Key Findings

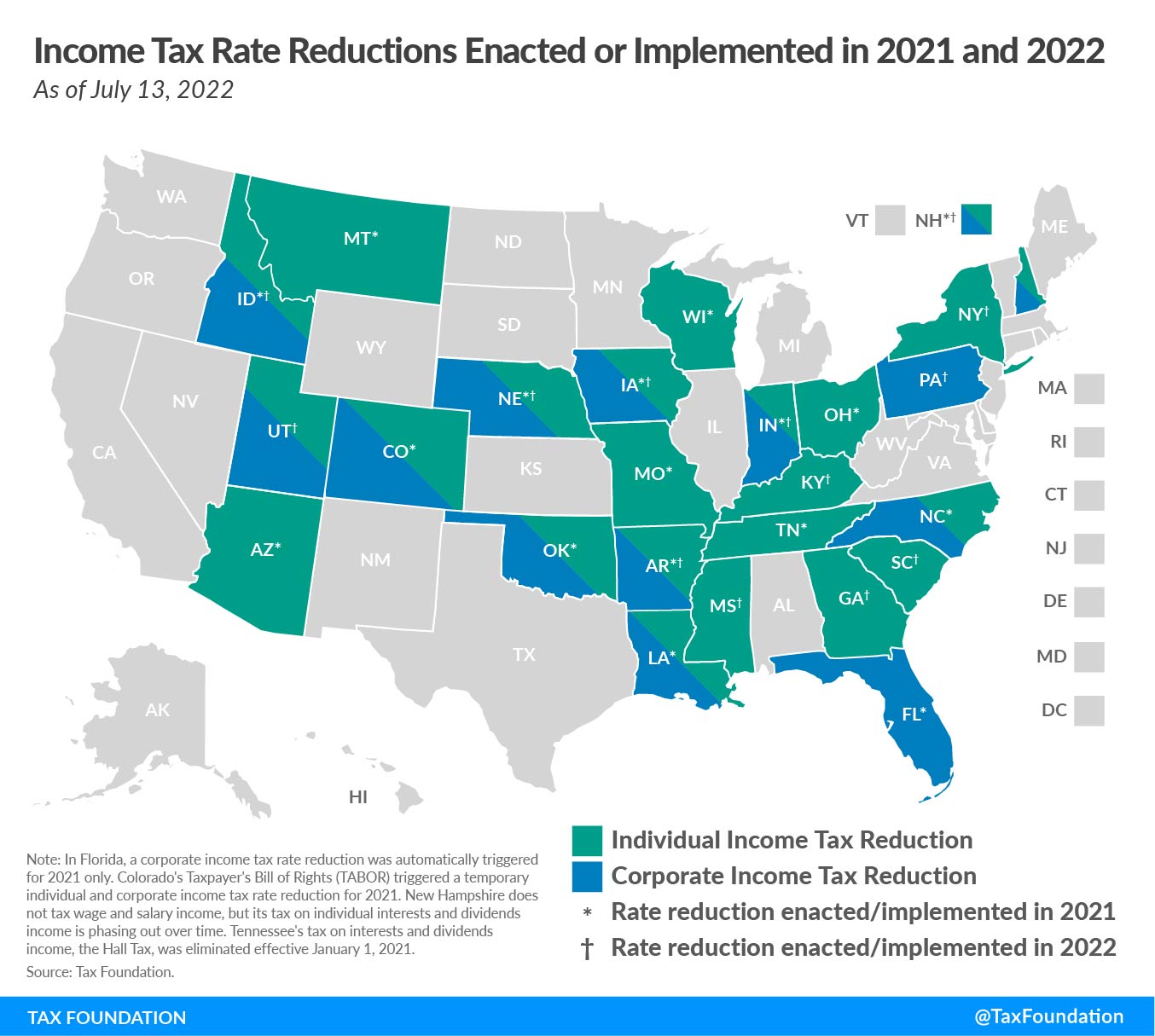

- Ten states enacted individual income tax rate reductions.

- Six states enacted corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. rate reductions.

- Oklahoma became the first state to make permanent the full expensing of capital investments by C corporations in the year they made the investments.

- Two states permanently exempted groceries from their respective sales taxA sales tax is levied on retail sales of goods and services and, ideally, should apply to all final consumption with few exemptions. Many governments exempt goods like groceries; base broadening, such as including groceries, could keep rates lower. A sales tax should exempt business-to-business transactions which, when taxed, cause tax pyramiding. bases.

- Five states suspended their taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. on gasoline.

- Eleven states chose to return surplus revenue to eligible taxpayers through direct tax rebates.

Related Resources

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

SubscribeIntroduction

Among the 46 states that held legislative sessions this year, structural state tax reform and temporary state tax relief measures were recurring themes. With most states’ sessions now complete, individual income tax rate reductions have been enacted in 10 states: Georgia, Idaho, Indiana, Iowa, Kentucky, Mississippi, Nebraska, New York, South Carolina, and Utah. A ballot measure that could lower the individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source rate in Colorado is scheduled to be voted on in November, and there is still the possibility that Oklahoma or other states could enact income tax rate reductions in a future special session.

Corporate income tax rate reductions have been enacted in six states: Idaho, Iowa, Nebraska, New Hampshire, Pennsylvania, and Utah. If approved in November, a ballot measure in Colorado would reduce the state’s corporate income tax rate.

During this year’s sessions, several states considered proposals to permanently reduce the sales tax on groceries. Ultimately, only Kansas and Virginia lawmakers decided to permanently exempt groceries from the state sales tax base. Illinois and Tennessee chose to temporarily suspend all or some of their respective sales tax on groceries.

Many other states have enacted a variety of temporary state tax relief measures. Connecticut, Florida, Georgia, Maryland, and New York enacted gas tax suspensions. Illinois delayed a two-cent gas tax increase. States such as Connecticut, Florida, New Jersey, and Tennessee have enacted new sales tax holidays, while 11 states (California, Colorado, Delaware, Georgia, Hawaii, Idaho, Illinois, Maine, New Mexico, South Carolina, and Virginia) chose to issue rebates to eligible taxpayers.

State Individual Income Taxes

Colorado

The Colorado State Income Tax Rate Reduction Initiative (Initiative 31) could retroactively reduce the state’s flat individual income tax rate from 4.55 percent to 4.40 percent, if approved by voters in the upcoming November election.

Georgia

On January 1, 2024, Georgia will transition from a graduated individual income tax with a top rate of 5.75 percent to a flat taxAn income tax is referred to as a “flat tax” when all taxable income is subject to the same tax rate, regardless of income level or assets. structure with a rate of 5.49 percent. Per HB 1437, the rate could decrease to 4.99 percent by January 1, 2029, if certain revenue conditions are met. The personal exemption will increase markedly from $7,400 for a married filer in 2022 to $18,500 in 2024 and to $24,000 in 2030. For single filers, the personal exemption will increase from $2,700 in 2024 to $12,000 in 2024.

Idaho

With enactment of H0436, Idaho reduced its top individual income tax rate from 6.5 to 6 percent and reduced its second rate from 3.1 to 3.0 percent for tax year 2022. It also consolidated the five individual income tax brackets into four by eliminating the second-highest bracket.

Indiana

HB 1002 was enacted to reduce the flat individual income tax rate from 3.23 percent to 3.15 percent for calendar years 2023 and 2024. If subsequent revenue triggers are met, the rate could be reduced to 2.9 percent by 2029.

Iowa

Under HF 2317, the Hawkeye State will transition from a graduated individual income tax structure to a flat rate system by 2026. The current nine-bracket system will be consolidated to four brackets in 2023, and the top rate will decrease from 8.53 percent to 6.5 percent. There will be three brackets in 2024 and two brackets in 2025 with top rates of 5.70 percent and 4.82 percent, respectively. By 2026, the lone rate for all taxable income will be 3.9 percent. HF 2317 also exempts retirement income and some farm rental income from taxation.

Kentucky

With the passage of HB 8, Kentucky will use revenue triggers to reduce its individual income tax by 0.5 percentage points in years in which the triggers are met. The use of these triggers could theoretically lead to the phaseout of the individual income tax in its entirety.

Mississippi

Under HB 531, Mississippi will eliminate its current 4 percent individual income tax bracket on January 1, 2023. This will transition the state from a graduated income tax structure to a flat rate of 5 percent. The flat rate is scheduled to decrease to 4.7 percent in 2024, 4.4 percent in 2025, and finally 4 percent in 2026.

