In his “Liberation Day” tariff announcement, President Trump justified his tariffs by describing America’s manufacturing as “devastated.”

Three questions are worth asking. One, what is the state of manufacturing in the United States? Two, are tariffs a solution to what (if anything) ails the manufacturing sector? And three, if not tariffs, what is the alternative?

Manufacturing Production

“How much stuff do we make” is the most obvious starting point for evaluating the manufacturing sector. The numbers do not suggest the US has experienced a devastation of manufacturing capacity.

US manufacturing’s gross output has been fairly flat over recent decades. However, manufacturing value-added, which subtracts out input costs, has increased substantially since 1997. This difference stems from improvements in productivity, meaning we can make the same level of output with fewer inputs. Neither measure tells a story of an industry that’s been devastated.

The US has seen a decline in its share of global manufacturing, as China now has the largest manufacturing sector by value-added. The US remains a major player: the US has the second-largest manufacturing sector in the world, and it produces more manufacturing value-added than the third-, fourth-, and fifth-largest countries combined. And it does so with far fewer workers.

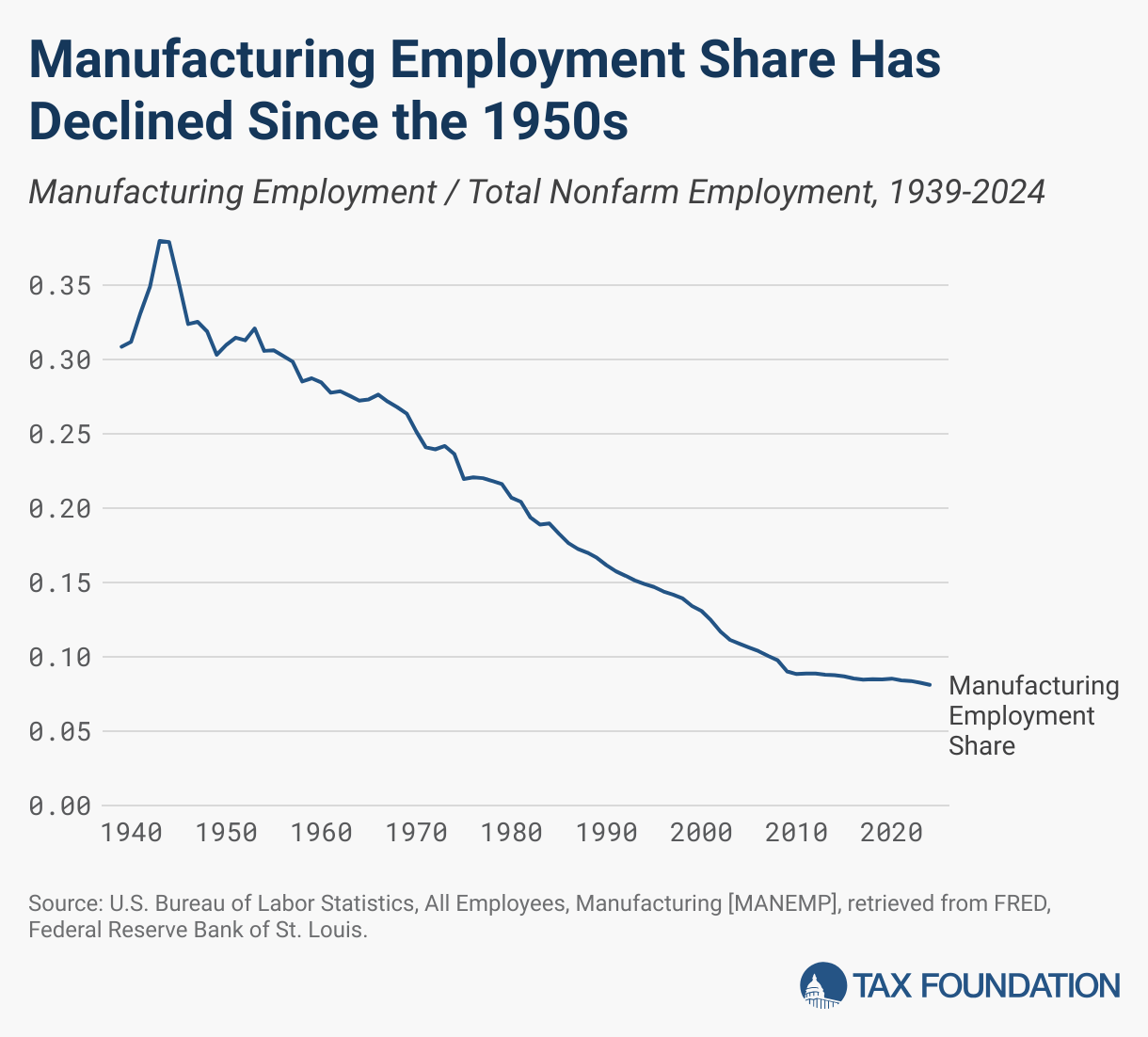

Manufacturing Employment Share

The manufacturing debate is as much about jobs as it is about production. The relevant metric here is manufacturing employment share. One could look to raw manufacturing employment, but that approach allows a growing overall population or prime-age workforce to mask sector-level changes. And while manufacturing employment share has declined, that should not be a source of policy concern.

Manufacturing as a share of overall employment has declined steadily ever since the 1950s. This trend is consistent across developed countries over the same period: major developed economies like the United Kingdom, France, Germany, and Japan have all seen declines in manufacturing as a share of total employment. And in the case of Singapore, an example of a rich country where manufacturing output has started to grow even as a share of GDP, manufacturing employment share has continued to decline.

This is consistent with the idea of Baumol’s cost disease. As some sectors grow in productivity, they lose employees to other sectors that have not been growing as much in terms of productivity. In the broader picture of the past several decades since World War II, manufacturing employment share has been declining thanks to a combination of automation-driven productivity growth and consumption shifting from goods to services.

