Wyoming is, without question, a low taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. state, with the nation’s second-lowest overall tax burdens on residents[1] and highly competitive taxes for many businesses. Residents benefit from the high exportability of state taxes, particularly those on extractive industries. Taxes on oil, gas, coal, and other industries are borne by investors and consumers across the country and even the world. This enables Wyoming to have middle-of-the-pack per capita tax collections (98 percent of the national average) along with some of the lowest burdens (68 percent of the national average) for in-state taxpayers, individuals and businesses alike.[2] But the taxes that Wyoming does impose fall overwhelmingly on businesses, which bear nearly 70 percent of Wyoming’s tax burden—the second-highest share in the country, after North Dakota.

Wyoming offers the lowest average effective tax rates for mature businesses and the seventh-lowest effective rates for new firms, according to an analysis conducted by the Tax Foundation and KPMG LLP.[3] This is good news as Wyoming seeks to diversify its economy: even if businesses bear a disproportionate share of state and local taxes in Wyoming, their tax levels tend to be modest compared to their tax exposure in other states.

The present distribution, however, will not scale. Businesses bear the burden of nearly 70 percent of state and local taxes in Wyoming, compared to about 44 percent nationwide. This can be sustained, if not necessarily equitably, when taxes are low and a significant proportion of those taxes are remitted by natural resource operators with geographically fixed assets. Should taxes increase, however, these ratios would become increasingly untenable. The volatility associated with too singular a reliance on business taxes—even beyond the volatility of energy taxes—is, similarly, a concern. As Wyoming’s economy diversifies, and as policymakers consider the role of the tax code in enabling that diversification, they will need to be cognizant of current tax incidence and its implications for future investment and growth.

Resource extraction looms large in Wyoming’s economy and in its economic and revenue data and can make it difficult to gauge how the state’s tax code affects businesses elsewhere, or how tax burdens on other industries compare to those of peer states. Location Matters, produced jointly by the Tax Foundation and KPMG, sheds light on these matters.

Location Matters compares corporate tax costs in all 50 states across eight model firms: a corporate headquarters, a research and development facility, a technology center, a data center, a shared services center, a distribution center, a capital-intensive manufacturer, and a labor-intensive manufacturer. Each firm is modeled twice, first as a new operation eligible for tax incentives and then as a mature operation not eligible for such incentives. This study explores the sort of industries that are sought after by economic development officials nationwide and are part of a diversified economy, and does not include the extractive industries that currently form such a large part of Wyoming’s tax base.

