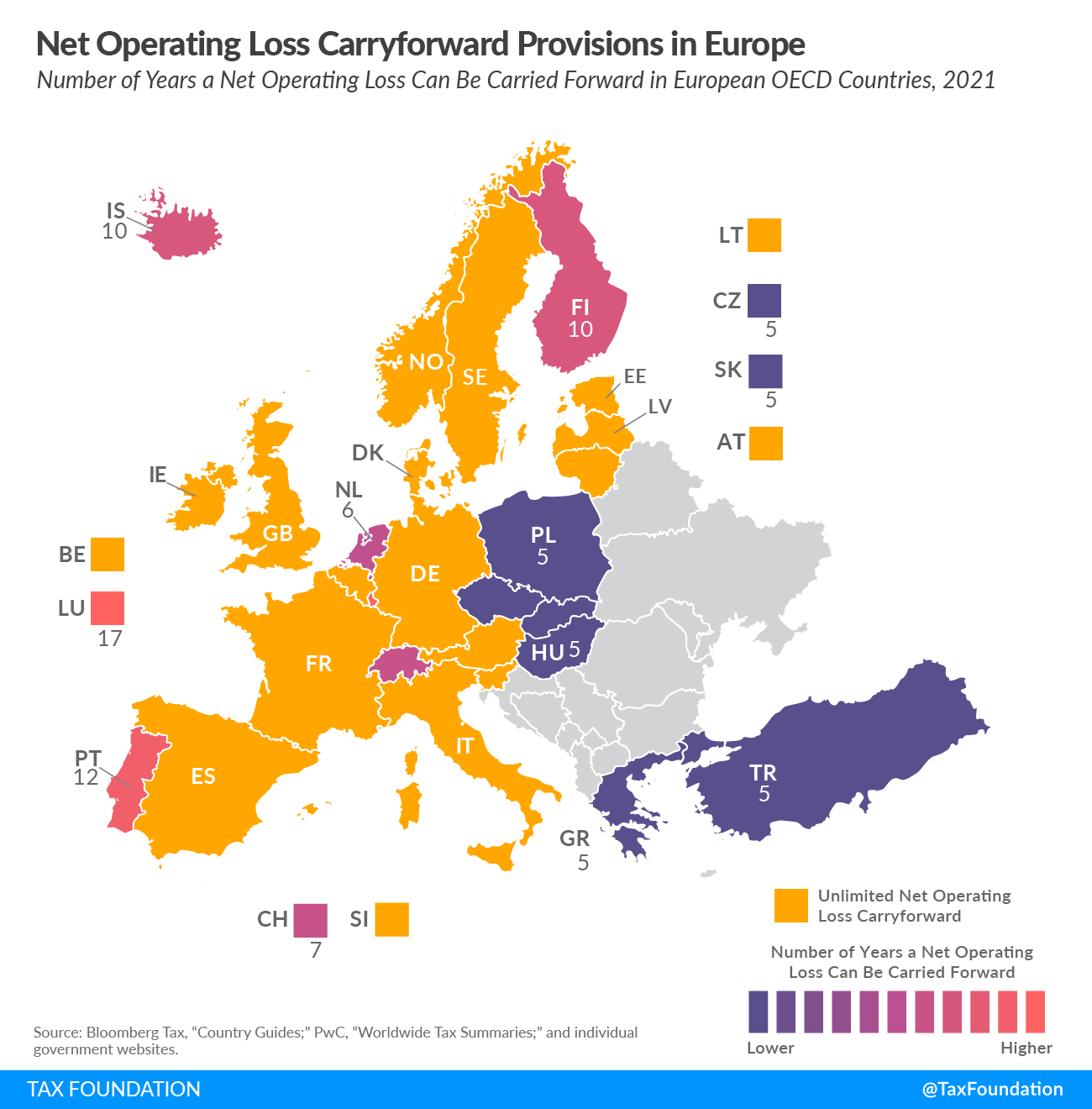

Ideally, a tax code allows businesses to carry over their losses for an unlimited number of years, ensuring that a business is taxed on its average profitability over time. While some countries do allow for indefinite loss carryovers, others have time limits. The following two maps look at this time restriction on loss carryovers, showing the number of years a business is allowed to carry forward and to carry back net operating losses.

Fifteen out of the 27 European OECD countries allow businesses to carry forward their net operating losses for an unlimited number of years. Of the remaining countries, Luxembourg has the most generous limit, at 17 years, while the Czech Republic, Greece, Hungary, Poland, Slovakia, and Turkey limit their carryforwards to five years.