Nebraska

Under provisions of LB 873, Nebraska will reduce the top individual income tax rate from 6.84 to 5.84 percent by 2027. The rate will decrease by 0.2 percentage points each year beginning January 1, 2023.

New York

The enacted budget bill, S. 8009, will accelerate tax rate cuts originally passed in 2016. Single filers will pay a tax of 5.5 percent on taxable incomeTaxable income is the amount of income subject to tax, after deductions and exemptions. Taxable income differs from—and is less than—gross income. between $13,900 and $80,650 beginning in tax year 2023—two years earlier than planned. They will also pay 6 percent on every dollar of taxable income between $80,650 and $215,400. These rates are reduced from 5.85 and 6.25 percent, respectively.

South Carolina

Effective this tax year, S1087 lowered the state’s top marginal rate from 7 percent to 6.5 percent, and the state’s previous six individual income tax brackets will collapse into three. The lowest bracket effectively exempts the first $3,200 of taxable income from taxation. The middle bracket imposes a 3 percent tax on the next $12,840 of taxable income, and all taxable income in excess of $16,040 is taxed at 6.5 percent—down from 7 percent. Beginning in tax year 2023, the top marginal rate will decrease by 0.1 percentage point each year until it reaches 6 percent in tax year 2027.

Utah

Effective this tax year under SB 59, Utah lowered its individual income tax rate from 4.95 percent to 4.85 percent. The law also established a state-level nonrefundable earned income tax credit capped at 15 percent of the federal credit.

State Corporate Income Taxes

Colorado

Initiative 31 could retroactively reduce the state’s corporate income tax rate from 4.55 percent to 4.40 percent, in parallel with an individual income tax rate reduction, if approved by voters in the upcoming November election.

Idaho

Under H0436, the state reduced its flat corporate income tax rate from 6.5 to 6 percent. The change is retroactive to January 1, 2022.

Iowa

Using revenue triggers as part of HF 2317, the state’s corporate income tax rate will begin to decrease from the current top marginal rate of 9.8 percent to as low as 5.5 percent. The magnitude of each rate cut will be contingent on corporate income tax collections. Each year, rates will be adjusted to those that would have been necessary to collect no more than $700 million in the preceding year. Given that FY 2022 net collections are projected at $780 million, Iowa starts with the capacity to cut approximately 1 percentage point from each of its current three corporate income tax brackets. The first reductions will go into effect at the beginning of calendar year 2023.

Nebraska

Under provisions of LB 873, the state will reduce its top marginal corporate income tax rate from 7.5 percent to 7.25 percent on January 1, 2023. The rate will continue to decrease an average of 0.33 percentage points per year until it reaches 5.84 percent on January 1, 2027.

New Hampshire

Enactment of HB 1221 trims the Business Profits Tax from 7.6 percent to 7.5 percent effective tax year 2024.

Oklahoma

With enactment of HB 3418, Oklahoma became the first state in the nation to make full expensing of large capital investments by C corporations permanent at the state level. Many states allow corporations to fully invest capital investments as part of the state’s conformity to the Tax Cuts and Jobs Act of 2017. However, that federal provision is set to begin phasing out at the beginning of 2023.

Pennsylvania

Enactment of HB 1342 as part of the state’s 2022-2023 budget will reduce the corporate net income tax rate from 9.99 percent to 8.99 percent on January 1, 2023. Each year thereafter the rate will decrease 0.5 percentage points until it reaches 4.99 percent at the beginning of 2031.

Utah

Effective this tax year, per SB 59, Utah trimmed its corporate income tax rate from 4.95 percent to 4.85 percent.

State Sales Tax on Groceries

Kansas

Enactment of HB 2106 will permanently exempt groceries from the state’s 6.5 percent sales tax. Grocery purchases will be taxed at 4 percent in 2023, 2 percent in 2024, and will be completely exempted as of 2025.

Illinois

The state enacted a budget, HB4700, that suspends the state’s 1 percent sales tax on groceries for fiscal year 2023, which began July 1.

Tennessee

The fiscal year 2023 budget includes a provision that will suspend the state’s 4 percent sales tax on groceries for 30 days beginning August 1.

Virginia

Under the enacted state budget, HB 30, the state’s 1.5 percent sales tax on groceries will be eliminated beginning January 1, 2023. A 1 percent local sales tax on groceries remains in effect.