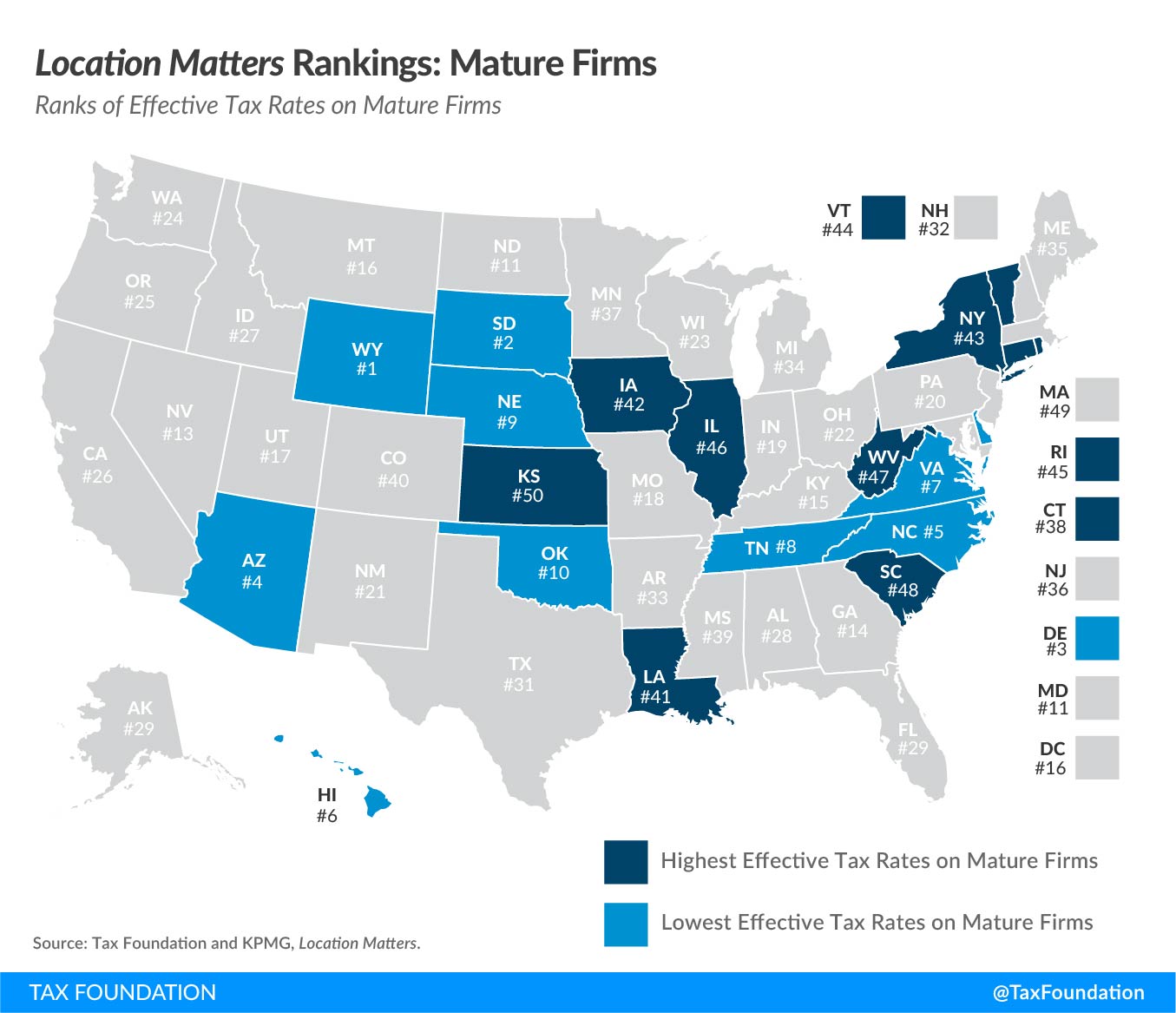

Every mature firm in Wyoming ranks in the top three nationwide for lowest effective tax rates due to the state’s lack of income taxes and modest rates of other taxes. New firms, which are often more incentivized elsewhere, still perform quite well in Wyoming, with six of the eight model firms ranking in the top third of states, and none ranking worse than 21st. Consequently, the state ranks first overall for mature operations and 7th for new operations. All this being equal, it is better and more neutral to offer competitive tax rates to mature firms, as the sort of businesses that states should wish to attract have long time horizons, and are more focused on long-term costs than targeted, time-limited incentives.

| Rank | ||

|---|---|---|

| State | New | Mature |

| Wyoming | 7 | 1 |

| Colorado | 50 | 40 |

| Idaho | 18 | 27 |

| Montana | 17 | 16 |

| Nebraska | 9 | 9 |

| South Dakota | 21 | 2 |

| Utah | 22 | 17 |

| Source: Tax Foundation, Location Matters. | ||

Two neighboring states—Nebraska and South Dakota—rank in the top ten for mature firms, and only Nebraska joins Wyoming in ranking in the top ten for new firms. The absence of income taxes of any sort in Wyoming the share of taxes paid by businesses, but more importantly, it also reduces business tax liability in absolute terms. Wyoming also benefits from uniformity in property taxation, avoiding the imposition of different tax rates on different classes of property. Business machinery and equipment is also subject to property taxes, though, like most states (and all of its neighbors), Wyoming exempts inventory.

Because Wyoming forgoes income taxes, business tax costs for industries outside the natural resource sector are predominantly property and sales taxes. Wyoming’s property taxA property tax is primarily levied on immovable property like land and buildings, as well as on tangible personal property that is movable, like vehicles and equipment. Property taxes are the single largest source of state and local revenue in the U.S. and help fund schools, roads, police, and other services. is generally low, but applies to business equipment in addition to land and buildings, which does not conform as well to the benefit principle and imposes a tax on capital investment. Companies face higher property tax burdens when they increase their investment in machinery and equipment, or when they replace older equipment that has substantially depreciated in value.

