A common refrain from many progressive lawmakers is that the rich don’t pay their fair share of taxes. “Fair share” is, of course, subjective. But a new Treasury study provides data showing that the rich not only pay more than the middle class, they pay more than one-third of their annual income in federal taxes and more than 45 percent when state and local taxes are included.

Indeed, the total taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. burden on the super-wealthy, especially those with large stakes in global businesses, is upwards of 60 percent of their annual income because of the taxes they pay abroad.

Segmenting Taxpayers by Wealth, Not Income

The study classifies taxpayers according to an estimate of their wealth rather than their income, with the intention of showing that the rich pay very little in taxes (individual income, estate, and corporate taxes) relative to their wealth. However, the data shows that the rich are not undertaxed relative to their annual income as many claim.

As Table 1 details, in 2019, there were 183 million tax units, which includes those with a tax liability and those with no liability (the so-called nonpayers) as well as non-filers. The average tax unit had adjusted gross incomeFor individuals, gross income is the total of all income received from any source before taxes or deductions. It includes wages, salaries, tips, interest, dividends, capital gains, rental income, alimony, pensions, and other forms of income. For businesses, gross income (or gross profit) is the sum of total receipts or sales minus the cost of goods sold (COGS)—the direct costs of producing goods, including inventory and certain labor costs. (AGI) of roughly $65,000 and about $503,500 in wealth from all sources.

Table 1. Wealth and Income by Wealth Categories

| All | Top 10% | Top 1% | Top .1% | Top .01% | Top .001% | |

|---|---|---|---|---|---|---|

| Number of Tax Units | 183,700,000 | 18,370,000 | 1,837,000 | 183,700 | 18,370 | 1,837 |

| Wealth per Tax Unit (Thousands) | $503.5 | $3,805 | $18,793 | $93,902 | $485,268 | $2,318,864 |

| Adjusted Gross Income per Tax Unit (Thousands) | $65.4 | $273.4 | $1,093 | $4,963 | $21,314 | $98,851 |

In 2019, the top 10 percent of tax units by wealth had an average AGI of about $273,000 and $3.8 million in wealth. At the top end of the scale, the top 0.001 percent, or the wealthiest 1,837 tax units, had an average AGI of nearly $99 million and more than $2.3 billion in wealth.

The study then compares the burden of federal, state and local, and foreign taxes on each of these various tax units.

