The mission of the global program is to promote tax and fiscal policy that leads to higher economic growth and improved quality of life for taxpayers throughout the world.

We produce the annual International Tax Competitiveness Index, a survey of corporate tax rates around the world, and several other comparative reports that allow taxpayers, journalists, and policymakers to compare their tax policies with those in other countries.

Tax Foundation Europe

The mission of Tax Foundation Europe is to promote tax policies that are stable, neutral, simple, and transparent at the Member State and EU levels. We produce research and analysis specifically designed to inform five key debates in European tax policy: the concept of tax fairness, the twin transition of the green and digital economies, government revenue and own resources, competitiveness and productivity, and the future of taxation in the EU.

|

Featured Issues

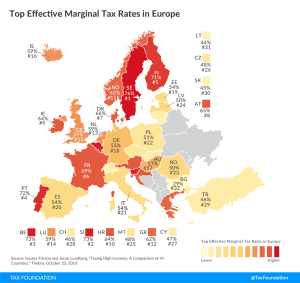

Global Tax Deal | European Tax Maps | Digital Taxation | Carbon Taxes | Cost Recovery