Many states offset this tax on investment by offering property tax abatements for new manufacturing firms, but Wyoming does not do so. An abatement itself is not ideal policy, because it is nonneutral—only available to eligible manufacturing firms rather than all businesses—and may abate taxes for some firms to the point of subsidization while other businesses face higher overall tax costs. The better policy is to avoid, or at least limit, the taxation of business tangible property. In failing to do this or offer an abatement, however, Wyoming imposes higher taxes on business property than would be indicated by its millages alone.

Wyoming’s sales taxA sales tax is levied on retail sales of goods and services and, ideally, should apply to all final consumption with few exemptions. Many governments exempt goods like groceries; base broadening, such as including groceries, could keep rates lower. A sales tax should exempt business-to-business transactions which, when taxed, cause tax pyramiding. , moreover, has the sixth broadest base in the country.[4] Unfortunately, while most state sales taxes would benefit from broader bases, Wyoming achieves this by taxing a broad swath of intermediate transactions (business inputs), not by capturing a larger share of final consumption. This results in much of the tax falling directly on—rather than simply being collected and remitted by—businesses. A modest sales tax rate helps mitigate the damage of a poorly designed base, but still penalizes businesses with long supply chains or which are not vertically integrated.

Wyoming is also one of sixteen states to impose a capital stock tax, called the Corporate License Tax, which is levied on businesses based on their net worth, regardless of profitability.[5] This is particularly inequitable for new firms which may take several years to earn a profit. However, Wyoming’s tax has the lowest rate of any of the country’s 16 capital stock taxes and only generated $15.6 million in FY 2020.[6] For some small companies it can be a burden, but in most cases, it is more of a compliance headache.

