About the Author

Cristina Enache writes on the economics of tax policy and is the author of the Spanish Regional Tax Competitiveness Index. She was formerly the Director of Research at Civismo, an economic research organization based in Spain. She also served as head of research at Institución Futuro, a regional think tank based in Navarra in northern Spain. She is also currently Secretary-General at the World Taxpayers Associations and General Manager of the Spanish Taxpayers Union, which she joined in 2016.

Previous Versions

-

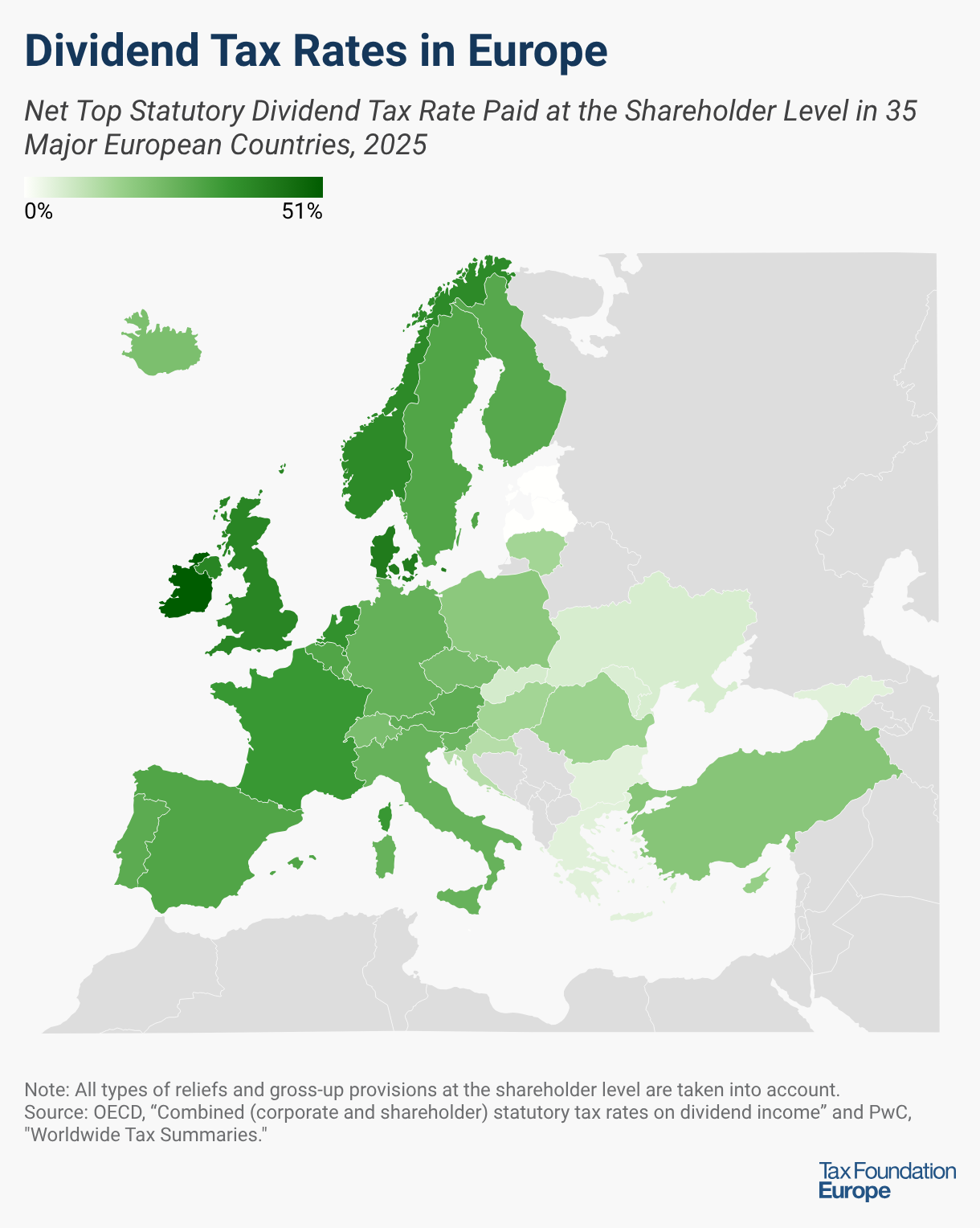

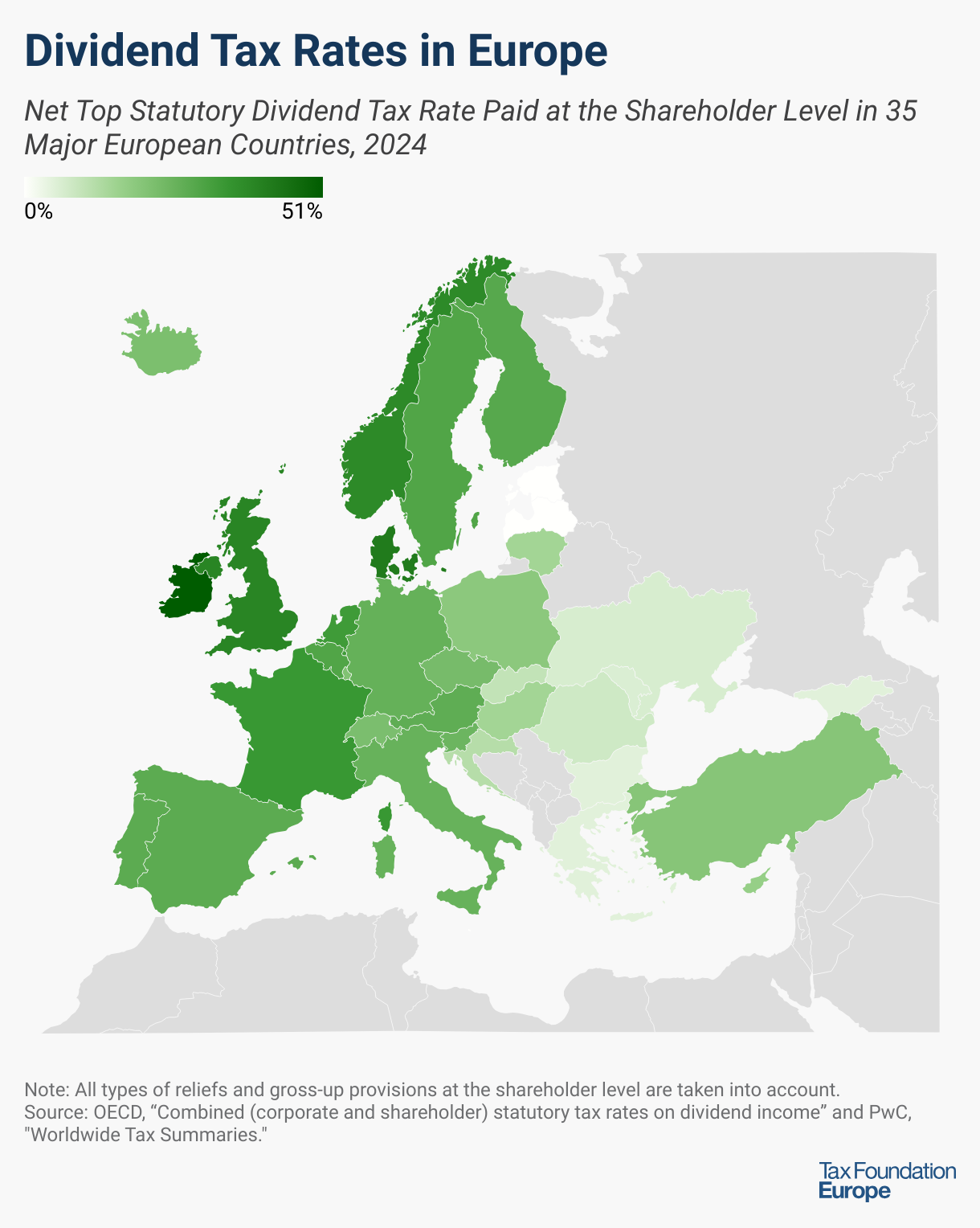

Dividend Tax Rates in Europe, 2024

2 min read -

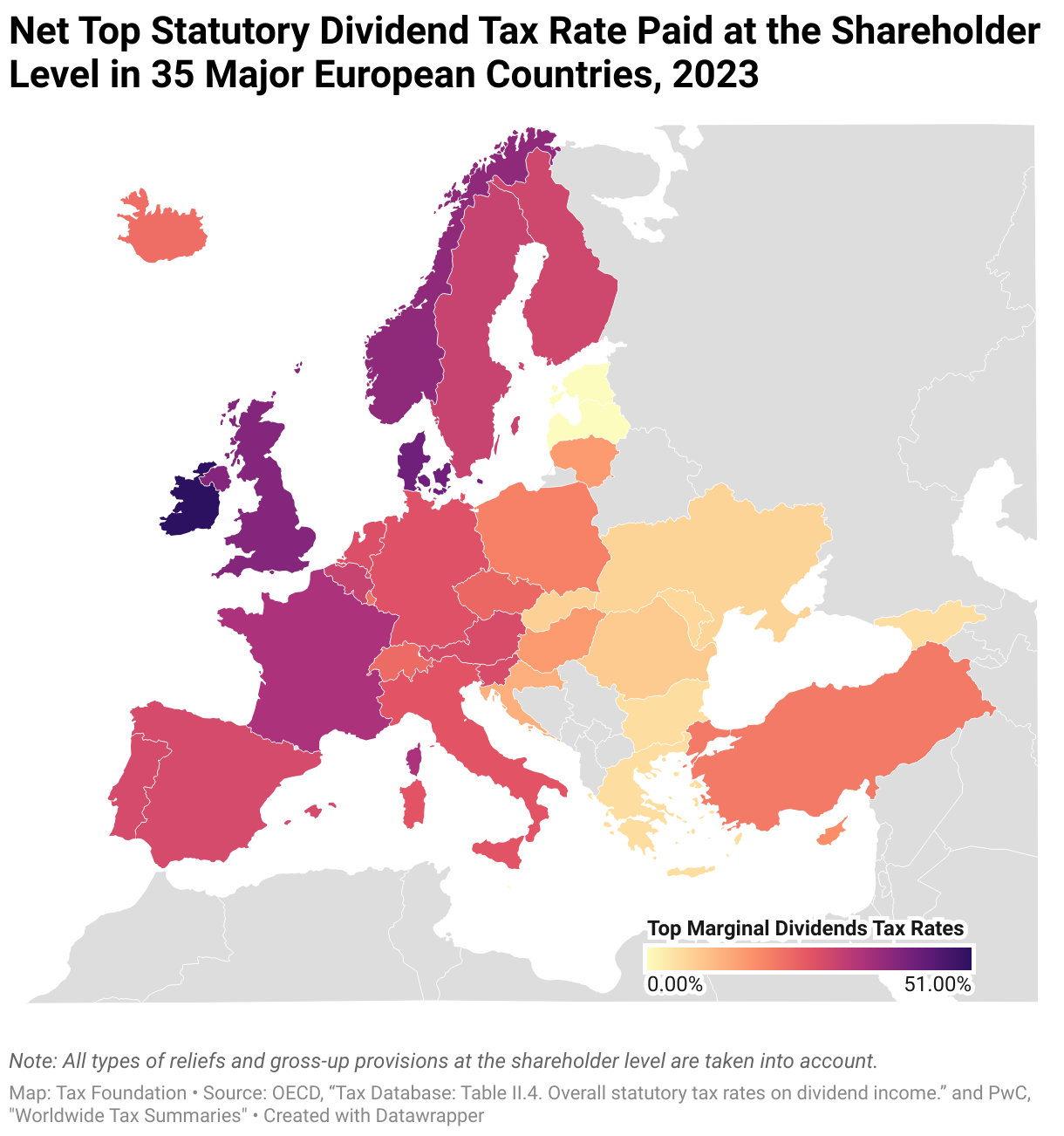

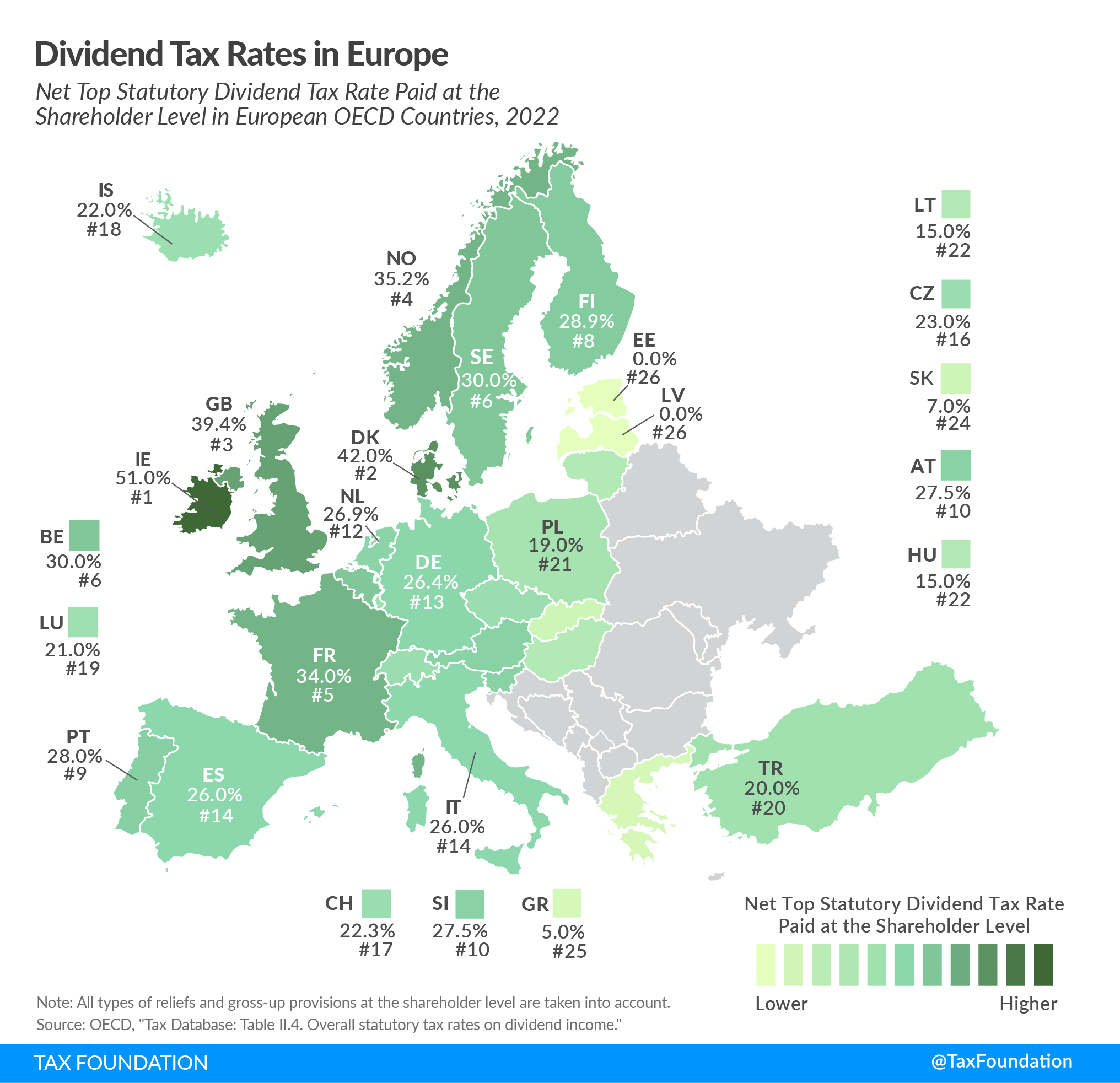

Dividend Tax Rates in Europe, 2023

3 min read -

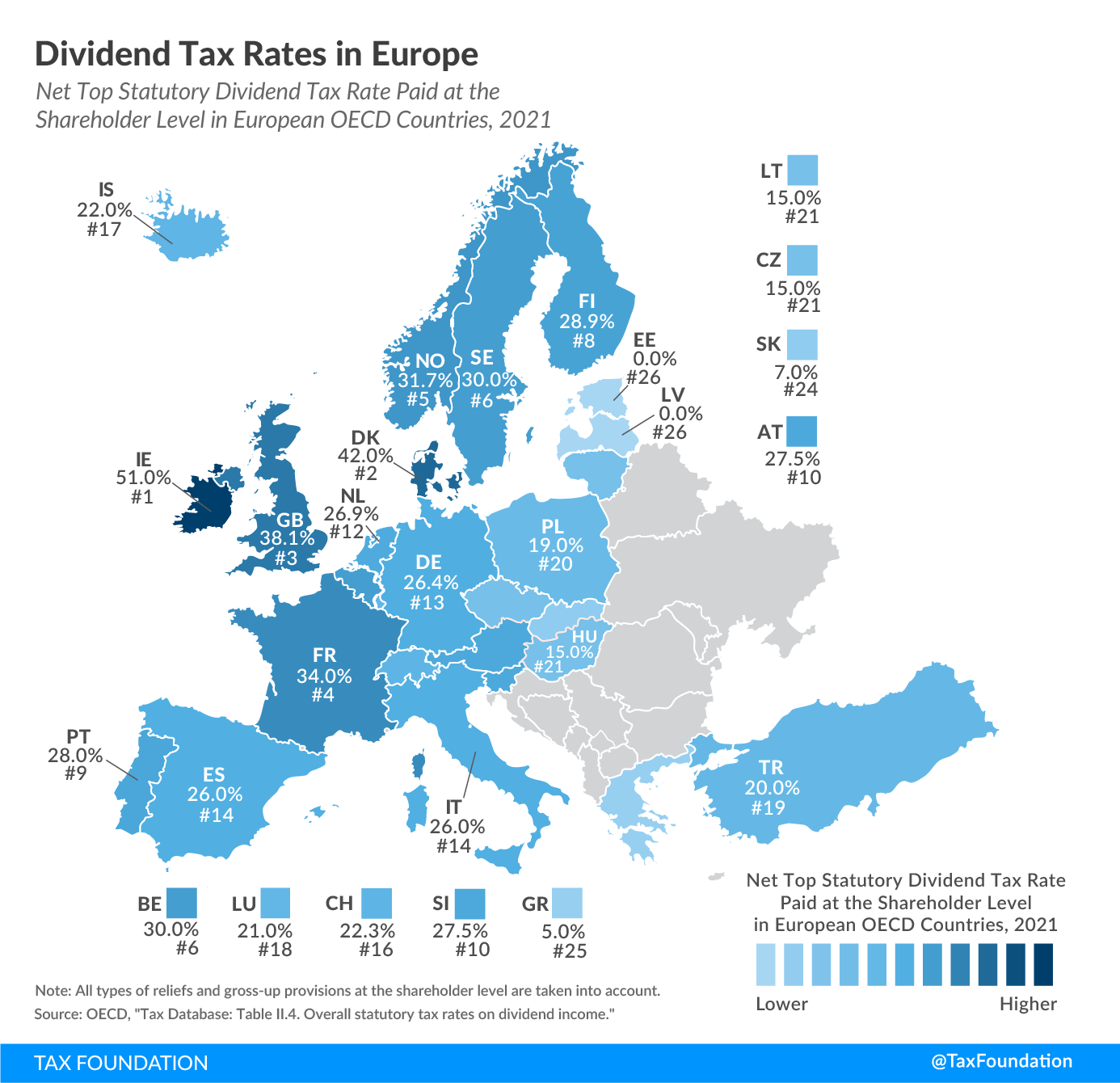

Dividend Tax Rates in Europe, 2021

2 min read -

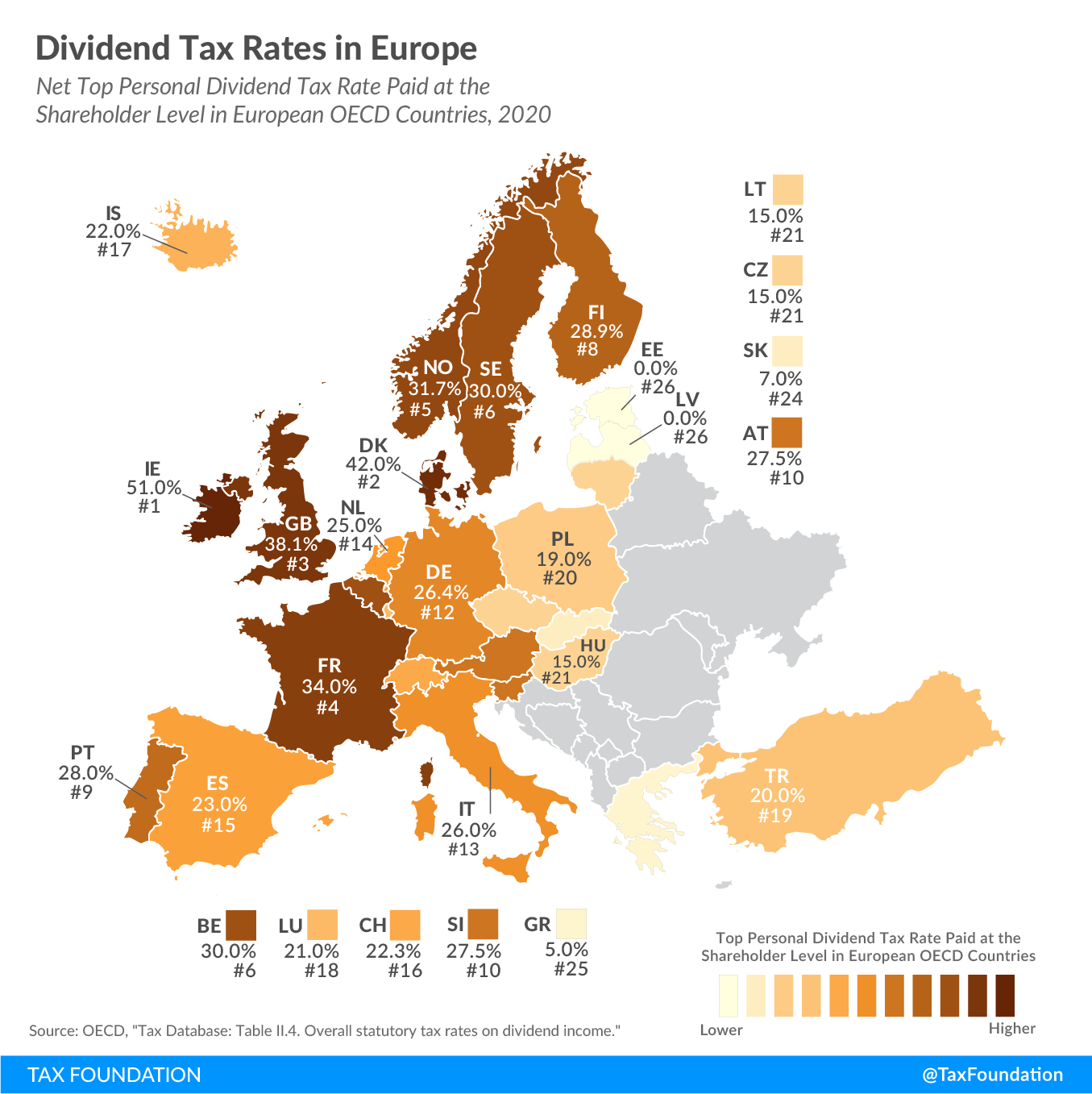

