Corporate income taxes are one of the smallest sources of state and local taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. revenue. On average, only 3.7 percent of state and local tax revenues came from corporate income taxes in fiscal year 2014 (the most recent data available).

Some, however, mistake the corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. as the entirety of a business’s tax burden. In reality, businesses pay many types of taxes (such as sales taxA sales tax is levied on retail sales of goods and services and, ideally, should apply to all final consumption with few exemptions. Many governments exempt goods like groceries; base broadening, such as including groceries, could keep rates lower. A sales tax should exempt business-to-business transactions which, when taxed, cause tax pyramiding. , property taxA property tax is primarily levied on immovable property like land and buildings, as well as on tangible personal property that is movable, like vehicles and equipment. Property taxes are the single largest source of state and local revenue in the U.S. and help fund schools, roads, police, and other services., excise taxes, and more) and the corporate income tax makes up only 9.5 percent of total business taxes.

The share of revenue from corporate income taxes will decline as more businesses organize as pass-throughs (S-corps, partnerships, sole proprietorships, etc.), which “pass their income through” to their individual tax returns and therefore are liable under the individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source code. Additionally, corporate income tax revenue will decline as more businesses receive special tax credits and incentives, eroding the tax base.

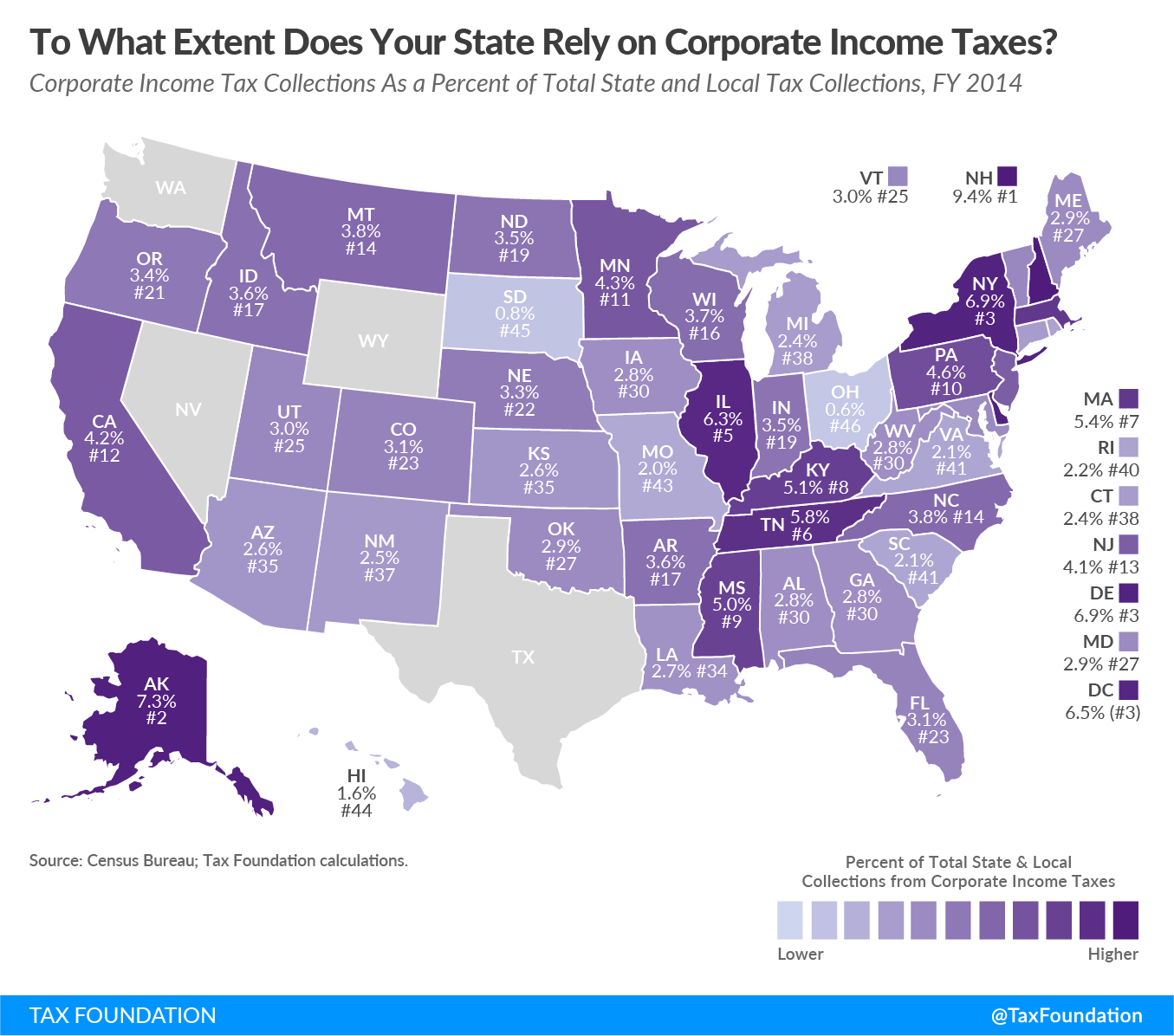

Today’s map shows what percentage of state and local tax collections derive from the corporate income tax. New Hampshire depends most heavily on the corporate income tax (9.4 percent of total tax collections) due to the lack of an individual income tax (except on interest and dividends) or a sales tax. Alaska comes in second (7.3 percent), again because the state does not levy an income tax or statewide sales tax. New York is the third most heavily dependent (6.9 percent) due to a heavy concentration of corporate payers and the state levies all major tax types.

At the other end of the spectrum, Nevada, Ohio, South Dakota, Texas, Washington, and Wyoming do not levy a corporate income tax, though four of these states (Nevada, Ohio, Texas, and Washington) levy a harmful gross receipts tax instead. Some of these states will still show a small amount of corporate income tax revenue due to taxes on corporate net income of special types of corporations (like financial institutions).

There are several reasons why the corporate income tax share is so low on average:

- The number of businesses organized as traditional C corporations has decreased over time. Pass-through businesses now earn more net income than traditional C corporations and employ the majority of the private-sector workforce.

- States hand out generous corporate tax incentive packages to move into (or remain in) their states. Jobs and investment credits, along with other targeted incentives, lower tax liability for some businesses and industries, effectively picking winners and losers while also chipping away at the tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates..

- States further reduce corporate tax bills by adjusting their income apportionmentApportionment is the determination of the percentage of a business’s profits subject to a given jurisdiction’s corporate income tax or other business tax. US states apportion business profits based on some combination of the percentage of company property, payroll, and sales located within their borders. formulas, reducing the in-state taxable incomeTaxable income is the amount of income subject to tax, after deductions and exemptions. Taxable income differs from—and is less than—gross income. of corporations within their borders. Location Matters helps to explain apportionment effects.

Corporate income taxes are not only limited in their revenue raising capacity, but they are also an extremely volatile tax type. During economic downturns, many corporations post losses and therefore have no tax liability under the corporate income tax.

Note: This is the second in a four-part map series in which we will examine the primary sources of state and local tax collections. Other maps in this series are linked below.