Key Findings:

- The United States’ taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. code places a double-tax on corporate income with one tax at the corporate level through the corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. and a second tax at the individual level through the individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source on dividends and capital gains.

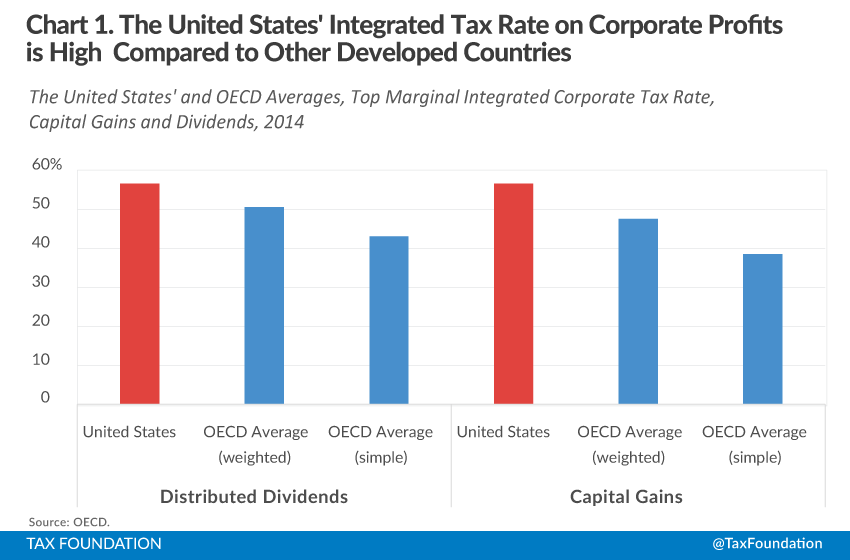

- The combined (integrated) tax rate on corporate income in the United States is 56.6 percent, which is the second highest in the developed world.

- The double-taxation of corporate profits reduces investment, encourages corporations to borrow money to finance investment, and encourages structuring as a pass-through businessA pass-through business is a sole proprietorship, partnership, or S corporation that is not subject to the corporate income tax; instead, this business reports its income on the individual income tax returns of the owners and is taxed at individual income tax rates..

- Short of reforming the entire U.S. tax code, integrating the corporate and individual income tax could eliminate the double taxationDouble taxation is when taxes are paid twice on the same dollar of income, regardless of whether that’s corporate or individual income. of corporate income.

- Both Australia and Estonia, among many other developed countries, integrate their corporate and individual income tax code in order to eliminate double taxation.

Introduction

The United States’ tax code treats corporations and their shareholders as separate taxable entities. The result is two layers of taxation on corporate income: one at the corporate level and a second at the shareholder level. This creates a high tax burden on corporate income, increasing the cost of capital. The double taxation of corporate income reduces investment and distorts business decisions. Specifically, businesses are more likely to borrow money to finance projects and conduct business as a pass-through entity rather than a corporation.

A goal of tax reform is to make the U.S. tax code more neutral and to encourage economic growth. One step toward this goal is the elimination of the double tax on corporate income. Short of a complete overhaul of the tax code, integration of the corporate and individual income tax code is an option to eliminate double taxation. Many developed countries have integrated their tax systems in order to mitigate or completely eliminate the double taxation of corporate income.

The Double Taxation of Corporate Income

The United States has a modified version of what is called a “classical” corporate income tax system. A classical corporate tax system treats the corporation and the shareholder as two separate taxable entities.[1] This means that income and losses earned at the corporate level and individual level are separate in the eyes of the code, even if they result from the same economic activity.

The result is that corporate income is generally subject to two layers of taxation; one tax at the entity level when the corporation earns income and a second tax at the individual level when that income is passed to its shareholders as either dividends or capital gains. The U.S. system modifies this classic treatment slightly by providing a reduced tax rate on dividend and capital gains income.[2]

| Corporate Profits | $ 100.00 |

| Corporate Income Tax @ 39.1% | $ 39.10 |

| Distributed Dividends | $ 60.90 |

| Dividend Income Tax @ 28.7% | $ 17.47 |

| Total After-Tax Income | $ 43.43 |

| Total Tax Rate | 56.57% |

The two layers of tax create a significant tax burden on corporate income (Table 1). Suppose a corporation earns $100 in profit. It needs to pay the corporate income tax of $39.10 (a federal and state rate of 39.1 percent), which leaves the corporation with $60.90 in after-tax profits. When the corporation distributes these earnings as a dividend, the income is taxed again at the individual level. The shareholder then pays $17.47 in income taxes (a federal and state rate of 28.7 percent).[3] In total, the $100 of corporate profits face a combined marginal tax rateThe marginal tax rate is the amount of additional tax paid for every additional dollar earned as income. The average tax rate is the total tax paid divided by total income earned. A 10 percent marginal tax rate means that 10 cents of every next dollar earned would be taken as tax. of 56.6 percent.[4]

