As Congress debates expensing and other policies impacting business investment, lawmakers should consider the importance of business investment in research and development (R&D) as a driver for economic growth. Recent studies suggest that the economic benefits of R&D spending are even greater than previously understood.

R&D is not just another business expense. Rather, it is a key engine of long-term productivity and innovation. As Congress considers how to boost growth through better taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. policy, immediate expensing of R&D spending and reducing the compliance burden of the R&D tax creditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income rather than the taxpayer’s tax bill directly. are the lowest-hanging fruit.

The Tax Code’s Treatment of R&D

Under Section 174 of the Internal Revenue Code (IRC), qualified research expenditures include both direct and indirect costs associated with developing or improving a product or process. These costs may include wages, supplies, and even depreciationDepreciation is a measurement of the “useful life” of a business asset, such as machinery or a factory, to determine the multiyear period over which the cost of that asset can be deducted from taxable income. Instead of allowing businesses to deduct the cost of investments immediately (i.e., full expensing), depreciation requires deductions to be taken over time, reducing their value and discouraging investment. of tangible assets like buildings and equipment.

Companies that engage in qualified R&D activities can claim deductions for their expenditures but must spread them out over 5 years for domestic R&D or 15 years for foreign R&D. Not being able to deduct the costs in the year the expenses are incurred leads to tax savings being delayed and diminished in present value, effectively increasing the after-tax cost of conducting R&D.

In addition, under IRC Section 41, companies may claim tax credits for a subset of section 174 expenditures either as a regular credit or alternative simplified credit, which provides a dollar-for-dollar reduction in tax liability. Claiming the credit will reduce the deduction by the amount of credits claimed, leading to two sources of tax relief for the same expense.

While research is often discussed as a single category, it can be broadly divided into three types:

- Basic research investigates fundamental topics without immediate commercial applications. This type of research has the greatest long-term impact on economic growth, as it can create new industries or dramatically change others. However, it is primarily conducted by universities and public institutions due to the high uncertainty and long lag in returns, often averaging multiple decades, depending on the industry.

- Applied research focuses on practical applications of scientific discoveries. Companies use applied research to translate theoretical insights into usable technologies.

- Developmental research enhances existing technologies to optimize performance for specific commercial purposes. This stage is closest to commercialization and typically has the highest expected returns.

Despite these distinctions, the tax code generally treats all R&D activities the same. This one-size-fits-all approach overlooks the fact that basic research generates the highest long-term societal benefits yet struggles to secure private funding due to its uncertain nature.

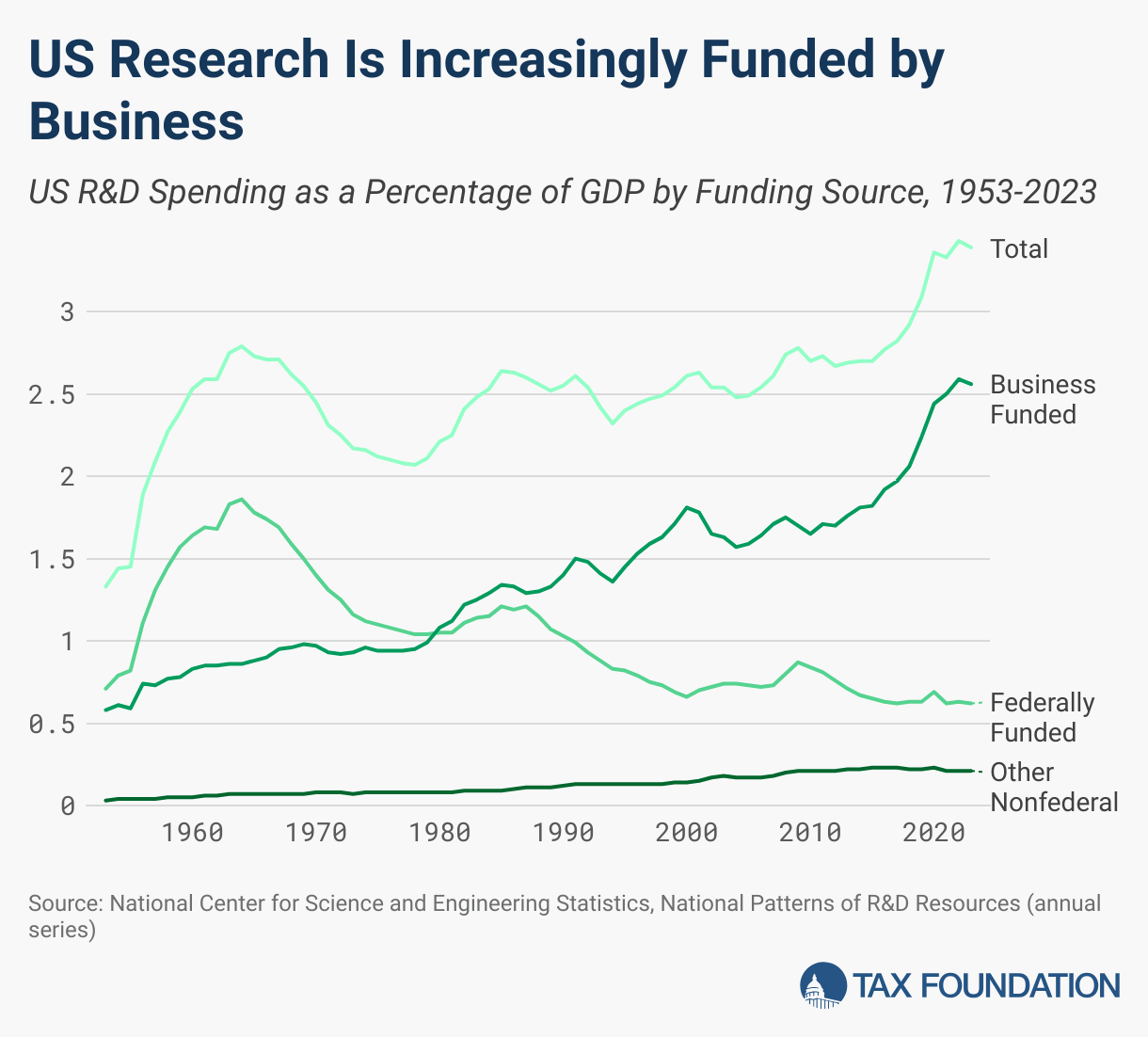

The Changing Landscape of R&D Investment

Over the past 70 years, total R&D spending as a share of GDP has increased from 1.3 percent in 1953 to 3.4 percent in 2023. While overall growth has occurred, public investment in R&D has declined even as private investment has increased.

Private sector investment is largely directed toward developmental research, rising from 74 percent of all business R&D in 1953 to nearly 79 percent in 2023, while basic and applied research trail behind. Developmental research is crucial for refining and commercializing new technologies, but it does not generate the same long-term spillover benefits as basic and applied research.

Even though the federal government is the largest funder of basic research, business sector basic research spending has grown recently at around 10 percent annually while overall R&D spending has grown at a rate of 7 percent.

The Unique Nature of R&D – Spillovers and Diffusion

R&D is distinct from other types of investment because its benefits often extend beyond the firm conducting the research. Spillover effects occur when knowledge created by one entity spreads and benefits others without direct compensation, creating surplus value that is not captured by the original firm. These spillovers can broadly benefit society, such as increased life expectancy due to a novel medicine.

Estimating effects is difficult due to the indirect nature of returns, but recent studies suggest that the economic returns from R&D investment exceed those from physical capital investment. Moreover, research diffusion can occur almost instantaneously, meaning that R&D conducted abroad can be just as beneficial as domestic research.

From an economic perspective, research teams are a limited resource, since only so many experts possess the knowledge needed to push the frontiers of a given field. In contrast, the technologies they produce can often be shared among many users without being depleted, provided those users have the necessary access, such as through licensing or partnerships.

Because research is getting costlier due to the difficulty of reaching new findings, it is increasingly difficult for new research teams to enter pre-existing fields, making existing research teams highly valuable. Penalizing companies for funding research teams abroad could lead to those teams being acquired by foreign competitors, resulting in a loss of competitive advantage for the US. Furthermore, most other developed countries have more generous R&D tax incentives than the US, and the gap has generally grown in recent years.

While private sector R&D focuses heavily on development, public R&D spillovers tend to be more effective than private spillovers. Government agencies, universities, and public institutions conduct more basic research, which is widely disseminated and leads to broader economic benefits. Because basic research is not typically protected by patents or trade secrets, it is more easily adopted and used by other firms. Additionally, basic research often addresses foundational questions that require further applied research before becoming commercially viable, making patent protection impractical.

Smaller firms also experience larger productivity gains from public R&D spillovers. Unlike large corporations with in-house research teams, small firms often lack the capacity to conduct extensive R&D, but they are more flexible to pursue new avenues that might have been opened by research done in the public sector. Immediate expensing of R&D spending and reducing the compliance burden of the R&D tax credit are the most effective means of helping small and medium-sized enterprises (SMEs) enter the market and facilitating growth in the economy.

R&D Full ExpensingFull expensing allows businesses to immediately deduct the full cost of certain investments in new or improved technology, equipment, or buildings. It alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs. Has Larger Effects than Estimated

Tax Foundation estimates R&D expensing has a high “bang for the buck,” or increase in economic output per dollar of tax revenue loss. Our estimates likely understate the growth impacts of R&D policies as they do not capture the spillover effects.

Spillover effects are difficult to model as the expected value of investment does not follow a normal distribution, but a distribution where almost all investments have close to no value and very few account for almost everything. However, not all of the effects are as opaque.

Research from Stanford Business School estimates the requirement to amortize R&D beginning in 2022 has led to a reduction of $12.2 billion in R&D expenditures and a 62 percent increase in effective tax rates on average during the first year. This implies that going back to full expensing permanently would result in a similarly sized increase in research expenditures.

It is also likely that expensing would encourage smaller research companies to invest due to the simplified tax code and more certain compliance landscape.

Large Firms Dominate R&D Credit Applications

Data show that larger firms apply for R&D credits at a significantly higher rate than smaller firms, despite smaller firms benefitting more from tax credits. This is concerning because startups and small enterprises are often at the forefront of breakthrough innovations. The lack of SME participation in research credit applications is due to a lack of awareness about expense eligibility and the high administrative burden required to comply with research credit regulations.

Regarding the challenge of funding basic research, one solution may be to boost and redesign the R&D credit to better target basic research, perhaps through increased collaboration between business funders and universities and other non-profit research centers that conduct the research. Currently, the university basic research credit encourages companies to fund universities or non-profit companies to conduct research without specific commercial objectives, but this credit is a missed opportunity to further enhance research cooperation between private and public research teams as it does not cover expenses made by firms.

In sum, it is important to get R&D policy right, and tax policy is a key tool. Most clearly, companies should be allowed to fully deduct (expense) their R&D costs, as was the case prior to 2022. Lawmakers may also want to revisit the R&D credit to simplify the rules so that start-ups and small companies can better use it, and better target it for basic research where there is more evidence of positive spillovers.

Share this article