Agriculture is illustrative here. The agricultural sector has seen a dramatic decline in its share of employment since 1900, and an even more dramatic decline if traced back to 1800. That does not mean the American agriculture has been devastated. American agriculture feeds America’s much larger population (plus exports) with roughly the same amount of land and many fewer workers than it did in 1900. How? Productivity growth. American farmers have bigger and better machines and technological innovation has produced much higher crop yields. As long as there’s productivity growth, a decline in employment share is nothing to worry about.

Manufacturing Productivity Growth

Productivity growth is arguably the most important metric for the manufacturing sector, and the largest source of concern.

There are really two stories to tell. For decades, manufacturing productivity grew strongly. As manufacturing employment declined (first as a share of overall employment and then in raw terms), manufacturing production continued to grow. That’s only possible with productivity growth. But when manufacturing employment share stabilized, manufacturing productivity growth flatlined.

Since the Great RecessionA recession is a significant and sustained decline in the economy. Typically, a recession lasts longer than six months, but recovery from a recession can take a few years. , manufacturing productivity has been stagnant. Productivity growth has been slow across the economy since the Great Recession, but the manufacturing slowdown has been pronounced. For many years, owing to the dynamics of Baumol’s cost disease, manufacturing productivity growth outpaced aggregate productivity growth. Since the recession, productivity growth in manufacturing has lagged the aggregate.

Slow productivity growth, in the manufacturing sector specifically but also in the aggregate, is where we should be concerned.

How Tariffs Affect Manufacturers

While the US manufacturing sector has not been “devastated,” there are some real problems, specifically surrounding slow productivity growth. But are tariffs the right solution?

The most recent survey of Texas manufacturers conducted by the Federal Reserve Bank of Dallas shows that American manufacturers are less than happy. While many comments focus on the uncertainty surrounding trade policy, a world with permanent tariffs would not fix American manufacturing productivity growth. If anything, it would make it worse.

Consider the composition of US imports. A hair over half of US imports are either non-automotive capital goods or industrial supplies and materials. Adding the chunk of cars and agricultural products that go toward the business market means a decisive majority of US imports are business inputs, and taxing them will negatively impact investment.

Delving beyond the headline categories here shows why manufacturers feel the pinch.

Who imported almost $393 billion worth of industrial and electric-generating machinery (more than 40 percent of non-automotive capital goods imports) last year? It’s not software companies or financial institutions; it’s American manufacturers and energy producers buying imported goods to reinvest in their American operations and workforce. Tariffs on those imports will hurt American manufacturers. We have seen this dynamic before, most clearly in the 2002 and 2018 steel tariffs, where the tariffs cost US manufacturing jobs as higher steel prices drove up input costs for manufacturers.

Tariffs also have more pernicious industry-level distortions. The United States exports a lot of high-tech manufactured goods like civilian aircraft, gas turbines, and specialized chemicals. We import a lot of basic, low-value consumer goods like textiles. Imposing tariffs on US imports hurts US exporters—whether through currency appreciation or retaliatory action against US exports. This dynamic pushes resources away from the high-value manufacturing industries in which the US leads and toward low-value activities like textile manufacturing.

Finally, tariffs produce perverse political incentives. Instead of reinvesting, companies insulated from competition often become complacent with their control of the domestic market and abandon their global competitiveness. This pattern appeared prominently in the American steel industry, starting in the late 1960s, in which major steel producers began lobbying for protections rather than reinvesting in new technology being adopted by foreign firms.

Meanwhile, other manufacturing firms, often the ones that can benefit from importing advanced foreign machinery to grow their domestic production, must spend resources arguing for exemptions. Tariffs on imported capital goods slowed capital accumulation in the much-discussed 1890s; meanwhile, the constant need for exemptions (in addition to their inadequacy as a major revenue source) drove the abandonment of tariffs in favor of an income taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. .

What Do We Do Now?

Catastrophic rhetoric about US manufacturing is not justified. The tariffs are extremely counterproductive. Still, all is not well in the US manufacturing sector. What should we do?

One prominent potential cause of the stagnation in American manufacturing productivity is low capital investment. Capital deepening, or the increase in physical machinery per worker, is a driver of long-run productivity growth, and it has been slow during the period of American manufacturing productivity stagnation. The trend of lower investment can be seen in specific categories, like investment in industrial robots, where the US lags well behind other countries.

There is a tax angle here. Manufacturing is a capital- and research-intensive business. The tax code, however, does not treat capital and research expenses equally relative to operating expenses. Operating expenses are deducted immediately, but capital costs must be spread over several years, meaning companies cannot fully deduct those costs in real terms. While this structure penalizes any firm looking to invest regardless of sector, it can have a disproportionate impact on manufacturers, particularly advanced manufacturers that both fund significant research and require very expensive capital goods like lithography machines.

In some cases, the tax bias against manufacturers was a deliberate choice. In the policy debate leading up to the Tax Reform Act of 1986, some policymakers (wrongly) saw accelerated depreciationDepreciation is a measurement of the “useful life” of a business asset, such as machinery or a factory, to determine the multiyear period over which the cost of that asset can be deducted from taxable income. Instead of allowing businesses to deduct the cost of investments immediately (i.e., full expensing), depreciation requires deductions to be taken over time, reducing their value and discouraging investment. provisions for capital investment introduced in the Economic Recovery Tax Act of 1981 as an unfair preference for manufacturers. The final 1986 reform limited accelerated depreciation against the wishes of capital-intensive manufacturers but aligned with the preferences of more capital-light industries.

In the coming reconciliation debate, policymakers can fix these biases. They can permanently repeal research and development (R&D) amortization, which forces companies to spread deductions for R&D out over 5 years or 15 years. They can permanently reintroduce 100 percent bonus depreciationBonus depreciation allows firms to deduct a larger portion of certain “short-lived” investments in new or improved technology, equipment, or buildings in the first year. Allowing businesses to write off more investments partially alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs. , which allows companies to fully deduct investment in equipment and machinery. One hundred percent bonus depreciation is a proven policy both to grow investment in aggregate as well as specifically in manufacturing. They could go further and allow faster deductions for long-lived assets like factories previously ineligible for bonus depreciation.

Tax policy is not the only dimension in which facially neutral rules that apply to all industries can place a disadvantage on manufacturing—for instance, permitting rules around major construction projects apply broadly but not every industry builds large-scale physical infrastructure. Fixing the tax treatment of capital investment is not a cure-all for manufacturing productivity, but it would remove a chain holding manufacturing productivity back.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe