Pass-through businesses, such as sole proprietorships, S corporations, and partnerships, make up a majority of businesses in the United States. The owners of these firms pay individual income tax on income derived from these businesses. The marginal tax rates vary for pass-through firms depending on the state where they operate, as states tax individual income differently.

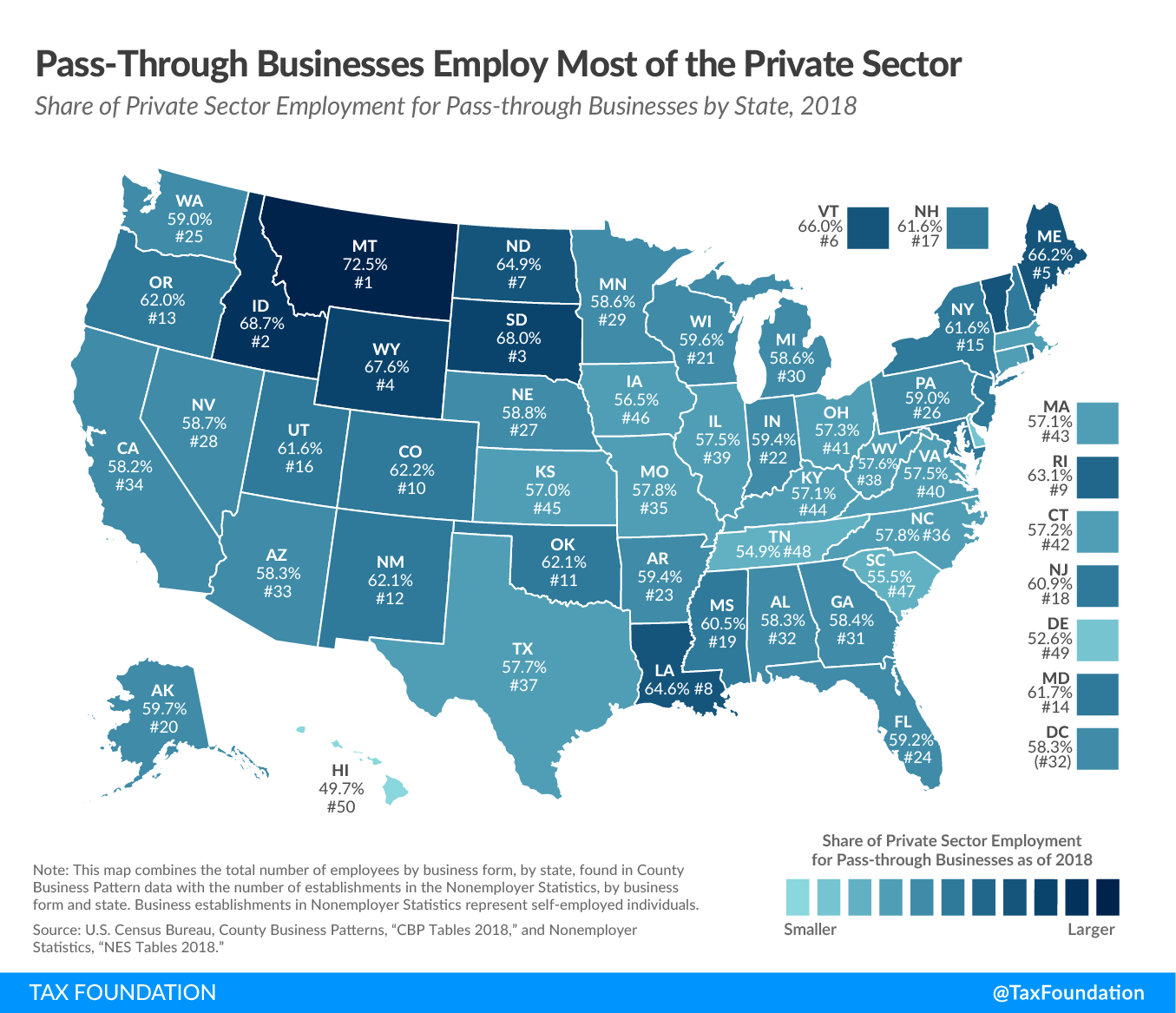

In 2018, pass-through firms made up over half of nearly every state’s private sector employment. The share of private sector employment provided by pass-through firms ranges from 49.7 percent in Hawaii to 72.5 percent in Montana.

