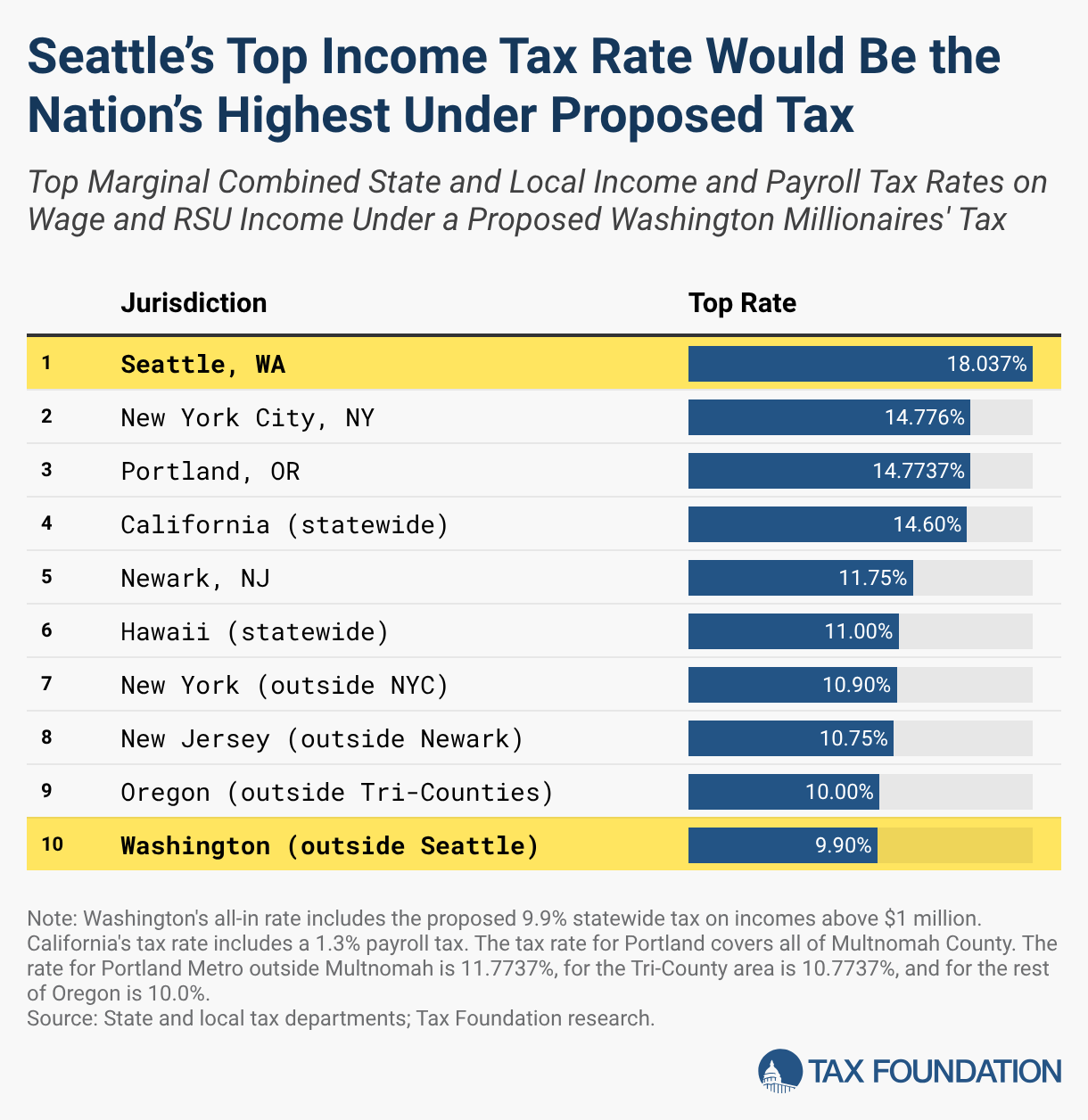

In Washington, which had no income taxation until recently, many high earners could face the highest combined state and local top rate in the country—18.037 percent (split across employer and employee)—if lawmakers adopt a new proposed millionaires’ taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities..

In December, Governor Bob Ferguson (D) announced his support for percolating legislative proposals to adopt a 9.9 percent income tax on income above $1 million. Such a tax would make the state increasingly undesirable for high earners, particularly in the state’s crucial tech sector. Washington already taxes high earners’ capital gains income with a 9.9 percent rate on capital gains income above $1 million (7 percent between $278,000 and $1 million), and both the state and the city of Seattle have payroll taxes that create significant additional tax burdens on high earners and their employers.

At the state level, a 0.58 percent Washington Cares tax for long-term care insurance applies to all wage income. The city of Seattle applies two additional payroll taxes: the JumpStart Payroll Expense Tax on high-earning employees, which funds housing, economic development, and climate initiatives, and imposes rates as high as 2.557 percent, and a Social Housing Tax of 5 percent on income above $1 million. Washington also imposes a Paid Family & Medical Leave Tax of 1.13 percent, but because it is tied to the Social Security wage base (currently $184,500), it does not increase the marginal rate for the highest earners.

These payroll taxes are remitted by employers, not employees, but they are priced into wages. As new taxes are imposed, employers may initially bear some of the burden because wages are “sticky” and the adjustment is largely through smaller raises or lower starting salaries. Ultimately, however, the economic incidence of payroll taxes is on employees, just like the individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source. They increase the cost of employing workers in Seattle and reduce the wages of those employed there. For employees with more than $1 million in compensation, the all-in marginal rate would be an eye-popping 18.037 percent if the state implemented a new 9.9 percent tax on high earners.

