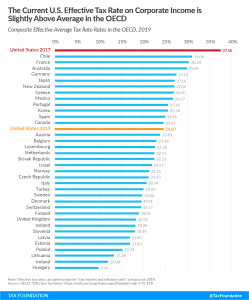

New Research Shows Major Changes for U.S. Companies Earning Profits from Ireland

New data show that the recent policy changes that have been implemented by the U.S., Ireland, and dozens of other countries are having an impact. The question for policymakers is whether they will take the time to understand these impacts before jumping to the next project to change international tax rules yet again.

3 min read