Dividend Tax Rates in Europe, 2020

2 min read -

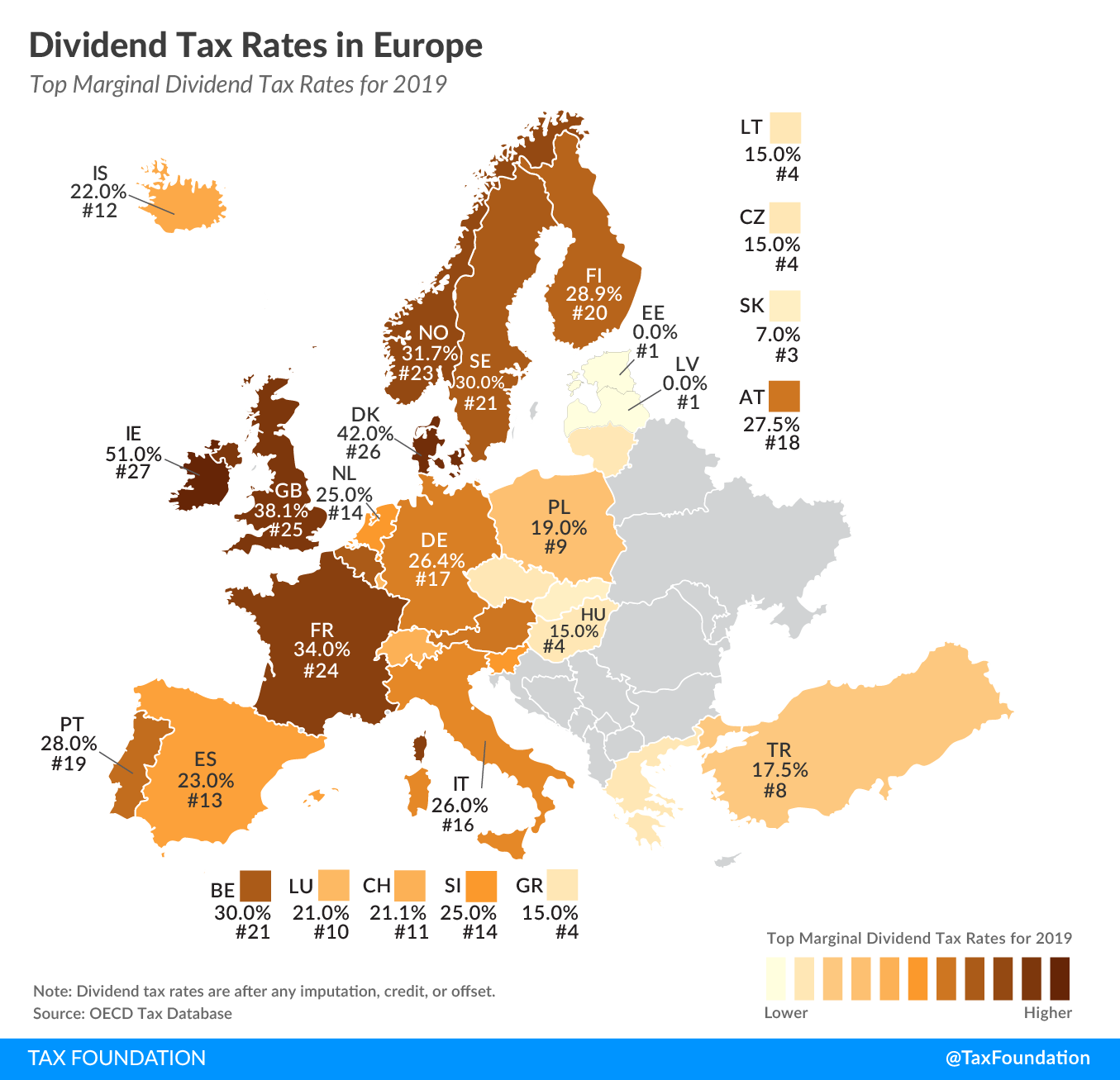

Dividend Tax Rates in Europe, 2019

2 min read