Key Findings

- An update to the EU’s Excise TaxAn excise tax is a tax imposed on a specific good or activity. Excise taxes are commonly levied on cigarettes, alcoholic beverages, soda, gasoline, insurance premiums, amusement activities, and betting, and typically make up a relatively small and volatile portion of state and local and, to a lesser extent, federal tax collections. Directive that embraces harm reduction principles would save lives and provide a steady stream of revenue to support public health expenditures.

- Taxing tobacco products according to the risks they pose to consumers encourages smokers to switch to less harmful products.

- One EU country, Sweden, has embraced alternative tobacco products, which has driven the nation’s smoking rate to the lowest level in the EU.

- The European Council and other Member States could learn from Sweden’s success and embrace harm reduction to reduce smoking rates across the EU.

- The EU plays an influential role in international tobacco taxation and could set an example for the rest of the world to effectively promote public health.

The EU Tobacco Excise TaxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. Directive and Current Tax Policies

The European Union’s Tobacco Excise Tax Directive (TED) significantly impacts public health across the European Union (EU) by providing a common framework for Member States’ tobacco tax policy.[1]

After more than a decade without changes to the TED, the EU is expected to release an updated TED in 2025. A principled update to the TED, embracing harm reduction through new categories and rate differentials for less harmful products, will save lives and provide a steady stream of revenue for public health expenditures; poor choices in TED policy updates will result in more deaths, volatile revenue, and encourage the growth of illicit markets.

Currently, the TED requires a minimum excise duty on cigarettes and other tobacco products. The TED mandates both a specific ad quantum excise tax (a fixed euro amount per pack) and an ad valorem tax (an additional percentage of the average retail selling price) on cigarettes.

The current minimum tax rates are €1.80 tax per pack of 20 cigarettes and a minimum duty of 60 percent of the country’s weighted average retail price. The minimum duty is not required to be 60 percent in countries that levy a higher excise tax of at least €2.30 per pack. The TED provides minimum rates, but all countries levy taxes that exceed these rates.[2]

The excise taxes are both levied before adding the broader value-added taxes (VAT) in each country. These myriad taxes stack up to a significant burden on consumers—totaling more than 80 percent of the retail selling price on average in 2024, meaning the combined taxes increasedharmoni consumer prices of cigarettes by more than 450 percent in the EU on average.

Table 1. Average EU Cigarette Taxes on a Pack of 20 Cigarettes as of January 2025

| Tax | Average Rates and Prices |

|---|---|

| Base Market Price (excluding taxes) | €1.1 |

| (+) Excise Duty (min. 60% of RSP) | €3.99 (64.3% of RSP) |

| (=) Pre-VAT Price | €5.09 |

| (+) VAT | €1.11 (21.8%) |

| (=) Retail Selling Price (incl. all taxes) | €6.21 (463% increase vs pre-tax price) |