The same double taxation occurs if the corporation retains its after-tax earnings, rather than distribute them as dividends. When corporate earnings are retained, the value of the stock increases to reflect an increase in assets held by the corporation. Shareholders that decide to sell their stock will realize a capital gain and pay tax on that gain. The integrated corporate tax rate through capital gains in the United States is 56.6 percent.

There are a few cases in which business income may not necessarily face this double taxation. Corporations that finance investments with debt, rather than equity, are able to deduct interest payments made to lenders. This passes the pre-tax earnings to lenders in the form of interest who pay only one layer of tax on that income.[5] Likewise, pass-through businesses—sole proprietorships, S corporations, and partnerships—face no entity level tax at the federal level.[6] Their income is passed directly to its owners, who pay individual income taxes.

The United States has High Integrated Tax Rates on Corporate Profits

The United States’ integrated tax rate on corporate profits is high by international standards. The United States has the second highest integrated tax rate in the OECD (Chart 1),[7] which has an average integrated tax rate on dividends of about 43 percent (50 percent weighted by GDP).

The United States’ integrated tax rate on capital gains is similarly high internationally. The United States’ integrated tax rate on capital gains is also 56.6 percent, which is also the second highest in the OECD. The OECD average in 2014 was 39 percent (47.5 percent weighted by GDP).

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

SubscribeThe Double Taxation of Corporate Profits Creates a Number of Distortions in the Economy

The double taxation of corporate earnings creates several economic distortions that have real effects on both business decisions and the overall economy.

Reduced Saving and Investment

When a corporation decides whether to invest in a new project, it needs to make sure its after-tax return on the project is high enough to satisfy investors. If the return is too low, the corporation won’t pursue the investment. This minimum required return is the cost of capital.

A higher tax rate on both corporate income and investment income increases the cost of capital. All things being equal, a higher cost of capital makes it less likely that corporations will invest in projects. This leads to lower levels of investment and a smaller capital stock in the overall economy. A smaller capital stock means lower worker productivity, lower wages, and slower economic growth.

Shift to Non-Corporate Business Forms

The double tax on corporate income also distorts the organizational form of businesses. Unlike traditional C corporations, pass-through business only face one layer of tax. S corporations, partnerships, sole proprietorships face no entity level tax. All profits from these entities are immediately passed through to their owners, who pay the individual income tax (Table 2). The top marginal tax rate on pass-through business income (around 47.2 percent)[8] is a meaningful savings compared to the combined 56.6 percent faced by corporate income.

| Traditional C Corporations | Pass-through Businesses | |

| Entity-Level Tax | 39.1% | 0.0% |

| Individual-Level Tax | 28.7% | 47.2% |

| Total Tax Rate | 56.6% | 47.2% |

| Note: Example assumes C corporation distributes dividends. Pass-through Business is a Partnership. | ||

Due to the tax differential between the two forms, businesses have an incentive to forgo the benefits of incorporation in order to receive a higher rate of return on investments. Since 1986, when individual income tax rates sharply declined relative to corporate tax rates, more and more business income has been reported by pass-through businesses (Chart 2). In 1980, pass-through businesses only accounted for around 20 percent of total business income. As more business activity was performed as a pass-through business, rather than a C corporation, pass-through income steadily climbed. As of 2011, pass-through businesses earned more than 60 percent of all business income.[9]

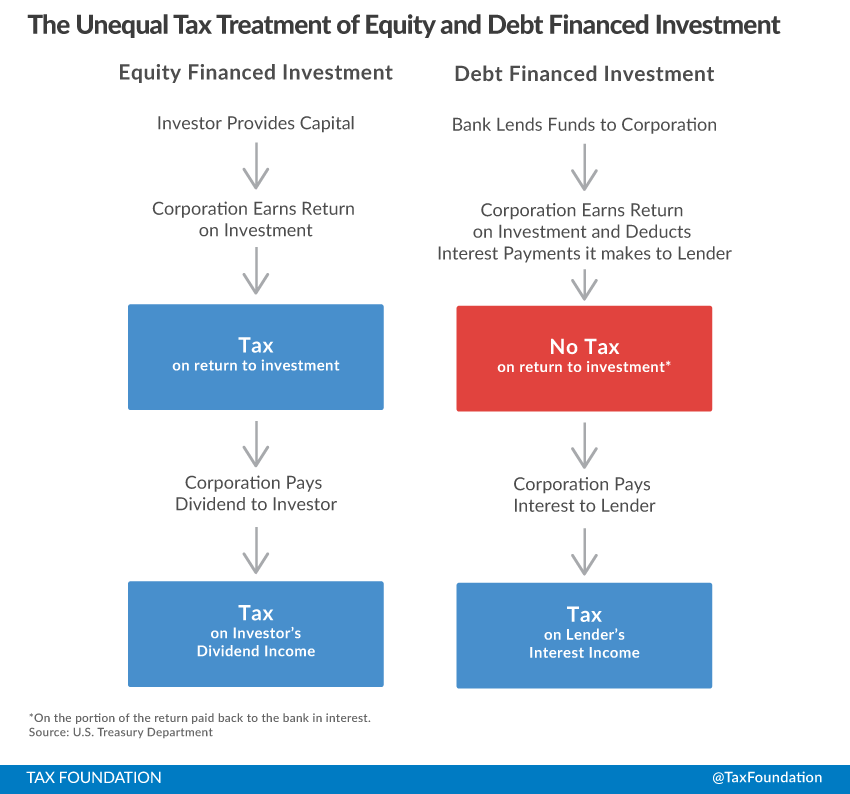

Debt over Equity

When a corporation wants to fund a new project it can either finance it through equity (issue of new stock) or it can borrow money. There are many non-tax reasons that a corporation would choose one funding mechanism over another, but the current tax code treats debt financing more favorably than equity financing. Specifically, there are two layers of taxation on equity financing and only one layer of taxation on debt financing.

Suppose a corporation decides to raise money to purchase a machine by issuing new stock. When this investment earns a profit the corporation needs to pay the corporate income tax. It then needs to compensate the original investors, so the corporation distributes the after-tax earnings as dividends. The investors then need to pay tax on the dividends they receive from the corporation. This equity-financed project nets two layers of tax, one at the corporate level and one at the shareholder level.

In contrast, the corporation could finance the same investment by borrowing money. When the corporation earns a profit from a debt financed investment, it needs to pay the corporate income tax on its profits. But before the corporation pays its income tax, it needs to pay its lender back a portion of what it borrowed plus interest. Under current law, corporations are able to deduct interest payments they make to lenders against their taxable incomeTaxable income is the amount of income subject to tax, after deductions and exemptions. Taxable income differs from—and is less than—gross income. . Thus, profits derived from the debt-financed investment do not face a corporate level tax on the portion of the profit that is paid back in interest.[10] The lender then receives the interest as income and needs to pay tax on it. The debt financed project only nets a single layer of tax at the debt holder’s level.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

SubscribeDue to this inequitable treatment of debt and equity in the tax code, the rate of return on debt financed projects, all else equal, is higher. This encourages corporations to borrow more than they otherwise would in the absence of the double tax on equity investment.

Integrating the Corporate and Individual Income Tax

One of the ultimate goals of fundamental tax reform is to eliminate many of the current biases in the tax code caused by the double taxation of corporate income. Short of reforming the entire tax code, integrating the individual and corporate tax code is a reasonable step towards fixing the problem. It would lower the combined burden on corporate income and eliminate many of biases in the current system.

There are several ways to integrate the corporate tax code. Corporate income can be fully taxed at the entity level (a corporate income tax) and then tax exempt when passed to shareholders as dividend income, or corporations could be given a deduction for dividends passed to their shareholders, who pay tax on the dividend income. Alternatively, shareholders and corporations both pay tax on their income, but shareholders can be given a credit to offset taxes the corporation already paid on their behalf.

Many developed nations have integrated their corporate and individual tax codes to reduce or eliminate the two layers of taxation on corporate income. The following section provides two examples of countries with integrated corporate tax codes: Australia and Estonia.

Australian Credit Imputation System

Australia integrates their corporate and individual income tax with a tax credit imputation. This method of integration is a system by which the corporation and the shareholder both pay part of the corporate income tax, but the shareholder is given a tax creditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income rather than the taxpayer’s tax bill directly. to offset the taxes already paid by the corporation. In the end, corporate income is taxed at the marginal income tax rate of its shareholders, whether the shareholder has a higher or lower tax rate than the corporation.

Suppose a corporation in Australia earns $100 (Table 3). This corporation would need to pay the corporate income tax of 30 percent ($30). It then decides to pass the remaining $70 of after-tax profits to its shareholder.

Corporate Profits$100

| Corporate Income Tax @ 30% | $30 |

| After-Tax Corporate Profits | $70 |

| ↓ | |

| Distributed Dividends | $70 |

| Grossed-up Dividends | $100 |

| Individual Income Tax @ 46.5% | $46.50 |

| Tax Credit for Corporate Taxes Paid | ($30.00) |

| Net Personal Tax | $16.50 |

| After-Tax Personal Income | $53.50 |

| Total Tax on Corporate Income | |

| $100 – $53.50 –> | $46.50 |

| Rate: | 46.50% |

The shareholder receives the $70. For tax purposes, the shareholder then grosses-up the dividends, which means they add back the taxes the corporation already paid on those profits ($30). This makes their taxable dividend income $100. This shareholder faces a marginal tax rate of 46.5 percent, which means a tentative tax bill of $46.50. The Australian tax code then provides a credit that reduces the shareholder’s tax bill by the amount the corporation already paid in taxes on those dividends, in this case $30. On net, the shareholder’s tax bill is $16.50. Combine that with the corporation’s bill of $30, the total tax rate on corporate profits was $46.50, or 46.5 percent of the original $100 of corporate profit.[11]

In order to make sure corporate income is taxed at the marginal rate of shareholder—whether higher or lower than the corporate income tax rate—the credit against corporate taxes paid is refundable. For example, if a taxpayer who received dividend’s faced a marginal tax rate of 15 percent, instead of 46.5 percent, they would receive $15 back as a refund so the marginal rate on the corporate income totals $15 (the $30 corporate tax for the corporation minus $15 tax refund for the individual).

| Corporate Profits | $100 |

| Corporate Tax @ 21% | $21 |

| After-Tax Income | $79 |

| ↓ | |

| Dividend Income | $79 |

| Dividend Tax @ 0% | $0 |

| After-Tax Personal Income | $79 |

| Total Tax on Corporate Income | |

| $100 – $79 –> | $21 |

| Rate: | 21% |

Including Australia, seven OECD countries have full or partial credit imputation systems.[12] (See Appendix Table 2, below)

Estonian Dividend Exemption

Estonia integrates its corporate and individual income tax code by having a full dividend exemption at the shareholder level. This system of integration levies only one layer of tax on corporate income at the corporate level. When the shareholder receives dividends from the corporation, there is no additional tax due.

When an Estonian corporation makes a profit and distributes it to shareholders, it must pay the corporate income tax of 21 percent, or $21 on $100 of profit.[13]

When shareholder receives the after-tax profits of $79, no additional tax is due. The total tax on distributed profits between the corporation and the individual is 21 percent.

Including Estonia, 6 OECD countries have full or partial dividend exemptions (Appendix Table 2, below).

Dealing with Capital Gains

Countries also reduce the double taxation of corporate profits that are retained and lead to capital gains. Nearly all OECD countries either mitigate or eliminate the double taxation with reduced, or no, capital gains taxes.[14] (Appendix Table 3, below). For example, Australia provides a 50 percent deduction (50 percent of a capital gain is tax exempt) for capital gain income. The United States is among the 18 OECD countries that provide a reduced tax rate for capital gains. Nine countries completely exempt capital gains from individual-level taxation, which eliminates the double taxation of retained earnings. Estonia, uniquely, exempts retained earnings at the corporate level, but taxes capital gains at the individual level as ordinary income.

Dealing with Pass-through Businesses

Ideally, business tax reform would bring all business income under the same tax code. This way all business income is taxed once and treated equally, regardless of legal form. Short of a comprehensive reform, efforts to integrate the corporate tax code have to consider pass-through business income. Certain types of integration may create single taxation for all business income, but could leave a large disparity between the taxation of different legal forms of business. For example, exempting dividend income at the shareholder level would eliminate double taxation for corporate income, but could give favorable treatment to corporate income compared to pass-through business income. However, if the United States enacted an imputation credit, the tax disparity between pass-through businesses and corporations could be closed. All business income, pass-through or corporate, would be taxed once at the owner’s or shareholders marginal tax rate.