State Gas TaxA gas tax is commonly used to describe the variety of taxes levied on gasoline at both the federal and state levels, to provide funds for highway repair and maintenance, as well as for other government infrastructure projects. These taxes are levied in a few ways, including per-gallon excise taxes, excise taxes imposed on wholesalers, and general sales taxes that apply to the purchase of gasoline. Holidays

Connecticut

The state enacted HB 5501 on March 24, which suspended the state’s 25-cent motor vehicle fuels tax from April 1 until July 1.

Florida

HB 7071 included a provision to suspend the state’s 25.3 cents per gallon fuel tax for the month of October.

Georgia

On March 18, Gov. Brian Kemp (R) signed HB 304, immediately suspending the gas tax through May 31.

Illinois

The state delayed until January 2023 its annual inflation adjustment to the gas tax that would have increased the tax by 2 cents per gallon on July 1, as required by a 2019 state law that doubled the gas tax and indexed it to inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spendin.

Maryland

Under SB 1010, Maryland suspended its 36.1 cents per gallon tax on gasoline and its 36.85 cents per gallon tax on diesel fuel for 30 days (March 18 through April 16).

New York

The enacted state budget (S. 8009) includes a provision to suspend the state’s sales tax and motor fuel excise tax from purchases of gasoline and diesel until the end of the calendar year.

State Sales Tax Holidays

Connecticut

As part of HB 5501, policymakers enacted a one-week sales tax holiday applicable to clothing and shoes that cost $100 or less. The holiday took effect April 10 and was in addition to the annual back-to-school tax holiday that occurs in August.

Florida

In addition to the gas tax holiday referenced earlier, the state established nine other sales tax holidays as part of HB 7071. This legislation expands to 14 days the annual back-to-school and disaster preparedness sales tax holidays, establishes a new seven-day sales tax holidayA sales tax holiday is a period of time when selected goods are exempted from state (and sometimes local) sales taxes. Such holidays have become an annual event in many states, with exemptions for such targeted products as back-to-school supplies, clothing, computers, hurricane preparedness supplies, and more. for recreational supplies over Independence Day, creates a new seven-day sales tax holiday for tools and equipment over Labor Day, and suspends the sales tax for purchases of children’s books over the summer. It creates a new one-year sales tax exemption for purchases of baby and toddler clothing, a new one-year sales tax exemption for diapers, and a new one-year sales tax exemption for Energy Star refrigerators, washers, dryers, and water heaters. Finally, it suspends for two years the sales tax on purchases of impact-resistant windows, doors, and garage doors.

New Mexico

Under HB 163, New Mexico enacted a permanent reduction to the state’s very broad-based, hybrid sales tax (known within the state as a gross receipts taxGross receipts taxes are applied to a company’s gross sales, without deductions for a firm’s business expenses, like compensation, costs of goods sold, and overhead costs. Unlike a sales tax, a gross receipts tax is assessed on businesses and applies to transactions at every stage of the production process, leading to tax pyramiding.). The tax will be reduced by one-quarter of a percentage point, from 5.125 to 4.875 percent, over two years (5.0 percent as of July 1, 2022; 4.875 percent as of July 1, 2023). The law also includes a tax deductionA tax deduction allows taxpayers to subtract certain deductible expenses and other items to reduce how much of their income is taxed, which reduces how much tax they owe. For individuals, some deductions are available to all taxpayers, while others are reserved only for taxpayers who itemize. For businesses, most business expenses are fully and immediately deductible in the year they occur, but ot for certain professional services sold to manufacturers, which was intended to reduce gross receipts tax pyramiding by approximately $5 million per year.

New Jersey

As part of the fiscal year 2023 budget, policymakers have enacted a 10-day sales tax holiday effective August 27 to September 5. The temporary exemption applies to school supplies, art supplies, instructional materials, computers, and computer supplies.

Tennessee

In addition to the annual back-to-school sales tax holiday (July 29-31) that exempts the purchase of clothing, school supplies, and computers, lawmakers have also enacted a one-year sales tax holiday for gun safes and gun safety devices effective July 1.

