Tracking the Impact of the Trump Tariffs & Trade War

The Trump tariffs have not meaningfully altered the trade balance and amount to an average tax increase per US household of $700 in 2026.

55 min readThe Tax Foundation is the world’s leading independent tax policy 501(c)(3) nonprofit. For over 85 years, our mission has remained the same: to improve lives through tax policies that lead to greater economic growth and opportunity.

Our Center for Federal Tax Policy, Center for State Tax Policy, and Center for Global Tax Policy each produce timely and high-quality research and analysis that influences the debate toward economically principled tax policies. Our experts are continuously analyzing the day’s most relevant tax policy topics and are relied upon routinely for presentations, testimony, and media appearances on tax issues spanning every level of government.

Likewise, providing journalists, taxpayers, and policymakers with basic data on taxes and spending has been a cornerstone of the Tax Foundation’s educational mission since its founding. As we wrote in our first edition of Facts & Figures in 1941, “Facts give a broader perspective; facts dissipate predilections and prejudices…[and are] an important step to meet the challenge presented by the broad problems of public finance.”

The Trump tariffs have not meaningfully altered the trade balance and amount to an average tax increase per US household of $700 in 2026.

55 min read

How will recent federal tax changes affect you?

4 min read

The State Tax Competitiveness Index enables policymakers, taxpayers, and business leaders to gauge how their states’ tax systems compare. While there are many ways to show how much state governments collect in taxes, the Index evaluates how well states structure their tax systems and provides a road map for improvement.

122 min read

Lawmakers can constrain the growth of property taxes without creating new problems. But the details matter.

Our experts explain how this major tax legislation may affect you and how policymakers can better improve the tax code.

24 min read

For Congress, work on the One Big Beautiful Bill Act is done. But in state capitols, the work has not yet begun. Many of the tax changes in the federal reconciliation act flow through to state tax codes—automatically in some states, and subject to an update in states’ Internal Revenue Code conformity date in others.

39 min read

As a rule, an individual’s income can be taxed both by the state in which the taxpayer resides and by the state in which the taxpayer’s income is earned.

52 min read

Notably, the OBBBA makes permanent the individual tax changes first put in place by the TCJA, which avoids a tax hike on an estimated 62 percent of tax filers in 2026.

4 min read

Facts & Figures serves as a one-stop state tax data resource that compares all 50 states on over 40 measures of tax rates, collections, burdens, and more.

2 min read

While there are many factors that affect a country’s economic performance, taxes play an important role. A well-structured tax code is easy for taxpayers to comply with and can promote economic development while raising sufficient revenue for a government’s priorities.

93 min read

New IRS data shows the US federal income tax system continues to be progressive as high-income taxpayers pay the highest average income tax rates. Average tax rates for all income groups remain lower after the Tax Cuts and Jobs Act (TCJA).

6 min read

The variety of approaches to taxation among European countries creates a need to evaluate these systems relative to each other. For that purpose, we have developed the European Tax Policy Scorecard—a relative comparison of European countries’ tax systems.

55 min read

We estimate that moving to permanent full expensing and neutral cost recovery for structures would add more than 1 million full-time equivalent jobs to the long-run economy and boost the long-run capital stock by $4.8 trillion.

4 min read

Our analysis shows that the economic benefits of federal investment in productivity-enhancing infrastructure may be undercut by the negative effects of the financing of those investments, such as when the corporate income tax is increased.

6 min read

In many cases, when two single workers combine their incomes and file jointly, the progressive tax system penalizes the secondary earner by subjecting their wages to a higher marginal tax rate.

25 min read

Transfer pricing rules are under stress given the current economic crisis. The OECD should provide transfer pricing guidance during the coronavirus crisis.

13 min read

As more states consider legalization of recreational marijuana, lawmakers should take note of the experiences of the states already allowing legal sales and consumption.

66 min read

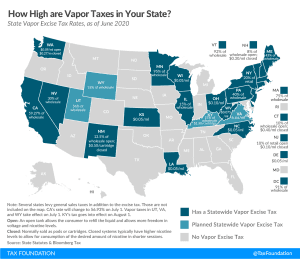

Many states may be looking toward vapor and other excise taxes to fill budget holes caused by the coronavirus crisis. While those areas may represent untapped revenue sources for many states, taxing those activities is unlikely to raise much revenue in the short term.

3 min read

The digitalization of the economy has been a key focus of tax debates in recent years. Our new report reviews digital tax policies around the world with a focus on OECD countries, explores the various flaws and benefits associated with the wide set of proposals, and provides recommendations for lawmakers to consider.

12 min read

A digital services tax like the one implemented by France likely violates both the General Agreement on Trade in Services and a model U.S. free trade agreement. However, it is uncertain whether meaningful relief could be obtained under either regime.

26 min read

Most countries provide tax relief to families with children—typically through targeted tax breaks that lower income taxes. While all European OECD countries provide tax relief for families, its extent varies substantially across countries.

2 min read

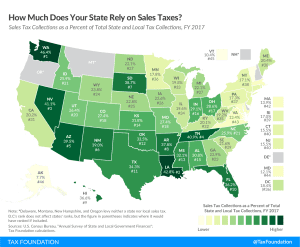

Consumption taxes, like sales taxes, are more economically neutral than taxes on capital and income because they target only current consumption.

3 min read