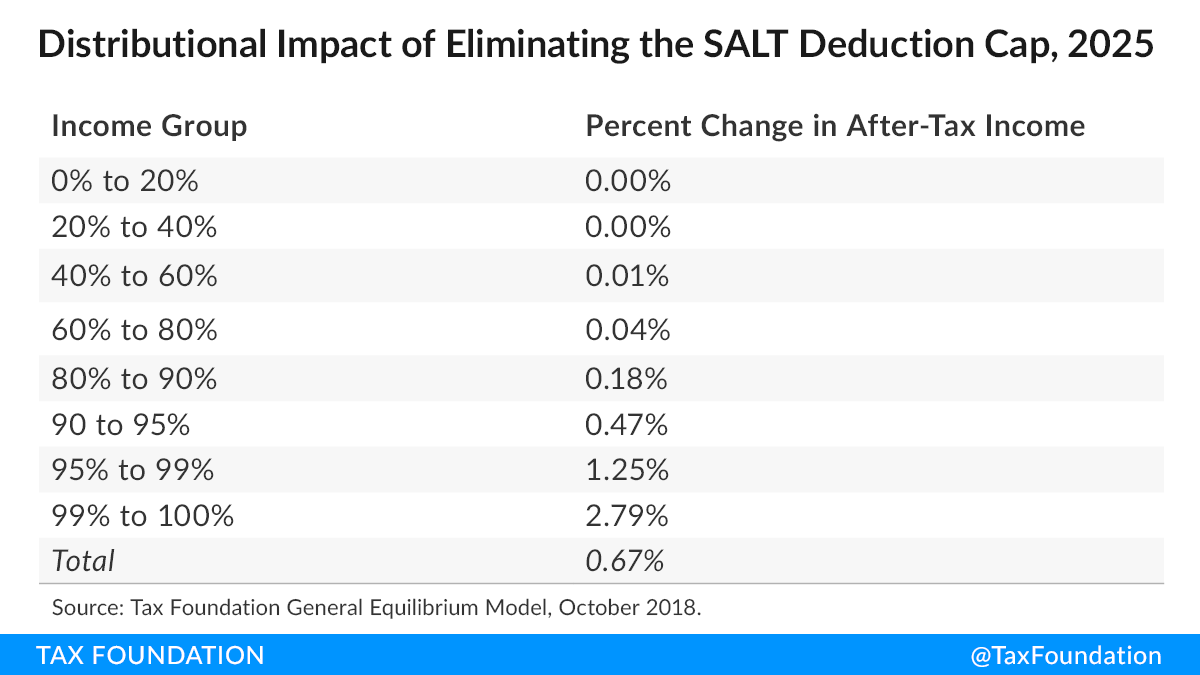

As President Joe Biden and policymakers in Congress consider changes in taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. policy over the coming year, the fate of the $10,000 state and local tax (SALT) deduction cap will be an ongoing part of the policy debate. Senate Majority Leader Chuck Schumer (D-NY) has expressed interest in repealing the SALT cap, which was originally imposed as part of the Tax Cuts and Jobs Act (TCJA) in late 2017.

It is important to understand who benefits from the SALT deduction as it currently exists, and who would benefit from the deduction if the SALT cap were repealed.

The Internal Revenue Service (IRS) has provided data on state and local taxes paid and deducted for tax year 2018, the first year the SALT cap went into effect.

The value of the SALT deduction as a percentage of adjusted gross incomeFor individuals, gross income is the total pre-tax earnings from wages, tips, investments, interest, and other forms of income and is also referred to as “gross pay.” For businesses, gross income is total revenue minus cost of goods sold and is also known as “gross profit” or “gross margin.” (AGI) tends to increase with a taxpayer’s income. Since the SALT cap was put into place, however, very high earners have seen a sharp reduction in the deduction as a percent of AGI, from 7.7 percent in 2016 for those earning over $500,000 to 0.71 percent in 2018. The value dropped so significantly because the deduction remains at a maximum value of $10,000 even if AGI and state and local taxes rise beyond that amount.

