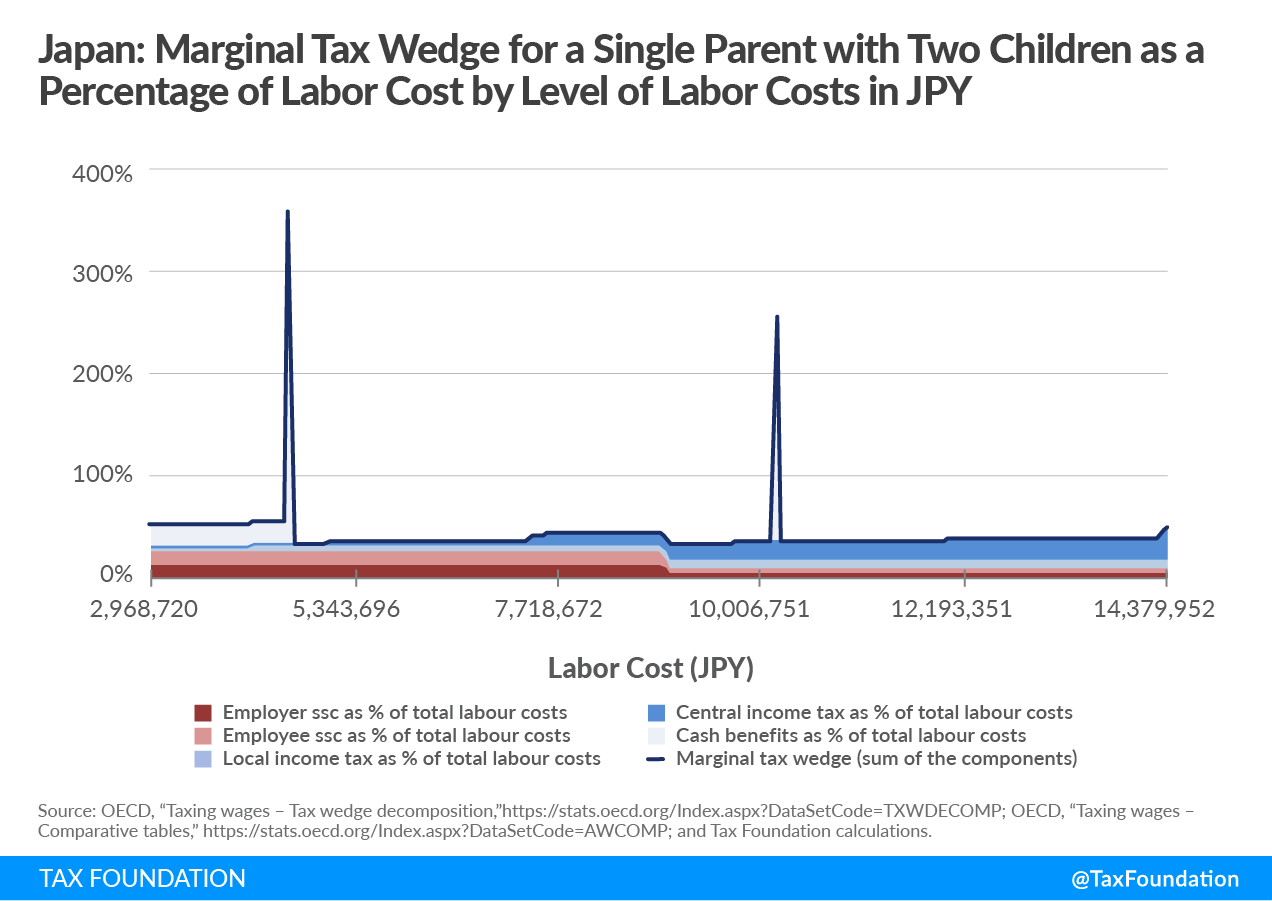

Imagine that a government provides subsidies to single parents that actually increase taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. rates on additional work. This is the case for a Japanese single parent who earns a rough equivalent of US $39,981 and faces a 57 percent marginal tax rate. With just a small increase in pay of $599, she would face a 359 percent marginal tax rateThe marginal tax rate is the amount of additional tax paid for every additional dollar earned as income. The average tax rate is the total tax paid divided by total income earned. A 10 percent marginal tax rate means that 10 cents of every next dollar earned would be taken as tax. . A Japanese parent who benefits from a government program worth $5,123 might lose 100 percent of that benefit if he or she earns above the earnings threshold.

