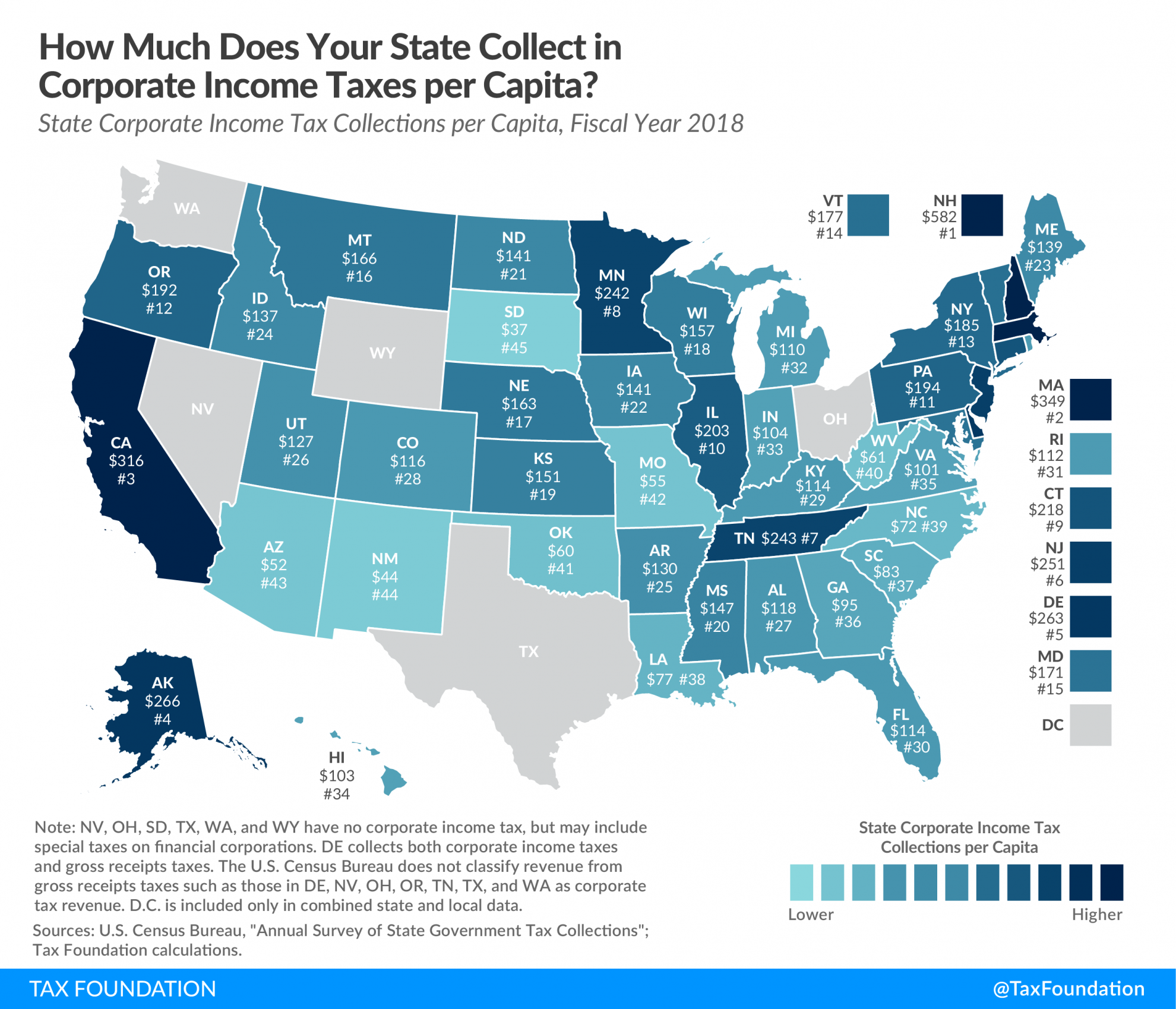

This week’s map compares corporate income tax collections per capita among the 50 states. The states with the highest collections are New Hampshire ($582), Massachusetts ($349), California ($315), Alaska ($266), and Delaware ($263). States with the lowest corporate income collections per capita are South Dakota ($37), New Mexico ($44), Arizona ($52), Missouri ($54), and Oklahoma ($60).

Six states—Nevada, Ohio, South Dakota, Texas, Washington, and Wyoming—do not levy a corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. . However, in some states without a corporate income taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. , a small amount of corporate income tax revenue is shown (such as in Ohio and South Dakota) due to taxes on specific types of businesses (such as financial institutions), which are sometimes structured as corporations.

It is important to note that among the six states without a corporate income tax, four (Nevada, Ohio, Texas, and Washington) instead have state-levied gross receipts taxes on businesses. The U.S. Census Bureau does not classify revenue from gross receipts taxes as corporate income tax revenue, but gross receipts taxes are generally considered more economically harmful than corporate income taxes due to tax pyramiding, non-neutrality, and lack of transparency. Delaware, among the states with the highest corporate income tax collections per capita, has both a corporate income tax and a state-levied gross receipts taxGross receipts taxes are applied to a company’s gross sales, without deductions for a firm’s business expenses, like compensation, costs of goods sold, and overhead costs. Unlike a sales tax, a gross receipts tax is assessed on businesses and applies to transactions at every stage of the production process, leading to tax pyramiding. .

When thinking about business taxes, the corporate income tax may be among the first that comes to mind, but it is far from the only tax businesses pay. In addition to corporate income taxes, corporations are subject to sales, property, unemployment insurance, excise, payroll, and business license taxes, among others. In fiscal year 2018, corporate income taxes accounted for only 8.5 percent of all taxes paid by businesses to state governments.

Compared to other sources of tax revenue—such as income, sales, and property taxes—states rely relatively little on corporate income taxes. According to the U.S. Census Bureau, in fiscal year 2017, the corporate income tax generated only 3.2 percent of total state tax collections.

Note: This is part of a map series in which we examine the primary sources of state and local tax collections.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe