Among President Joe Biden’s many tax proposals, one that has gotten less attention would modify how traditional retirement accounts are treated in the tax code. This proposal would shift some of the benefits of taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. deferral in traditional retirement accounts toward lower- and middle-income earners with the goal of encouraging additional saving by those taxpayers.

Biden proposes converting the current deductibility of traditional retirement contributions into matching refundable tax credits for 401(k)s, individual retirement accounts (IRAs), and other types of traditional retirement vehicles, such as SIMPLE accounts. Biden’s proposal would eliminate deductible traditional contributions and instead provide a 26 percent refundable tax credit for each $1 contributed. The tax creditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income rather than the taxpayer’s tax bill directly. would be deposited into the taxpayer’s retirement account as a matching contribution. Existing contribution limits would remain, and Roth-style tax treatment would be unaffected.

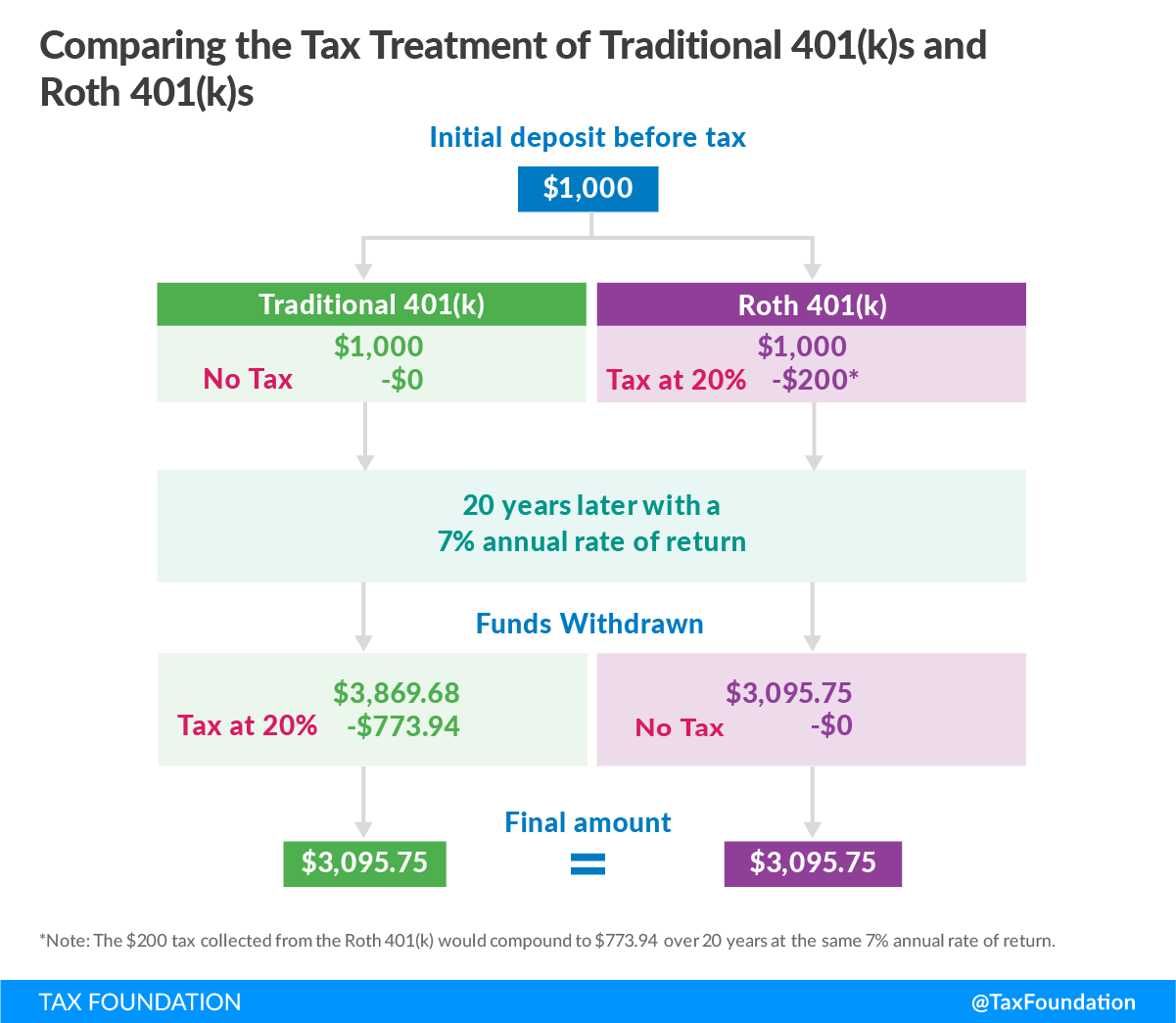

Under current law, traditional retirement accounts allow taxpayers to defer paying tax on contributions, deducting the contribution when calculating adjusted gross income (AGI). Taxpayers can let the contribution earn returns when invested, eventually paying tax on the distributions when the funds are withdrawn.

Traditional treatment can be contrasted with Roth-style tax treatment, where taxpayers pay income tax on the contribution up front but can withdraw the principal and return tax-free upon distribution. These tax treatments are equivalent (assuming the contribution and tax rates are identical over time), while ensuring the tax code is neutral with respect to saving and consumption decisions.

Because the individual income tax is progressive, the value of a tax deduction rises as income increases. For example, a taxpayer in the top marginal tax bracket receives a $37 tax benefit for every $100 contributed into a retirement account, while a taxpayer in the bottom bracket would only get a $10 tax benefit for the same $100 contribution.

Biden’s proposal to offer a flat 26 percent tax credit for retirement contributions seeks to equalize this treatment. Compared to current law, the flat credit would provide a larger benefit to lower-income earners and reduce the benefit to higher-income earners. This can be illustrated by converting the proposed 26 percent tax credit into a tax deduction of equal benefit, allowing us to see how much of a deduction would need to be provided to give the same benefit as the matching tax credit.

To see how, consider the after-tax cost of a taxpayer contributing $100 into a traditional account. The 26 percent credit is equal to a deduction at a 20.5 percent marginal tax rate for all taxpayers, independent of their income level: if a taxpayer contributed $100 and received a 20.5 percent deduction, their after-tax cost of contributing $100 to their retirement account would be $79.50. Under Biden’s proposal, if instead the taxpayer had no deduction, but contributed $79.50 and received a 26 percent matching credit, they would have contributed a total of about $100 at the same after-tax cost.

Additionally, this credit is expected to be roughly revenue neutral, with the elimination of deductibility offsetting the revenue lost from the new tax credit.

In effect, the proposal takes the rising value of deductibility by income level and converts it into a flat deduction. This provides a new benefit to taxpayers in lower income tax bracketsA tax bracket is the range of incomes taxed at given rates, which typically differ depending on filing status. In a progressive individual or corporate income tax system, rates rise as income increases. There are seven federal individual income tax brackets; the federal corporate income tax system is flat., while providing slightly worse treatment for higher earners.

For example, a taxpayer in the 12 percent tax bracket earning $35,000 would receive a 12 percent deduction under current law for their traditional retirement contributions, but under Biden’s proposal would see an effective deduction at a 20.5 percent marginal tax rateThe marginal tax rate is the amount of additional tax paid for every additional dollar earned as income. The average tax rate is the total tax paid divided by total income earned. A 10 percent marginal tax rate means that 10 cents of every next dollar earned would be taken as tax. (higher than currently) when they receive the 26 percent matching tax credit. By contrast, a taxpayer in the 37 percent tax bracket would only receive an equivalent deduction at a 20.5 percent marginal tax rate, rather than a deduction at a 37 percent marginal tax rate they receive under current law.

This means that taxpayers in the 10 percent and 12 percent tax brackets (roughly up to $80,250 filing jointly) would benefit from this change, while those in the higher brackets would lose some of the value of traditional accounts when compared to current law.

Proponents of this change argue that this would help encourage lower income earners to save by providing a salient reward for saving in the form of a matching tax credit and raise the value of saving on the margin, as higher earners tend to contribute more often (see table below). They also argue that higher earners would not decrease their saving on net, as they often use retirement accounts to shift other savings they already had from taxable to non-taxable accounts.

| Wage Income Level | Number of Taxpayers with Elective Contributions | Share of Taxpayers with Contributions |

|---|---|---|

| Source: IRS, “SOI Tax Stats – Individual Information Return Form W2 Statistics,” Tax Year 2017– Table 3.A. Note: This table does not include IRA contributions, though the distribution of such contributions is similar to defined contribution plans. | ||

| $1 to $25,000 | 7,576,971 | 13.67% |

| $25,000 to $50,000 | 18,878,432 | 43.77% |

| $50,000 to $75,000 | 13,632,135 | 59.69% |

| $75,000 to $100,000 | 7,469,588 | 69.40% |

| $100,000 to $200,000 | 8,030,911 | 76.33% |

| $200,000 to $500,000 | 2,103,670 | 81.88% |

| $500,000 and up | 421,525 | 82.77% |

| Total | 58,113,232 | 39.9% |

There are drawbacks to this idea, however. First, Roth-style retirement accounts will become more attractive to higher earners, which could shift savings away from traditional accounts. Second, this plan would reduce the tax benefit of traditional retirement accounts for those earning above $80,250 but under $400,000, violating Biden’s tax pledge to not raise taxes on earners below the $400,000 threshold.

This proposal would be paired with additional changes, such as establishing an “auto-IRA” for lower-income Americans. There is an opportunity to reform and simplify America’s complicated retirement savings options short of replacing traditional tax deferral with tax credits. Simplifying the dizzying array of retirement and tax-neutral savings options would be a positive step forward for savers across all income levels.

Taxes make more sense with us in your inbox.

Subscribe to our newsletter for tax insights that cut through the noise—and make sense of it.

Sign Up