Some higher-income earners still disproportionately benefit from the SALT deduction, however: those earning between $100,000 and $499,999 had average SALT deductions of 1.75 percent of AGI, compared to 0.56 percent for those earning under $25,000.

| Adjusted Gross Income (AGI) | State and Local Tax Deduction Value as Percent of AGI | Percentage of Filer Itemizing |

|---|---|---|

| $0 to $24,999 | 0.56% | 1.8% |

| $25,000 to $49,999 | 0.65% | 4.8% |

| $50,000 to $99,999 | 1.29% | 13.7% |

| $100,000 to $499,999 | 1.75% | 32.1% |

| $500,000+ | 0.71% | 70.0% |

|

Source: Internal Revenue Service, “Statistics of Income Tax Stats, Tax Year 2018: Historic Table 2, ‘Total File, All States,’” https://www.irs.gov/statistics/soi-tax-stats-historic-table-2, and author’s calculations. |

||

Higher earners tend to itemize more often, rather than taking the standard deductionThe standard deduction reduces a taxpayer’s taxable income by a set amount determined by the government. It was nearly doubled for all classes of filers by the 2017 Tax Cuts and Jobs Act (TCJA) as an incentive for taxpayers not to itemize deductions when filing their federal income taxes. . More taxpayers took the standard deduction in 2018 than did in 2016 due to the TCJA’s doubling of the standard deduction. For example, in 2016, 80.2 percent of those earning between $100,000 and $499,999 itemized. In 2018, only 32.1 percent of those filers itemized. The expansion of the standard deduction further limited the value of the SALT deduction for taxpayers under the $10,000 cap.

The SALT deduction tends to benefit states with many higher-earners and higher state taxes. This was true prior to the SALT deduction cap and remained the case in 2018. Seven states—California, New York, Texas, New Jersey, Maryland, Illinois, and Florida—claimed more than half of the value of all SALT deductions nationwide in 2018. California alone was responsible for 19.8 percent of all SALT deductions in the U.S., close to its 2016 share of 20.7 percent.

| State | Deduction as Percent of AGI | State Share | AGI Per Filer | Percent of Itemizers | |

|---|---|---|---|---|---|

| Top States (and D.C.) | Maryland | 2.50% | 4.20% | $82,105 | 24.03% |

| District of Columbia | 1.84% | 0.46% | $105,458 | 22.27% | |

| Virginia | 1.80% | 4.00% | $81,989 | 17.71% | |

| California | 1.80% | 19.86% | $89,234 | 17.69% | |

| New Jersey | 1.79% | 4.96% | $91,132 | 16.97% | |

| Oregon | 1.71% | 1.64% | $71,707 | 14.57% | |

| Hawaii | 1.61% | 0.51% | $67,444 | 13.93% | |

| Utah | 1.60% | 1.07% | $72,167 | 14.80% | |

| Georgia | 1.55% | 3.28% | $67,925 | 13.84% | |

| New York | 1.53% | 9.06% | $89,384 | 12.43% | |

| Bottom States | Ohio | 0.82% | 2.00% | $64,256 | 6.70% |

| Florida | 0.81% | 4.16% | $73,565 | 9.02% | |

| Nevada | 0.81% | 0.59% | $73,539 | 9.89% | |

| Indiana | 0.75% | 1.00% | $62,150 | 6.10% | |

| Tennessee | 0.60% | 0.81% | $64,782 | 6.69% | |

| Alaska | 0.59% | 0.10% | $72,150 | 7.66% | |

| West Virginia | 0.59% | 0.17% | $55,040 | 4.32% | |

| South Dakota | 0.48% | 0.09% | $67,743 | 5.26% | |

| North Dakota | 0.44% | 0.08% | $73,050 | 5.56% | |

| Wyoming | 0.44% | 0.07% | $80,208 | 6.45% | |

|

Source: Internal Revenue Service, “Statistics of Income Tax Stats, Tax Year 2018: Historic Table 2, ‘Total File, All States,’” https://www.irs.gov/statistics/soi-tax-stats-historic-table-2, and author’s calculations. |

|||||

Overall, the SALT deduction’s value as a portion of AGI fell between 2016 and 2018. In California, the deduction’s value fell from 8.1 percent in 2016 to just 1.8 percent in 2018. The state with the largest amount of SALT deductions as a portion of AGI in 2016 was New York at 9.4 percent. In 2018, Maryland was the top state at 2.5 percent of AGI. The decline from 2016 to 2018 was driven by the SALT deduction cap and, to a lesser extent, the drop in itemization due to the doubling of the standard deduction.

