Daniel Bunn is President and CEO of the Tax Foundation. Daniel has been with the organization since 2018 and, prior to becoming President, successfully built its Center for Global Tax Policy, expanding the Tax Foundation’s reach and impact around the world.

Prior to joining the Tax Foundation, Daniel worked in the United States Senate at the Joint Economic Committee as part of Senator Mike Lee’s (R-UT) Social Capital Project and on the policy staff for both Senator Lee and Senator Tim Scott (R-SC). In his time in the Senate, Daniel developed legislative initiatives on tax, trade, regulatory, and budget policy.

He has a master’s degree in Economic Policy from Central European University in Budapest, Hungary, and a bachelor’s degree in Business Administration from North Greenville University in South Carolina.

Daniel lives in Halethorpe, Maryland, with his wife and their three children.

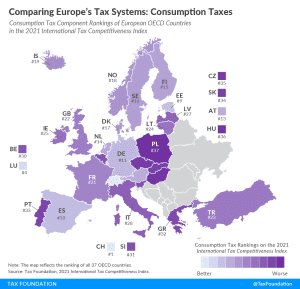

According to the 2021 International Tax Competitiveness Index, Switzerland has the best-structured consumption tax among OECD countries while Poland has the worst-structured consumption tax code.

According to the 2021 International Tax Competitiveness Index, Switzerland has the best-structured consumption tax among OECD countries while Poland has the worst-structured consumption tax code.

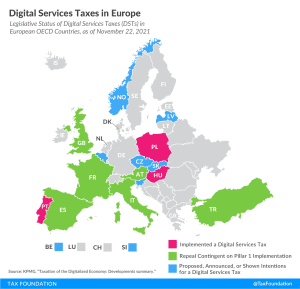

Despite ongoing multilateral negotiations in the OECD, about half of all European OECD countries have either announced, proposed, or implemented their own unilateral digital services tax.

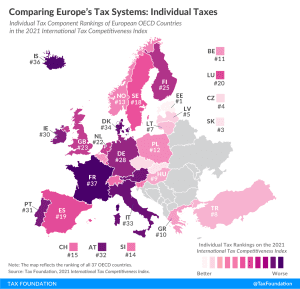

France’s individual income tax system is the least competitive of all OECD countries. It takes French businesses on average 80 hours annually to comply with the income tax.

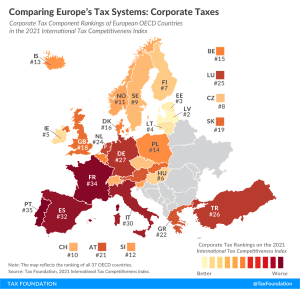

According to the corporate tax component of the 2021 International Tax Competitiveness Index, Latvia and Estonia have the best corporate tax systems in the OECD.

The legislation put forward by Democratic members of the House of Representatives would reverse many of the 2017 reforms while increasing burdens on businesses and workers.

The Index provides lessons for policymakers when they are thinking of ways to remove distortions from their tax systems and remain competitive against their peers. The further up a country moves on the Index, the more likely it is to have broader tax bases, relatively lower rates, and policies that are less distortionary to individual or business decisions. Going the other way reveals a policy preference for narrow tax bases, special tax policy tools, and rules that make it difficult for compliance.

A well-structured tax code (that’s both competitive and neutral) is easy for taxpayers to comply with and can promote economic development while raising sufficient revenue for a government’s priorities.

Over the course of the last year, it has become clear that Democratic lawmakers want to change U.S. international tax rules. However, as proposals have surfaced in recent weeks, there are clear divides among various proposals.

As Congress prepares to rewrite some portion of the current international tax rules, it’s hoped that they are able to achieve a more principled approach and one that is not so subject to obfuscation and misinterpretation.

As lawmakers are reviewing international tax rules and determining what to change and update, they should pay attention to the way GILTI interacts with profitable and loss-making companies.

This interaction between the U.S. proposals and those that may be put into law in foreign jurisdictions should give lawmakers caution when evaluating the revenue potential of changes to GILTI.

Intellectual property is a key driver in the current economy. Among other things, intellectual property includes patents for life-saving drugs and vaccines and software that runs applications on phones and computers.

The Biden administration has proposed to significantly increase the tax burden on foreign income through a policy known as Global Intangible Low-Tax Income (GILTI). While the administration’s rhetoric focuses on doubling the tax rate on GILTI from 10.5 percent to 21 percent, this is less than half the story.

From a policy perspective it is appropriate to combat base erosion and profit shifting, but policymakers need to keep in mind the need for simplicity to avoid increasing the compliance burden on taxpayers and administrative burdens on tax authorities.

Leaders around the world are quickly moving to finalize an agreement on a global minimum tax in 2021, based on the so-called “Pillar Two” proposal from the OECD.

New data show that the recent policy changes that have been implemented by the U.S., Ireland, and dozens of other countries are having an impact. The question for policymakers is whether they will take the time to understand these impacts before jumping to the next project to change international tax rules yet again.

There has been some confusion about how some parts of the recent G7 agreement on new tax rules for multinational companies might work. The new policies would target the largest and most profitable multinationals and bring in a global minimum tax.

To encourage private retirement savings, OECD countries commonly provide tax-preferred retirement accounts. However, in many countries, including the United States, the system of tax-preferred retirement accounts is complex, which may deter savers from using such accounts—and potentially lower overall savings.