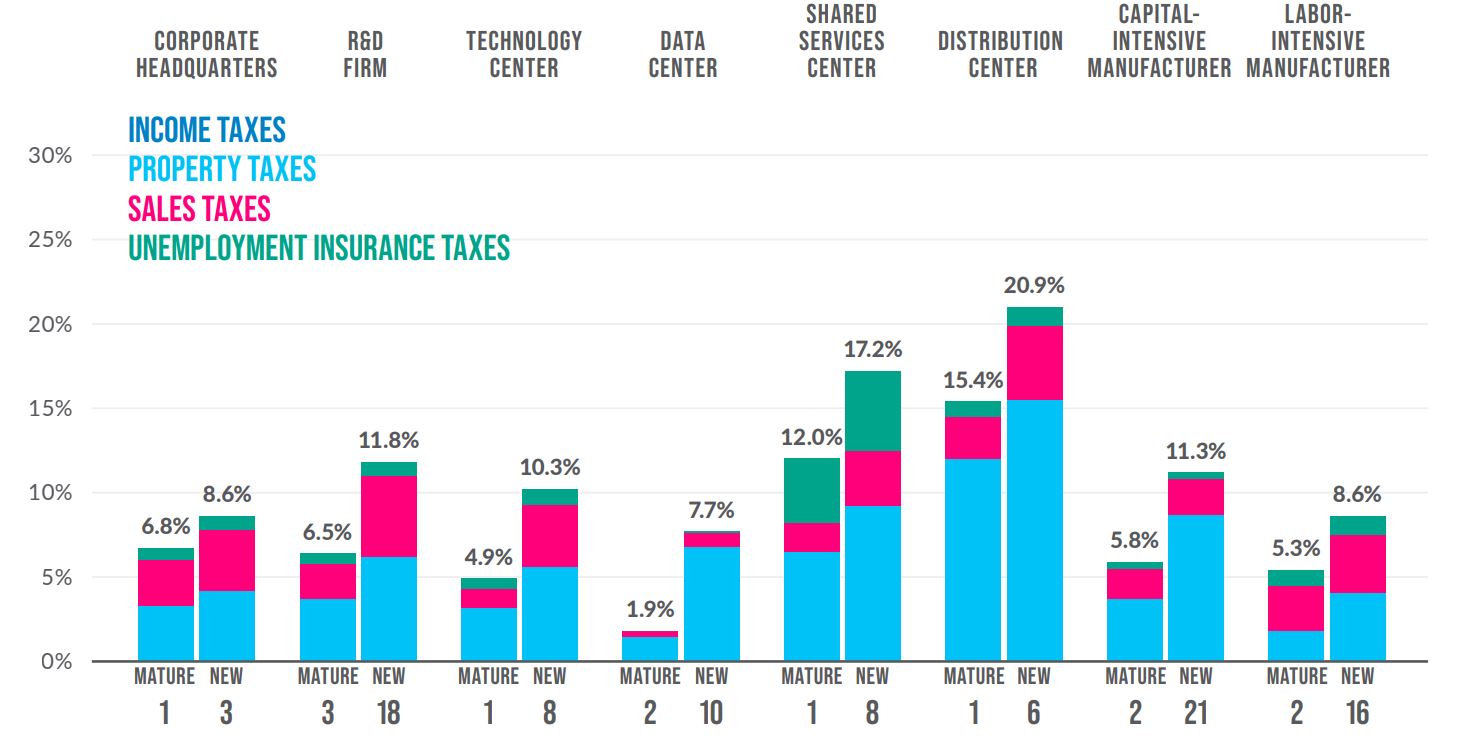

Mature capital-intensive manufacturing operations in Wyoming face the second-lowest effective tax rate nationwide, with an effective tax rate of only 5.8 percent, due to the lack of an income tax and modest sales and property taxes, despite a high unemployment insurance tax burden. A newly established operation, however, experiences roughly average burdens for its type due to high unemployment insurance taxes and the capital stock tax, which is imposed on the business’s assets and net worth rather than its profits. The firm experiences below-average property tax burdens, but is unable to claim the abatements available to peer firms in some other states.

The mature research and development (R&D) facility has the lowest property tax burden in the nation for its firm type, and its overall effective tax rate is just over half the median rate for that firm type nationwide. However, R&D equipment is subject to sales tax in Wyoming—a rarity, and a demonstration of how many business inputs are included in the state’s sales tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. —and the new R&D operation receives no incentives, contributing to an 18th-place rank for new facilities.

| Income & Business Taxes | Property Taxes | Sales Taxes | UI Taxes | Total Effective Tax Rate | Rank | |

|---|---|---|---|---|---|---|

| Corporate Headquarters | ||||||

| Mature | 0.0% | 3.3% | 2.7% | 0.7% | 6.8% | 1 |

| New | 0.0% | 4.2% | 3.6% | 0.8% | 8.6% | 3 |

| Research & Development | ||||||

| Mature | 0.0% | 3.7% | 2.1% | 0.6% | 6.5% | 3 |

| New | 0.0% | 6.2% | 4.8% | 0.8% | 11.5% | 18 |

| Technology Center | ||||||

| Mature | 0.0% | 3.2% | 1.1% | 0.6% | 4.9% | 1 |

| New | 0.0% | 5.6% | 3.7% | 0.9% | 10.3% | 8 |

| Data Center | ||||||

| Mature | 0.0% | 1.5% | 0.3% | 0.0% | 1.9% | 2 |

| New | 0.0% | 6.8% | 0.8% | 0.1% | 7.7% | 10 |

| Shared Services Center | ||||||

| Mature | 0.0% | 6.5% | 1.7% | 3.8% | 12.0% | 1 |

| New | 0.0% | 9.2% | 3.3% | 4.7% | 17.2% | 8 |

| Distribution Center | ||||||

| Mature | 0.0% | 12.0% | 2.5% | 0.9% | 15.4% | 1 |

| New | 0.0% | 15.5% | 4.4% | 1.1% | 20.9% | 6 |

| Capital-Intensive Manufacturer | ||||||

| Mature | 0.0% | 3.7% | 1.8% | 0.4% | 5.8% | 2 |

| New | 0.0% | 8.7% | 2.1% | 0.4% | 11.3% | 21 |

| Labor-Intensive Manufacturer | ||||||

| Mature | 0.0% | 1.8% | 2.7% | 0.9% | 5.3% | 2 |

| New | 0.0% | 4.1% | 3.4% | 1.1% | 8.6% | 16 |

| Source: Tax Foundation, Location Matters. | ||||||

Property and sales taxes, among other forms of taxation, are borne by both individuals and businesses. With property taxes, this largely reflects correct treatment, whereas with the sales tax, it represents a divergence from sound tax policy—a divergence on which Wyoming is particularly notable.