States with fewer SALT deductions also experienced a decline—the average deduction as a portion of AGI for the bottom 10 states fell from 2.33 percent of AGI in 2016 to 0.63 percent in 2018.

| State | Deduction as Percent of AGI | State Share | AGI Per Filer | Percent of Itemizers |

|---|---|---|---|---|

| Alabama | 0.87% | 0.74% | $60,336 | 8.55% |

| Alaska | 0.59% | 0.10% | $72,150 | 7.66% |

| Arizona | 1.08% | 1.54% | $67,798 | 10.95% |

| Arkansas | 0.82% | 0.42% | $61,340 | 6.93% |

| California | 1.80% | 19.86% | $89,234 | 17.69% |

| Colorado | 1.23% | 1.91% | $82,401 | 13.50% |

| Connecticut | 1.46% | 1.77% | $100,599 | 15.15% |

| Delaware | 1.23% | 0.28% | $70,371 | 11.73% |

| District Of Columbia | 1.84% | 0.46% | $105,458 | 22.27% |

| Florida | 0.81% | 4.16% | $73,565 | 9.02% |

| Georgia | 1.55% | 3.28% | $67,925 | 13.84% |

| Hawaii | 1.61% | 0.51% | $67,444 | 13.93% |

| Idaho | 1.03% | 0.35% | $63,480 | 8.95% |

| Illinois | 1.29% | 4.28% | $79,989 | 11.26% |

| Indiana | 0.75% | 1.00% | $62,150 | 6.10% |

| Iowa | 0.86% | 0.57% | $66,613 | 7.53% |

| Kansas | 0.96% | 0.60% | $68,863 | 8.12% |

| Kentucky | 0.86% | 0.67% | $59,776 | 6.58% |

| Louisiana | 0.82% | 0.67% | $60,821 | 7.76% |

| Maine | 0.98% | 0.27% | $61,601 | 7.36% |

| Maryland | 2.50% | 4.20% | $82,105 | 24.03% |

| Massachusetts | 1.38% | 3.25% | $99,066 | 14.72% |

| Michigan | 0.95% | 2.06% | $66,504 | 7.63% |

| Minnesota | 1.24% | 1.84% | $77,816 | 11.25% |

| Mississippi | 0.92% | 0.39% | $51,426 | 7.67% |

| Missouri | 0.93% | 1.15% | $65,096 | 7.75% |

| Montana | 1.05% | 0.23% | $62,452 | 8.91% |

| Nebraska | 0.88% | 0.36% | $67,117 | 7.63% |

| Nevada | 0.81% | 0.59% | $73,539 | 9.89% |

| New Hampshire | 1.00% | 0.39% | $81,177 | 9.91% |

| New Jersey | 1.79% | 4.96% | $91,132 | 16.97% |

| New Mexico | 0.88% | 0.31% | $56,147 | 7.28% |

| New York | 1.53% | 9.06% | $89,384 | 12.43% |

| North Carolina | 1.18% | 2.46% | $66,292 | 10.29% |

| North Dakota | 0.44% | 0.08% | $73,050 | 5.56% |

| Ohio | 0.82% | 2.00% | $64,256 | 6.70% |

| Oklahoma | 0.88% | 0.61% | $62,598 | 8.13% |

| Oregon | 1.71% | 1.64% | $71,707 | 14.57% |

| Pennsylvania | 1.02% | 3.12% | $72,045 | 8.87% |

| Rhode Island | 1.32% | 0.34% | $69,431 | 10.59% |

| South Carolina | 1.13% | 1.09% | $62,220 | 9.49% |

| South Dakota | 0.48% | 0.09% | $67,743 | 5.26% |

| Tennessee | 0.60% | 0.81% | $64,782 | 6.69% |

| Texas | 0.95% | 6.01% | $73,288 | 9.20% |

| United States | 1.26% | 100.00% | $75,778 | 11.47% |

| Utah | 1.60% | 1.07% | $72,167 | 14.80% |

| Vermont | 0.92% | 0.13% | $64,695 | 7.15% |

| Virginia | 1.80% | 4.00% | $81,989 | 17.71% |

| Washington | 1.15% | 2.54% | $89,906 | 13.43% |

| West Virginia | 0.59% | 0.17% | $55,040 | 4.32% |

| Wisconsin | 0.95% | 1.27% | $68,428 | 7.77% |

| Wyoming | 0.44% | 0.07% | $80,208 | 6.45% |

|

Source: Internal Revenue Service, “Statistics of Income Tax Stats, Tax Year 2018: Historic Table 2, ‘Total File, All States,’” https://www.irs.gov/statistics/soi-tax-stats-historic-table-2, and author’s calculations. Includes District of Columbia. |

||||

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe