Vice President Kamala Harris’s proposal to raise the federal corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. rate to 28 percent would increase the combined average top taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. rate on corporate income to 32.2 percent, the second highest in the Organisation for Economic Co-operation and Development (OECD), reducing US competitiveness and long-run economic output.

As policymakers debate the future of the federal corporate tax rate, they must also consider state-level corporate taxes to better understand the total tax burden on corporate income.

Under current law, corporations in the United States pay federal corporate income taxes levied at a 21 percent rate plus state-level corporate taxes that range from zero to 9.8 percent, resulting in a combined average top tax rate of 25.6 percent in 2024.

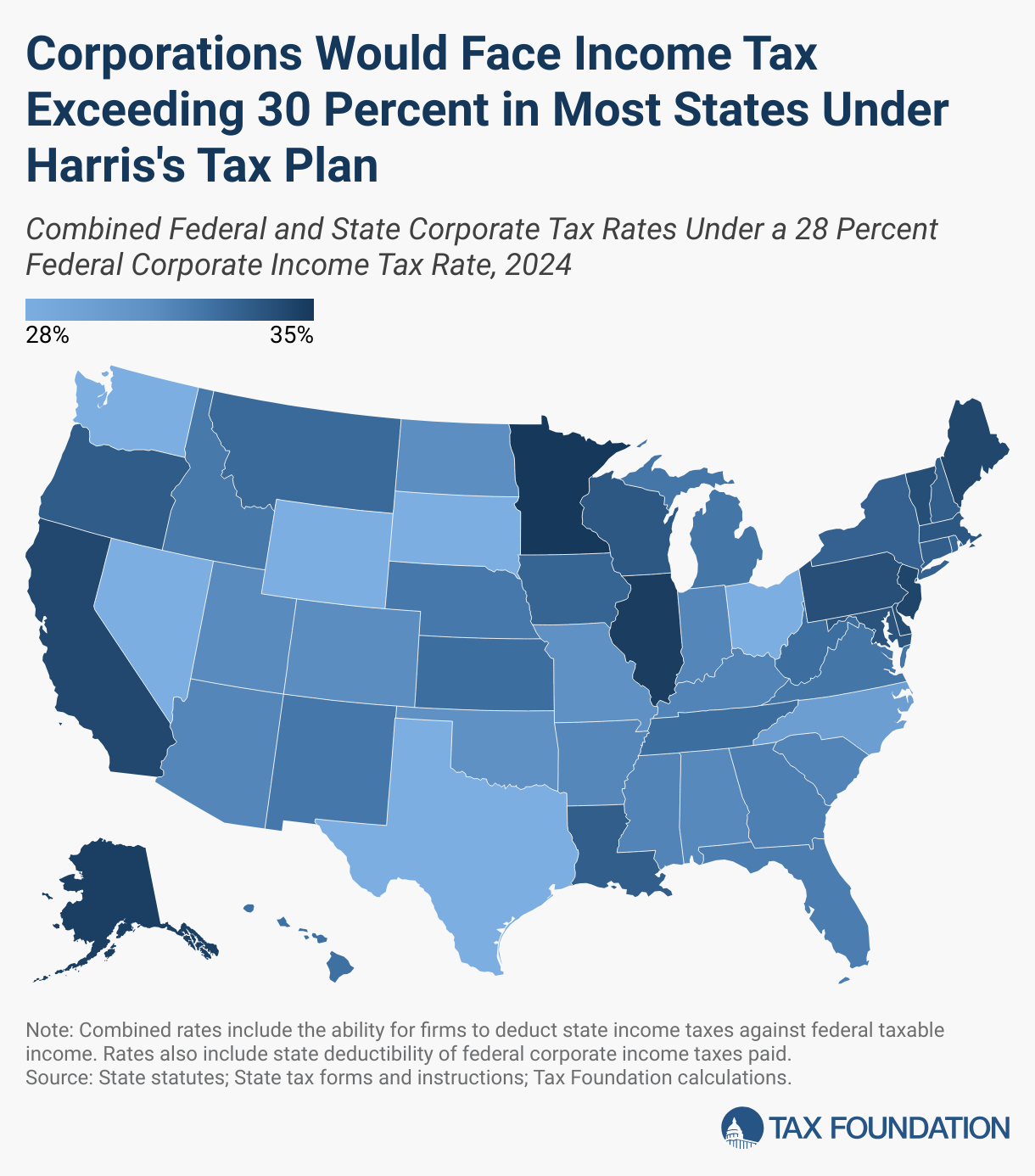

If the federal corporate tax rate were raised to 28 percent this year, corporations operating in 43 states and the District of Columbia would face corporate tax rates exceeding 30 percent.

Corporations in Alaska, California, Delaware, Illinois, Maine, Minnesota, New Jersey, Pennsylvania, and Vermont would face combined rates at or above 34 percent. Minnesota’s 35.1 percent combined rate would exceed the highest combined corporate tax rate in the OECD, a distinction currently held by Colombia with a 35.0 percent rate.

Only seven states—Ohio, Nevada, North Carolina, South Dakota, Texas, Washington, and Wyoming—would face a corporate rate less than 30 percent, due to forgoing a state corporate income tax (except for North Carolina, which has a low rate of 2.5 percent).

Corporations may deduct state corporate income tax paid against federal taxable incomeTaxable income is the amount of income subject to tax, after deductions and exemptions. Taxable income differs from—and is less than—gross income. , lowering the effective federal corporate income tax rate. For example, a corporation in Michigan may deduct tax paid at a 6 percent flat rate against a 28 percent federal corporate income tax, reducing its effective top federal rate to 26.3 percent and yielding a combined rate of 32.3 percent. Additionally, Alabama allows corporations to fully deduct federal corporate income tax against state corporate income tax, lowering the effective corporate income tax rate faced by corporations there.

Raising the combined US corporate rate to the second highest in the OECD would encourage corporations to depart from the US, reducing economic output and worker wages across the income spectrum. Retaining the 21 percent corporate rate—which places the US in the middle of the pack when including the state-level corporate tax burden—ensures the US remains an attractive location for corporate investment.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe