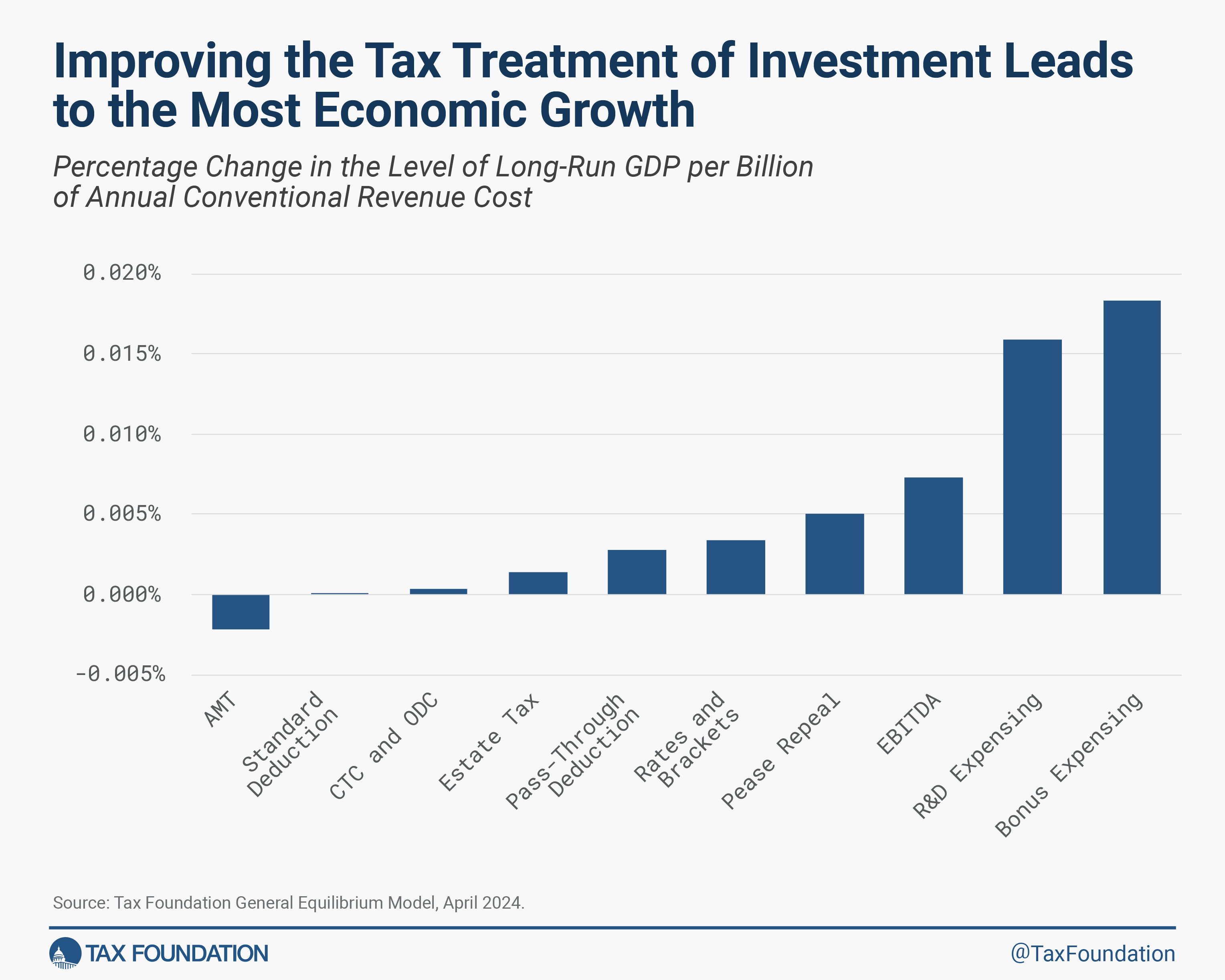

As the US House and Senate iron out their plans to extend the expiring provisions of the TaxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. Cuts and Jobs Act (TCJA), tax changes are being considered to offset at least some of the $4.5 trillion revenue cost over 10 years. Congress should design a pro-growth and fiscally responsible package that retains the 21 percent corporate tax rate, makes permanent tax cuts with the most bang-for-the-buck, such as R&D and 100 percent bonus expensing, and uses offsets with relatively small economic costs.

One potential offset is a limitation on corporate deductions for state and local taxes, or C-SALT. As we discuss below, a C-SALT limit will reduce economic output as it is like a corporate tax rate increase, making the path to a pro-growth package more challenging.

Different design choices for a C-SALT limit will affect how economically damaging a limit would be. Limiting C-SALT would also place larger tax burdens on specific industries, notably the manufacturing, finance and insurance, and mining sectors. Finally, many (but not all) other countries disallow deductions for income taxes while deductibility for property and excise taxes is very common around the world.

Design and Revenue Considerations

Businesses pay several different state and local taxes, including income, property, sales, and excise taxes. Lawmakers need to consider which deductions to limit and the potential revenue implications. Most discussion of limitations focuses on entity-level income taxes, such as state and local corporate income taxes and pass-through businessA pass-through business is a sole proprietorship, partnership, or S corporation that is not subject to the corporate income tax; instead, this business reports its income on the individual income tax returns of the owners and is taxed at individual income tax rates. entity taxes. The limit could also apply to property taxes.

Disallowing a deduction for state and local corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. paid would raise $209 billion in revenue over 10 years if the deduction is fully repealed. Applying the limit to property taxes would raise an additional $223 billion over the same period.

These revenue estimates only consider the revenue effect of limiting the deduction for C corporations. Pass-through businesses, such as S corporations and partnerships, can similarly deduct business taxes when calculating net income.

The tax code should ideally treat similar sources of income the same regardless of the firm’s chosen form of business. If lawmakers apply limitations to corporations, they should consider extending that treatment to pass-through firms, though this would increase the potential revenue and economic implications.

For example, eliminating the deduction for entity-level pass-through business taxes (workarounds) would raise over $226 billion over 10 years. Our forthcoming work will examine the tax treatment of pass-through workarounds in more detail.

Economic Implications

The deduction for business taxes paid under current law reduces the effective statutory tax rate. For example, the net corporate income tax rate in the United States is 25.63 percent, which is the sum of the federal rate of 21 percent plus the average state tax rate, reduced by the C-SALT deduction.

Eliminating the deduction for income tax, for example, would raise the all-in rate by about 1.2 percentage points. Increasing the effective tax rate would diminish investment incentives in the United States.

Our modeling estimates that eliminating the deduction for corporate state and local taxes paid would reduce long-run economic output by 0.1 percent, roughly the same economic impact as a 1 percentage point increase of the corporate income tax. This would reduce hours worked by 28,000 full-time equivalent jobs.

Dollar-for-dollar, extending the C-SALT limitation to property taxes has a greater negative effect than disallowing income tax deductions. We find eliminating the deduction for income and property taxes would reduce output by 0.6 percent and hours worked by 147,000 full-time equivalent jobs.

Extending the limitation to property taxes has a greater economic impact because property taxes fall more heavily on the normal returns to investment than a corporate income tax. The economic effect only comes from the impact on property improvements and not on land, which makes up about 19 percent of the combined value of land and improvements.

The ultimate economic impact, however, depends on the composition of the entire package. Like the original TCJA, the package will include reforms that would both improve investment incentives and diminish them, making it important that permanent pro-growth provisions are prioritized.

But if lawmakers use C-SALT to offset policies that do not support long-run growth, then they will risk adopting a package that, on net, reduces economic output and makes our fiscal challenges harder to address.

{kind=link}

If lawmakers make R&D expensing permanent, for example, it would boost output by 0.1 percent and more than offset the negative effect of limiting the deduction for corporate income taxes paid.

Or if lawmakers make 100 percent bonus depreciationBonus depreciation allows firms to deduct a larger portion of certain “short-lived” investments in new or improved technology, equipment, or buildings in the first year. Allowing businesses to write off more investments partially alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs. permanent, it would increase output by 0.5 percent in the long run and roughly offset the negative economic implications of limiting the income and property tax deductionA tax deduction allows taxpayers to subtract certain deductible expenses and other items to reduce how much of their income is taxed, which reduces how much tax they owe. For individuals, some deductions are available to all taxpayers, while others are reserved only for taxpayers who itemize. For businesses, most business expenses are fully and immediately deductible in the year they occur, but others, particularly for capital investment and research and development (R&D), must be deducted over time. for corporations.

Table 1. Long-Run Economic Effects of Options for C-SALT and Pro-Growth Tax Changes

| Option | Repeal C-SALT Deductions for Corporate Income Tax | Cancel R&D Amortization | Repeal C-SALT Deductions for Corporate Income Tax And Cancel R&D Amortization | Repeal C-SALT Deductions for Corporate Income and Property Tax | Make 100 Percent Depreciation for Short-Lived Assets Permanent | Repeal C-SALT Deductions for Corporate Income and Property Tax and Make 100 Percent Depreciation for Short-Lived Assets Permanent |

|---|---|---|---|---|---|---|

| GDP | -0.1% | 0.1% | Less than +0.05% | -0.6% | 0.5% | Less than -0.05% |

| GNP | -0.1% | 0.1% | Less than +0.05% | -0.5% | 0.5% | Less than -0.05% |

| Capital Stock | -0.2% | 0.3% | 0.10% | -1.1% | 1.0% | Less than -0.05% |

| Wage Rate | -0.1% | 0.1% | Less than +0.05% | -0.5% | 0.5% | Less than -0.05% |

| Hours-Weighted Full-Time Equivalent Jobs | -24,000 | 28,000 | 7,000 | -147,000 | 145,000 | -6,000 |

| Ten-Year Conventional Revenue Impact (2025-2034) | $209.4 | -$201.5 | $21.3 | $432.0 | -$350.1 | $81.9 |

Note that the swaps we modeled are not revenue neutral. Because accelerated depreciationDepreciation is a measurement of the “useful life” of a business asset, such as machinery or a factory, to determine the multiyear period over which the cost of that asset can be deducted from taxable income. Instead of allowing businesses to deduct the cost of investments immediately (i.e., full expensing), depreciation requires deductions to be taken over time, reducing their value and discouraging investment. provisions cost less in the long run than in the 10-year window, lawmakers would have additional revenue outside the budget window from capping state and local tax deductions to enact additional pro-growth reforms. For example, they could expand expensing to other business investment including structures.

The options above represent a net tax increase on C corporations, since the benefits of R&D expensing and bonus depreciation accrue to C corporations and pass-through businesses. Lawmakers could include other tax reductions for C corporations to avoid worsening their competitiveness.

Industry Impacts

While pairing C-SALT limitations with pro-growth tax cuts may come out ahead for the economy overall, C-SALT limitations will have disparate impacts on firms depending on industry and state and local tax payments.

Corporate state and local taxes vary across a wide range of industries. Manufacturing firms pay the highest share overall at 6.3 percent of value-added. Other industries like agriculture and utilities pay 5.6 percent of their value-added in state and local taxes. Finance, insurance, and management businesses follow at 5.4 percent, while mining firms pay about 5 percent of value-added in state and local taxes.

Table 2. Estimated Corporate State and Local Taxes Paid by Industry, 2025

| Industry | Value-Added, 2023, Billions | Corporate State and Local Taxes Paid, 2025, Billions | State and Local Taxes Paid as a Portion of 2023 Value-Added |

|---|---|---|---|

| Manufacturing | $2,840.4 | $179.2 | 6.3% |

| All other industries | $720.7 | $40.0 | 5.6% |

| Finance, insurance and management | $2,015.6 | $109.5 | 5.4% |

| Mining | $411.8 | $20.7 | 5.0% |

| Retail trade | $1,772.4 | $68.9 | 3.9% |

| Transportation and warehousing | $943.7 | $33.7 | 3.6% |

| Information | $1,477.9 | $46.3 | 3.1% |

| Wholesale trade | $1,653.0 | $49.6 | 3.0% |

| Accommodation and food services | $911.8 | $21.4 | 2.3% |

| Administrative services | $886.6 | $20.3 | 2.3% |

| Professional, scientific and technical services | $2,725.1 | $39.6 | 1.5% |

| Miscellaneous services | $3,240.0 | $39.4 | 1.2% |

| Construction | $1,220.6 | $13.5 | 1.1% |

| Real estate and rental and leasing | $3,796.0 | $13.8 | 0.4% |

| Total | $24,615.6 | $695.9 | 2.8% |

The benefits of 100 percent bonus depreciation and R&D expensing also vary by industry. For example, manufacturing receives a sizable share of the benefits of R&D expensing, reducing their federal taxes paid by about 1.2 percent of the manufacturing industry’s value-added. The information industry sees vast benefits from 100 percent bonus depreciation, while industries such as construction see lesser benefits.

