As part of President Biden’s proposed budget for fiscal year 2023, the White House has once again endorsed a major taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. increase on accumulated wealth, adding up to a 61 percent tax on wealth of high-earning taxpayers.

Biden’s latest budget includes two major tax increases on accumulated wealth originally proposed in last year’s American Families Plan (AFP), along with a new tax increase that would penalize taxpayer wealth even further.

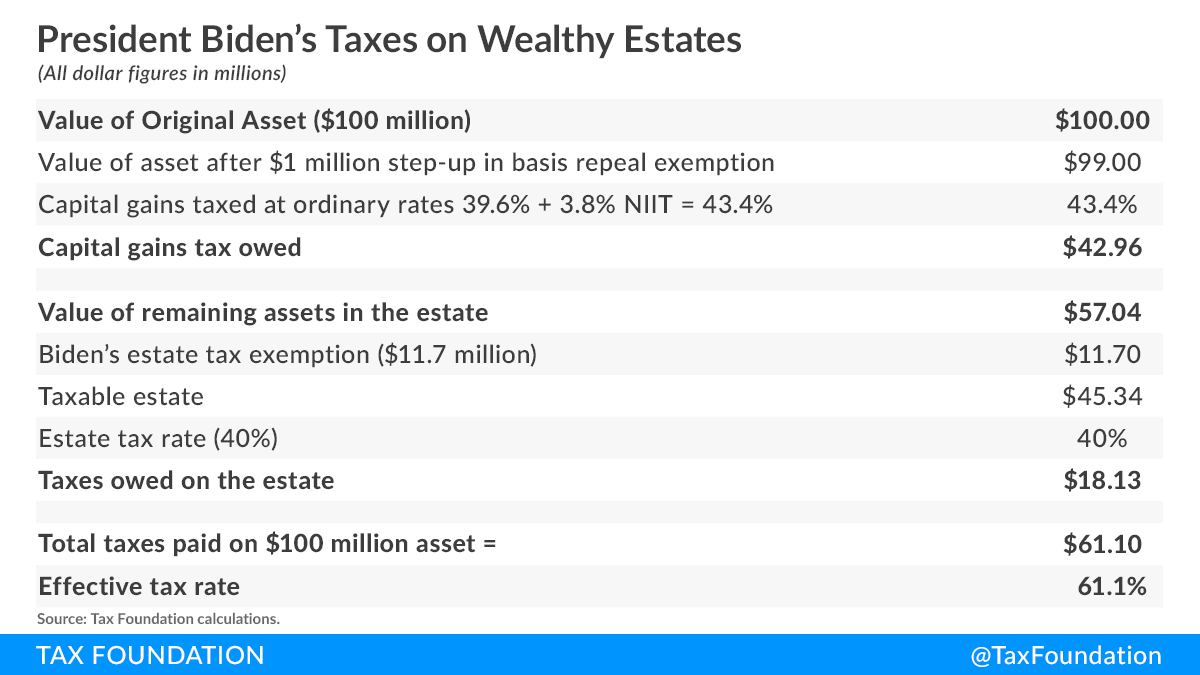

First, the budget proposes a tax on unrealized capital gains at death for unrealized capital gains above $1 million. Currently, long-term capital gains of high earners are subject to a 20 percent tax rate and the 3.8 percent net investment income tax (NIIT) when the gains are realized (sold).

Second, Biden also wants to tax the capital gains of millionaires at ordinary income tax rates, which would be levied at his proposed top marginal rate of 39.6 percent. Added to the NIIT, it would mean a combined top tax rate on capital gains of 43.4 percent, compared to 23.8 percent today.

Third, Biden’s budget proposes a new “minimum tax” on unrealized capital gains for households with wealth above $100 million. It would require taxpayers to include phantom gains from assets they have not sold in their taxable incomeTaxable income is the amount of income subject to tax, after deductions and exemptions. Taxable income differs from—and is less than—gross income. each year and pay tax on the phantom gains to reach a minimum tax rate of 20 percent. Taxes paid under the proposal would be considered “pre-payments” of the final capital gains taxes owed when the taxpayer sells their assets or when they owe capital gains taxes at death.

In addition to Biden’s proposed tax hikes, large estates would also be subject to the current estate tax of 40 percent above an exemption of $11.7 million per person.

As the accompanying table illustrates, for an asset worth $100 million (all of which is a capital gain for the sake of simplicity), the two changes would mean an immediate capital gains taxA capital gains tax is levied on the profit made from selling an asset and is often in addition to corporate income taxes, frequently resulting in double taxation. These taxes create a bias against saving, leading to a lower level of national income by encouraging present consumption over investment. liability of $42.9 million at the time of death. Upon paying the capital gains tax at death, the value of the $100 million asset falls to $57 million for the purposes of the estate taxAn estate tax is imposed on the net value of an individual’s taxable estate, after any exclusions or credits, at the time of death. The tax is paid by the estate itself before assets are distributed to heirs.. After subtracting the $11.7 million exemption, the 40 percent estate tax rate is levied on the remaining $45.3 million in assets to produce an estate tax bill of about $18.1 million.

Combining both taxes results in a total tax liability of $61.1 million on the original $100 million asset, for an effective tax rate of 61 percent. The tax rate under Biden’s proposal is nearly twice the effective tax rate that the same asset would face today under existing tax rules.

The latest budget takes the two tax hikes and goes even further by layering on yet another complicated tax on unrealized gains during the taxpayer’s lifetime. The taxpayer would have to navigate taxes on unrealized gains while alive, and their estate would have to reconcile the pre-payments and deal with paying up to a 61 percent effective tax rate on unrealized gains at death.

By historical standards, Biden’s plan to tax unrealized gains (during life and death, no less) and levy the estate tax at the same time is quite unique. Traditionally, estate tax law has allowed for a “step-up” in the basis of transferred assets so that they are not hit by the capital gains tax and the estate tax at the same time.

When the estate tax was repealed for one year in 2010, the step-up was also repealed, which meant that heirs did face tax liability on any gains when they sold inherited assets.

However, the impact of the step-up’s repeal was mitigated somewhat for smaller estates by a provision that exempted “$1.3 million of an estate’s increased value from the capital gains tax and $3 million for transfers to a spouse.” Even though some heirs did pay higher capital gains taxes on the assets they inherited in 2010, Congress has historically understood that it was bad policy to levy a capital gains tax and estate tax on the same assets.

Of course, most economists agree that both the estate tax and capital gains taxes already amount to a second or third layer of tax on the same income. In the case of corporate stocks, capital gains (and dividends) are second layers of tax on corporate profits that were already taxed by the corporate income tax. Estate taxes are levied on assets that were purchased with after-tax income and on assets that may already have been taxed, as might be the case with stocks or corporate bonds.

Increasing the top capital gains tax rate to 43.4 percent alone would mean high-earning taxpayers may face tax rates north of 50 percent on capital gains when including state taxes. Taxing unrealized gains at death while still levying the estate tax further compounds the total tax burden on saving and investment, which may be the highest tax burden on capital gains seen in nearly a century. Add on top of this the latest proposal to tax certain unrealized gains every year, and we are now looking at an unprecedented increase in the capital gains tax burden.

Rather than penalize productive activity further, tax policy that encourages greater economic growth and opportunity is a better path ahead for U.S. tax policy.

Launch Resource Center: President Biden’s Tax Proposals

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

Subscribe