Download Special Report No. 204: The Fiscal Cliff: A Primer

Update: For a description of the taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. deal passed by the Senate on January 1, 2013, see here.

Introduction

On December 31, 2012, a large swath of the federal income tax code is scheduled to expire, an event which has come to be known as the “fiscal cliff.” Among the expiring provisions are the 2001 and 2003 tax cuts enacted under President Bush, a compromise on the estate taxAn estate tax is imposed on the net value of an individual’s taxable estate, after any exclusions or credits, at the time of death. The tax is paid by the estate itself before assets are distributed to heirs., a “patch” in the Alternative Minimum Tax (AMT) reducing its impact, the temporary 2 percent payroll taxA payroll tax is a tax paid on the wages and salaries of employees to finance social insurance programs like Social Security, Medicare, and unemployment insurance. Payroll taxes are social insurance taxes that comprise 24.8 percent of combined federal, state, and local government revenue, the second largest source of that combined tax revenue. holiday, increased business expensing, and the “extenders” package of miscellaneous tax deductions. On January 1, 2013, five taxes enacted as part of the Patient Protection and Affordable Care Act (PPACA)—popularly referred to as Obamacare—also take effect, along with sequester spending reductions of $109 billion due to the failure of the “supercommittee” to reach consensus on budget reductions. Taken together this “fiscal cliff,” or “Taxmageddon,” could potentially reduce economic output by hundreds of billions of dollars.[1]

Congress and the President will have little time to rest after the New Year: in late February, the U.S. government will hit the debt ceiling, exhausting its ability to borrow to finance ongoing spending without an increase by Congress. Finally, the federal government’s continuing resolution appropriating spending expires on March 27, 2013.

The fiscal cliff is the culmination of a decade of “temporary” tax and budget bills that have postponed resolution of key policy differences. Should the tax code be used to heavily promote income distribution or aim instead to raise revenue in the least distortive manner possible? How large should federal spending be? Should PPACA be modified or repealed? Should there be a federal estate tax and if so, at what level? Should the payroll tax be reduced and if so, how should we fund Social Security and Medicare? What should Social Security, Medicare, and Medicaid look like as the population ages?

Table 1: Tax Changes Taking Effect January 1, 2013 |

|

|

Tax Change |

Tax Increase |

|

Expiration of the 2001-03 tax cuts (not including estate) |

$156 billion |

|

Expiration of the payroll tax holiday |

$125 billion |

|

Failure to patch the Alternative Minimum Tax |

$88 billion |

|

Expiration of business expensing |

$48 billion |

|

Expiration of other “tax extenders” |

$40 billion |

|

New PPACA (Obamacare) taxes |

$36 billion |

|

Expiration of the 2009 stimulus |

$11 billion |

|

Estate tax increase |

$10 billion |

|

Total, Tax Increases |

$514 billion |

|

Source: Tax Foundation; Congressional Budget Office; Joint Committee on Taxation; Office of Management & Budget. |

While most observers recognize the importance of dealing with the fiscal cliff before it happens, the divided political landscape can encourage brinksmanship to improve negotiating positions. No political actor wants the fiscal cliff to take permanent effect in full; the next few months will determine whether that happens anyway despite those intentions. Table 1, above, illustrates the revenue impact of the fiscal cliff provisions.

2001 and 2003 Tax Cuts Expiration

In 2001 and 2003, President George W. Bush signed into law significant tax reductions for nearly all taxpayers.[2] These cuts included marginal rate reductions, the introduction of a new 10 percent tax bracket, an expansion of the child tax credit, and a variety of other provisions (see Table 2).

Both the 2001 bill and the 2003 bill were passed using a Senate procedure known as “reconciliation”—a tactic that lowers the threshold for cloture to a simple majority of senators (as opposed to a sixty-vote supermajority.) This procedure, under the Congressional Budget Act, is not allowed for any bill which affects budget deficits beyond a ten-year window, so these tax cuts included a "sunset" provision which caused them to automatically expire at the end of 2010, in order to bypass that requirement. A compromise in late 2010 extended the provisions for two years, to the end of 2012.[3]

Table 2: Major Bush Tax Cut Income Tax Provisions, 2001-2013 |

|||||||||

|

Tax Category |

2000 |

2001 |

2002 |

2003 |

2004-2005 |

2006-2007 |

2008-2009 |

2010-2012 |

2013* |

|

Income Tax Brackets |

— |

10% |

10% |

10% |

— |

||||

|

Capital Gains Tax (max) |

20% |

16.7% |

15% |

23.8% |

|||||

|

Dividend Tax (max) |

39.6% |

39.1% |

38.6% |

15% |

43.4% |

||||

|

PEP & Pease |

Full |

Minus 1/3 |

Minus 2/3 |

Repealed |

Full |

||||

|

Joint Filer = 1.67 x Single |

Joint Filer = 2 x Single |

Joint Filer = 1.67 x Single |

|||||||

|

Child Tax Credit |

$500 |

$600 |

$1,000 |

$500 |

|||||

|

Source: Tax Foundation |

Absent action prior to January 1, 2013, many tax provisions would revert to pre-2001 law:

- The lowest income tax bracket of 10 percent would expire, reverting to 15 percent.

- The top four income tax bracketsA tax bracket is the range of incomes taxed at given rates, which typically differ depending on filing status. In a progressive individual or corporate income tax system, rates rise as income increases. There are seven federal individual income tax brackets; the federal corporate income tax system is flat. would see rate increases. The 25 percent bracket would rise to 28 percent, the 28 percent bracket would rise to 31 percent, the 33 percent bracket would rise to 36 percent, and the top bracket would rise from 35 percent to 39.6 percent. Republicans generally advocate preventing increases in all these tax rates. Democrats generally advocate preventing increases on the lower tax brackets but allowing the 35 percent bracket to increase to 39.6 percent and the 33 percent bracket to increase to 36 percent for taxpayers whose income exceeds $200,000 ($250,000 for couples).

- The tax on long-term capital gains would rise from a maximum of 15 percent to a maximum of 20 percent. Additionally, a 3.8 percent capital gains taxA capital gains tax is levied on the profit made from selling an asset and is often in addition to corporate income taxes, frequently resulting in double taxation. These taxes create a bias against saving, leading to a lower level of national income by encouraging present consumption over investment. on high-income individuals, enacted as part of PPACA (Obamacare), takes effect in 2013. The top capital gains tax rate would thus be 23.8 percent (20 percent plus 3.8 percent). President Obama’s budgets have recommended retaining the 15 percent preferential rate for taxpayers whose income is below $200,000 ($250,000 for couples).

- The tax on qualified dividends would rise from 15 percent to ordinary wage tax rates. Additionally, a 3.8 percent dividend tax on high-income individuals, enacted as part of PPACA (Obamacare), takes effect in 2013. The top dividend tax rate would thus be 43.4 percent (39.6 percent plus 3.8 percent). President Obama’s budgets have recommended retaining the 15 percent preferential rate for taxpayers whose income is below $200,000 ($250,000 for couples).

- Personal exemption phaseouts (PEP) and itemized deductionItemized deductions allow individuals to subtract designated expenses from their taxable income and can be claimed in lieu of the standard deduction. Itemized deductions include those for state and local taxes, charitable contributions, and mortgage interest. An estimated 13.7 percent of filers itemized in 2019, most being high-income taxpayers. disallowance (Pease) for certain high-income individuals would be restored, rescinding the value of some exemptions and deductions. President Obama’s budgets have recommended raising the PEP and Pease thresholds to $200,000 ($250,000 for couples).

- The standard deductionThe standard deduction reduces a taxpayer’s taxable income by a set amount determined by the government. Taxpayers who take the standard deduction cannot also itemize their deductions; it serves as an alternative. for married couples will fall to 167% of single filers, down from 200% of single filers.

- The child tax creditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income rather than the taxpayer’s tax bill directly. will fall from $1,000 to $500 and no longer be refundable.

Figure 1 shows the average annual savings by state from a one-year extension of the Bush tax cuts. Connecticut would be impacted the most; Mississippi, the least.[4]

Figure 1.

Estate Tax Increase

The estate of an individual who dies on December 31, 2012 will pay a federal estate tax (or death tax) of 35 percent on anything above $5.12 million. If the decedent instead passes away the next day, and Congress has not yet acted to change the law, the estate will instead owe a 55 percent tax on anything above $1 million. Even President Obama, no defender of estate tax repeal, considers this level too high: he has urged a compromise proposal of a 45 percent tax on estates over $3.5 million. Republicans generally support complete repeal of the tax.

There are few taxes that are as polarizing as the estate tax. A 2009 poll by the Tax Foundation found that the estate tax is viewed by taxpayers as the most "unfair" of all federal taxes but at the same time the estate tax seems to be a rallying point for those that agitate for redistribution through the tax code.[5] (In 2009, the estate tax raised about $20 billion, from a very small number of estates.) Opponents argue that the estate tax can break down family businesses while creating large compliance costs which are a drag on the economy.

Table 3: Estate Tax Rates & Exemption Levels, 2000-present |

||

|

Estate tax (top rate) |

Estate tax exemption |

|

|

2000 |

55% |

$675,000 |

|

2001 |

55% |

|

|

2002 |

50% |

$1,000,000 |

|

2003 |

49% |

|

|

2004 |

48% |

$1,500,000 |

|

2005 |

47% |

|

|

2006 |

46% |

$2,000,000 |

|

2007 |

45% |

|

|

2008 |

||

|

2009 |

$3,500,000 |

|

|

2010 |

Repealed |

Repealed |

|

2010-2012 |

35% |

$5,120,000 |

|

2013* |

55% |

$1,000,000 |

|

*Absent further congressional action. |

||

|

Source: Internal Revenue Service |

Despite this seeming rift, there is a large and growing body of research by economists that generally lean left-of-center pointing toward repeal of the estate tax.[6] Nobel laureate economist Joseph Stiglitz, who served as chairman on Bill Clinton's Council of Economic Advisors, authored a paper which argued that the estate tax actually increases inequality by reducing savings and driving up returns on capital (which largely benefit wealthy holders of capital).[7] Economist Larry Summers, former Treasury Secretary under President Clinton, co-authored a paper in 1981 that showed that the estate tax has severe impacts on the accumulation of privately held capital. Using Summers' methodology, a July 2012 study by the Joint Economic Committee Republicans showed that since its inception, the estate tax has reduced the capital stock by approximately $1.1 trillion.[8]

The estate tax also encourages firms to structure as corporations instead of as family businesses, because corporations do not pay estate taxes when the person at the helm changes. Family businesses, however, can be subject to rates of over half the value of the estate when a deceased owner transfers the business to their heirs. This observation should be disconcerting to left-leaning voters, who recognize that smaller family businesses have ties to their communities. It should also concern right-leaning voters, who should see this as a distortion of the market process.

Perhaps the worst aspect of the estate tax is how uneven its impact is in practice. By utilizing careful estate planning, many wealthy taxpayers are able to shield much of their income from taxation upon their death. The people that tend to get hit the hardest are those that die unexpectedly, or, like farmers, have their assets tied up in illiquid holdings.[9] The estate planning industry has grown in size over the years as estate law becomes more complex. Three studies have even found that the compliance costs associated with the collection of the estate tax are actually higher than the amount of revenue the tax brings in.[10] Almost the entire estate planning industry can be thought of as economic waste, because it would not exist without the estate tax, and the high-skilled labor and capital utilized in that industry would be applied to other, more productive economic endeavors if the estate tax were repealed.

2011 and 2012 marked the first time in a decade that the estate tax rate and exemption level have been the same for more than one year. For 2010, the president and Congress (unintentionally) allowed the estate tax to expire completely, an outcome unexpected by most observers. While a repeat in 2013 may be desirable, exactly what happens remains to be seen.

Alternative Minimum Tax (AMT) Patch

Congress enacted the AMT in 1969 following testimony by the Secretary of the Treasury that 155 people with adjusted gross incomeFor individuals, gross income is the total of all income received from any source before taxes or deductions. It includes wages, salaries, tips, interest, dividends, capital gains, rental income, alimony, pensions, and other forms of income. For businesses, gross income (or gross profit) is the sum of total receipts or sales minus the cost of goods sold (COGS)—the direct costs of producing goods above $200,000 had paid zero federal income tax on their 1967 tax returns. (In inflation-adjusted terms, those 1967 incomes would be over $1.2 million in today’s dollars.) This tax avoidance by a few high-income taxpayers (primarily by investing in tax-exempt municipal and state bonds) was widely perceived as unfair. Rather than directly addressing the problem by eliminating the deductions and credits in the tax code that were leading to the tax avoidance, Congress laid an additional layer of complexity over the regular income tax in the form of the AMT.

Under the current system, taxpayers who file using the 1040 form at tax time fill out a special worksheet to determine if they pay the AMT. In addition to the worksheet, certain deductions serve as red flags that might signal suspicious tax avoidance activities and these automatically throw taxpayers into the AMT. Some, but not all, deductions and credits are denied under the AMT code. Essentially, taxpayers calculate their tax liability under both the regular income tax and the AMT and then pay the higher of the two amounts. About five million taxpayers currently pay the AMT.

Two factors are causing the current AMT crisis, potentially extending the AMT to twenty million more taxpayers. First, unlike the regular income tax, the AMT’s parameters are not indexed for inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spendin. That means that over time, economic growth and inflation cause a steady increase in the number of taxpayers drawn into the AMT—commonly known as “bracket creepBracket creep occurs when inflation, or real income growth, pushes taxpayers into higher income tax brackets. Bracket creep results in an increase in income taxes without an increase in real income. Many tax provisions—both at the federal and state levels—are adjusted for inflation. Over time, bracket creep can increase how much income tax people owe as their income grows, either due to inflat.” As nominal incomes rise along with inflation, the AMT’s standard deduction shrinks in relative terms, affecting more middle-income taxpayers. Second, the 2001 and 2003 income tax cuts threatened to sharply increase AMT liability as many upper-income people (roughly those with between $150,000 and $1 million in income) would have a larger liability under the AMT than under the regular income tax. Since taxpayers must pay the greater of the two, the AMT in essence took back some of their tax cut. According to Congressional Budget Office estimates, taxpayers earning between $50,000 and $200,000 will be hardest hit by the AMT in coming years, especially those in high cost of living areas with high per-capita incomes and high state and local taxes.

To prevent this from occurring, Congress has routinely “patched” the AMT. The AMT patch raises the AMT exemption level, increasing the amount a taxpayer must earn before being subject to the AMT. The most recent AMT patch, for example, occurred in 2010 to cover tax year 2011. Congress set an exemption level of $48,450 ($74,450 for couples) for calendar year 2011, preventing what would have automatically occurred otherwise: the exemption level for 2011 would have fallen to just $33,750 ($45,000 for couples). The AMT patch expired on December 31, 2011 and it will need to be patched again prior to taxpayers filing their 2012 tax forms (due mid-April 2013).

Congress has been resistant to making permanent the current practice of inflation-adjusting the AMT exemption level because congressional budget rules would score it is as a large tax reduction, running afoul of budget-neutrality requirements. And so throughout the past decade, during the Bush years and continuing in the Obama years, Congress passes and the president signs a one- or two-year patch to prevent AMT from hitting twenty million more taxpayers.

One important note is the Buffett Rule, a proposal by President Obama to require all individuals with at least $1 million in income to pay no less than 30 percent of that income in federal income tax. The proposed Buffett Rule would replace the AMT, possibly with something similar, but the legislative language remains unspecified. In any case, the stated need for the Buffett Rule highlights the failure of the AMT to achieve its purpose: ensuring that high-income taxpayers could not use available deductions and credits to wipe out their tax liability.

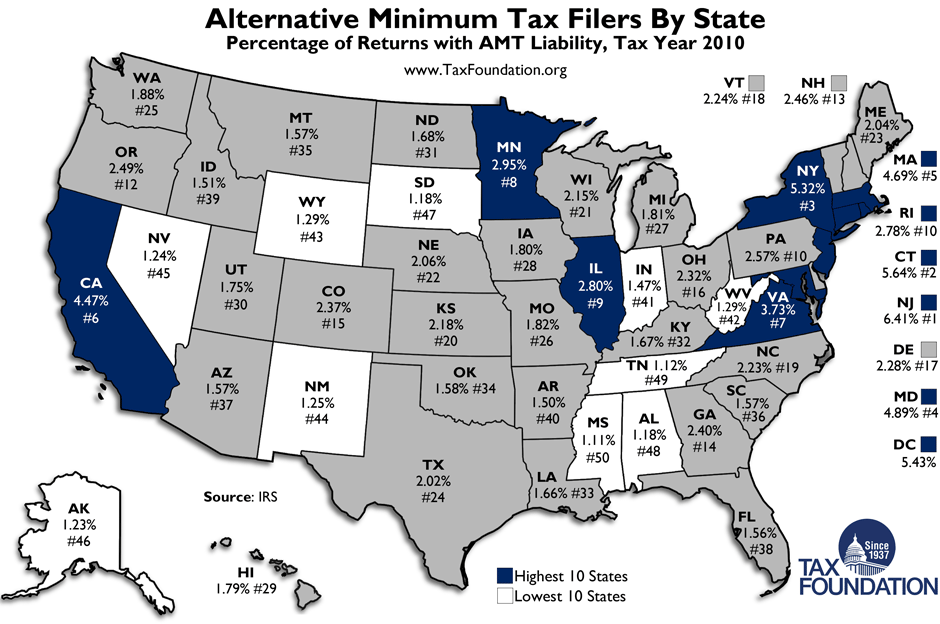

Figure 2.

Payroll Tax Holiday

The 2009 stimulus law included the Making Work Pay tax credit, a cornerstone of President Obama’s 2008 campaign tax proposals.[11] The credit was equivalent to 6.2 percent of earnings up to $400 ($800 for a married couple), with the credit reduced for those earning more than $75,000 ($150,000 for a married couple) and eliminated entirely for those earning more than $95,000 ($190,000 for a married couple). Put succinctly, the credit refunded the Social Security tax paid on income up to $6,500 for all but high-income earners. The credit was also refundable, meaning that those who earned less than $6,500 could still receive the full credit.

The Making Work Pay credit expired at the end of 2010, and was replaced by a 2 percentage point reduction in the Social Security payroll tax (see Table 4). Before 2010, wage earners and their employers equally split a 15.3 percent payroll tax: 6.2 percent was withheld from employee’s paychecks for Social Security, 1.45 percent was withheld from employee’s paychecks for Medicare, 6.2 percent was paid by employers for Social Security, and 1.45 percent was paid by employers for Medicare. For 2011 and 2012, employees now pay just 4.2 percent, while employers continue to pay 6.2 percent, for a total of 10.4 percent.

This payroll tax holiday is popular and costly, reducing federal revenues by some $10 billion per month. U.S. payroll taxes, which fund some of our largest federal entitlement programs, are among the lowest in the industrialized world, potentially aggravating the long-term solvency of Social Security.[12] Proponents of the holiday argue that short-term stimulus can effectively put cash in the pockets of those most likely to spend it. Opponents find little economic growth from short-run stimulus measures in general and the payroll tax holiday in particular.

Table 4: Payroll Tax Holiday Impact on Payroll Taxes |

|||

|

Payroll Tax Component |

2010 |

2011 and 2012 |

2013 (unless changed)* |

|

Employee Share |

|||

|

Social Security |

6.20% |

4.20% |

6.20% |

|

Medicare |

1.45% |

1.45% |

1.45% |

|

Subtotal, Employee |

7.65% |

5.65% |

7.65% |

|

Employer Share |

|||

|

Social Security |

6.20% |

6.20% |

6.20% |

|

Medicare |

1.45% |

1.45% |

1.45% |

|

Subtotal, Employer |

7.65% |

7.65% |

7.65% |

|

Total Payroll Tax** |

15.30% |

13.30% |

15.30% |

|

Source: Tax Foundation |

Increased Business Expensing

A business may purchase a capital asset immediately but generally may not deduct the entire purchase from its taxes the first year. Instead, the business may take deductions as the asset wears out over time, a process known as depreciationDepreciation is a measurement of the “useful life” of a business asset, such as machinery or a factory, to determine the multiyear period over which the cost of that asset can be deducted from taxable income. Instead of allowing businesses to deduct the cost of investments immediately (i.e., full expensing), depreciation requires deductions to be taken over time, reducing their value and disco. Businesses depreciate assets for both tax and accounting purposes, using two main methods: straight-line (equal amounts each year) and accelerated (larger up-front deductions and smaller deductions in later years).[13]

Congress frequently enacts temporary depreciation allowances in hopes of spurring economic growth via capital investment. For instance, bonus depreciationBonus depreciation allows firms to deduct a larger portion of certain “short-lived” investments in new or improved technology, equipment, or buildings in the first year. Allowing businesses to write off more investments partially alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs. was allowed as part of the 2001 and 2003 tax cut laws and the 2008 Bush stimulus. The 2009 stimulus allowed firms to immediately deduct 50 percent of qualifying property expenses, and the 2010 tax compromise increased that deduction to full expensing, a 100 percent immediate deduction, in 2011 and 50 percent expensing in 2012. (Such congressional actions help put tax law out of sync with accounting statements, leading to mismatches between corporate tax reporting and corporate accounting reporting.)

Bonus depreciation and expensing on a temporary basis are sometimes referred to as tax cuts, but in reality they are more like tax shifts. Instead of businesses taking their deductions in future years, they take them now. This feature—a long-term revenue loss of nearly zero—is why it is a standard feature of stimulus packages that are trying to avoid the ten-year pay-go requirement for revenue reductions. The idea behind bonus depreciation is to encourage capital purchases earlier and hopefully encourage the use of that capital to increase production. This is what happened in 2003, leading to an immediate rebound in investment and GDP. But because it was temporary, it mainly borrowed investment from future years when it expired. Full expensingFull expensing allows businesses to immediately deduct the full cost of certain investments in new or improved technology, equipment, or buildings. It alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs. on a permanent basis would permanently shift investment forward, leading to permanently increased production and income.[14]

Tax “Extenders”

The “tax extenders” are a grab bag of several dozen tax provisions that regularly expire and must be renewed by Congress. Most are politically popular but have the purpose of using the tax code for social purposes rather than to raise revenue.[15] These include tax benefits for alternative fuels, energy efficiency, tuition expenses, veterans hiring preferences, and even a special write-off period for building NASCAR racing tracks.[16] However, some of these provisions help to mitigate the tax code’s bias against saving and investment.[17] Notably, the research and development credit is used widely by businesses to invest in areas thought to have spillover benefits for society. The active financing provision gives equal treatment to financial services and non-financial services companies in regards to foreign income, allowing them to defer taxes on actively invested foreign income.[18]

Congress routinely postpones action on these tax preferences until the last minute, despite (or because of) intense interest in their renewal by beneficiary interests. While most will likely be renewed without review, some (including the NASCAR write-off) may fall by the wayside.

Taxes in PPACA (Obamacare)

The Patient Protection and Affordable Care Act (PPACA), commonly referred to as Obamacare, included a number of provisions that take effect over a six-year period.[19] Tax provisions already in effect include a 10 percent excise tax on tanning bed services (effective July 1, 2010) and a higher tax on HSA and Archer MSA distributions not used for qualified medical expenses.

New PPACA taxes take effect on January 1, 2013 (see Table 5):

- Payroll tax increase for high-income earners. For those earning more than $200,000 ($250,000 for married filers), the employee payroll tax for Medicare rises by 0.9 percentage points, from 1.45 percent to 2.35 percent (the total Medicare payroll tax, including the employer share, will rise from 2.9 percent to 3.8 percent). Additionally, those same high-income taxpayers with investment income must pay the 3.8 percent Medicare tax on their dividend and capital gain income. This change is estimated to raise $317 billion over ten years.

- New excise taxAn excise tax is a tax imposed on a specific good or activity. Excise taxes are commonly levied on cigarettes, alcoholic beverages, soda, gasoline, insurance premiums, amusement activities, and betting, and typically make up a relatively small and volatile portion of state and local and, to a lesser extent, federal tax collections. on medical devices. Producers of medical devices face a tax equivalent to 2.3 percent of their gross sales. This tax is estimated to raise $29 billion over ten years.

- New Limitations on Flexible Spending Accounts (FSAs). FSAs will face an annual cap of $2,500 for medical expense reimbursements, as opposed to the present unlimited level. This change is estimated to raise $24 billion over ten years.

- Increased threshold for deducting medical expenses. Presently, taxpayers who itemize deductions may deduct their medical expenses exceeding 7.5 percent of their income. Effective January 1, 2013, that threshold rises to 10 percent. This change is estimated to raise $19 billion over ten years.

- Reduced tax deductions for health insurance company payments to executives and directors. This change is estimated to raise $800 million over ten years.

Table 5: PPACA (“Obamacare”) Taxes ($ billions) |

||||

|

Provision (Effective Date) |

2013 |

2022 |

Total, 2013-17 |

Total, 2013-22 |

|

3.8% payroll tax increase for high-income earners (2013) |

20 |

46 |

115 |

318 |

|

40% “Cadillac” tax on expensive health plans (2018) |

– |

32 |

– |

111 |

|

Annual fee on health insurers (2014) |

– |

15 |

36 |

102 |

|

Annual fee on drug manufacturers (2011) |

8 |

3 |

20 |

34 |

|

2.3% excise tax on medical devices (2013) |

2 |

4 |

13 |

29 |

|

Limit FSA reimbursements to $2,500 (2013) |

1 |

3 |

10 |

24 |

|

Raise 7.5% AGI floor on itemized medical deduction to 10% (2013) |

* |

3 |

5 |

19 |

|

Exclude unprocessed fuels from cellulosic biofuel producer credit (2010) |

5 |

– |

16 |

16 |

|

Increase tax to 20% on HSAs and Archer MSAs not used for qualified medical purposes (2011) |

* |

* |

1 |

5 |

|

Penalty for certain tax underpayments (2009) |

* |

1 |

2 |

5 |

|

Exclude over-the-counter purchases from FSAs, Archer MSAs and HSAs (2011) |

* |

* |

2 |

4 |

|

Eliminate deduction for Medicare Part D expenses (2013) |

* |

* |

2 |

3 |

|

10% indoor tanning excise tax |

* |

* |

1 |

2 |

|

Deduction limitation on health insurer pay to executives (2013) |

* |

* |

1 |

1 |

|

Require information reporting on payments to vendors (2012) |

Repealed |

|||

|

Increase corporate tax withholding for third quarter of 2014 |

Repealed |

|||

|

Total |

36 |

109 |

222 |

675 |

|

Source: Joint Committee on Taxation. |

Automatic Sequester Budget Reductions

If current policy were to be extended, the federal government over the next ten years will raise $36.48 trillion in revenue and spend $46.46 trillion, for a gap of $9.98 trillion (see Table 6).[20]

Table 6: Current Policy Budget Projections, FY 2012-22 |

|||||||||||||

|

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

Total |

Total 2013-22 |

|

|

Revenues |

2.44 |

2.58 |

2.83 |

3.11 |

3.36 |

3.60 |

3.81 |

4.00 |

4.20 |

4.40 |

4.61 |

15.48 |

36.48 |

|

Outlays |

3.56 |

3.62 |

3.75 |

3.92 |

4.20 |

4.43 |

4.68 |

5.00 |

5.30 |

5.60 |

5.97 |

19.91 |

46.46 |

|

Deficit |

-1.13 |

-1.04 |

-0.92 |

-0.81 |

-0.83 |

-0.83 |

-0.87 |

-1.00 |

-1.10 |

-1.20 |

-1.36 |

-4.43 |

-9.98 |

|

Debt Held By Public |

11.32 |

12.46 |

13.48 |

14.39 |

15.32 |

16.26 |

17.22 |

18.30 |

19.48 |

20.75 |

22.18 |

– |

– |

|

Revenues (%GDP) |

15.7 |

16.3 |

17.2 |

17.8 |

18.1 |

18.3 |

18.3 |

18.4 |

18.5 |

18.5 |

18.6 |

17.6 |

18.1 |

|

Outlays (%GDP) |

22.9 |

22.8 |

22.9 |

22.5 |

22.6 |

22.5 |

22.5 |

23.0 |

23.3 |

23.6 |

24.1 |

22.6 |

23.0 |

|

Deficit (%GDP) |

-7.3 |

-6.5 |

-5.6 |

-4.6 |

-4.5 |

-4.2 |

-4.2 |

-4.6 |

-4.8 |

-5.1 |

-5.5 |

-5.0 |

-4.9 |

|

Debt Held By Public (%GDP) |

73 |

79 |

82 |

83 |

83 |

83 |

83 |

84 |

86 |

88 |

90 |

– |

– |

|

Source: Congressional Budget Office. |

The Bowles-Simpson Commission, assembled to recommend a path to long-term fiscal balance, recommended $4 trillion of deficit reduction over that ten-year period, to reduce the federal budget deficit to below 3 percent of the economy.[21]

Table 7: Bowles-Simpson Commission Proposal, FY 2010-20 |

||||||||||

|

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

Total 2011-20 |

|

|

Revenues ($trillions) |

2.72 |

3.05 |

3.39 |

3.60 |

3.84 |

4.08 |

4.30 |

4.54 |

4.77 |

36.81 |

|

Outlays ($trillions) |

3.67 |

3.69 |

3.84 |

4.02 |

4.28 |

4.45 |

4.60 |

4.84 |

5.05 |

42.14 |

|

Deficit ($trillions) |

-0.94 |

-0.65 |

-0.46 |

-0.42 |

-0.43 |

-0.37 |

-0.29 |

-0.30 |

-0.28 |

-5.34 |

|

Debt Held By Public ($trillions) |

11.20 |

11.95 |

12.50 |

13.00 |

13.52 |

13.99 |

14.38 |

14.78 |

15.16 |

– |

|

Revenues (%GDP) |

17.3 |

18.2 |

19.1 |

19.3 |

19.7 |

20.0 |

20.2 |

20.5 |

20.6 |

19.3 |

|

Outlays (%GDP) |

23.3 |

22.1 |

21.6 |

21.6 |

21.9 |

21.8 |

21.6 |

21.8 |

21.8 |

22.1 |

|

Deficit (%GDP) |

-6.0 |

-3.9 |

-2.6 |

-2.3 |

-2.2 |

-1.8 |

-1.4 |

-1.3 |

-1.2 |

-2.8 |

|

Debt Held By Public (%GDP) |

71 |

72 |

70 |

70 |

69 |

69 |

68 |

67 |

66 |

– |

The two most-cited plans for future years are President Obama’s budget plan (Table 8), which includes the expiration of the Bush tax cuts for high-income earners, the new health care taxes, and other tax increases on high-income earners; and the House Republican plan (Table 9), authored by House Budget Committee Chair and 2012 Republican vice-presidential nominee Paul Ryan, and which includes significant entitlement program reform.

Table 8: President Obama’s Budget Projections, FY 2012-22 |

||||||||||||

|

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

Total 2013-22 |

|

|

Revenues ($trillions) |

2.47 |

2.90 |

3.22 |

3.45 |

3.68 |

3.92 |

4.15 |

4.38 |

4.60 |

4.86 |

5.12 |

40.27 |

|

Outlays ($trillions) |

3.80 |

3.80 |

3.89 |

4.06 |

4.33 |

4.53 |

4.73 |

5.00 |

5.26 |

5.54 |

5.82 |

46.96 |

|

Deficit ($trillions) |

-1.33 |

-0.90 |

-0.67 |

-0.61 |

-0.65 |

-0.61 |

-0.58 |

-0.63 |

-0.66 |

-0.68 |

-0.70 |

-6.68 |

|

Debt Held By Public ($trillions) |

11.58 |

12.64 |

13.45 |

14.20 |

14.98 |

15.71 |

16.40 |

17.14 |

17.90 |

18.68 |

19.49 |

– |

|

Revenues (%GDP) |

15.8 |

17.8 |

18.7 |

19.0 |

19.1 |

19.2 |

19.4 |

19.5 |

19.7 |

19.9 |

20.1 |

19.2 |

|

Outlays (%GDP) |

24.3 |

23.3 |

22.6 |

22.3 |

22.5 |

22.2 |

22.0 |

22.3 |

22.5 |

22.7 |

22.8 |

22.5 |

|

Deficit (%GDP) |

-8.5 |

-5.5 |

-3.9 |

-3.4 |

-3.4 |

-3.0 |

-2.7 |

-2.8 |

-2.8 |

-2.8 |

-2.8 |

-3.3 |

|

Debt Held By Public (%GDP) |

74 |

77 |

78 |

78 |

78 |

77 |

77 |

76 |

77 |

77 |

77 |

– |

| Source: White House Office of Management & Budget, The President’s Budget for Fiscal Year 2013 (Feb. 13, 2012) (Summary Tables), http://www.whitehouse.gov/sites/default/files/omb/budget/fy2013/assets/tables.pdf. |

Table 9: House Republican “Ryan Plan” Budget Projections, FY 2012-22 |

||||||||||||

|

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

Total 2013-22 |

|

|

Revenues ($trillions) |

2.44 |

2.73 |

2.98 |

3.23 |

3.45 |

3.64 |

3.81 |

3.99 |

4.18 |

4.39 |

4.60 |

37.01 |

|

Outlays ($trillions) |

3.62 |

3.53 |

3.48 |

3.54 |

3.69 |

3.82 |

3.98 |

4.20 |

4.41 |

4.61 |

4.89 |

40.14 |

|

Deficit ($trillions) |

-1.18 |

-0.80 |

-0.50 |

-0.30 |

-0.24 |

-0.18 |

-0.17 |

-0.21 |

-0.23 |

-0.22 |

-0.29 |

-3.13 |

|

Debt Held By Public ($trillions) |

11.36 |

12.26 |

12.86 |

13.26 |

13.60 |

13.87 |

14.13 |

14.42 |

14.72 |

15.00 |

15.36 |

– |

|

Revenues (%GDP) |

15.8 |

17.2 |

18.0 |

18.3 |

18.4 |

18.5 |

18.4 |

18.4 |

18.5 |

18.6 |

18.7 |

18.3 |

|

Outlays (%GDP) |

23.4 |

22.2 |

21.0 |

20.1 |

19.7 |

19.4 |

19.3 |

19.4 |

19.5 |

19.5 |

19.8 |

20.0 |

|

Deficit (%GDP) |

-7.6 |

-5.0 |

-3.0 |

-1.7 |

-1.3 |

-0.9 |

-0.8 |

-1.0 |

-1.0 |

-0.9 |

-1.2 |

-1.7 |

|

Debt Held By Public (%GDP) |

73 |

77 |

78 |

75 |

73 |

70 |

68 |

67 |

65 |

64 |

62 |

– |

| Source: House Budget Committee, The Path to Prosperity: A Blueprint for American Renewal (Mar. 20, 2012), http://budget.house.gov/uploadedfiles/pathtoprosperity2013.pdf. |

In the first half of 2011, debt ceiling negotiations between President Obama and congressional leaders failed to reach agreement on a $4 trillion deficit reduction plan. President Obama sought a debt ceiling increase of $2.4 trillion, which would have carried the federal government past the 2012 election into February 2013. Republicans insisted that the long-term deficit be reduced by at least the amount of the debt ceiling increase. During negotiations, it became clear that Republicans rejected large revenue increases and demanded major entitlement program changes for a minor revenue increase; Democrats rejected major changes to entitlement programs and insisted on a large revenue increase in return for minor entitlement changes. Consequently, a law enacted in August 2011 implemented $900 billion of initial budget reductions but set up a joint select committee to develop a further $1.5 trillion in deficit reduction for congressional consideration.[22] In November 2011, this “supercommittee” announced that it would not be able to produce a recommendation.

The law provided a “stick” if Congress failed to implement the required deficit reduction: $1.2 trillion in forced automatic cuts (sequestration) would take place over the ten years, divided equally between defense and non-defense discretionary programs. The FY 2013 portion of the across-the-board reductions total $109.33 billion, again divided equally between defense ($54.67 billion) and non-defense ($54.67 billion).[23] Thus, defense spending for FY 2013 would be reduced 9.4 percent from the planned spending level, and non-exempt non-defense spending would be reduced 8.2 percent from the planned spending level. However, it is important to recognize that government spending still increases each year over the next ten years: the “cuts” are to spending increases.

As the sequester cuts were designed to be so horrible as to motivate action by the supercommittee and by Congress, few in Washington support their full implementation. Republicans are eager to avoid the defense cuts in particular; Democrats are eager to avoid the non-defense cuts. If the sequester is repealed entirely, the $1.2 trillion in deficit reduction goes with it. If the sequester is replaced by another package of deficit reduction strategies, some partisan agreement will be necessary. As commentator Ezra Klein explained in September, “The political obstacles are the same as during the supercommittee negotiations: Republicans don’t want to raise taxes to generate revenue, while Democrats are reluctant to make dramatic changes to entitlement programs to achieve savings.”[24]

Debt Ceiling

On Wednesday, August 3, 2011, the U.S. government borrowed $238.3 billion, a one-day record.

The action was not unexpected: President Obama had signed the Budget Control Act the day before, increasing the debt ceiling over time from $14.294 trillion to $16.394 trillion. The large immediate sum was needed due to accumulated obligations; since May, the U.S. Treasury had used “extraordinary measures”—delayed payments and shifted internal accounts—to avoid exceeding the debt ceiling.[25]

Due to the extraordinary level of federal borrowing (an average of $2.7 billion per day), federal debt will again approach the debt ceiling near the end of 2012, although similar “extraordinary measures” should postpone default until February 2013.[26] Many congressional Republicans were resistant to raising the debt ceiling at all, while many congressional Democrats favored increasing the debt ceiling without any future deficit reduction. As during the summer of 2011, these perspectives will make a debt ceiling agreement very difficult.

Continuing Resolution

The U.S. government last passed a federal budget in April 2009. Since then, spending authorizations and appropriations have been on an ad hoc basis, through continuing resolutions. These measures take the approved FY 2008 budget and increase or reduce amounts, usually based on inflation. For example, the latest continuing resolution adopted in September 2012 sets total appropriated (non-mandatory) spending at $1.153 trillion for FY 2013, an $8 billion increase.[27] This continuing resolution runs from October 1, 2012 through March 27, 2013.

Eventually, Congress will again need to debate and enact a budget that re-evaluates the priorities of various programs. Either a new budget or another continuing resolution must occur before the end of March 2013.

Conclusion

The sheer size of the fiscal cliff in scope, importance, and dollars signifies the uncertainty faced by American taxpayers. With so much of the tax and budget system on short-term lease, and with the proposed permanent fixes so widely varying, speedy economic growth becomes untenable. While past practice suggests Washington will once again duct tape together another short-term extension and put off the hard choices, anything can happen.

[1] See, e.g., Congressional Budget Office, Economic Effects of Reducing the Fiscal Restraint That Is Scheduled to Occur in 2013 (May 2012), http://www.cbo.gov/sites/default/files/cbofiles/attachments/FiscalRestraint_0.pdf (estimating economic effect of fiscal cliff provisions to be a 4 percentage point reduction in GDP); Fidelity Viewpoints, Fiscal cliff ahead: What it may mean (Jun. 28, 2012), https://www.fidelity.com/viewpoints/fiscal-cliff (estimating economic effect of fiscal cliff provisions to be 4 to 5 percentage point reduction in GDP);

Douglas Holtz-Eakin & Ike Brannon, The Economic Effects of the Fiscal Cliff, American Action Forum (Jul. 2012), http://americanactionforum.org/sites/default/files/Fiscal%20Cliff.pdf (“[W]hen considering economic multipliers, the contraction could approach ten percent, which would amount to the biggest year-over-year decline since 1932.”).

[2] The 2001 law was the Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA), Pub. L. 107-16, and the 2003 law was the Jobs and Growth Tax Relief Reconciliation Act of 2003 (JGTRRA), Pub. L. 108-27.

[3] The 2010 law was the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010, Pub. L. 111-312.