Taxes come in a variety of forms. Some, like taxes on real property, roughly accord with the benefit of taxation, where the value of the property is correlated with the value of the government services the taxpayer receives. A property’s value is inextricably linked to the roads serving it, police and fire protection, and schools, for instance—and the latter is true even for homeowners without school-age children, as evidenced by the higher property values stemming from desirable school districts. The benefit principle of taxation applies to both residential and commercial real property; it makes sense that businesses pay property taxes.

Other taxes, like fuel taxes, are essentially user fees. Taxes on gasoline and diesel help fund road maintenance, again in at least very rough proportion to utilization of transportation infrastructure. Here too it is eminently reasonable that commercial operations pay fuel taxes, since they are contributing—often disproportionately—to road wear-and-tear.

The sales tax, however, is different. It is intended to be a consumption tax, but Wyoming’s tax is sufficiently imbalanced that it is closer to a production tax. Sales taxes are intended to fall on final consumption, and if they are also levied at intermediate stages (on so-called business inputs).

A well-structured sales tax is imposed on all final consumer goods and services while exempting all purchases made by businesses that will be used as inputs in the production process. This is not because businesses deserve special treatment under the tax code, but because applying the sales tax to business inputs results in multiple layers of taxation embedded in the price of goods once they reach final consumers, a process known as “tax pyramiding.” The result is higher and inequitable effective tax rates for different industries and products, which is both nonneutral and nontransparent, hiding actual tax costs from consumers. It also specifically penalizes in-state businesses in a way that a sales tax on final consumption does not.

Because sales taxes tend to be destination-based, they are paid at the consumer’s location, not the producer’s. When a Colorado-based business sells into Utah, they are not disadvantaged by Colorado’s higher rate, because both they and their Wyoming competition will levy Wyoming taxes on Wyoming residents. But when business inputs are taxed, the locus of taxation is the point of production. A Wyoming business that has sales tax imposed at multiple points in its production process has to compete with that Colorado business which faces fewer taxes on inputs, meaning that its margins will be smaller.

According to estimates from the Council on State Taxation and Ernst & Young, over 58 percent of Wyoming’s sales tax falls on intermediate transactions rather than final consumption,[7] which is basically a $558 million tax on business expenses ($976 for each Wyomingite)—more than 28 states generate in corporate income taxes.[8] And while every state inappropriately includes some business inputs in the tax base, Wyoming collects $162 million more from businesses in its sales tax than it would if it had a tax base reflective of national averages, equal to an additional $278 per resident. This is a significant amount: if that extra revenue had been captured from businesses via a corporate income tax instead, then on a per capita basis it would be the country’s eighth largest.

Businesses pay a variety of other taxes in Wyoming as well. Severance and mineral ad valorem taxes are among the most significant, but there are also corporate license taxes, unemployment insurance and workers compensation taxes, and other taxes imposed on businesses. All told, 69.5 percent of Wyoming’s tax collections in FY 2021 came from business taxpayers, based on Tax Foundation analysis.[9]

| Tax Category | Total | Personal | Business |

|---|---|---|---|

| Sales and Use Tax | $972,810,379 | $404,689,118 | $568,121,261 |

| Property (excl. severance) | $843,978,502 | $434,025,354 | $409,953,148 |

| Minerals Ad Valorem | $449,575,104 | — | $449,575,104 |

| Severance Taxes | $443,472,121 | — | $443,472,121 |

| UI & Workers Comp. | $324,765,852 | — | $324,765,852 |

| Vehicle & Fuel Taxes | $268,129,466 | $121,706,069 | $146,423,397 |

| Sin Taxes | $57,212,679 | $57,212,679 | — |

| Lodging Taxes | $25,179,431 | $25,179,431 | — |

| Corporate License Tax | $15,642,543 | — | $15,642,543 |

| Misc. Energy Taxes | $12,706,601 | — | $12,706,601 |

| Total | $3,413,472,678 | $1,042,812,651 | $2,370,660,027 |

| Share | 100% | 30.5% | 69.5% |

| Sources: Wyoming Department of Taxation; U.S. Department of Labor (UI taxes); Wyoming Taxpayers Association; Tax Foundation analysis. | |||

In FY 2021, businesses paid an estimated $2.37 billion in Wyoming taxes, while individuals paid $1.04 billion. If Wyoming’s breakdown matched national averages, businesses would have remitted $1.51 billion to individuals’ $1.90 billion. No one is, of course, suggesting such a switch, particularly given the contribution of extractive industries to these figures, but if tax bases grow in the future, there are constraints on further expansion to business taxpayers.