This is why the marginal tax wedgeBroadly speaking, a tax wedge is the difference between the pre-tax price or return and after-tax price or return. For labor income, it is the difference between the total labor costs to the employer and the corresponding net take-home pay of the employee. is relevant for understanding how workers might benefit (or not) from an increase in pay once taxes enter the picture.

While the tax and benefit system can be successful in keeping low-income working households out of poverty and encouraging workforce participation, high marginal tax rates like the one observed in the case of this Japanese working parent act as barriers to upward mobility, discouraging parents from advancing in their careers. Very often these high rates are hidden in complex tax structures. However, a recently published study by Archbridge Institute and Tax Foundation highlights the underlying policies that drive the marginal tax rate spikes that workers are subject to in a number of countries.

When moving up the income ladder a Japanese worker with children can face tax rate spikes of over 250 percent at two different points due to the child-rearing allowance and child benefits.

| Japanese Single Parent with Two Children Average Labor Cost: JPY 5,937,440 (US $59,899) | ||

|---|---|---|

| Total Labor Cost | JPY 4,571,829 | JPY 10,170,746 |

| Net Earnings Before the Raise | JPY 3,562,284 | JPY 6,778,705 |

| Amount of the Raise | JPY 59,374 | JPY 54,665 |

| Amount of Additional Tax/Benefits Reduction Due to the Raise | JPY 213,227 | JPY 140,751 |

| % of the Raise Eaten up by the MTR | 359.12% | 257.48% |

| Net Earnings After the Raise | JPY 3,408,432 | JPY 6,692,619 |

| Source: OECD, “Taxing wages – Tax wedge decomposition,” https://stats.oecd.org/Index.aspx?DataSetCode=TXWDECOMP; OECD, “Taxing wages – Comparative tables,” https://stats.oecd.org/Index.aspx?DataSetCode=AWCOMP; and Tax Foundation calculations. | ||

In 2021, the first marginal tax rate spike occurred at 77 percent of the average wage and approximately 88 percent of the median wage. If the employer of this Japanese worker increased compensation by just JPY 59,374, the worker faced a net loss and saw his earnings cut by JPY 153,853. This Japanese parent faced a marginal tax wedge of 359 percent for a 1 percent increase in gross earnings on top of the gross annual wage of JPY 3,963,097. This is because the child-rearing allowance, which is a benefit available for single parents, disappears at the income cap.

Moving up the income ladder this worker faced a marginal tax wedge of 257 percent for a 1 percent increase in gross earnings on top of the gross annual wage of JPY 8,904,101. This Japanese single parent faced a net loss and saw his earnings cut by JPY 86,086. This is due to child benefits being cut by half from JPY 240,000 to JPY 120,000 when the cap of JPY 6,980,000 is reached.

Both the child-rearing allowance and the child benefit generate marginal tax rate spikes of over 250 percent as they reach the income cap. A gradual fading of these benefits would eliminate these tax spikes.