[4] See William McBride & Ed Gerrish, How the States Would Be Affected by Extension of the Bush Tax Cuts and Other Provisions, Tax Foundation Fiscal Fact No. 325 (Aug. 1, 2012), https://taxfoundation.org/article/how-states-would-be-affected-extension-bush-tax-cuts-and-other-provisions; Nick Kasprak, Monday Map: Average Tax Savings from One Year Extension of Bush Tax Cuts, Tax Foundation Tax Policy Blog (Aug. 23, 2012), https://taxfoundation.org/blog/monday-map-average-tax-savings-one-year-extension-bush-tax-cuts.

[5] Scott A. Hodge, Americans Say Estate Tax Unfair, Should Be Repealed, Tax Foundation Tax Policy Blog, Aug. 1, 2005, https://taxfoundation.org/blog/americans-say-estate-tax-unfair-should-be-repealed.

[6] Scott Drenkard, Why Progressives Should Want to End the Estate Tax, Too, Tax Foundation Article, https://taxfoundation.org/article/why-progressives-should-want-end-estate-tax-too.

[7] Tax Foundation, The Economic Effects of the Estate Tax (Testimony of David S. Logan before the Pennsylvania House Finance Committee), Oct. 17, 2011, https://taxfoundation.org/article/economic-effects-estate-tax-testimony-david-s-logan-pennsylvania-house-finance-committee.

[8] Joint Economic Committee Republicans, Cost and Consequences of the Federal Estate Tax: An Update (July 25, 2012), http://www.jec.senate.gov/republicans/public/?a=Files.Serve&File_id=bc9424c1-8897-4dbd-b14c-a17c9c5380a3.

[9] David Block & Scott Drenkard, The Estate Tax: Even Worse Than Republicans Say, Tax Foundation Fiscal Fact No. 326 (Sept. 4, 2012), https://taxfoundation.org/article/estate-tax-even-worse-republicans-say.

[10] Id.

[11] Mark Robyn, The Making Work Pay Credit: Who Will Benefit?, Tax Foundation Tax Policy Blog, Feb. 25, 2009, https://taxfoundation.org/blog/making-work-pay-credit-who-will-benefit.

[12] William McBride, Global Evidence on Taxes and Economic Growth: Payroll Taxes Have No Effect, Tax Foundation Fiscal Fact No. 290 (Feb. 8, 2012), https://taxfoundation.org/article/global-evidence-taxes-and-economic-growth-payroll-taxes-have-no-effect.

[13] David S. Logan, Three Differences Between Tax and Book Accounting that Legislators Need to Know, Tax Foundation Fiscal Fact No. 277 (July 27, 2011), https://taxfoundation.org/article/three-differences-between-tax-and-book-accounting-legislators-need-know.

[14] Stephen J. Entin, Administration Advocates Expensing: One Big Plus (Among the Minuses), IRET Congressional Advisory No. 268 (Sept. 14, 2010), http://iret.org/pub/ADVS-268.PDF.

[15] Scott A. Hodge, Pork Barrel Tax Provisions in the Extenders Bill, Tax Foundation Tax Policy Blog, May 27, 2010, https://taxfoundation.org/blog/pork-barrel-tax-provisions-extenders-bill.

[16] Kim Dixon, Senate panel passes tax bill in rare bipartisan show, Reuters, Aug. 2, 2012, http://www.reuters.com/article/2012/08/02/us-usa-congress-tax-idUSBRE8711MX20120802.

[17] William McBride, Romney, Obama, & Simpson-Bowles: How Do the Tax Reform Plans Stack Up?, Tax Foundation Fiscal Fact No. 327 (Sept. 6, 2012), https://taxfoundation.org/article/romney-obama-simpson-bowles-how-do-tax-reform-plans-stack.

[18] Stephen J. Entin, Extenders Bill (H.R. 4213) Up for Action in Senate, IRET Congressional Advisory No. 266 (June 9, 2010), http://iret.org/pub/ADVS-266.PDF.

[19] Joint Committee on Taxation, Revenue Estimates for the Patient Protection and Affordable Care Act, Memorandum from Thomas A. Barthold, June 15, 2012, http://waysandmeans.house.gov/uploadedfiles/jct_june_2012_partial_re-estimate_of_tax_provisions_in_aca.pdf.

[20] Congressional Budget Office, An Update to the Budget and Economic Outlook: Fiscal Years 2012 to 2022 (Aug. 2012), http://cbo.gov/sites/default/files/cbofiles/attachments/43539-08-22-2012-Update_One-Col.pdf.

[21] National Commission on Fiscal Responsibility and Reform, Co-Chairs’ Proposal (Nov. 2010), http://www.fiscalcommission.gov/sites/fiscalcommission.gov/files/documents/CoChair_Draft.pdf.

[22] Budget Control Act of 2011, Pub. L. 112-25.

[23] Office of Management and Budget, OMB Report Pursuant to the Sequestration Transparency Act of 2012 (P.L. 112-155), http://www.washingtonpost.com/blogs/ezra-klein/files/2012/09/Combined_STAReport_Watermark.pdf.

[24] Suzy Khimm, The sequester, explained, Ezra Klein’s Wonkblog, Washington Post, Sept. 14, 2012, http://www.washingtonpost.com/blogs/ezra-klein/wp/2012/09/14/the-sequester-explained/.

[25] Department of the Treasury, Timothy Geithner, Letter to Harry Reid, May 16, 2011, http://www.treasury.gov/connect/blog/Documents/20110516Letter%20to%20Congress.pdf.

[26] Rachelle Younglai, U.S. gov’t poised to hit debt limit before 2013, Reuters, Oct. 31, 2012, http://www.reuters.com/article/2012/10/31/usa-debt-idUSL1E8LV2LU20121031.

[27] Emily Goff, FY 2013 Appropriations Tracker Update: Continuing Resolution Spends Even More, Heritage Foundation Foundry blog, Sept. 28, 2012, http://blog.heritage.org/2012/09/28/fy-2013-appropriations-tracker-update-continuing-resolution-spends-even-more/.

Share this article