Table 3. Estimated Share of Taxes Changes Under 100% Bonus Depreciation and R&D Expensing by Industry

| Industry | Value-Added, 2023, Billions | Change in Federal Taxes Paid Under 100% Bonus Depreciation, 2025 | Share of Federal Taxes Paid Under 100% Bonus as a Portion of Value Added | Change in Federal Taxes Paid Under R&D Expensing, 2025 | Share of Federal Taxes Paid Under R&D Expensing as a Portion of Value-Added |

|---|---|---|---|---|---|

| Real estate and rental and leasing | $3,796.0 | -$3.0 | -0.1% | $0.0 | Less than -0.05% |

| Miscellaneous services | $3,240.0 | -$0.5 | 0.0% | -$0.1 | Less than -0.05% |

| Manufacturing | $2,840.4 | -$9.5 | -0.3% | -$33.4 | -1.2% |

| Professional, scientific and technical services | $2,725.1 | -$1.5 | -0.1% | -$2.1 | -0.1% |

| Finance, insurance and management | $2,015.6 | -$7.0 | -0.3% | -$0.5 | Less than -0.05% |

| Retail trade | $1,772.4 | -$5.5 | -0.3% | -$1.1 | -0.1% |

| Wholesale trade | $1,653.0 | -$4.3 | -0.3% | -$1.4 | -0.1% |

| Information | $1,477.9 | -$9.4 | -0.6% | -$4.0 | -0.3% |

| Construction | $1,220.6 | -$0.2 | 0.0% | -$0.1 | Less than -0.05% |

| Transportation and warehousing | $943.7 | -$4.2 | -0.4% | $0.0 | Less than -0.05% |

| Accommodation and food services | $911.8 | -$0.8 | -0.1% | -$0.1 | Less than -0.05% |

| Administrative services | $886.6 | -$0.6 | -0.1% | $0.0 | Less than -0.05% |

| All other industries | $720.7 | -$6.4 | -0.9% | $0.0 | Less than -0.05% |

| Mining | $411.8 | -$1.7 | -0.4% | -$0.2 | -0.1% |

| Total | $24,615.6 | -$54.5 | -0.2% | -$43.2 | -0.2% |

Can We Learn Anything from Our Trading Partners?

Another consideration for Congress is how new C-SALT deduction limits compare to the rest of the world. While international tax approaches are not and should not be the end-all, be-all of US tax reform, the international scene can help inform how changing US C-SALT deductions stacks up against peer countries.

Most countries allow deductions for property taxes from national income taxes but disallow deductions for subnational corporate income taxes.

Federal systems like the US national and subnational systems, which permit national deductibility of all subnational taxes, are uncommon across the globe.

International exceptions to the norms do exist. Two comparable federal systems in Europe take opposite approaches. In Germany, municipal-level trade taxes are not deductible against the 15 percent federal corporate income tax. But across the border in Switzerland, income taxes paid to cantons may be deducted against Swiss corporate income tax.

Like the German approach, corporations in Canada and Japan may not deduct provincial corporate income taxes from federal corporate tax.

Excise taxes paid by businesses are commonly deductible across the world. However, if companies receive a deduction or a credit for a tax (like a value-added tax), they do not receive a separate deduction within the corporate income tax.

Conclusion

Lawmakers should prioritize pro-growth tax policies and use the least economically damaging offsets to make the legislation fiscally responsible. If lawmakers choose to use C-SALT, they should carefully consider the economic trade-off with permanent, pro-growth tax cuts that support investment and innovation in the US.

The TCJA tilted investment incentives toward the US and improved the competitiveness of US-based companies. Further changes to corporate taxes must be considered through a lens that considers revenues, growth, and competitiveness.