Co-Chair Roblan, Co-Chair Smith Warner, Co-Vice Chair Knopp, Co-Vice Chair Smith, and Members of the Committee:

My name is Garrett Watson, and I’m an economist and the Special Projects Manager at the TaxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. Foundation, the nation’s leading nonpartisan, nonprofit tax research organization that has informed smarter tax policy at the state, federal, and global levels since 1937. We have produced the Facts & Figures handbook since 1941, we calculate Tax Freedom Day each year, we produce the State Business Tax Climate Index, and we have a wealth of other data, rankings, and analysis at our website, www.TaxFoundation.org.

I am pleased to submit written testimony on House Bill 3427, which provides a plan to improve Oregon’s public schools and dedicates $2 billion per biennium in additional funding for the Oregon public school system. While I take no position on this bill, I will argue that Oregon should not adopt the proposed Corporate Activity Tax, a gross receipts tax, as the funding mechanism to improve Oregon’s public schools.

Gross Receipts Taxes Are Unsound Tax Policy

Gross receipts taxes, which are levied on the receipts from the sales a business makes, do not live up to the principles of sound tax policy.[1] Taxes on gross receipts create tax pyramiding, which is when the same economic value is taxed multiple times as business inputs are taxed at each stage in the production process. This raises the effective tax rate on consumers, who will bear the burden of higher prices for goods and services.

While businesses are legally required to remit the Corporate Activity Tax, the economic impact of the tax will be borne by consumers, workers, and shareholders. In addition to higher prices felt by consumers, the proposed tax will result in fewer jobs for Oregonians and lower portfolio valuations for those invested in businesses paying the tax.

The key problem with gross receipts taxes is they do not exempt business-to-business transactions from the tax base. This creates tax pyramidingTax pyramiding occurs when the same final good or service is taxed multiple times along the production process. This yields vastly different effective tax rates depending on the length of the supply chain and disproportionately harms low-margin firms. Gross receipts taxes are a prime example of tax pyramiding in action. and incentivizes firms to integrate vertically to avoid the tax. The tax affects industries differently, more heavily impacting industries with high production volumes and low profit margins.

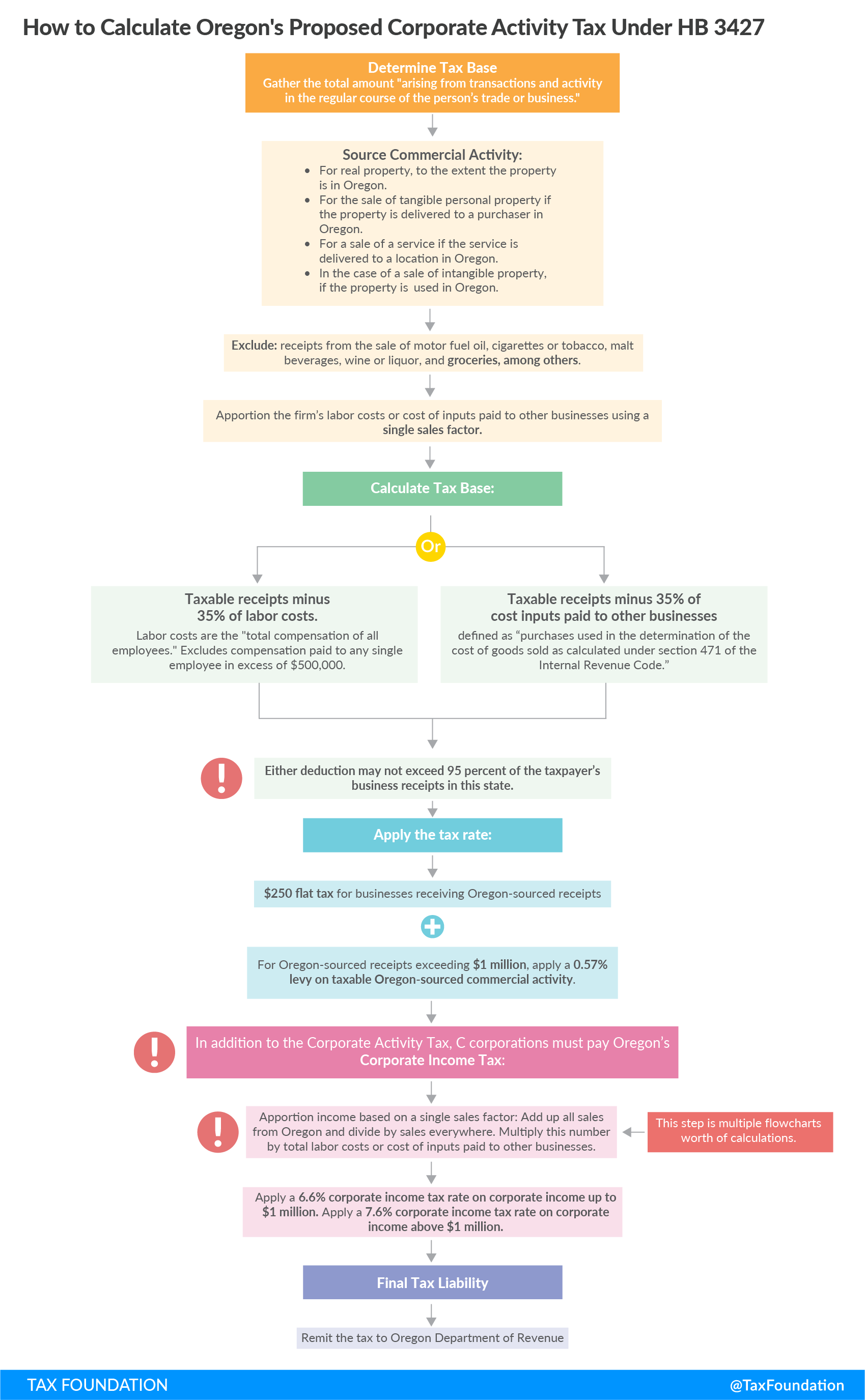

Deductions for Business Inputs and Labor Costs

The proposed Corporate Activity Tax would provide firms subject to the tax a 25 percent deduction for the cost of business inputs or labor compensation. This will help mitigate some of the tax pyramiding and negative economic effects of the tax but does so by creating complexity for businesses that must file and remit the tax.

The experience Texas has with its Margin (Franchise) Tax is instructive.[2] Like the proposed Corporate Activity Tax, the Margin Tax provided a deduction for the greater of a firm’s labor costs and the cost of business inputs, among other options. This created complexity for businesses operating in Texas and resulted in the tax failing to raise the anticipated revenue for the first two years of collections. Texas has since reduced its Margin Tax rates, and the state legislature expressed its intent to repeal the tax.

In addition to the tax complexity, the offered deductions in House Bill 3427 do not offset the negative effects the tax will create for Oregonians. The Oregon Legislative Revenue Office (LRO) finds that prices will increase by about 0.39 percent if the Corporate Activity Tax rate is levied, which is close to the 0.40 percent increase in prices projected if the legislature adopted a gross receipts taxGross receipts taxes are applied to a company’s gross sales, without deductions for a firm’s business expenses, like compensation, costs of goods sold, and overhead costs. Unlike a sales tax, a gross receipts tax is assessed on businesses and applies to transactions at every stage of the production process, leading to tax pyramiding. with no deductions permitted.[3] There are also negligible differences in employment levels and household incomes. The results are similar because the proposed deductions narrow the tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. and reduce expected revenue, which requires a higher tax rate to raise about $2 billion per biennium. The higher tax rate mostly offsets the benefits of the available deductions.

The Proposed Gross Receipts Tax Will Harm Low-Income Oregonians

The proposed Corporate Activity Tax will harm low-income Oregonians.[4] The proposed reductions in Oregon’s individual income tax rates will help mitigate the cost of the tax for many middle-income and upper-income households, but these tax rate reductions will not reach the least well-off in Oregon. This happens for two reasons. First, those households often have little to no state individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source liability to reduce. Second, while the income tax rates at the lower end of the rate schedule are being reduced, high-income filers have income in those brackets as well. Lowering rates does not actually target relief effectively.

The LRO estimates that Oregonians with household incomes below about $20,500 will experience a 0.2 percent decrease in their incomes in the long run, which translates to about $85 annually.[5] While this may be a small amount for those households with higher incomes, it could be critical for these households to make ends meet. By contrast, LRO estimates that Oregonians making above about $34,300 will experience increases in household income between 0.1 percent and 0.4 percent due to improvements in Oregon’s public school system and long-run labor force productivity.[6]

While some adjustments have been made to mitigate the regressivity of the Corporate Activity Tax, more work is needed. Ideally, the gross receipts tax would be replaced to avoid the tax pyramiding and price increases that harm low-income households, but in the interim, a refundable tax credit targeted at those with low incomes would also help these households.

Alternatives to Raise Additional Revenue

If the legislature wishes to raise $2 billion per biennium to support Oregon’s public education system, there are better options available to raise the revenue than via a gross receipts tax. A value-added tax can provide a stable source of revenue while avoiding the problems associated with taxing gross receipts.

Economic value is taxed only once under a value-added tax, which eliminates tax pyramiding and ensures that businesses and industries are treated equally under the tax code. LRO’s preliminary modeling of a value-added tax shows that prices rise less under this tax regime than a gross receipts tax, with fewer jobs lost and slightly higher average household incomes.[7]

LRO has estimated that a value-added tax has fewer negative effects on low-income Oregonians than the proposed Corporate Activity Tax. These households may still experience lower household incomes in the long run, which suggests that a refundable tax credit may also be deployed to ensure that these households are made whole.

While state-level value-added taxes are less common than gross receipts taxes, New Hampshire is a state that has successfully administered this tax and could serve as a model for designing a similar tax for Oregon.

Conclusion

The proposed Corporate Activity Tax in the amendment to House Bill 3427 may harm low-income Oregonians while introducing complexity into Oregon’s corporate tax code. The experience other states have with gross receipts taxes shows that it is not an efficient nor a simple way to raise revenue when compared to a value-added tax. Oregon can raise the revenue needed to improve public education in the state through a value-added tax, reducing the economic harm placed on low-income households and maintaining Oregon’s competitive business tax code.

Taxes make more sense with us in your inbox.

Subscribe to our newsletter for tax insights that cut through the noise—and make sense of it.

Sign Up[1] Garrett Watson, “Resisting the Allure of Gross Receipts Taxes: An Assessment of Their Costs and Consequences,” Tax Foundation, Feb. 6, 2019, https://taxfoundation.org/gross-receipts-tax/.

[2] Garrett Watson and Nicole Kaeding, “Oregon Shouldn’t Adopt a Margin Tax in Its Search for Revenue,” Tax Foundation, April 8, 2019, https://taxfoundation.org/oregon-margin-tax-revenue/.

[3] Oregon Legislative Revenue Office, “Modified Commercial Activity Tax Option 1AL and 2AL,” Oregon Joint Committee on Student Success Revenue Subcommittee Meeting Document, April 8, 2019, https://olis.leg.state.or.us/liz/2019R1/Downloads/CommitteeMeetingDocument/189142.

[4] Garrett Watson, “Oregon’s Proposed Corporate Activity Tax Would Harm Low-Income Oregonians the Most,” Tax Foundation, April 19, 2019, https://taxfoundation.org/oregon-business-tax-proposal/.

[5] Oregon Legislative Revenue Office, “Modified Commercial Activity Tax Option 2AL.”

[6] Ibid.

[7] Garrett Watson and Nicole Kaeding, “Oregon’s Proposed Gross Receipts Tax Is More Damaging Than Proposed Value-Added Tax,” Tax Foundation, March 13, 2019, https://taxfoundation.org/oregons-gross-receipts-tax-proposal-vat//.