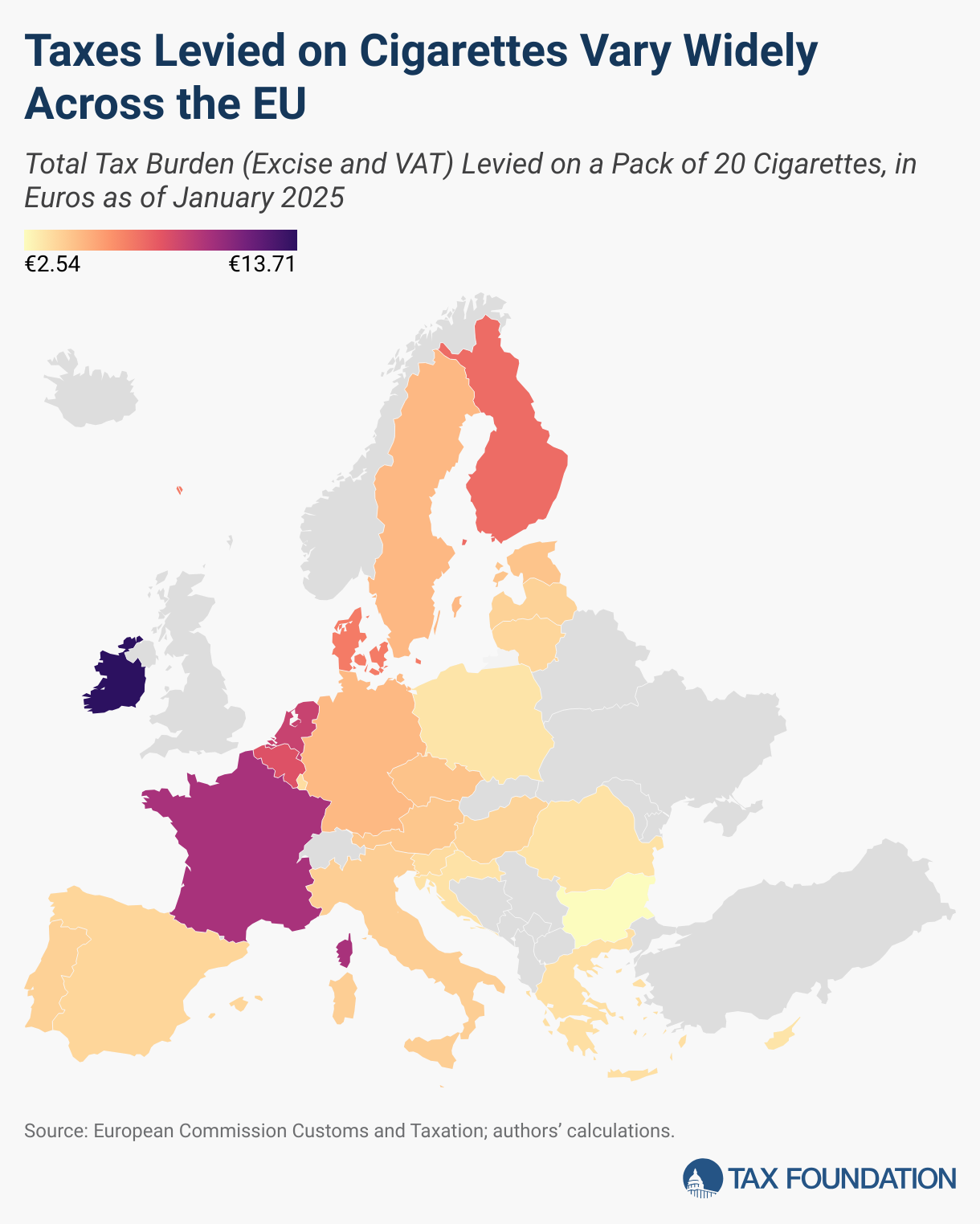

While the TED establishes a minimum tax rate, the harmonization efforts do not extend to any rate maximum. The result is a wide range of tax rates across the bloc, as several Member States levy taxes significantly higher than the minimum rate.

The excise tax burden ranges from a low of €2.02 per pack of 20 cigarettes in Bulgaria to a high of €10.71 in Ireland. With the addition of VAT, this becomes a low of €2.54 in Bulgaria to a high of €13.72 in Ireland. In terms of the relative tax burden, Germany has the lowest with total taxes comprising 69.1 percent of the country’s weighted average price, while the Netherlands has the highest with total taxes comprising 110 percent of the country’s weighted average price. Weighted average price is determined from previous years, pursuant to Article 8 (Subsection 2) of the Tobacco Tax Directive, enabling tax shares exceeding 100 percent from the previously lower prices. Taxes as a percentage of current year prices are always less than 100 percent.

The EU’s TED also establishes minimum tax rates on other tobacco products. These products include fine-cut smoking tobacco, cigars and cigarillos, and other smoking tobacco.

Table 2. Minimum EU Tax Rate on Other Tobacco Products

| Product Category | Minimum Rates |

|---|---|

| Fine-cut smoking tobacco | 50% of the weighted average retail selling price or €60 per kilogram |

| Cigars and Cigarillos | 5% of the retail selling price or €12 per 1000 units or per kilogram |

| Other smoking tobaccos | 20% of the retail selling price or €22 per kilogram |

Notably, the other tobacco products (OTP) covered by the TED are limited to combustible tobacco, which leaves out most innovative alternative tobacco products (ATPs).

The TED has three broad goals for the Commission: ensuring the “proper functioning of the internal market” via harmonization across Member States, ensuring a “high level of health protection,” and generating tax revenues.

“Proper functioning” of the EU’s internal market refers generally to avoiding distortions to competition between Member States to further the maintenance of an economic union. Establishing a minimum tax rate prevents any one Member State from undercutting the rest, which might also undermine health protection efforts. Harmonization is also used to help reduce the prevalence of smuggling and illicit markets.

Taxes increase the price consumers must pay for tobacco, thereby incentivizing smokers to purchase fewer (legal) products. Historically, smokers have generally been resistant to decreases in consumption in response to tax-induced price increases, meaning large taxes would be necessary to meaningfully decrease consumption.[3] This effect was driven, in part, by a lack of substitutes for nicotine consumption. However, with affordable alternative nicotine sources now available, smokers have demonstrated a willingness to move away from combustible cigarettes to ATPs.

Cigarette consumption is associated with harms to consumers and some bystanders, so a reduction in cigarette consumption would improve public health. Improved public health goals could be achieved through means other than taxation, of course, but revenue generation is also a goal of the TED. The directive implicitly places competition in the internal market and health protection in higher priority than revenues.

The European Commission uses the TED to set minimum rates across the EU to further these three broad goals, but Member States retain a significant degree of their sovereign rights to act within this framework. Maximum rates are not codified, leaving rate determination primarily up to each Member State provided they abide by the tax rate floor. So long as internal market competition, health protection, and revenue generation are not unduly burdened by a Member State, the TED does not justify intervention into domestic policies.

The forthcoming update of the TED may create new categories to include the ever more popular smoking alternatives like heat-not-burn tobacco, oral nicotine pouches, and vaping and other electronic nicotine delivery systems (ENDS).[4] The existing directive already acknowledges differences between types of manufactured tobacco that necessitate different tax treatments between them, so this understanding could easily be expanded to encompass ATPs.

