Top Personal Income Tax Rates in Europe, 2019

5 min readBy:Most countries have a progressive income tax structure. This means that the taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. rate paid by individuals increases as they earn higher wages. The top income tax rate is applied to the share of income that falls into the highest tax bracket. If a country has five tax brackets with a top income tax rate of 50 percent at a threshold of €1 million, then each additional euro of income over €1 million would be taxed at 50 percent.

Individuals in the top tax bracket also pay social security contributions or payroll taxes. These are typically flat-rate taxes levied on wages and are additional to the tax rate on income.

Workers recognize the impact of marginal tax rates and thresholds when deciding whether to work an additional hour or whether to take a new job paying a higher salary. High marginal tax rates can make additional work more expensive and lead to individuals deciding to stay in less productive positions or choosing not to work. When high tax rates increase the cost of labor, this has the effect of decreasing hours worked, which decreases the amount of production in the economy.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

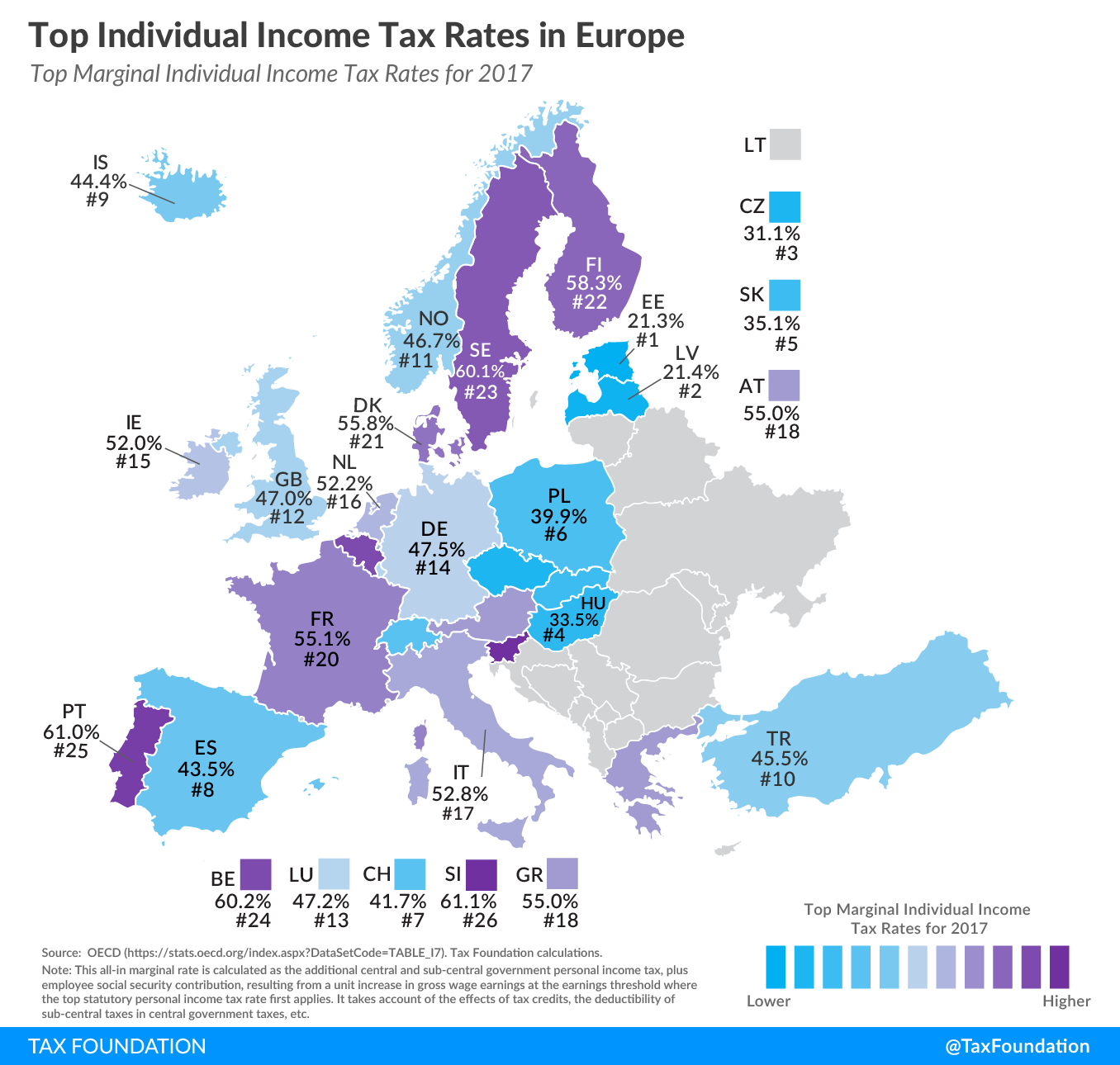

SubscribeEstonia (21.3 percent), Latvia (21.4 percent), and the Czech Republic (31.1 percent) have the lowest top income tax rates of all European countries covered. The countries with the highest top income tax rates are Slovenia (61.1 percent), Portugal (61.0 percent), and Belgium (60.2 percent).