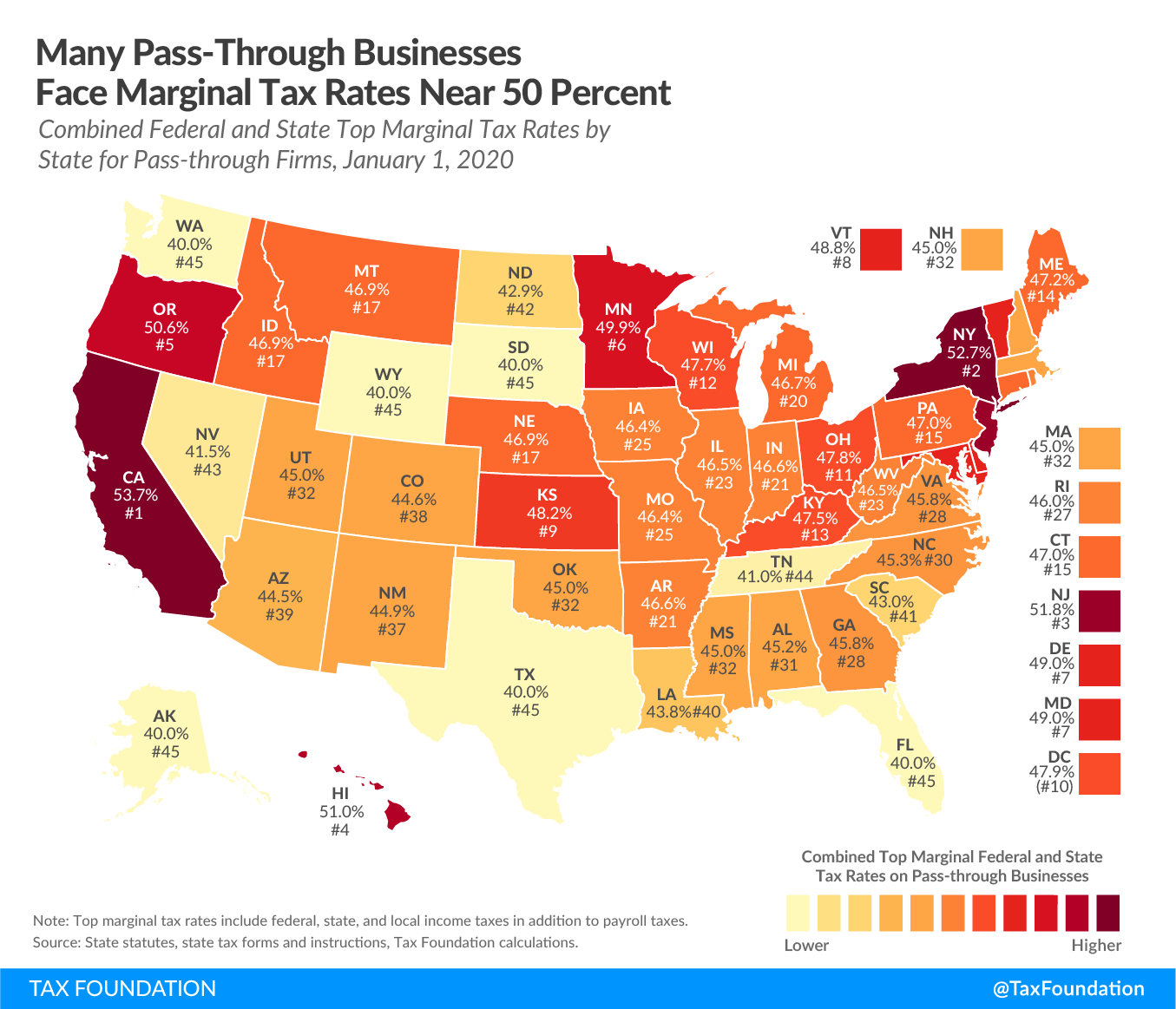

Top marginal taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. rates faced by pass-through firms also vary by state, ranging from 40 percent in states with no state and local income tax, like Wyoming and Florida, to 53.7 percent in California. These combined rates include federal, state, and local income taxes in addition to payroll tax.

A driver of variation in top marginal income tax rates faced by pass-through firms is whether a state taxes individual income and what the top marginal rate is. For example, states without individual income taxes, such as Alaska, Florida, South Dakota, Texas, Washington, and Wyoming, apply lower combined income tax rates on pass-through firms.

By contrast, states like California (with a 13.3 percent top marginal individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source rate) and New York (with a top marginal rate of 8.82 percent) subject pass-through firms to top combined marginal rates exceeding 50 percent. (Nevada does not have an individual income tax but has an uncapped payroll taxA payroll tax is a tax paid on the wages and salaries of employees to finance social insurance programs like Social Security, Medicare, and unemployment insurance. Payroll taxes are social insurance taxes that comprise 24.8 percent of combined federal, state, and local government revenue, the second largest source of that combined tax revenue. called the modified business tax that is levied on wages at a rate of 1.475 percent, which increases its top tax rate for pass-through businesses.)

Three states—Alabama, Iowa, and Louisiana—allow taxpayers to deduct a portion of their federal taxes paid from their taxable income. This reduces the amount of income subject to state income tax and lowers the top marginal rate faced by pass-throughs. Other states, such as Missouri, permit some deductibility but limitations to the deduction mean the top marginal rate is not affected.

Most of a pass-through firm’s tax burden is from federal income and payroll taxes. Pass-through firms must remit payroll taxes to fund programs such as Social Security and Medicare in addition to paying federal individual income tax with a top rate of 37 percent.

Qualifying pass-through firms may use Section 199A, commonly known as the pass-through deduction, to deduct 20 percent of their qualified business income from federal income tax. However, the pass-through deduction is subject to limitations for firms earning above certain income limits that operate in a “specified service trade or business” (SSTB) and other guardrails that limit the size of the deduction. This means that many pass throughs are not eligible for Section 199A and face top marginal income tax rates without it.

Pass-through firms make up a large part of the American economy and workforce, providing over half of private sector employment in nearly every state. The combined top marginal tax rateThe marginal tax rate is the amount of additional tax paid for every additional dollar earned as income. The average tax rate is the total tax paid divided by total income earned. A 10 percent marginal tax rate means that 10 cents of every next dollar earned would be taken as tax. faced by these firms is a product of federal, state, and local individual income taxes. Policymakers should keep in mind the combined tax burden levied on these businesses when considering changes to tax policy.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

Subscribe