Conclusion

The U.S. tax code double taxes corporate income: once at the corporate level and then again at the shareholder level. This creates a significant tax burden on corporate income, which increases the cost of investment, encourages a shift away from the traditional C corporate form, and an incentive to finance projects with debt.

The United States has one of the highest combined tax rates on corporate income in the industrialized world. Integrating the corporate and individual income tax would ensure that corporate income is only taxed once and would increase the incentive to invest and reduce the incentive to avoid the second layer of tax. This would eliminate the current biases in the tax code and encourage investment and economic growth. Many countries in the OECD have fully or partially integrated corporate tax systems that eliminate or limit double taxation.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

SubscribeAppendix

| Country | Personal Dividend Income Tax Rate | Capital Gains Tax Rate | Corporate Income Tax Rate | Integrated Corporate Tax Rate (Dividends) | Integrated Corporate Tax Rate (Capital Gains) |

|---|---|---|---|---|---|

| Australia | 23.5% | 24.5% | 30.0% | 46.5% | 47.2% |

| Austria | 25.0% | 25.0% | 25.0% | 43.8% | 43.8% |

| Belgium | 25.0% | 0.0% | 34.0% | 50.5% | 34.0% |

| Canada | 33.8% | 22.6% | 26.3% | 51.2% | 42.9% |

| Chile | 25.0% | 20.0% | 20.0% | 40.0% | 36.0% |

| Czech Republic | 15.0% | 0.0% | 19.0% | 31.2% | 19.0% |

| Denmark | 42.0% | 42.0% | 24.5% | 56.2% | 56.2% |

| Estonia | 0.0% | 21.0% | 21.0% | 21.0% | 21.0% |

| Finland | 27.2% | 33.0% | 20.0% | 41.8% | 46.4% |

| France | 44.0% | 34.4% | 38.0% | 65.2% | 59.3% |

| Germany | 26.4% | 25.0% | 30.2% | 48.6% | 47.7% |

| Greece | 10.0% | 15.0% | 26.0% | 33.4% | 37.1% |

| Hungary | 16.0% | 16.0% | 19.0% | 32.0% | 32.0% |

| Iceland | 20.0% | 20.0% | 20.0% | 36.0% | 36.0% |

| Ireland | 48.0% | 33.0% | 12.5% | 54.5% | 41.4% |

| Israel | 30.0% | 25.0% | 26.5% | 48.6% | 44.9% |

| Italy | 20.0% | 26.0% | 27.5% | 42.0% | 46.4% |

| Japan | 20.3% | 20.3% | 37.0% | 49.8% | 49.8% |

| Korea | 35.4% | 0.0% | 24.2% | 51.0% | 24.2% |

| Luxembourg | 20.0% | 0.0% | 29.2% | 43.4% | 29.2% |

| Mexico | 17.1% | 10.0% | 30.0% | 42.0% | 37.0% |

| Netherlands | 25.0% | 0.0% | 25.0% | 43.8% | 25.0% |

| New Zealand | 6.9% | 0.0% | 28.0% | 33.0% | 28.0% |

| Norway | 27.0% | 27.0% | 27.0% | 46.7% | 46.7% |

| Poland | 19.0% | 19.0% | 19.0% | 34.4% | 34.4% |

| Portugal | 28.0% | 28.0% | 31.5% | 50.7% | 50.7% |

| Slovak Republic | 0.0% | 25.0% | 22.0% | 22.0% | 41.5% |

| Slovenia | 25.0% | 0.0% | 17.0% | 37.8% | 17.0% |

| Spain | 27.0% | 27.0% | 30.0% | 48.9% | 48.9% |

| Sweden | 30.0% | 30.0% | 22.0% | 45.4% | 45.4% |

| Switzerland | 20.0% | 0.0% | 21.1% | 36.9% | 21.1% |

| Turkey | 17.5% | 0.0% | 20.0% | 34.0% | 20.0% |

| United Kingdom | 28.7% | 28.0% | 21.0% | 45.1% | 43.1% |

| United States | 28.7% | 28.7% | 39.1% | 56.6% | 56.6% |

| Source: PwC Worldwide Tax Summaries and OECD Tax Database | |||||

| Classical System | Modified Classical System | Full Credit Imputation | Partial Credit Imputation | Full Dividend Exemption | Partial Dividend Exemption | Other |