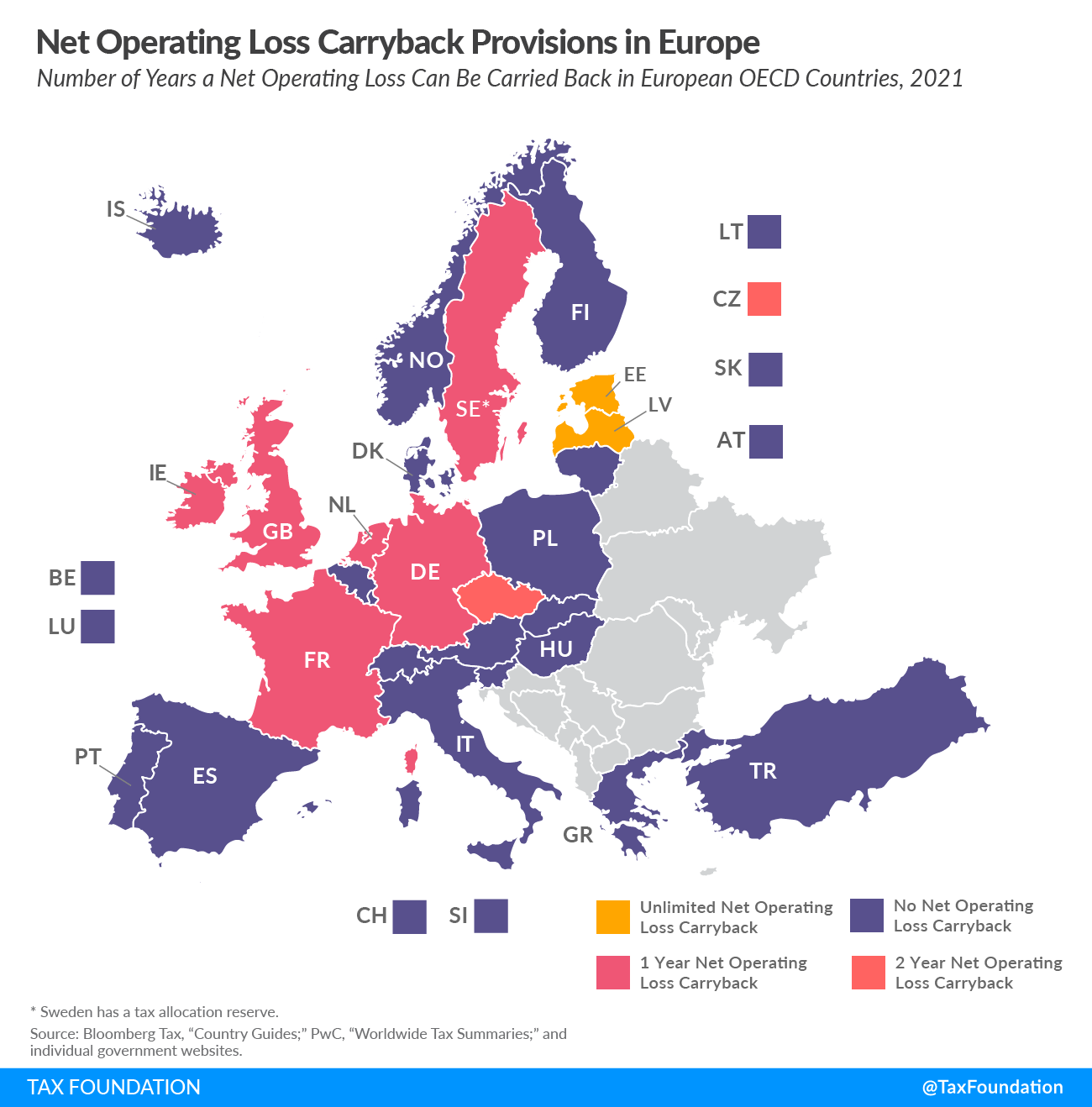

While all European OECD countries allow their businesses to carry forward losses, they tend to be much more restrictive with carryback provisions. Of the nine countries that allow carrybacks, only Estonia and Latvia provide them without a time limit.

It is worth noting that Estonia and Latvia do not explicitly allow for indefinite loss carryovers. Both of their corporate taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. systems utilize a so-called “cash-flow tax.” This tax is only levied when a business distributes its profits to its shareholders, making calculating the annual taxable profits—including potential loss deductions—redundant. Compared to a traditional corporate tax system, such a cash-flow tax effectively allows for indefinite loss carryovers.

In addition to year limits, several countries impose deductibility limits. For example, Italy’s loss deduction can only be applied to 80 percent of taxable income.

Finally, in response to the economic effects of COVID-19, a number of countries have implemented temporary loss carryback provisions or increased their deductibility limits. For example, Germany has increased its loss carryback amount from €1 million to €10 million for fiscal years 2020 and 2021.

| Country | Loss Carryback (Number of Years) | Loss Carryforward (Number of Years) | COVID-19 NOL Policies |

|---|---|---|---|

| Austria (AT) | 0 | No limit, capped at 75% of taxable income | Losses that cannot be offset in 2020 can, upon request, be carried back into 2019 up to an amount of EUR 5 million. If the loss carryback cannot be used in full in 2019, a further carryback into 2018 (up to EUR 2 million) is possible. |

| Belgium (BE) | 0 | No limit, capped at 70% of taxable income exceeding EUR 1 million | One-time possibility for loss carryback: An exemption can be applied during the financial year closing between March 13, 2019 and July 31, 2020 for the estimated loss incurred in the subsequent year (i.e., the COVID-19 year). Limits apply. |

| Czech Republic (CZ) | 2, limited to CZK 30 million | 5 | Permanent 2-year carryback provision was introduced as part of a COVID-19 relief package (went into effect on June 30, 2020). |

| Denmark (DK) | 0 | No limit, capped at 60% of taxable income exceeding DKK 8,767,500 for 2021 | – |

| Estonia (EE) | No limit (cash-flow tax) | No limit (cash-flow tax) | – |

| Finland (FI) | 0 | 10 | – |

| France (FR) | 1, limited to EUR 1 million | No limit, capped at 50% of taxable income exceeding EUR 1 million | Accelerated refunds for loss carryback receivables: Taxpayer can request immediate reimbursement of unused carryback receivables for the financial year ending December 31, 2020. |

| Germany (DE) | 1, limited to EUR 10 million | No limit, capped at 60% of taxable income exceeding EUR 1 million | Loss carryback amount was increased from EUR 1 million to EUR 10 million for the fiscal years 2020 and 2021. |

| Greece (GR) | 0 | 5 | – |

| Hungary (HU) | 0 | 5, capped at 50% of taxable income | – |

| Iceland (IS) | 0 | 10 | – |

| Ireland (IE) | 1 | No limit | Accelerated refunds for loss carrybacks: Companies can estimate their trading losses in an accounting period which includes some or all of the period from March 1, 2020 to December 31, 2020 and carry back up to 50 percent of those losses on an accelerated basis. Such an “interim claim” for the relief can be made as early as four months after the beginning of the accounting period. |

| Italy (IT) | 0 | No limit, capped at 80% of taxable income | Certain companies that increased their capital between May 20, 2020 and December 31, 2020 can benefit from a tax credit equal to 50% of any operating losses exceeding 10% of the net equity (up to 30% of the capital increase). |

| Latvia (LV) | No limit (cash-flow tax) | No limit (cash-flow tax) | – |

| Lithuania (LT) | 0 | No limit, capped at 70% of taxable income | – |

| Luxembourg (LU) | 0 | 17 | – |

| Netherlands (NL) | 1 | 6 | Accelerated refunds for loss carrybacks: Rather than having to wait until after the filing of the 2020 tax return to gain the benefit of the carryback, a company may instead estimate the coronavirus-related loss for 2020 and include all or part of it in a reserve when determining its 2019 taxable profit. The corona reserve can be set off immediately against the company’s 2019 taxable profit but must not exceed it. |

| Norway (NO) | 0 | No limit | 2020 losses of up to NOK 30 million can be carried back and offset against 2018 and 2019 tax surpluses. |

| Poland (PL) | 0 | 5, capped at 50% of total loss per year | Taxpayers whose profits are at least 50 percent lower in 2020 than in 2019 due to the pandemic may carry back a tax loss incurred in 2020 and deduct it from their 2019 income for tax purposes. The deduction is capped at PLN 5 million. |

| Portugal (PT) | 0 | 12, capped at 80% of taxable income | Tax losses incurred in 2020 or 2021 can be carried forward for 12 years and offset against up to 80 percent of taxable profits. (The permanent policy is as follows: Loss carryforwards are limited to 5 years and capped at 70% of taxable income.) |

| Slovak Republic (SK) | 0 | 5, capped at 50% of taxable income | Taxpayers may deduct unused tax losses for accounting periods ending in the years 2015 to 2018, in a total amount of EUR 1 million, from the income tax base for the accounting period for which the deadline for submitting an income tax return occurs in the year 2020. |

| Slovenia (SI) | 0 | No limit, capped at 63% of taxable income | – |

| Spain (ES) | 0 | No limit, capped at 70% of taxable income exceeding EUR 1 million (additional revenue-based restrictions apply) | – |

| Sweden (SE) | 1.5 (tax allocation reserve) | No limit | – |

| Switzerland (CH) | 0 | 7 | – |

| Turkey (TR) | 0 | 5 | – |

| United Kingdom (GB) | 1 | No limit, capped at 50% of taxable income exceeding GBP 5 million | The proposed UK Finance Bill 2021 contains provisions allowing losses to be carried back for 3 years if they are incurred in accounting periods ending from April 1, 2020 through March 31, 2022. While the amount that can be carried back to the immediately preceding year is unlimited, the carryback of any unused loss to the two earlier years will be subject to a cap of GBP 2 million for each of the accounting periods. In addition, there is the option of accelerated loss relief. |

|

Sources: Bloomberg Tax, “Country Guides,” https://www.bloomberglaw.com/product/tax/toc/source/511920/147664382; PwC, “Worldwide Tax Summaries,” https://www.pwc.com/gx/en/services/tax/worldwide-tax-summaries.html; and individual government websites. |

|||

Taxes make more sense with us in your inbox.

Subscribe to our newsletter for tax insights that cut through the noise—and make sense of it.

Sign UpAbout the Author

Thomas Locher

Summer Global Intern

Thomas Locher is a 2021 summer intern with the Tax Foundation’s Center for Global Tax Policy.