The threshold at which the top income tax rate applies also plays an important role. Both the top tax rate and threshold can determine the amount of tax revenue raised by the top bracket. For instance, if a country has a top income tax rate of 50 percent on income over €1 million, only a small number of high-earning taxpayers will pay that rate and it may not generate significant tax revenues. In contrast, a top income tax rate of only 20 percent on all income over €10,000 would apply to most taxpayers, implying a broad income tax base and higher tax revenues from the top tax bracket.

The top income tax threshold can also be expressed as a multiple of a country’s average wage. While a low multiple indicates a flatter tax structure, high values signify more progressive tax systems.

|

Source: OECD (https://stats.oecd.org/index.aspx?DataSetCode=TABLE_I7), Tax Foundation calculations. (a) This all-in marginal rate is calculated as the additional central and sub-central government personal income tax, plus employee social security contribution, resulting from a unit increase in gross wage earnings at the earnings threshold where the top statutory personal income tax rate first applies. It takes account of the effects of tax credits, the deductibility of sub-central taxes in central government taxes, etc. (b) The average top threshold wage was converted to euros for countries that have a national currency other than the Euro. The average 2017 exchange rates provided by the European Central Bank (ECB) were used for the conversion. For Iceland, the ECB did not publish the average Euro-Icelandic Krona exchange rate for the year 2017, therefore the 2018 average was used. |

|||

| Country | Top Marginal Income Tax Rate (in %) (a) | Top Marginal Income Tax Threshold (in Euros) (b) | Top Marginal Income Tax Threshold (expressed as a multiple of the average wage) |

|---|---|---|---|

| Austria | 55.0 | € 1,096,059 | 23.8 |

| Belgium | 60.2 | € 49,638 | 1.0 |

| Czech Republic | 31.1 | € 4,694 | 0.3 |

| Denmark | 55.8 | € 70,081 | 1.3 |

| Estonia | 21.3 | € 2,196 | 0.1 |

| Finland | 58.3 | € 81,449 | 1.9 |

| France | 55.1 | € 562,377 | 14.6 |

| Germany | 47.5 | € 267,190 | 5.4 |

| Greece | 55.0 | € 233,129 | 11.2 |

| Hungary | 33.5 | € 0 | 0.0 |

| Iceland | 44.4 | € 81,597 | 1.2 |

| Ireland | 52.0 | € 70,045 | 1.5 |

| Italy | 52.8 | € 83,275 | 2.7 |

| Latvia | 21.4 | € 804 | 0.1 |

| Luxembourg | 47.2 | € 214,275 | 3.7 |

| Netherlands | 52.2 | € 70,593 | 1.4 |

| Norway | 46.7 | € 100,145 | 1.6 |

| Poland | 39.9 | € 23,647 | 2.0 |

| Portugal | 61.0 | € 280,899 | 15.6 |

| Slovak Republic | 35.1 | € 40,442 | 3.5 |

| Slovenia | 61.1 | € 95,263 | 5.1 |

| Spain | 43.5 | € 64,859 | 2.4 |

| Sweden | 60.1 | € 67,630 | 1.5 |

| Switzerland | 41.7 | € 270,683 | 3.4 |

| Turkey | 45.5 | € 31,406 | 3.1 |

| United Kingdom | 47.0 | € 171,103 | 3.9 |

Hungary applies a flat taxAn income tax is referred to as a “flat tax” when all taxable income is subject to the same tax rate, regardless of income level or assets. of 33.5 percent on all income earned, setting the top income tax threshold to €0. Latvia (€804) and Estonia (€2,196) are the countries with the second and third lowest top income tax thresholds, respectively. In contrast, Austria (€1,096,059), France (€562,377), and Portugal (€280,899) have the highest thresholds for their top income tax rates.

Because Hungary applies a flat tax on all income, top-income earners are subject to the same tax rate as average income earners. On this measure, Austria has the most progressive taxA progressive tax is one where the average tax burden increases with income. High-income families pay a disproportionate share of the tax burden, while low- and middle-income taxpayers shoulder a relatively small tax burden. system, with a top income tax rate that applies at 23.8 times the average income.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

SubscribeUpdate (4/23/2019):

The OECD made some corrections to its 2017 data on top individual income tax rates and the corresponding tax thresholds. Note that the changes mentioned below do not necessarily reflect policy changes by the countries. The map and table above have been adjusted as follows:

- For Austria, the top individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source rate has been changed from 48 percent to 55 percent. Its top marginal income tax threshold (in Euros) has been changed from €361,936 to €1,096,059. Its top marginal income tax threshold (expressed as a multiple of the average wage) has been changed from 7.9 to 23.8.

- For Greece, the top marginal income tax threshold (in Euros) has been changed from €82,052 to €233,129. Its top marginal income tax threshold (expressed as a multiple of the average wage) has been changed from 3.9 to 11.2.

- For Ireland, the top marginal income tax threshold (in Euros) has been changed from €70,148 to €70,045. Its top marginal income tax threshold (expressed as a multiple of the average wage) has been changed from 1.9 to 1.5.

- For Luxembourg, the top individual income tax rate has been changed from 42.8 percent to 47.2 percent. Its top marginal income tax threshold (in Euros) has been changed from €164,321 to €214,275. Its top marginal income tax threshold (expressed as a multiple of the average wage) has been changed from 2.8 to 3.7.

- For the Netherlands, the top individual income tax rate has been changed from 52.3 percent to 52.2 percent. Its top marginal income tax threshold (in Euros) has been changed from €70,513 to €70,593.

- For Slovenia, the top marginal income tax threshold (expressed as a multiple of the average wage) has been changed from 5.0 to 5.1.

- For Switzerland, the top marginal income tax threshold (expressed as a multiple of the average wage) has been changed from 3.5 to 3.4.

- For Turkey, the top marginal income tax threshold (expressed as a multiple of the average wage) has been changed from 3.2 to 3.1.

We calculated the top marginal income tax threshold (in Euros) by multiplying the average wage in national currency by the top marginal income tax threshold (expressed as a multiple of the average wage) (both variables are OECD data). Thresholds of non-Euro countries were converted into Euros. Due to rounding effects, fluctuating exchange rates, and estimated average wages, the top marginal income tax thresholds (in Euros) are only approximations of the actual top marginal income tax thresholds determined by tax jurisdictions.

About the Author

Elke Asen

Policy Analyst

Elke Asen was a Policy Analyst with the Tax Foundation’s Center for Global Tax Policy, focusing on international tax issues and tax policy in Europe. Prior to joining the Tax Foundation, Elke interned with the EU Delegation in Washington, D.C., the German Development Agency, and a social startup in Munich, Germany. She holds a BS in Economics from Ludwig Maximilian University of Munich.