State Rebate Checks

California

Under a provision of the state’s fiscal year 2023 budget, single residents who filed their 2020 tax return by October 15, 2021 may be eligible for a tax rebate of up to $700. Receipt of the maximum amount is contingent on having at least one dependent and a California adjusted gross incomeFor individuals, gross income is the total of all income received from any source before taxes or deductions. It includes wages, salaries, tips, interest, dividends, capital gains, rental income, alimony, pensions, and other forms of income. For businesses, gross income (or gross profit) is the sum of total receipts or sales minus the cost of goods sold (COGS)—the direct costs of producing goods (CA AGI) of $75,000 or less. Single filers with a CA AGI between $75,001 and $125,000 are eligible for $500 while taxpayers with a CA AGI between $125,001 and $250,000 are eligible for $400. Without a dependent the payment is cut in half at all income levels. Joint filers with a dependent and a CA AGI of $150,000 or less will receive a $1,050 rebate. Those earning $150,001 to $250,000 and $250,001 to $500,000 are eligible for a $750 or $600 rebate, respectively. Without a dependent, joint filers would see payments of $700, $500, and $400 corresponding to the aforementioned income ranges.

Colorado

Due to a tax revenue surplus that exceeded the Taxpayer Bill of Rights (TABOR) cap by more than $1 billion, single tax filers will receive a $750 tax rebate in August. Joint filers are eligible for $1,500.

Delaware

With the ratification of HB360, the Delaware Department of Finance will issue a one-time $300 tax rebate throughout the summer to every adult resident of the state.

Georgia

HB 304 contains a provision that issues tax rebates of up to $250 for single filers or $500 per household.

Hawaii

Under SB514, single filers earning less than $100,000 in 2021 (or $200,000 for joint filers) will be eligible for a $300 tax rebate for each tax exemptionA tax exemption excludes certain income, revenue, or even taxpayers from tax altogether. For example, nonprofits that fulfill certain requirements are granted tax-exempt status by the Internal Revenue Service (IRS), preventing them from having to pay income tax. on their 2021 return.

Idaho

As part of H0436, Idaho issued one-time rebate checks of 12 percent of a filer’s tax year 2020 individual income tax liability, or $75 per taxpayer and dependent, whichever was greater.

Illinois

The state will issue tax rebate checks to eligible taxpayers under provisions of the state’s fiscal year budget, HB4700. The rebate will be $50 for single filers whose Illinois adjusted gross income in 2021 was less than $200,000 or $100 for joint filers whose Illinois adjusted gross income was less than $400,000 in 2021.

Maine

Single taxpayers whose federal adjusted gross income was less than $100,000 in tax year 2021 are eligible for an $850 tax rebate under provisions of the state’s supplemental budget, HP 1482. Joint filers whose federal adjusted gross income was less than $200,000 in 2021 are eligible to collect a combined $1,700.

New Mexico

Under HB 2 of the legislature’s 3rd Special Session of 2022, single taxpayers will receive at least a $500 tax rebate by August, regardless of income. Married filers will receive $1,000. Single filers who earned less than $75,000 in 2021 are eligible for an additional $250 ($500 for joint filers earning less than $150,000).

South Carolina

Under provisions of S1087, eligible South Carolinians can receive a tax rebate ranging from $100 to $800. Refunds begin at $100 for filers with a 2021 tax liability of $100 and grow proportionately with the liability up to a maximum of $800.

Virginia

The fiscal year 2023 state budget, HB 30, includes a provision that authorizes a tax rebate of up to $250 for individual filers and up to $500 for joint filers, provided the filers had a tax liability of at least that amount in 2021.

Conclusion

Although 14 state legislatures remain in session or have been called into special session, much—though not all—of the year’s work on tax reform is likely behind us. Last year was a remarkable year for state tax relief and tax reform, and legislation enacted thus far this year has 2022 closely following 2021’s pattern. The large revenue increases most states have experienced in recent years have proved fertile soil for rate reductions and structural reform, and the enhanced mobility facilitated by the pandemic has increased the role of tax competition, further nudging states in that direction.

While recession fears may slow the pace of revenue-negative tax reform in particular in 2023, there remains an important role for both state tax relief and, just as importantly, structural state tax reform, which can be revenue neutral while still enhancing a state’s overall competitiveness. In particular, reforms which reduce the cost of capital investment can help address the supply chain crisis and put states’ economies on a firmer footing.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

Subscribe