A similar analysis conducted by COST puts the FY 2020 share at 69.7 percent, the second highest in the nation and well above the national average of 44.3 percent. According to COST, 69.4 percent of state taxes and 70.2 percent of local taxes fall on businesses,[10] with $10,300 in business taxes per employee in the state, the third-highest amount in the nation and well above the $6,500 average nationwide.

Wyoming’s oil, natural gas, and coal industries complicate this analysis, however. These industries are capital- rather than labor-intensive, and even reasonable taxes on these activities can yield very high taxes per employee. This is where a multiple firms analysis, like Location Matters, provides additional insights, since it facilitates an examination of the tax costs of the sort of real-world businesses that Wyoming and other states would like to attract. It demonstrates that, while Wyoming businesses bear a disproportionate share of the tax code (even after accounting for the state’s heavy reliance on the natural resource industry), effective tax rates remain highly competitive for many of the firms Wyoming would like to attract.

Policymakers have rightly prioritized diversifying the state’s economy, and many believe that the state will also need to diversify its revenue streams as taxes on oil, gas, and coal experienced increased volatility, or even suffer long-term decline. In evaluating those options, however, policymakers must gain an appreciation of where tax burdens currently fall. Particularly in a state with exceedingly low population density, taxes that cut into the already razor-thin margins of some industries seeking to operate or expand in Wyoming could prove counterproductive.

Wyoming’s low taxes are highly attractive, but policymakers are still hard at work helping the state achieve broader economic development goals. Changes in the energy sector are a source of genuine consternation, but if lawmakers can maintain a competitive business tax environment as they make revenue and spending decisions in the coming years, the state’s future will be bright.

[1] Erica York and Jared Walczak, “State and Local Tax Burdens, Calendar Year 2019,” Tax Foundation, March 18, 2021, https://taxfoundation.org/state-tax-burden-2019/.

[2] Tax Foundation calculations based on U.S. Census data and the Tax Foundation’s “State and Local Tax Burdens” study.

[3] Jared Walczak et al., Location Matters 2021: The State Tax Costs of Doing Business, Tax Foundation, May 5, 2021, https://www.taxfoundation.org/state-tax-costs-of-doing-business-2021/.

[4] Jared Walczak, “State Sales Tax Breadth and Reliance, Fiscal Year 2020,” Tax Foundation, Feb. 9, 2021, https://taxfoundation.org/sales-tax-base-reliance-2020.

[5] Janelle Cammenga, “Does Your State Levy a Capital Stock Tax?” Tax Foundation, March 24, 2021, https://taxfoundation.org/state-capital-stock-tax-2021/.

[6] Wyoming Taxpayers Association, “Wyoming Tax Summary 2021,” 16, http://wyotax.org/wp-content/uploads/2021/11/WTA-How-Wyoming-Compares-2021.pdf.

[7] Council on State Taxation and Ernst & Young, “Total State and Local Business Taxes: State-by-State Estimates for FY20,” October 2021, 5, https://www.cost.org/globalassets/cost/state-tax-resources-pdf-pages/cost-studies-articles-reports/2108-3843085_50-state-tax-2021-final.pdf.

[8] Sales tax collections data from State of Wyoming Department of Revenue, “2021 Annual Report,” Feb. 7, 2022, https://drive.google.com/file/d/1XZmmnxll5ibqoleu0q-umNBXt-78o9Xw/view. Ratios follow COST/EY calculations.

[9] Fiscal Year 2021 tax collections derived from the Wyoming Department of Revenue’s annual report, augmented by adjusted FY 2020 revenues for select taxes as compiled by the Wyoming Taxpayers Association. Unemployment insurance tax collections are based on state reports to the U.S. Department of Labor.

[10] Council on State Taxation and Ernst & Young, “Total State and Local Business Taxes: State-by-State Estimates for FY20,” 16.

Share this article