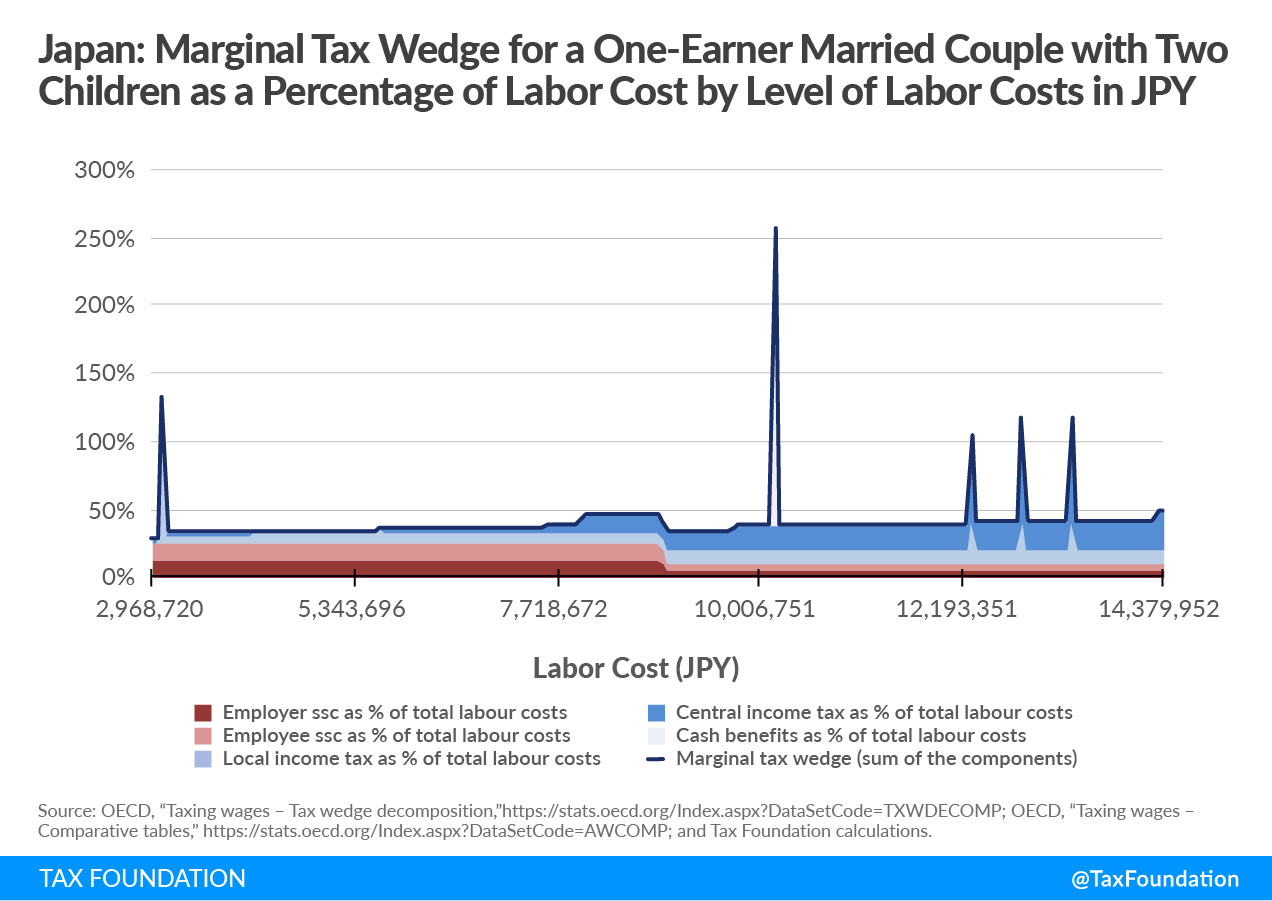

Additionally, a one-earner Japanese couple with two children faced marginal tax rates of over 100 percent at five different points due to the child allowance, but also due to local fixed standard tax and spouse’s allowance.

| Japanese One-Earner Married Couple with Two Children Average Labor Cost: JPY 5,937,440 (US $59,899) | |||||

|---|---|---|---|---|---|

| Total Labor Cost | JPY 3,087,469 | JPY 10,170,746 | JPY 12,302,681 | JPY 12,849,331 | JPY 13,395,981 |

| Net Earnings Before the Raise | JPY 2,496,730 | JPY 6,889,301 | JPY 8,091,945 | JPY 8,381,282 | JPY 8,663,965 |

| Amount of the Raise | JPY 59,374 | JPY 54,665 | JPY 54,665 | JPY 54,665 | JPY 54,665 |

