Update (5/18/17): When we presented this testimony in January 2017, our written testimony cited a pass-through carveout estimate of over $500 million from the Kansas tax expenditure report because on the day we testified, Kansas acting revenue secretary Sam Williams withdrew the official state estimate of the cost as inadequately low and promised a future revision, and no other official estimates were publicly available. In oral testimony that day, we said the actual number was probably between $200 million and $300 million per year, and since then, more recent estimates have confirmed that range. We have decided to update this number in this post since this post is cited frequently. We also replaced an incorrect reference to 2015 spending growth with spending changes each year since 2013. Additionally, we have changed several references to years in this testimony to indicate fiscal years or calendar years, to improve clarity.

Update (6/30/17): We have appended a note on pass-through data information following a May 2017 revelation that the Governor’s original 2012 estimate of pass-through entities was incorrect.

Presentation to the Kansas House Committee on Taxation

Chairman Johnson, Vice Chairman Phillips, Ranking Member Sawyer, Members of the Committee,

Thank you for the opportunity to speak with you today. My name is Scott Drenkard, and I’m an economist and the director of state projects at the TaxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. Foundation. I am joined by my colleague Joe Henchman, Vice President of Legal & State Projects at the Tax Foundation. For those unfamiliar with our group, we are a non-partisan, non-profit organization that has monitored fiscal policy at all levels of government since 1937. We have produced the Facts & Figures handbook since 1941, we calculate Tax Freedom Day each year, and have a wealth of data, rankings, and other information at our website, www.TaxFoundation.org.

While we take no position on legislation, we hope to offer our insights and provide a national perspective on tax issues.

Kansas’ pass-through exemption is costly and has forced other tax increases

In 2012, Kansas enacted a tax cut package that reduced income tax rates while completely eliminating income tax on pass-through entities like LLCs, S corps, partnerships, farms, and sole proprietorships. At the time, we warned that the pass-through exemption did not have good economic justification and would “encourage economically inefficient, though tax-reducing” restructuring activity. We also warned that the “tax reductions, while producing positive economic benefits, would cost revenue and ultimately need to be paid for either by cutting spending or increasing taxes elsewhere.”