With federal income tax (37 percent) and Medicaid tax (2.9 percent) liability, that yields an all-in top rate of 57.937 percent.

Table 1. Seattle’s High Earners Could Face Top Income Tax Rates of Almost 58 Percent

Top Marginal Rates Under Current and Proposed Taxes

| Tax | Rate |

|---|---|

| Washington Millionaires' Tax (proposed) | 9.90% |

| WA Cares Tax | 0.58% |

| Seattle Social Housing Tax | 5.00% |

| Seattle JumpStart Tax | 2.557% |

| State and Local Subtotal | 18.037% |

| Federal Income Tax | 37.00% |

| Medicaid Tax | 2.90% |

| Federal Subtotal | 39.90% |

| Total Marginal Tax Rate | 57.937% |

For tens of thousands of tech workers in Washington, restricted stock units are a key component of compensation. RSUs are essentially a promise to grant shares in the future, contingent on certain conditions being met (e.g., remaining with the company for a set period or meeting performance benchmarks). Once the employee has fulfilled the vesting conditions, the shares are granted, sometimes in one year but often over several years. These RSUs are income, but they are not capital gains income. (There may be capital gains income later if the shares are sold after appreciating in value.) These vesting events are not taxed in Washington now, but would be under the proposed tax, which is how tech workers could find themselves subject to a tax on incomes above $1 million even though salaries are rarely that high.

Importantly for a “millionaires’ tax,” RSU vesting can be lumpy. While many established companies have regular vesting (often quarterly), some companies use weighted vesting schedules for new hires, so that most of their vesting occurs in later years. Even more significantly, startups often have “double trigger” RSUs with both a time-based service condition and a liquidity-event condition (an IPO or acquisition). Someone could work at a startup for five years, and then when it goes public, all five years of accumulated stocks vest at once, yielding income above $1 million even though their average income over the period is well below that.

For Washington taxpayers with adjusted gross incomeFor individuals, gross income is the total of all income received from any source before taxes or deductions. It includes wages, salaries, tips, interest, dividends, capital gains, rental income, alimony, pensions, and other forms of income. For businesses, gross income (or gross profit) is the sum of total receipts or sales minus the cost of goods sold (COGS)—the direct costs of producing goods above $1 million, 32 percent of their income is from capital gains, 28 percent is from wages and RSU vesting, 19 percent each comes from interest and dividends and pass-through business income, and 2 percent derives from other sources. (This is for all income of those with $1 million or more in AGI, including for amounts below $1 million for those filers.) With capital gains already taxed and relatively little actual wage income above $1 million, the proposed new tax is predominantly a tax on receiving RSUs, owning a small business, and earning interest and dividend income.

Table 2. Washington’s Millionaires Derive Income from Investments, RSUs, and Business Ownership

Sources of Income for Washington Filers with AGIs of $1 Million or More (2022)

| Income Source | Income Share |

|---|---|

| Capital Gains | 31.8% |

| Wages and RSU Vesting | 28.0% |

| Interest & Dividends | 19.1% |

| Business Income | 18.7% |

| Other Income | 2.4% |

Not all small businesses are pass-throughs, and not all pass-throughs are small businesses, but there’s a strong alignment, and according to the US Small Business Administration, Washington’s 672,472 small businesses employ 1.4 million people, representing 48.4 percent of all Washington employees. A 9.9 percent tax on small business owners imposes one of the nation’s highest taxes on their income in a state that already imposes a high-rate gross receipts taxGross receipts taxes are applied to a company’s gross sales, without deductions for a firm’s business expenses, like compensation, costs of goods sold, and overhead costs. Unlike a sales tax, a gross receipts tax is assessed on businesses and applies to transactions at every stage of the production process, leading to tax pyramiding. (the Business & Occupation Tax) and subjects an unusually high share of their business inputs to the sales taxA sales tax is levied on retail sales of goods and services and, ideally, should apply to all final consumption with few exemptions. Many governments exempt goods like groceries; base broadening, such as including groceries, could keep rates lower. A sales tax should exempt business-to-business transactions which, when taxed, cause tax pyramiding. .

Washington’s existing tax code is heavily skewed toward business taxes, in part because it forgoes a broad-based individual income tax but, unlike other states without one, doesn’t have a low-tax, limited-government ethos. This forces a disproportionate share of the tax burden onto businesses. By adopting a high-rate income tax only on high earners, Washington would create the worst of both worlds for its small business owners, limiting their ability to grow and undercutting job creation.

Washington residents, who long understood the state’s constitution to prohibit income taxation, have good reason to be concerned about the proposed income tax even if their incomes are well below its threshold, for at least two reasons.

First, if lawmakers and jurists conclude that the state constitution does not prohibit an income tax on high earners, it’s highly possible that this tax would eventually be applied to everyone else as well. (Governor Ferguson has suggested a constitutional amendment prohibiting income taxation below $1 million adjusted for inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spendin, but, to date, he has not publicly conditioned support for millionaires’ tax legislation on submitting such an amendment to the voters.) In the early days of state income taxes, many states only applied their income tax to high earners. Today, every state income tax is broadly applied to earners at all levels of income.

Second, a tax this aggressive would do real damage to Washington’s economy, sending jobs and economic opportunity elsewhere. In particular, for significant swaths of the state’s tech sector, already the target of anomalously high business taxes, a 9.9 percent income tax could prove the last straw, driving any subsequent expansion to other states, and quite possibly taking existing jobs with them.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

Subscribe