|---|---|---|---|---|---|---|

| Austria | Denmark | Australia | Korea | Estonia | Finland | Hungary |

| Belgium | Japan | Canada | United Kingdom | Slovak Republic | France | Norway |

| Czech Republic | Poland | Chile | Luxembourg | |||

| Germany | Portugal | Mexico | Turkey | |||

| Greece | Spain | New Zealand | ||||

| Iceland | Switzerland | |||||

| Israel | United States | |||||

| Italy | ||||||

| Netherland | ||||||

| Slovenia | ||||||

| Sweden | ||||||

| Source: OECD Tax Database, Table II.4, 2014 | ||||||

| Ordinary Income | Reduced Rate | 50 Percent Exemption | Fully Exempt |

|---|---|---|---|

| Denmark | Austria | Australia | Belgium |

| Estonia | Chile | Canada | Czech Republic |

| Finland | France | Korea | |

| Norway | Germany | Luxembourg | |

| Slovak Republic | Greece | Netherlands | |

| Hungary | New Zealand | ||

| Iceland | Slovenia | ||

| Ireland | Switzerland | ||

| Israel | Turkey | ||

| Italy | |||

| Japan | |||

| Mexico | |||

| Poland | |||

| Portugal | |||

| Spain | |||

| Sweden | |||

| United Kingdom | |||

| United States | |||

| Source: PwC Worldwide Tax Summaries, 2014 | |||

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

Subscribe[1] U.S. Department of Treasury, Integration of the Individual and Corporate Tax Systems—Taxing Business Income Once, (Jan. 1992), http://www.treasury.gov/resource-center/tax-policy/Documents/integration.pdf.

[2] The top marginal dividend and capital gains income tax rate is 20 percent. In addition, there is a 3.8 percent net investment tax, for a total federal rate of 23.8 percent. State and local governments also tax capital gains and dividend income.

[3] This is the combined top marginal individual income tax rate on dividends (23.8 percent) plus the weighted average of state and local income tax rates on dividends.

[4] The formula is 1-((1-x)*(1-y)), where x is the corporate income tax rate and y is the top marginal personal income tax rate on dividend income.

[5] U.S. Department of Treasury, Integration of the Individual and Corporate Tax Systems—Taxing Business Income Once, (Jan. 1992), http://www.treasury.gov/resource-center/tax-policy/Documents/integration.pdf.

[6] Some state do not recognize some forms of pass-through business, thus levying the corporate income tax on their net income. Some states also levy franchise taxes on pass-through business income.

[7] OECD Tax Database.

[8] The average combined top marginal income tax rate on sole proprietorship and partnership income. Kyle Pomerleau, An Overview of Pass-through Businesses in the United States, Tax Foundation Special Report No. 227, (Jan. 2015), https://taxfoundation.org/article/overview-pass-through-businesses-united-states.

[9] Internal Revenue Service, SOI Tax Stats – Integrated Business Data, 1980–2008, http://www.irs.gov/uac/SOI-Tax-Stats-Integrated-Business-Data; Internal Revenue Service, Business Tax Statistics, 2009–2011, http://www.irs.gov/uac/Tax-Stats-2.

[10] U.S. Department of Treasury, Integration of the Individual and Corporate Tax Systems—Taxing Business Income Once, (Jan. 1992), http://www.treasury.gov/resource-center/tax-policy/Documents/integration.pdf.

[11] Only what are called “franked” dividends are eligible for a credit against corporate income taxes paid. Australia has what is called a franking account. This account is set up for each corporation to deposit after-tax income that can be distributed to shareholders. Only income that has first faced the full 30 percent corporate income tax rate is eligible to be deposited. Shareholders that receive dividends from this account are eligible for the tax credit against their dividend income tax. Any dividends that are not from this account are not eligible for the credit.

[12] OECD Tax database, Table II.4, May 2014.

[13] Estonia only applies its corporate income tax to distributed profits.

[14] Providing that certain requirements are met. For example, the United States provides a reduced “long-term” capital gains rate of 28.7 percent provided that the stock was held for at least a year. PwC, PwC Worldwide Tax Summaries, 2014, http://taxsummaries.pwc.com/uk/taxsummaries/wwts.nsf/ID/PPAA-85RDKF.