Tax Policies Carry Trade-offs: The Economics of Taxing Tobacco

Tax policy carries trade-offs and tobacco taxes are no different. While tobacco taxes decrease legal sales, the greater the tax, the greater the incentive for participation in illicit and black markets. Harmonization, health protection, and revenue generation are all undermined by the prevalence of smuggling, fraud, and illicit markets of tobacco products like cigarettes.

From a public finance perspective, cigarette taxes are also regressive and provide a volatile revenue stream attached to a shrinking tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. . These issues should raise concerns over further increases to the existing tax rates.

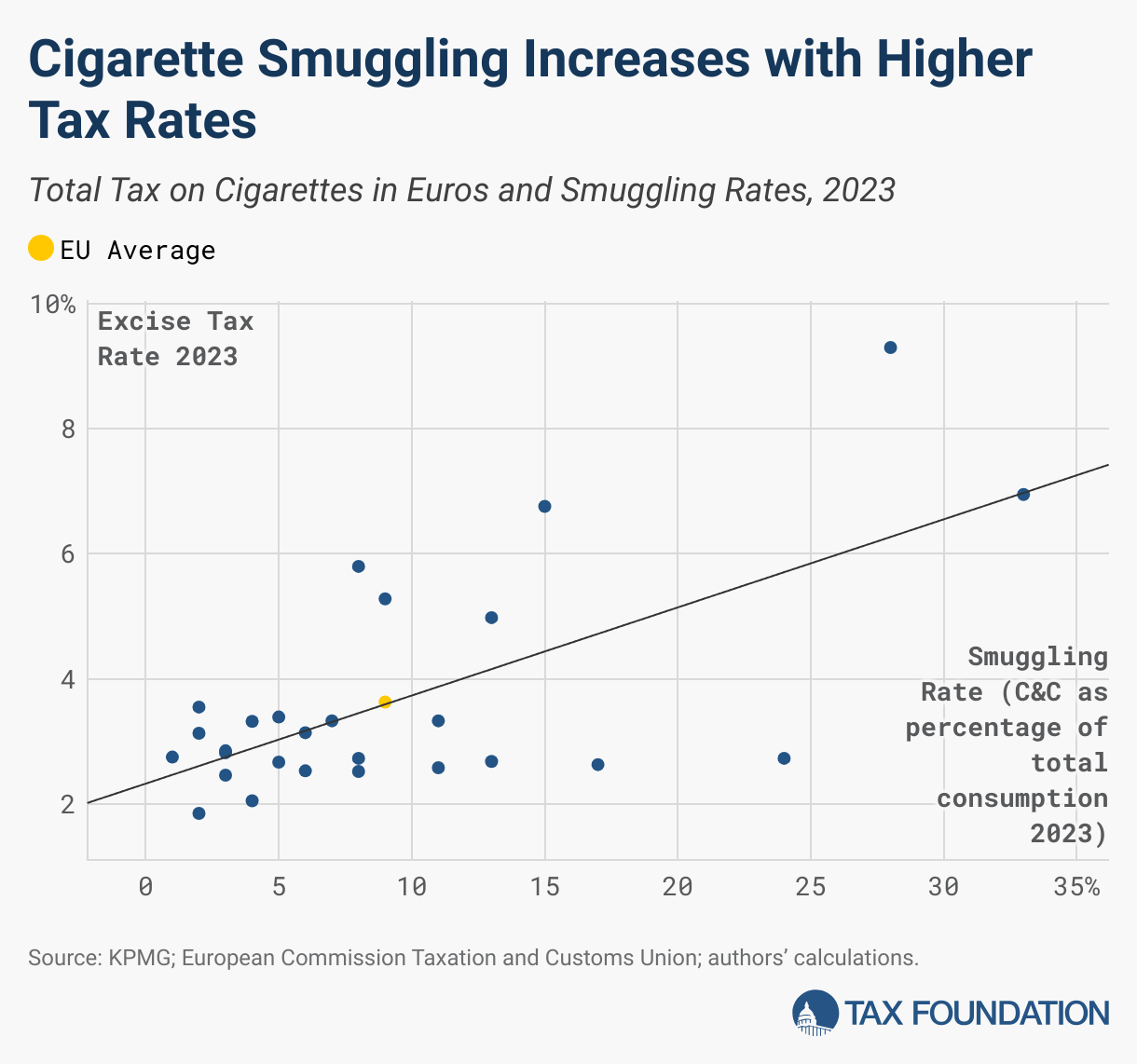

Cigarettes make an ideal product for illicit markets.[5] They are lightweight, easy to transport, legal to consume, and products can be sold for a fraction of the legal price simply through tax evasion. KPMG estimates that 35.2 billion counterfeit and contraband cigarettes were consumed across EU Member States in 2023.[6] This amounts to 8.3 percent of all cigarettes consumed in these countries. These counterfeit and contraband cigarettes, if purchased legally, would have generated at least €11.6 billion in additional tax revenue.

Punitive taxation and enforcement alone will likely not be enough to adequately address the problem, let alone eliminate it. While enforcement plays an important role in combating illicit markets, designing a tax and regulatory regime that encourages participating in legal (and taxed) transactions is an even more important factor.

Similarly, draconian regulatory schemes and excessive taxation rates threaten to grant market share to an illicit market for ATPs just as they do for cigarettes. Throughout Europe, a thriving illicit market already exists for vaping systems, often smuggled from China and Russia. Germany and Spain seized hundreds of thousands of illegal e-cigarettes in 2024.[7]

Illicit market issues overlap with tax equity concerns. Tobacco taxes disproportionately affect low-income consumers because cigarette taxes are regressive.[8] All excise taxes tend to be regressive to some degree, but cigarette taxes are the most regressive of the common excise taxes largely due to the increased prevalence of smoking among people with lower incomes.[9]

From a public finance standpoint, excise taxes have particularly narrow tax bases, which contribute to their revenues tending to be particularly volatile.[10] This makes them uniquely ill-suited to furnish general funds as the revenues are inherently unreliable.

This effect is exacerbated for cigarette taxes by the decades-long trend of declining cigarette consumption. The prevalence of smoking has decreased steadily across most EU countries since at least 2006.[11] The tax base of cigarette taxes is ever shrinking, which means that even if revenue increases temporarily in response to a rate hike, the long-run trend will steadily decrease as fewer Europeans smoke.

Tobacco tax policy is complicated because combustible tobacco products are far from the only option to consume nicotine; innovation and development of ATPs have massively changed a market historically dominated by traditional cigarettes.

Harm Reduction and Alternative Tobacco Products

ATPs are products that enable the consumption of nicotine without the most harmful aspect of smoking: the inhalation of burning toxins. Nicotine is an addictive chemical found in tobacco products, but nicotine itself isn’t a carcinogen. Research shows that nicotine alone does not cause lung cancer, stroke, or chronic obstructive pulmonary disease (COPD) that are commonly associated with smoking.[12] Rather, the other toxic chemicals and combustion in cigarettes and tobacco are what cause cancer. Avoiding these other chemicals drastically reduces the harms experienced by both consumers and bystanders via secondhand contact. The reduction in harm thus also reduces the necessary health-care costs of treating those harms.

ATPs come in many forms, each with their own associated risk profile, nicotine delivery medium, and consumer price profile. Some of the most popular ATPs are heat-not-burn (HNB) or heated tobacco products (HTP), oral products such as snus and tobacco-free nicotine pouches, and ENDS or vaping products.

HNB products do not combust the tobacco but merely heat it, facilitating the consumption of the nicotine in the tobacco with fewer harmful chemicals than combustible tobacco products. There are also tobacco-free nicotine units available for use in HNB products. Vaping products, or e-cigarettes or ENDS, aerosolize nicotine e-liquid with electronics, removing tobacco from the process and thus avoiding associated harms. Snuff and snus are cut or powdered tobacco products that are sniffed via the nostrils or placed in the mouth, again enabling nicotine consumption while avoiding more harmful combustion. Nicotine pouches or modern oral nicotine are small pouches containing nicotine to be placed in the mouth and absorbed without the harm associated with chemical inhalation.

Each poses a varying degree of health risk, but those health risks are all considerably less than smoking. These noncombustible tobacco products and tobacco-free nicotine products are also considerably less harmful to consumers and bystanders than combustible cigarettes. Designing a taxation and regulatory scheme to embrace their potential for harm reduction via smokers switching to less harmful alternatives may save millions of lives.

The availability of less harmful options for nicotine consumption accelerated the decades-long trend of declining smoking prevalence. A large share of consumers switched to less harmful methods of nicotine consumption. This switching to a less harmful form of nicotine consumption is the foundation for the principle of harm reduction, a key aspect of sound tobacco and nicotine tax and regulatory design.

Harm reduction recognizes the feasibility of reducing negative outcomes associated with certain goods rather than attempting to eliminate the harm entirely through punitive taxation or outright bans. Embracing the potential for less harm is significantly more effective than the insistence on nicotine abstinence that has traditionally dominated cigarette cessation efforts in public health and regulation. Substituting ATPs for cigarettes has widely been found to be a useful tool for smoking cessation.[13]

Smoking cessation is notoriously challenging.[14] Embracing substitution for a less harmful nicotine consumption method is one possible resource for smokers wanting to quit. Nicotine replacement therapies like patches and lozenges are longstanding resources for cessation, and ATPs can be used in similar ways. Harm reduction through substitution is likely more effective at encouraging smoking cessation than punishment through taxation, as are direct monetary incentives.[15]

Some countries outside of the EU have already integrated harm reduction, to some degree, into their tobacco control regimes. The US Food and Drug Administration (FDA) recognizes less harmful products as modified risk tobacco products that receive a lower tax rate commensurate with their lower risk profiles.[16] The FDA began these classifications with Swedish-style snus products—popular in Sweden but outright prohibited almost everywhere else in the EU.

The UK’s Royal College of Physicians has concluded that the long-term health risks from vaping is “unlikely to exceed 5% of the harm from smoking tobacco” and emphasizes that “harm reduction has huge potential to prevent death and disability from tobacco use, and to hasten our progress to a tobacco-free society.”[17] Public Health England agrees that e-cigarettes are approximately 95 percent less harmful than smoking cigarettes.[18]

In the EU, however, the TED fails to acknowledge many ATPs and thus precludes much harm reduction. In many Member States, ATPs like e-liquids face tax policies that run counter to tobacco harm reduction. The silence of the current TED on ATPs like vapor has led to disparate treatment across Member States, distorting the EU’s internal market and creating unequal grounds.[19]

Some ATPs, like some oral tobacco, and flavored tobacco products are largely prohibited by the Tobacco Products Directive, a separate regulatory scheme governing tobacco products and their ingredients. Sweden was granted a derogation from this prohibition on oral tobacco, which the country insisted upon as a condition for joining the EU.[20]

An update to the TED can and should shift this regime toward embracing harm reduction, enabling ATPs to assist with smoking cessation, promoting public health, and driving consumers towards safer legal markets. This would mean ensuring that ATPs are accessible, acceptable, and affordable for consumers.

It is likely that a tax regime that optimizes harm reduction by taxing safer products less would not maximize revenues. The primary focus of these taxes should not be revenue generation, but public health outcomes. Excessively taxing popular substitutions for smoking might yield extra revenues in the short term, but would do so at the cost of many preventable deaths from smokers discouraged from switching to less harmful alternatives in the long term. A more pragmatic tax policy that integrates harm reduction could provide a better balance between public health and revenue generation.

The best practices for sound tax treatment of ATPs involve simple, direct ad quantum taxes. This means taxing by stick, by weight, or by milliliter of vape fluid depending on the product type. This most effectively targets the harm-causing element of the good and keeps the taxes as neutral as possible. Tax rates on ATPs should yield a price differential between combustible tobacco products and less harmful alternatives, thereby encouraging smokers to switch. This rate can be levied as a reduction to the rate applied to cigarettes, commensurate with a specific product’s understood place on the risk continuum.

The risk continuum quantifies the relative overall risk of a product—accounting for the direct harm that the product causes to consumers and bystanders, the ease of substitution for combustible cigarettes, the ease of consumption of mass quantities, and the addictiveness of a product.

Using this framework, a spectrum of four categories of reduced-harm products can be delineated.

Table 3. Alternative Tobacco Product Tax Rates to Optimize Harm Reduction

| Product | Tax Rate Relative to Combustible Cigarettes |

|---|---|

| Very Low Nicotine Cigarettes, Loose Tobacco | 50% of Cigarette Tax Rate (a 50% Reduction Compared to Cigarettes) |

| Heated Tobacco Products, Moist Tobacco | 25% of Cigarette Tax Rate (a 75% Reduction Compared to Cigarettes) |

| E-Cigarettes and Vaping Products, Modern Oral Tobacco | 10% of Cigarette Tax Rate (a 90% Reduction Compared to Cigarettes) |

| Nicotine Replacement Therapies (Gums, Patches, Lozenges) | 0% of Cigarette Tax Rate (a 100% Reduction Compared to Cigarettes) |

This categorical approach establishes a relatively easy way for Member States to embrace harm reduction policies to promote smoking cessation and more effectively promote public health. Assigning products to categories based on their risk ensures that safer products will suffer a lower tax rate, establishing price differentials that encourage consumers to choose less harmful alternatives to smoking.

Making a wider variety of less harmful products available to smokers saves lives, shrinks illicit markets, and allows governments to gradually transition from the shrinking tax base that is combustible cigarettes.

Policies in Practice

The exclusion of most ATPs from the current TED has created a fragmented market that, in addition to the problems of compliance and international business distortions, has also created a series of case studies on different policy outcomes.

One country has far outperformed its EU peers in reducing smoking prevalence and avoiding preventable deaths from tobacco use: Sweden. Except for Sweden, no EU Member State has yet to reduce their smoking rate below 10 percent. Studies show that, for most countries, progress on reducing smoking prevalence has stagnated or reversed since 2020.[21]

In 2024, Sweden became the first country to officially be “smoke-free,” defined in this context as having a smoking prevalence of less than 5 percent.[22] Only 4.5 percent of Swedish-born adults, or 5.3 percent of all adults including immigrants, smoked. The Swedes were pioneers in the field of ATPs with the early development of snus. They have since been pioneers in tobacco control policy by leveraging this and other innovations to embrace harm reduction and improve their nation’s public health.

Dr. Anders Milton, physician and former president of the Swedish Medical Association, credits the success to the country’s “pragmatic focus on harm reduction rather than prohibition. A wide range of safer nicotine products, with a variety of strengths and flavours [sic], is legally available both online and in stores, supported by advertising, which raises awareness and encourages uptake.”

Concurrent with the country’s consistently low smoking prevalence, Sweden consistently has among the lowest per capita cancer rates and tobacco-related deaths in the EU.[23]

Embracing ATPs and their harm reduction capacity is clearly heavily contributory to Sweden’s uniquely low smoking rate.[24] A study of tobacco use in Sweden over 36 years showed a continuous decline in smoking rates coupled with a substantial rise in snus prevalence.[25] Snus plays a clear role in Sweden’s uniquely low per capita tobacco mortality rates.[26]

According to Swedish Minister of Finance Mikael Damberg, taxes on tobacco and nicotine products “are already structured in such a way that products are generally taxed on the basis of hazard.”[27] As a result, a wide array of smoking alternatives has become available and accepted in Sweden, resulting in monumental strides towards reducing harms from smoking and tobacco consumption.