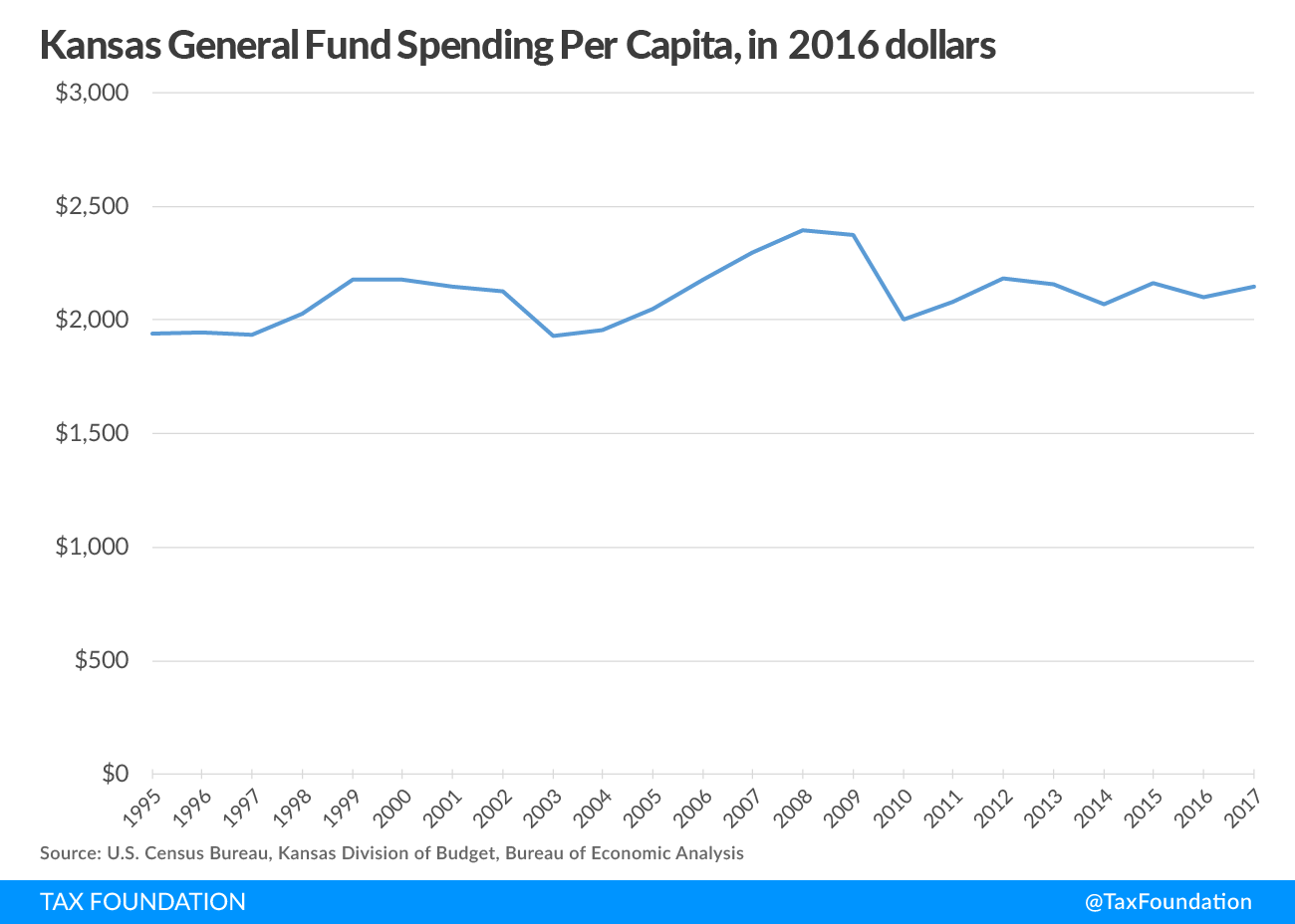

Between FY 2013 and FY 2014, revenue dropped by $688 million, from $6.341 billion to $5.653 billion ($293 million more than the predicted drop to $5.947 billion). Spending between those years was only cut $152 million, from $6.134 billion to $5.982 billion. These numbers are quite large for a $6 billion general revenue fund. The state delayed a planned cut to the sales taxA sales tax is levied on retail sales of goods and services and, ideally, should apply to all final consumption with few exemptions. Many governments exempt goods like groceries; base broadening, such as including groceries, could keep rates lower. A sales tax should exempt business-to-business transactions which, when taxed, cause tax pyramiding. , weakened the generosity of itemized deductions, and drew down reserves to make ends meet.

FY 2015 had a significant cash deficit, masked by draining the rainy day fund and beginning balances. Spending growth has also been slow, averaging about 0.5 percent in recent years (+1.11 percent in 2013, -2.96 percent in 2014, +4.25 percent in 2015, -0.55 percent in 2016, and proposed +1.09 percent in 2017), and just 0.3 percent per year since 2008.

{kind=link}

At the beginning of FY 2016, budget deficits widened sufficiently and spending remained adequately high that hikes to other taxes were necessary to make the budget balance. The state hiked the sales tax rate from from 6.15 percent to 6.5 percent, giving the state the 8th highest sales tax in the country. The state hiked the cigarette tax rate from 79 cents per pack to $1.29 per pack. A new tax was placed on vapor products (e-cigarettes). The state also eliminated many deductions in the individual income tax, and created a one-time tax amnesty program.

Governor Brownback’s latest budget proposal includes a further $1 cigarette tax increase, which for a state that borders Missouri is in my view untenable (Missouri levies a 17 cent per pack tax). This proposal is joined by a plan to securitize funds from the tobacco Master Settlement Agreement, which would dry up a future revenue stream to solve this year’s budget issues.

This budget history is unsustainable in the long term.

The pass-through exemption encourages tax avoidance without generating desired growth

My judgment, which is shared by my colleagues, is that the pass-through exemption is an important reason for Kansas’ revenue underperformance, and a carve-out which deserves reexamination. When the exemption was passed in 2012, it was projected that 191,000 entities would take advantage of the provision. As more and more people have realized the very sizeable tax advantage of being a pass-through entity in Kansas, the latest tally (2015) on that number has grown to 393,814 claimants, over twice as many as anticipated. Estimates are that this deduction results in $200 million to $300 million in foregone revenue annually.

[June 2017 Note: In late May, Dave Trabert of the Kansas Policy Institute reported that the Governor’s office’s 2012 estimate of 191,000 entities, which was used as the basis for the original revenue estimate, was incorrect. It was derived by adding up all Kansas tax filers who report income on Schedule C, while subsequent updates from the administration were based on filers who report income on Schedules C, E, and F. Federal tax return data shows Kansas filers who report income on Schedules C, E, and F grew just 1.9 percent between 2012 and 2014 (the most recent federal data available), not the sharp increase that we (and everyone) have reported occurred. However, the total pass-through income reported by those filers did spike, by 11 percent in that time frame. Similarly, Kansas data continues to report significant entity-level growth: the Kansas Secretary of State reports new business filings grew 11 percent between 2012 and 2014, and a further 10 percent through 2016, so new pass-throughs were being set up at a brisk rate under the pass-through carveout policy. It is reasonable to conclude, based on this data and anecdotal evidence, that while few people went from zero income on Schedules C, E, and F to some, Kansans who already reported income on those forms increased how much they were reporting and created new Kansas business entities with the Secretary of State. We look forward to post-2014 data becoming available to provide further information.]

It’s important to note here that while decreasing taxes is generally associated with greater economic growth, the pass-through carve out is primarily incentivizing tax avoidance, not job creation.

If they passed a provision like this in Washington, D.C., where I live and work, I would benefit from going to my employer the next day and ask them to start paying me as an independent contractor. I would still be doing the same job and contributing the same value to the economy, I just wouldn’t be paying any income taxes.

The individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source of tax revenue in the U.S. is one of the largest instruments in the Kansas revenue toolkit. Exempting pass-through income substantially narrowed the tax base of that instrument, and in a haphazard way.

The pass-through exemption is damaging the state tax reform conversation nationally

As a final comment, I think it may be in instructive to share a story about the impact this policy is having on tax reform in other states. In 2014, I testified before the Nebraska Senate Finance Committee on a bill to gradually lower corporate and individual income tax rates. The plan was to reduce rates by small bits each year with a revenue trigger built in so that the cuts only occurred in years with healthy revenue growth. It was a balanced proposal that was designed to cultivate bipartisan support. This is a state where the legislature is officially nonpartisan; members do not have a party affiliation.

I got multiple questions about Kansas’s budget issues, with committee members not wanting to subject themselves to the kind of revenue shortfalls this state has experienced. The tax reform package in Nebraska didn’t pass, and I’m pretty sure the feeling of trepidation about Kansas’ tax cuts contributed to its failure.

I speak on tax issues in other states almost every week, and I often get questions from the audience along the lines of, “what happened in Kansas?” This is not good for state branding or economic development.

Tax reform is about broadening tax bases and lowering tax rates. This state has lowered tax rates in some spaces, but the pass-through exemption significantly narrows the tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. , and this has made for a less stable, productive, and competitive code.