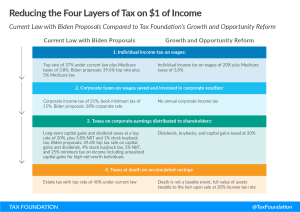

Biden’s New Tax Proposals Are Complicated and Rife with Double Taxation

Tax reform should be about increasing fairness. And the way to get there is by reducing complexity and double taxation, not by doubling down on them.

6 min read

Tax reform should be about increasing fairness. And the way to get there is by reducing complexity and double taxation, not by doubling down on them.

6 min read

The tax treatment of research and development (R&D) expenses is one of the biggest issues facing Congress as the year winds down.

5 min read

We find that the dynamic cost of permanent bonus depreciation rises by about 7 percent under 4 percent inflation, but the economic benefit, measured by the size of the economy, rises by about 25 percent.

4 min read

The phaseout of 100 percent bonus depreciation, scheduled to take place after the end of 2022, will increase the after-tax cost of investment in the U.S. Permanently extending it would increase long-run economic output by 0.4 percent and increase employment by 73,000 FTE jobs.

20 min read

The Senate has begun debate on the so-called Chips bill, which would provide $52 billion in grants and $24 billion in tax credits to supposedly strengthen the production of semiconductors in the U.S.

3 min read

Policymakers should continue to focus on longer term impacts rather than emphasizing the short-term stimulus effects of tax cuts.

3 min read

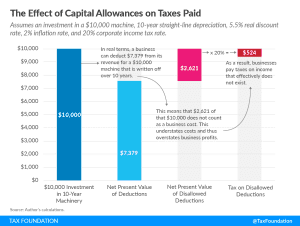

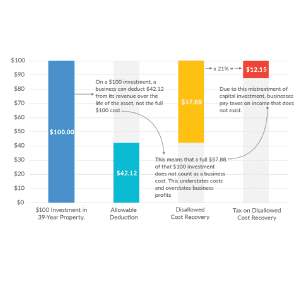

The U.S. tax system is biased against capital investments. Ending these tax penalties would boost economic output, productivity, and employment.

5 min read

Policymakers actively marginalized the manufacturing sector by saddling them with cost recovery rules that prevent them from deducting the full cost of investment in physical plant and equipment. Going forward, policymakers should avoid haphazard fixes, targeted measures, and protectionism.

50 min read

By reducing the tax code’s current barriers to investment and saving and simplifying its complex rules, lawmakers would greatly enhance the ability of Americans to pursue new ideas, create more opportunities, and build financial security for themselves and their families.

40 min read

The lockdowns imposed in response to the COVID-19 pandemic induced an increase in demand for broadband internet, as work from home and other social distancing measures pushed people to spend more time online. As broadband becomes a more important piece of America’s infrastructure, it makes sense to look at tax policy that will help drive more investment and better service.

2 min read

Making 100 percent bonus depreciation permanent avoids the uncertainty associated with the phaseout of a powerful pro-growth policy and would provide a cost-effective boost to long-run economic output, wages, and employment in the United States.

2 min read

Full expensing, if made permanent, would be one of the most cost-effective ways to increase growth as it would produce about 4.5 times more GDP growth per dollar of revenue than making the law’s individual tax provisions permanent, according to our analysis.

3 min read

While tax rates matter to businesses, so too does the measure of income to which those tax rates apply. The corporate income tax is a tax on profits, normally defined as revenue minus costs. However, under the current tax code, businesses are unable to deduct the full cost of certain expenses—their capital investments—meaning the tax code is not neutral and actually increases the cost of investment.

3 min read