In stark contrast to Sweden’s achievement 16 years ahead of the EU’s 2040 goal of reducing smoking rates below 5 percent, most other Member States are far behind on progress toward reducing smoking. Studies of Sweden relative to neighboring countries show that embracing harm reduction yields about an additional 0.4 percent per year to the rate of decline in smoking prevalence.[28] Instead, many EU Member States have chosen an opposite approach, suppressing ATPs and undermining their harm reduction potential.[29]

Estonia, for example, has particularly stringent restrictions on ATPs.[30] The nation levies an excise tax on e-cigarette fluid (€0.20 per mL) and has banned flavored vape products since 2019. Advertising of these alternative products is prohibited, even for nicotine replacement therapies, and ATPs experience particularly low prevalence relative to the rest of the EU.[31] Not coincidentally, Estonia experiences a relatively high smoking rate of 25 percent, which has increased by 7 percent since 2020.

Belgium’s smoking rate is slightly lower than the EU average at 21 percent. However, this has remained entirely unchanged from 2020. The country has since banned nicotine pouches and disposable vapes entirely, wholly precluding any harm reduction from the less harmful products.[32]

Ireland set a target for becoming “smoke-free” by 2025, much like Sweden, but the country’s smoking rate is still 16 percent, down only 2 percent from 2020 despite having the bloc’s heaviest tax on cigarettes. This will likely be exacerbated by the 2024 excise tax on vape fluid (€0.50 per mL) and the expected ban on disposable and flavored vapes.[33]

Other than Sweden, only the Czech Republic had taken significant steps to embrace harm reduction. The regulatory environment there enabled adoption of ATPs. The nation’s smoking rate decreased from 30 percent to 23 percent since 2020; however, this progress is likely to slow at best in the wake of new taxes on ATPs and a flavor ban on vapes in 2025.[34]

Many EU Member States have refused to learn from the example set by Sweden and suffer needlessly high rates of smoking as a result. The new EU TED should take inspiration from Sweden’s unique progress and embrace sound harm reduction policies that leverage the innovations from ATPs to promote public health.

If the present, stagnating trajectory continues unaltered, the EU will take an extra 60 years to achieve its goal—becoming “smoke-free” by the year 2100. Changes are clearly necessary to yield public health benefits from reducing the harms inflicted on smokers and the costs associated with treating those harms. Just as Sweden can be an example for the EU, the EU could be an example for the rest of the world.

The EU’s Global Role for the Future of Tobacco Policy

Much of the world looks to EU policy as a guide for their own. As the General Data Protection Regulation has transformed the global data privacy landscape, the new TED could help shape global health trends.[35]

Tax harmonization across EU Member States can lower compliance costs for businesses, but a sound tax design could do much more. International businesses that participate in the European market may shift their focus to reduced-harm products. Enabling accessible and affordable ATPs would undermine the market share of illicit markets, both for the ATPs themselves and for traditional cigarettes, by driving consumers into safer legal transactions.

The thriving global cigarette and tobacco product smuggling industry could be significantly undermined by a TED that effectively integrates innovative products, embraces harm reduction principles, and sets a shining example for the other countries of the world.

EU action is particularly important now, during a time of tense international relationships. If other countries follow the lead of an EU that embraces harm reduction, EU policies would not only benefit Europeans, but also citizens around the globe.

An update to the TED that enables less harmful alternative products has the potential to drastically improve public health in Europe and abroad. Modern oral nicotine, vapor products, snus, and other ATPs are significantly less harmful than traditional combustible cigarettes and thus should bear a reduced tax burden. Taxing tobacco products in proportion to their associated harms would help incentivize consumers to switch to less harmful consumption methods.

Embracing simple, science-based harm reduction principles would assist the EU in reaching its goals of reducing smoking rates, avoiding millions of preventable deaths, and setting an example that the rest of the world could follow to do the same for themselves.

References

[1] The Council of the European Union, “Council Directive 2011/64/EU,” June 21, 2011, https://eur-lex.europa.eu/eli/dir/2011/64/oj/eng.

[2] European Commission Taxation and Customs, “Taxes in Europe Database v4,” https://ec.europa.eu/taxation_customs/tedb/#/advanced-search.

[3] Craig A. Gallet and John A. List, “Cigarette demand: a meta‐analysis of elasticities,” Health economics 12:10 (2003): 821-835.

[4] Carl Deconinck, “Future of cigarettes in Europe up in smoke?” Brussels Signal, Feb. 13, 2025, https://brusselssignal.eu/2025/02/future-of-cigarettes-in-europe-up-in-smoke/; The Bulletin, “Tobacco taxation and smoke-free products: What is the future regulatory path for the EU Commission?” Nov. 11, 2024, https://www.thebulletin.be/tobacco-taxation-and-smoke-free-products-what-future-regulatory-path-eu-commission; and Tiziana Cauli, “EU Commission reveals its preferences for higher taxes on tobacco products,” TobaccoIntelligence, Nov. 3, 2022, https://tobaccointelligence.com/eu-commission-reveals-its-preferences-for-higher-taxes-on-tobacco-products/.

[5] Adam J. Hoffer and Donald J. Lacombe, “Excise tax setting in a dynamic space-time framework,” Public Finance Review 45:5 (2017): 628-646.

[6] KPMG, “Illicit cigarette consumption in Europe,” Sept. 9, 2024, https://www.pmi.com/resources/docs/default-source/itp/illicit-cigarette-consumption-in-europe_2023-results_final.pdf?sfvrsn=7a64b1c9_31.

[7] Vape HK, “German Customs Seize 400,000 Illegal Vapes: A Deep Dive into the Vaping Industry and Its Challenges in Europe,” Dec. 3, 2024, https://vape.hk/german-customs-seize-400000-illegal-vape; and Ali Anderson, “€1.55 million of illegal vapes seized by police in Spain,” Clearing the Air, Oct. 11, 2024, https://clearingtheair.eu/en/post/eu1-55-million-of-illegal-vapes-seized-by-police-in-spain/.

[8] Ulrik Boesen, “Taxing Nicotine Products: A Primer,” Tax Foundation, Jan. 22, 2020, https://taxfoundation.org/research/all/federal/taxing-nicotine-products/.

[9] Adam Hoffer, “Global Excise Tax Application and Trends,” Tax Foundation, Apr. 7, 2023, https://taxfoundation.org/research/all/global/global-excise-tax-policy-application-trends/.

[10] Adam Hoffer, “How Stable is Cigarette Tax Revenue?” Tax Foundation, May 23, 2023, https://taxfoundation.org/data/all/state/cigarette-tax-revenue-tool/.

[11] European Commission Special Eurobarometer 539, “Attitudes of Europeans towards tobacco and related products,” June, 2024, https://europa.eu/eurobarometer/surveys/detail/2995.

[12] Neal Benowitz, “Nicotine Addiction,” New England Journal of Medicine 362:24 (June 2010), https://doi.org/10.1056/NEJMra0809890.

[13] Joel Nitzkin, “The Case in Favor of E-Cigarettes for Tobacco Harm Reduction,” International Journal of Environmental Research and Public Health 11:6 (June 2014):6459-5471, https://doi.org/10.3390/ijerph110606459; Pasquale Caponnetto et al., “Efficiency and Safety of an electronic cigarette as Tobacco Cigarettes Substitute,” PLoS ONE 9:1 (June 2013), https://doi.org/10.1371/journal.pone.0066317; Public Health England, “E-cigarettes around 95% less harmful than tobacco estimates landmark review,” Aug. 19, 2015, https://www.gov.uk/government/news/e-cigarettes-around-95-less-harmful-than-tobacco-estimates-landmark-review; Konstantinos Farsalinos et al., “No Smoke, Less Harm,” Smoke Free Sweden, 2024, https://smokefreesweden.org/No%20Smoke%20Less%20Harm.pdf; and Derek Pope et al., “The Experimental Tobacco Marketplace: Demand and Substitutability as a Function of Cigarette Taxes and e-Liquid Subsidies,” Nicotine & Tobacco Research 22:5 (May 2020): 782-790, https://doi.org/10.1093/ntr/ntz116.

[14] US Centers for Disease Control and Prevention, “Smoking Cessation: Fast Facts,” https://www.cdc.gov/tobacco/php/data-statistics/smoking-cessation/.

[15] Kevin Volpp et al., “A Randomized, Controlled Trial of Financial Incentives for Smoking Cessation,” New England Journal of Medicine 360:7 (February 2009), https://doi.org/10.1056/NEJMsa0806819; and Jean-Francois Etter and Felicia Schmid, “Effects of Large Financial Incentives for Long-Term Smoking Cessation: A Randomized Trial,” Journal of the American College of Cardiology 68:8 (August 2016): 777-785, https://doi.org/10.1016/j.jacc.2016.04.066.

[16] US Food and Drug Administration, “Modified Risk Tobacco Products,” https://www.fda.gov/tobacco-products/advertising-and-promotion/modified-risk-tobacco-products; and US Food and Drug Administration, “Modified Risk Granted Orders,” June 11, 2024, https://www.fda.gov/tobacco-products/advertising-and-promotion/modified-risk-granted-orders.

[17] Royal College of Physicians, “Nicotine without smoke: Tobacco harm reduction,” Oct. 28, 2019, https://www.rcp.ac.uk/improving-care/resources/nicotine-without-smoke-tobacco-harm-reduction/.

[18] Public Health England, “E-cigarettes: an evidence update,” Aug. 19, 2015, https://www.gov.uk/government/publications/e-cigarettes-an-evidence-update.

[19] Business Standard, “16 member countries urge to include vapes in EU’s tobacco tax law,” Dec. 9, 2024, https://www.business-standard.com/world-news/16-member-countries-urge-to-include-vapes-in-eu-s-tobacco-tax-law-124120900261_1.html.

[20] European Parliament and the Council of the European Union, “Council Directive 2014/40/EU,” Apr. 3, 2014, https://health.ec.europa.eu/document/download/c4aa6f75-7e52-463b-badb-cbb6181b87c3_en?filename=dir_201440_en.pdf.

[21] Delon Human, Anders Milton, and Heino Stover, “Missing the Target,” Smoke Free Sweden, November 2024, https://smokefreesweden.org/wp-content/themes/smokefreesweden/assets/pdf/data/SFS_Missing%20the%20target_1%20Nov%202024.pdf.

[22] Smoke Free Sweden, “BREAKING NEWS: Swedes first in world to become smoke free – it’s a lesson for the world,” Nov. 13, 2024, https://smokefreesweden.org/2024/11/13/breaking-news-swedes-first-in-world-to-become-smoke-free-its-a-lesson-for-the-world/.

[23] Camille Bello, “Smoking in Europe: Which countries are the most and least addicted to tobacco and vaping?” Euronews, Aug. 14, 2023, https://www.euronews.com/health/2023/08/14/smoking-in-europe-which-countries-are-the-most-and-least-addicted-to-tobacco-and-vaping; Delon Human, Anders Milton, and Karl Fagerstrom, “The Swedish Experience: A Roadmap to a Smoke Free Society,” Smoke Free Sweden, 2023, https://smokefreesweden.org/wp-content/themes/smokefreesweden/assets/pdf/reports/Report%20The%20Swedish%20Experience%20EN.pdf; and The Snus Commission, “Snus saves lives: A study of snus and tobacco-related mortality in the EU,” June 2017, https://snusforumet.se/wp-content/uploads/2017/05/Snuskommissionen_rapport3_eng_PRINT.pdf

[24] Royal College of Physicians, “Nicotine without smoke: Tobacco harm reduction,” Oct. 28, 2019, https://www.rcp.ac.uk/improving-care/resources/nicotine-without-smoke-tobacco-harm-reduction/; Scientific Committee on Emerging and Newly Identified Health Risks, Health effects of smokeless tobacco products (Brussels: European Commission, 2008); and Jennifer Maki, “The incentives created by a harm reduction approach to smoking cessation: Snus and smoking in Sweden and Finland,” International Journal on Drug Policy 26:6 (August 2014):569-574, https://doi.org/10.1016/j.drugpo.2014.08.003.

[25] Erica Sjodin et al., “Thirty-six-year trends (1986-2022) in cigarette smoking and snus use in northern Sweden: a cross-sectional study,” BMJ Open 14 (2024), https://doi.org/10.1136/bmjopen-2024-088162.

[26] The Snus Commission, “Snus saves lives: A study of snus and tobacco-related mortality in the EU.”

[27] Mikael Damberg, “Excise duties on nicotine-containing consumer products after 2023,” Sveriges Riksdag, Apr. 27, 2022, https://www.riksdagen.se/sv/dokument-och-lagar/dokument/svar-pa-skriftlig-fraga/punktskatter-pa-nikotininnehallande_H9121477/.

[28] Tobacco Advisory Group, “Nicotine without smoke: Tobacco harm reduction,” Royal College of Physicians, April 2016, https://www.rcp.ac.uk/media/xcfal4ed/nicotine-without-smoke_0.pdf; and Jennifer Maki, “The incentives created by a harm reduction approach to smoking cessation: Snus and smoking in Sweden and Finland.”

[29] Delon Human, Anders Milton, and Heino Stover, “Missing the Target.”

[30] Global State of Tobacco Harm Reduction, “Smoking, vaping, HTP, NRT, and snus in Estonia,” Knowledge•Action•Change, 2024, https://gsthr.org/countries/profile/est/.

[31] European Commission Special Eurobarometer 539, “Attitudes of Europeans towards tobacco and related products,” June, 2024, https://europa.eu/eurobarometer/surveys/detail/2995.

[32] Belga News Agency, “Total ban on nicotine pouches in Belgium from 1 October,” Sept. 27, 2023, https://www.belganewsagency.eu/total-ban-on-nicotine-pouches-in-belgium-from-1-october; and Sylvain Plazy and Mark Carlson, “Belgium will ban sales of disposable e-cigarettes in a first for the EU,” Associated Press, Dec. 29, 2024, https://apnews.com/article/eu-belgium-vapes-cigarettes-health-environment-7726f7852994e9d4911ea9ce94b25e7a.

[33] Ireland’s National Public Service Media, “New excise duty on vapes and €1 rise on 20 cigarettes,” Raidio Teilifis Eireann, Oct. 1, 2024, https://www.rte.ie/news/budget-2025/2024/1001/1472997-new-excise-duty-on-vapes-and-1-rise-on-20-cigarettes/; and Micheal Lehane, “Cabinet approves ban on sale of disposable vapes,” Raidio Teilifis Eirann, Sept. 11, 2024, https://www.rte.ie/news/politics/2024/0910/1469226-vapes/.

[34] Ali Anderson, “Czech Republic to ban flavoured vapes and hike tax,” Clearing the Air, Sept. 10, 2024, https://clearingtheair.eu/en/post/czech-republic-to-ban-flavoured-vapes-and-hike-tax/.

[35] Harriet Hadnum, “The Global Impact of GDPR: How Its Influenced Privacy Laws Worldwide,” GlobalAILaw, https://globalailaw.com/the-global-impact-of-gdpr-how-its-influenced-privacy-laws-worldwide/; and Ampcus Cyber, “What is GDPR? A Complete Guide to GDPR Understanding & Compliance,” Feb. 14, 2025, https://www.ampcuscyber.com/knowledge-hub/what-is-gdpr/.

Share this article