| Amount of Additional Tax/Benefits Reduction Due to the Raise | JPY 79,334 | JPY 140,751 | JPY 57,116 | JPY 63,772 | JPY 63,772 |

| % of the Raise Eaten Up by the MTR | 133.62% | 257.48% | 104.48% | 116.66% | 116.66% |

| Net Earnings After the Raise | JPY 2,476,770 | JPY 6,803,215 | JPY 8,089,493 | JPY 8,372,176 | JPY 8,654,858 |

| Source: OECD, “Taxing wages – Tax wedge decomposition,” https://stats.oecd.org/Index.aspx?DataSetCode=TXWDECOMP; OECD, “Taxing wages – Comparative tables,” https://stats.oecd.org/Index.aspx?DataSetCode=AWCOMP; and Tax Foundation calculations. | |||||

For this couple, the first marginal tax rate spike occurred at 52 percent of the average wage and approximately 60 percent of the median wage. If the employer of this Japanese worker increased compensation by just JPY 59,374, the worker faced a net loss and saw his earnings cut by JPY 19,960. This Japanese couple faced a marginal tax wedge of 134 percent for a 1 percent increase in gross earnings on top of the gross annual wage of JPY 2,676,377. This is because at this level of income, in addition to the local fixed standard tax of JPY 5,000, a 10 percent local income tax is due.

The second marginal tax rate spike that this Japanese couple faced was due to the cap on child benefits, as in the case of a single parent with two children.

Moving up the income ladder this worker faced a marginal tax wedge of 104 percent for a 1 percent increase in gross earnings on top of the gross annual wage of JPY 10,911,384. This Japanese couple with two children faced a net loss and saw their earnings cut by JPY 2,451.

This Japanese couple with two children faced two more marginal tax wedges of 117 percent for a 1 percent increase in gross earnings on top of the gross annual wage of JPY 11,426,072 and JPY 11,940,760. These last three increases in the marginal tax wedge generated by the increase in income taxes are due to the gradual loss of the spouse’s allowance by one-third of its initial amount until it is completely withdrawn. Therefore, a gradual reduction of the spouse allowance would drastically reduce these three marginal tax rate spikes.

The tax and benefit system in Japan is extremely complex with numerous thresholds. Additionally, the existence of different tax benefits and thresholds for single parents and one-earner couples generates a series of marginal tax rates that might keep some workers in Australia just below the threshold earnings that trigger the tax rate spikes. Eliminating these barriers by implementing a more homogenous tax and benefit system will allow workers to have access to higher wages without confronting these barriers.

Additionally, the various levels of income tax and the design of the local income tax create a poverty trap for one-earner couples. In order to eliminate this poverty trap, the fixed standard local tax needs to be eliminated and regional and local income tax rates and thresholds need to be aligned.

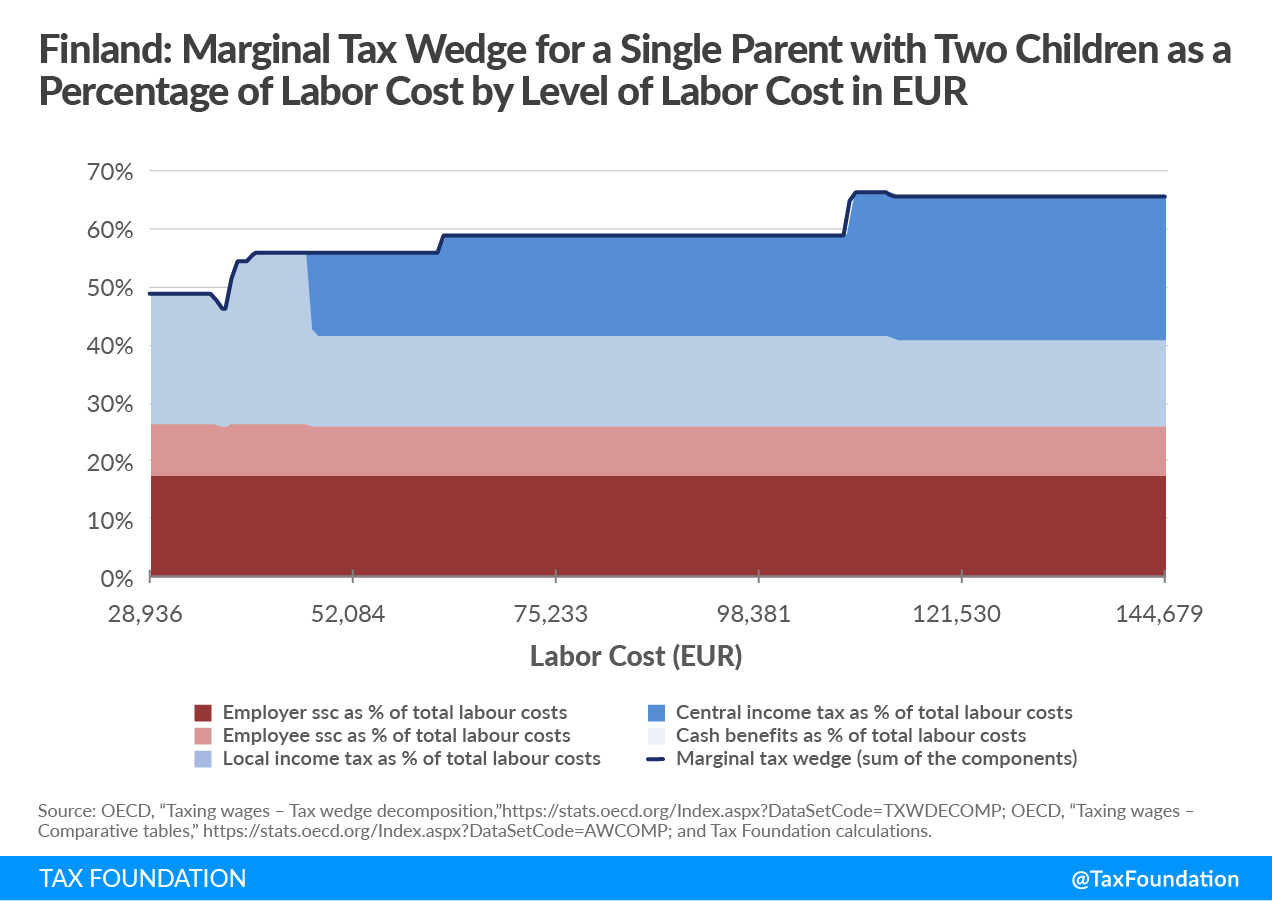

Two Lessons from Finland

Japan could follow the example of Finland where both central and local income taxes operate together. In Finland, the local income tax and the central income tax are adjusted and well-coordinated and do not generate marginal tax rate spikes like the ones described in Japan. Finland also offers a fixed child allowance independent of taxable income that prevents the formation of marginal tax rate spikes like the ones observed in Japan. Nevertheless, marginal tax rates above 50 percent as the ones observed in Finland might discourage employment and labor supply. Even if marginal rates do not spike in a way that traps people in poverty, high marginal rates still impact workers directly.

Finland. Marginal Tax Wedge for a Single Parent with Two Children as a Percentage of Labor Cost by Level of Labor Cost in EUR

The loss in benefits that especially Japanese single parents and one-earner couples face when taking on additional work hours can deter them from advancing in their careers, showing that the tax-benefit system is inefficient in promoting the upward mobility of parents. The Japanese tax and benefit system comes with trade-offs that policymakers must keep in mind when planning to reform the tax policy. In Japan, even close to poverty-level parents are impacted by marginal tax rate spikes. Therefore, reshaping some of these policies to generate a smoother variation of marginal tax rates over different income levels and household types would likely raise labor supply and encourage the upward mobility of Japanese parents.

Note: This is part of a five-part blog series that highlights the findings of a recently published study by Archbridge Institute and Tax Foundation and explores the underlying policies that drive the marginal tax rate spikes that workers are subject to in a number of countries.