Key Findings:

- California has one of the nation’s least business-friendly taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. environments, ranking 48th on the Tax Foundation’s State Business Tax Climate Index, which measures tax structure. However, the state’s property taxA property tax is primarily levied on immovable property like land and buildings, as well as on tangible personal property that is movable, like vehicles and equipment. Property taxes are the single largest source of state and local revenue in the U.S. and help fund schools, roads, police, and other services. code is a relative bright spot, with the state ranking 14th on that component of the Index.

- If approved by California voters on Election Day and fully implemented, Proposition 15—also known as The California Schools and Local Communities Funding Act of 2020—could see the state drop to 33rd for property taxes on the Index.

- In 1978, voters passed Proposition 13, which capped property tax rates at 1 percent (for both residential and commercial property) and limited assessment growth to 2 percent per year.

- Proposition 15 would introduce a split roll property tax system in California by changing the assessment regime just for commercial property. If enacted, the changes are expected to increase the property tax burden on commercial activity in California by between $8 billion and $12.5 billion annually.

- Proposition 15 is being offered as a measure to raise taxes on businesses but much of the cost will be picked up by consumers through higher prices on goods and services.

- Proposition 15 would add complexity and increase non-neutrality in California’s property taxes, rather than correcting the shortcomings of Proposition 13, and would make the state considerably less attractive for business investment.

Introduction

On Election Day this year, California voters will vote on Proposition 15, also known as The California Schools and Local Communities Funding Act of 2020.[1] This ballot measure would amend the state constitution to require commercial properties, except agricultural property, to be taxed based on market value from fiscal year (FY) 2023. If Proposition 15 is ratified, it would introduce the split roll concept to California’s property tax system. Split roll refers to a system that applies a different tax rate, ratio, or assessment schedule to commercial properties from the one that applies to residential properties. Currently, residential, and commercial real estate are taxed at similar rates and under a similar assessment regime. Proposition 15 does not change property taxes for residential property.

A split or differentiated property tax system introduces non-neutrality to the tax code because it encourages investment in one class of properties over another. Under a split roll system, classes of property can be pitted against each other, changing the incentives to own or invest in different kinds of property, and allowing local policymakers to ratchet up tax burdens without being seen as raising taxes on homeowners.

Proposition 15, in particular, would require owners of commercial real estate to pick up a larger share of the overall tax burden, creating significant—and ever-expanding—property tax increases centered on commercial property. Adding additional cost to California’s businesses in the midst of a recessionA recession is a significant and sustained decline in the economy. Typically, a recession lasts longer than six months, but recovery from a recession can take a few years. could further harm these businesses’ ability to recover. California already has one of the nation’s least business-friendly tax environments. In fact, the state ranks 48th on the Tax Foundation’s State Business Tax Climate Index, which measures tax structure.[2] The one area where California ranks quite well is in the sub-index on property taxes (14th). The commercial property tax system in California is neutral and stable, consistent with two of the core principles of sound tax policy.[3] Adoption of Proposition 15 would change that.

This paper discusses the issues surrounding split roll and impact on California’s competitiveness while giving a short background on California’s property tax system and Proposition 13.

Background

California voters passed Proposition 13 in 1978, which limited property tax rates to 1 percent (for both residential and commercial property) and limited the growth rate of future assessments to 2 percent per year.[4] That means California offers taxpayers two types of property tax limitations: an assessment limit and a rate limit.

Property tax limitations come in three forms: assessment limits and rate limits, as California has, as well as levy limits, which restrict overall collections. All told, eight states and the District of Columbia offer all three types of limitations in some form; 25 states offer two; and 13 offer limitations in only one form. That leaves just four states—Hawaii, New Hampshire, Tennessee, and Vermont—without any property tax limitations on the books.[5]

California’s limitations mean that assessment value is not determined by the market value of the property but by the purchase value plus an allowable rate of assessment growth of no more than 2 percent, and that the tax rate cannot exceed 1 percent of the assessed value. When a property is sold, new assessments are conducted to value the properties at their new purchase price. For this reason, it is not uncommon for a person to pay much less in property taxes than his next-door neighbors who just bought their house.

While Proposition 13 does create some perverse incentives, such as disincentivizing people with a favorable property assessment to move, it also prohibits split roll property taxation.[6] Under current law, California cannot charge different rates for residential and commercial properties, and instead must tax all property at the same rate. In addition, Proposition 13 “requires taxes raised by local governments for a designated or special purpose to be approved by two-thirds of the voters,” and all tax increases to be passed by two-thirds of both houses of the California legislature.[7]

Proposition 15 would keep the limitations in place for residential properties but repeal them for commercial and industrial properties. Applying different tax formulas for different classes of properties is known as split roll. But California’s approach would be particularly aggressive, because commercial property assessments would track market value while residential property would continue to have its value artificially suppressed—widening the gulf between the classes of property with each passing year.

What Is Split Roll?

A tax roll is the official list of all the properties to be taxed. “Split roll” refers to the practice of applying a different tax formula, either tax rate or assessment ratio, to commercial properties than that applied to residential properties.

For instance, a state could levy a property tax of 2 percent on assessed value across all classes but calculate assessed value differently depending on the class. To favor residential dwellings, a locality or state could classify assessed value on residential property as 10 percent of market value but as 20 percent of market value for commercial property. In this example, the levy on commercial real estate is effectively 100 percent higher on commercial real estate than on residential. This type of split roll is currently in place in 19 states. Another way of creating split roll is by levying different rates based on property class—a practice used by seven states (see the table below).

This differentiation makes the tax code less competitive, as uniformity in property taxation is highly desirable. Split roll taxation is non-neutral and economically inefficient and undermines business competitiveness. Property taxes constitute the single largest share of businesses’ state and total tax liability, accounting for 38 percent of state and local business taxes in fiscal year 2016.[8] When business property tax rates are set independently of residential rates, they tend to be increased more frequently. In California, Proposition 15 would cause businesses to take on a greater share of overall property tax liability with almost every passing year.

| State | Split Roll Between Commercial and Residential | Ratio |

|---|---|---|

|

Alabama |

Yes |

2.000 |

|

Alaska |

No |

|

|

Arizona |

Yes |

1.800 |

|

Arkansas |

No |

|

|

California |

No |

|

|

Colorado |

Yes |

4.0278 |

|

Connecticut |

Yes |

2.1732 |

|

Delaware |

No |

|

|

DC |

Yes |

4.000 |

|

Florida |

No |

|

|

Georgia |

No |

|

|

Hawaii |

Yes |

2.238 |

|

Idaho |

No |

|

|

Illinois |

Yes |

2.000 |

|

Indiana |

No |

|

|

Iowa |

Yes |

1.6181 |

|

Kansas |

Yes |

2.1739 |

|

Kentucky |

Yes |

|

|

Louisiana |

Yes |

|

|

Maine |

No |

|

|

Maryland |

No |

|

|

Massachusetts |

No |

|

|

Michigan |

Yes |

3.7500 |

|

Minnesota |

Yes |

3.1665 |

|

Mississippi |

Yes |

1.5000 |

|

Missouri |

Yes |

1.7526 |

|

Montana |

Yes |

1.4000 |

|

Nebraska |

No |

|

|

Nevada |

No |

|

|

New Hampshire |

No |

|

|

New Jersey |

No |

|

|

New Mexico |

No |

|

|

New York |

No |

|

|

North Carolina |

No |

|

|

North Dakota |

yes |

1.1111 |

|

Ohio |

No |

|

|

Oklahoma |

Yes |

1.1111 |

|

Oregon |

No |

|

|

Pennsylvania |

No |

|

|

Rhode Island |

No |

|

|

South Carolina |

Yes |

1.5000 |

|

South Dakota |

Yes |

2.0690 |

|

Tennessee |

Yes |

1.2000 |

|

Texas |

No |

|

|

Utah |

Yes |

1.8182 |

|

Vermont |

Yes |

1.535 |

|

Virginia |

No |

|

|

Washington |

No |

|

|

West Virginia |

Yes |

1.750 |

|

Wisconsin |

No |

|

|

Wyoming |

Yes |

1.2105 |

|

Note: Only statewide split roll included above. Several states (Georgia, Nebraska, North Carolina, and Wisconsin) have split roll between other classes. Source: Lincoln Institute of Land Policy, ”Property Tax Classification.” |

||

Proposition 15 on the Ballot

On November 3, 2020, voters in California will decide on Proposition 15. The measure would introduce a split roll property tax system in California by changing the assessment regime for commercial property. It does this by requiring commercial property to be reassessed according to market value beginning in FY 2023 and every three years hereafter. Property used for both commercial and residential purposes will be reassessed proportional to its commercial use.

There are a number of exclusions in the proposition as well. First, property used for residential purposes and agriculture are not included. Neither is commercial property under single ownership with no more than $3 million worth of property statewide. Second, the measure exempts up to $500,000 of personal property from taxation as well as all tangible personal property of various small businesses.[9]

If Proposition 15 becomes law, it would, according to California’s Legislative Analyst’s Office (LAO), increase taxes on commercial properties by between $8 billion and $12.5 billion by 2025. Proposition 15 includes provisions about how this new revenue should be allocated. Several hundred million per year would be allocated to the counties to conduct the new assessments. Sixty percent of the remaining funds would go to cities, counties, and special districts. Importantly, not all jurisdictions are guaranteed increased revenue from the change. In fact, some may see a decline of revenue due to the built-in exemptions. The rest of the remaining revenue (40 percent) would be allocated to increase funding for schools and community colleges through the Local School and Community College Property Tax Fund.[10] Of the revenue allocated to the Local School and Community College Property Tax Fund, 11 percent will go to community colleges and 89 percent will go to local schools. Each school is to receive a minimum of $100 (subject to annual adjustment) per full-time student.[11]

A tax increase of up to $12.5 billion is a significant additional burden on businesses already struggling due to the coronavirus pandemic—particularly small businesses with low cash flow. While the small business exemptions in Proposition 15 afford some protections from increased taxes, many small businesses rent space. Their rent is likely to go up as the tax increase is passed on through rental costs.

When developing tax policy, lawmakers often ignore the incidence of a tax, or who actually pays the tax. Many times, this is different from who is legally required to pay the tax. For Proposition 15, this effect could have an unfortunate result of passing the cost to small businesses or consumers. If small businesses are unable to pass costs on to consumers, they will need to absorb the tax increase and cut their costs. That could result in job losses, lower pay, or worse benefits. If they can pass it on, costs will go up for Californian consumers. Despite Proposition 15 being offered as a measure to raise taxes on businesses, much of the cost will be picked up by consumers through higher prices on goods and services.

Separate from split roll, Proposition 15 also impacts other tax practices currently in place in California. One of these is a property tax exclusion for solar energy production. Since voters passed Proposition 7 in 1980, solar energy systems have not been included in the value of the property when installed.[12] Solar energy currently accounts for more than 14 percent of in-state energy generation across nearly 750 solar power plants.[13] If Proposition 15 becomes law, it would reverse this practice and make solar energy systems a taxable type of real property at time of construction rather than change of ownership. Such a change would have significant cost implication for the solar industry and energy consumers in California. This is seemingly an unintended consequence as Senator Holly Mitchell (D) has introduced a bill (SB 364) to reclassify solar energy systems as personal property—a change that would exempt them from property taxes.[14]

While SB 364 could retain the exclusion for solar energy systems, there are questions raised about the constitutionality of such a reclassification, since the bill seeks to redefine a certain class of real property—which is established in the state constitution—as personal property to avoid subjecting it to the changes of Proposition 15.[15] This involves not only tinkering with the definition of a term embedded in the state constitution, changing it to mean something inconsistent with its traditional use, but also reversing an impact of a ballot measure, which enjoys constitutional-level protection. Should SB 364 be invalidated by the courts, which seems quite plausible, California’s longstanding policy of promoting solar energy generation would be undermined. This would not only be detrimental to future investment, about which there might be deliberations to be had about the use of investment incentives, but would also retroactively undercut long-standing tax provisions which businesses have relied on for planning and investing in current and future projects.

Proposition 13 has long secured a stable revenue stream, albeit one that improperly values many properties. Unfortunately, Proposition 15 introduces the downside of greater revenue volatility without the upside of accurate, neutral valuations, since it skews property tax burdens disproportionately toward businesses. If Proposition 15 becomes law, property tax revenue will be more volatile as it will follow the value developments of the commercial real estate market. During the Great Recession, commercial property values declined by about 35 percent.

Adopting Split Roll Can Hurt California’s Competitiveness

Given California’s high business taxes, lawmakers should proceed with additional caution before imposing new levies on businesses. On the Tax Foundation’s State Business Tax Climate Index, California ranks 48th, ahead of only New York and New Jersey. The Index examines five components of states tax codes—individual, corporate, sales and excise, unemployment insurance, and property taxes. The state’s best ranking (14th) is for property taxes, a rare bright spot in a state that not only has high but often poorly structured taxes. The state would rank better if property tax collections were limited in a neutral manner, such as with a levy limit, rather than with the non-neutral assessment limit. However, the combination of split roll and higher overall collections that Proposition 15 would bring about would harm the state’s component rank substantially, dropping it from 14th to 33rd, reflective of a less competitive and more volatile property tax system overall.

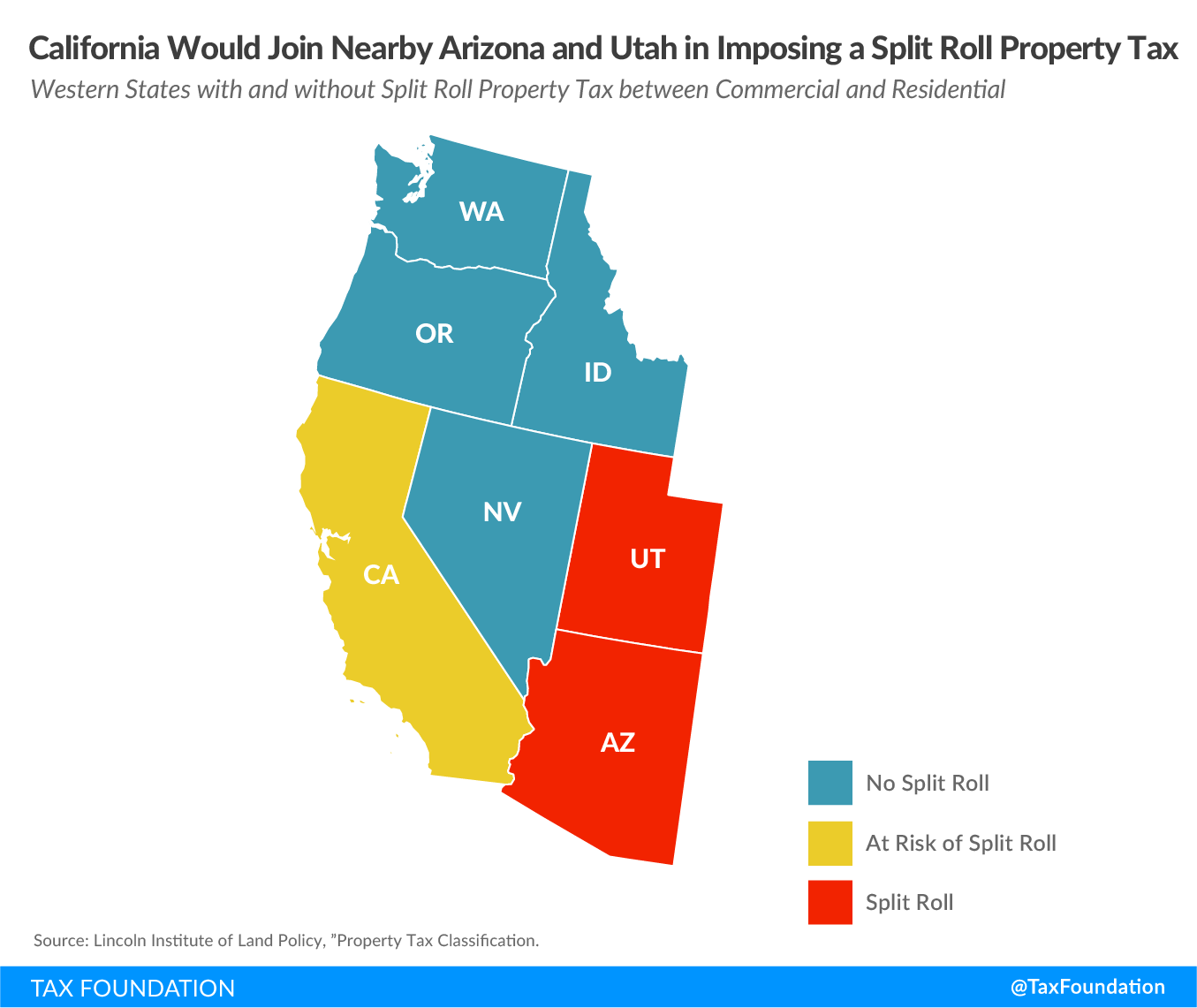

Tax competitiveness is an important consideration for companies looking to invest and for the ability of companies to attract talent. Under current law, companies in California have enjoyed stability and predictability in terms of their property taxes. This would disappear if Proposition 15 is approved. Thus, imposing a split roll system in California could have the unintended consequence of encouraging businesses to relocate to lower-taxed jurisdictions or invest out-of-state, accelerating an existing trend. Companies will not have to move far as few of California’s neighbors have a split roll system, and most have substantially more competitive tax codes overall.

In the midst of a pandemic, voters would be well-advised to consider the impact of significant new tax burdens on industries that are already suffering.

Conclusion

California’s voter-initiated Proposition 13 is deeply flawed. Its intentions—limiting property tax growth—are good but its design yields highly unequal treatment of properties across the state. Unfortunately, Proposition 15 does not improve the overall structure of California’s property tax system; instead, it adds complexity while dramatically increasing commercial property taxes. California already offers one of the least business-friendly tax environments in the country. Were voters to approve a split roll regime, they would be doubling down on that reputation and further harming businesses’ ability to grow and flourish.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

Subscribe[1] “The California Schools and Local Communities Funding Act of 2020,” Sept. 12, 2019, https://www.oag.ca.gov/system/files/initiatives/pdfs/19-0008%20%28The%20California%20Schools%20and%20Local%20Communities%20Funding%20Act%20of%202020%29_1.pdf.

[2] Jared Walczak, “2021 State Business Tax Climate Index,” Tax Foundation, forthcoming. Figures are from the forthcoming 2021 edition of the Index, to be released October 2020.

[3] Tax Foundation, “The Principles of Sound Tax Policy,” https://taxfoundation.org/principles/.

[4] Noah Glyn and Scott Drenkard, “Prop 13 in California, 35 Years Later,” Tax Foundation, June 6, 2013, https://taxfoundation.org/prop-13-california-35-years-later/.

[5] Jared Walczak, “Enhancing Tax Competitiveness in Connecticut,” Tax Foundation, July 31, 2018, https://taxfoundation.org/connecticut-tax-competitiveness/.

[6] Assessment limitations favor incumbent property owners at the expense of the next generation of homeowners, and, under some designs, preserve intergenerational wealth at significant cost to families just now climbing the income ladder.

[7] California Tax Data, “What is Proposition 13?” http://www.californiataxdata.com/pdf/Prop13.pdf.

[8] Andrew Phillips, Caroline Sallee, and Charlotte Peak, “Total State and Local Business Taxes: State-by-State Estimates For Fiscal Year 2018,” Council on State Taxation, August 2019, 4, http://cost.org/globalassets/cost/state-tax-resources-pdf-pages/cost-studies-articles-reports/fy16-state-and-local-business-tax-burden-study.pdf.

[9]California Legislative Analyst’s Office, “Proposition 15,” July 15, 2020, https://lao.ca.gov/ballot/2020/Prop15-110320.pdf; Ballotpedia, “California Proposition 15, Tax on Commercial and Industrial Properties for Education and Local Government Funding Initiative (2020),” https://ballotpedia.org/California_Proposition_15,_Tax_on_Commercial_and_Industrial_Properties_for_Education_and_Local_Government_Funding_Initiative_(2020).

[10] Ibid.

[11] “The California Schools and Local Communities Funding Act of 2020.”

[12] Ballotpedia, “California Proposition 7, Tax Assessments of Solar Energy Improvements (1980),” https://ballotpedia.org/California_Proposition_7,_Tax_Assessments_of_Solar_Energy_Improvements_(1980).

[13] California Energy Commission, “California Solar Energy Statistics and Data,” https://ww2.energy.ca.gov/almanac/renewables_data/solar/index_cms.php.

[14] California Senate Bill 364 (2020), https://leginfo.legislature.ca.gov/faces/billNavClient.xhtml?bill_id=201920200SB364.

[15] Laura Mahoney, “Solar Industry Wants Fix to Save California Property Tax Break,” Bloomberg Tax, July 27, 2020, https://news.bloombergtax.com/daily-tax-report-state/solar-industry-wants-fix-to-save-california-property-tax-break.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

Subscribe