Effective Tax Rates Rise as Incomes Rise

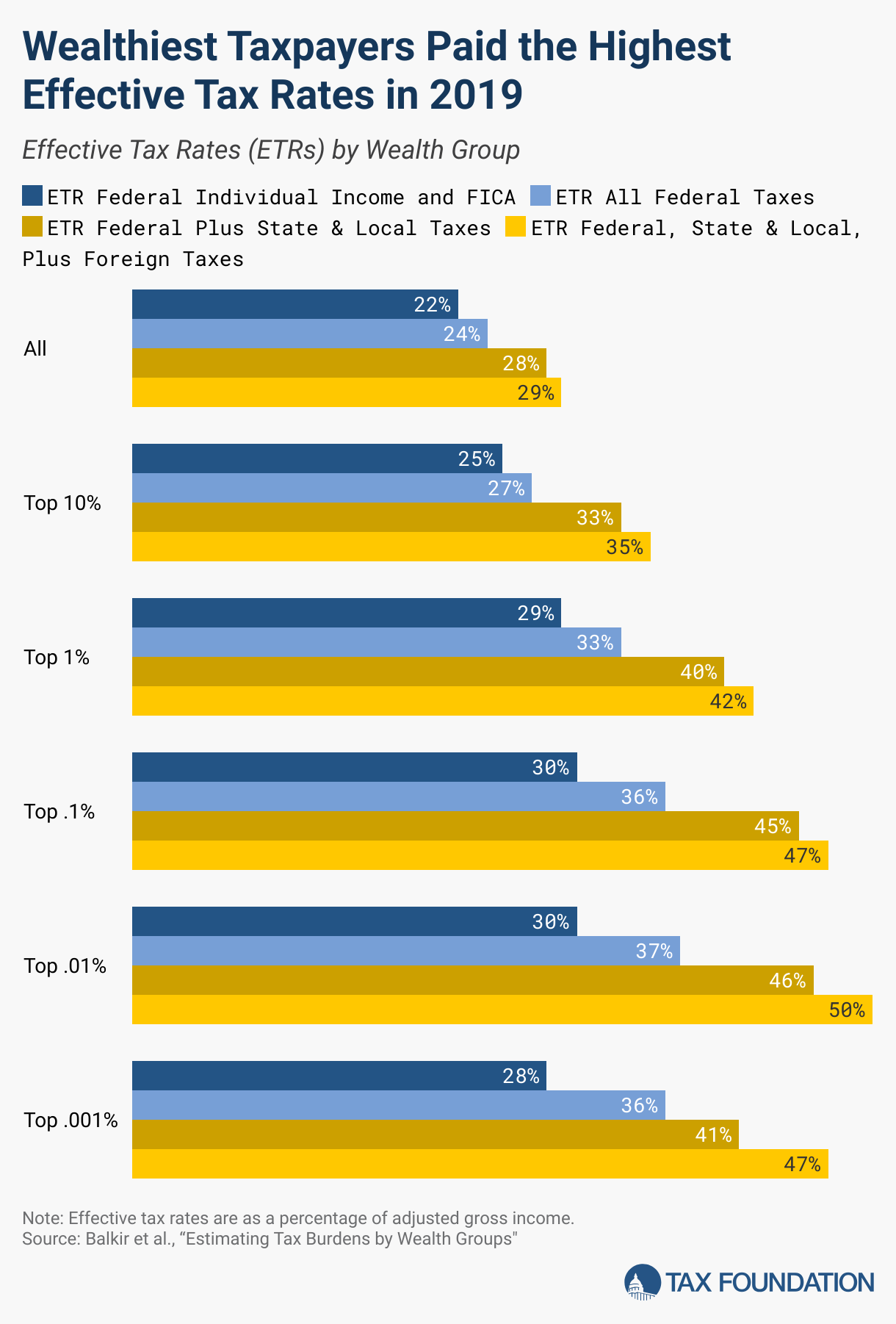

Figure 1 illustrates the effective tax rates (ETRs) paid by tax units in each wealth class based on four measures: the combination of federal individual income and payroll taxes; the combination of federal individual income, estate, and corporate income taxes; the combination of federal taxes plus state and local-level individual and corporate income taxes; and the combination of all US taxes plus foreign corporate and individual income taxes.

Figure 1 shows that the burden of federal income and payroll taxes for the average tax unit was about 22 percent in 2019. We should note that the Treasury report does not calculate effective tax rates. It only includes estimates of AGIs and estimates of the average taxes paid by each income group. We have calculated the effective tax rates using this information.

Effective tax rates generally go up with wealth. The wealthiest 10 percent had an effective federal income and payroll taxA payroll tax is a tax paid on the wages and salaries of employees to finance social insurance programs like Social Security, Medicare, and unemployment insurance. Payroll taxes are social insurance taxes that comprise 24.8 percent of combined federal, state, and local government revenue, the second largest source of that combined tax revenue. rate of 25 percent. For the next three wealthy groups (the top 1 percent, 0.1 percent, and 0.01 percent), the effective tax rate for federal income and payroll taxes climbs to 30 percent. It drops slightly to 28 percent for tax units in the richest 0.001 percent.

Corporate Income Estate Taxes Add Significantly to the Federal Effective Tax Rates of the Wealthy

Federal taxes on corporate income and estates add to every group’s effective tax rates. The authors assume that the burden of corporate taxes falls entirely on the owners of capital, so the more capital a tax unit owns or is invested in, the more corporate taxes they must pay. Most economists believe that some of the burden of the corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. falls on workers through lower wages (in some cases by more than 50 percent).

As a consequence of this assumption, the Treasury report likely underestimates the burden of corporate taxes on the average tax unit and overestimates the tax burden on the wealthy.

The data illustrates this assumption clearly. Federal corporate and estate taxes add 2 percentage points to the effective tax rates of the average tax unit as well as tax units in the top 10 percent. However, federal corporate and estate taxes add 4 percentage points to the effective tax rates of those in the top 1 percent, 6 percentage points to the effective tax rates of those in the top 0.1 percent, and 8 percentage points for those in the top 0.001 percent.

As a result, the all-in federal effective tax rates for the richest tax units rise to as high as 37 percent.

State Taxes Raise Effective Tax Rates Even Higher

Adding state and local taxes to federal tax burdens further illustrates how much more the rich pay overall compared to average taxpayers. For the average tax unit, state and local taxes add 4 percentage points to their federal effective tax rate, for a combined effective tax rate of 28 percent. But for tax units in the top .01 percent, for example, state and local taxes add 9 percentage points to their effective tax rates, resulting in a combined effective tax rate of 46 percent—approaching half of their annual income.

Foreign Corporate Taxes Raise Effective Tax Rates to 50 Percent for Some Wealthy

At every level of wealth, the Treasury study estimates that tax units bear some amount of foreign corporate income taxes. For the average tax unit, foreign corporate income taxes add less than 1 percentage point to their effective tax rate. But for the wealthy in the top 10 percent, foreign corporate income taxes add 2 percentage points to their effective tax rates, for a total rate of 35 percent. However, for those in the top 0.01 percent, corporate income taxes boost their overall effective tax rate to 50 percent, i.e., half of their annual income.

But What About the Super-Rich?

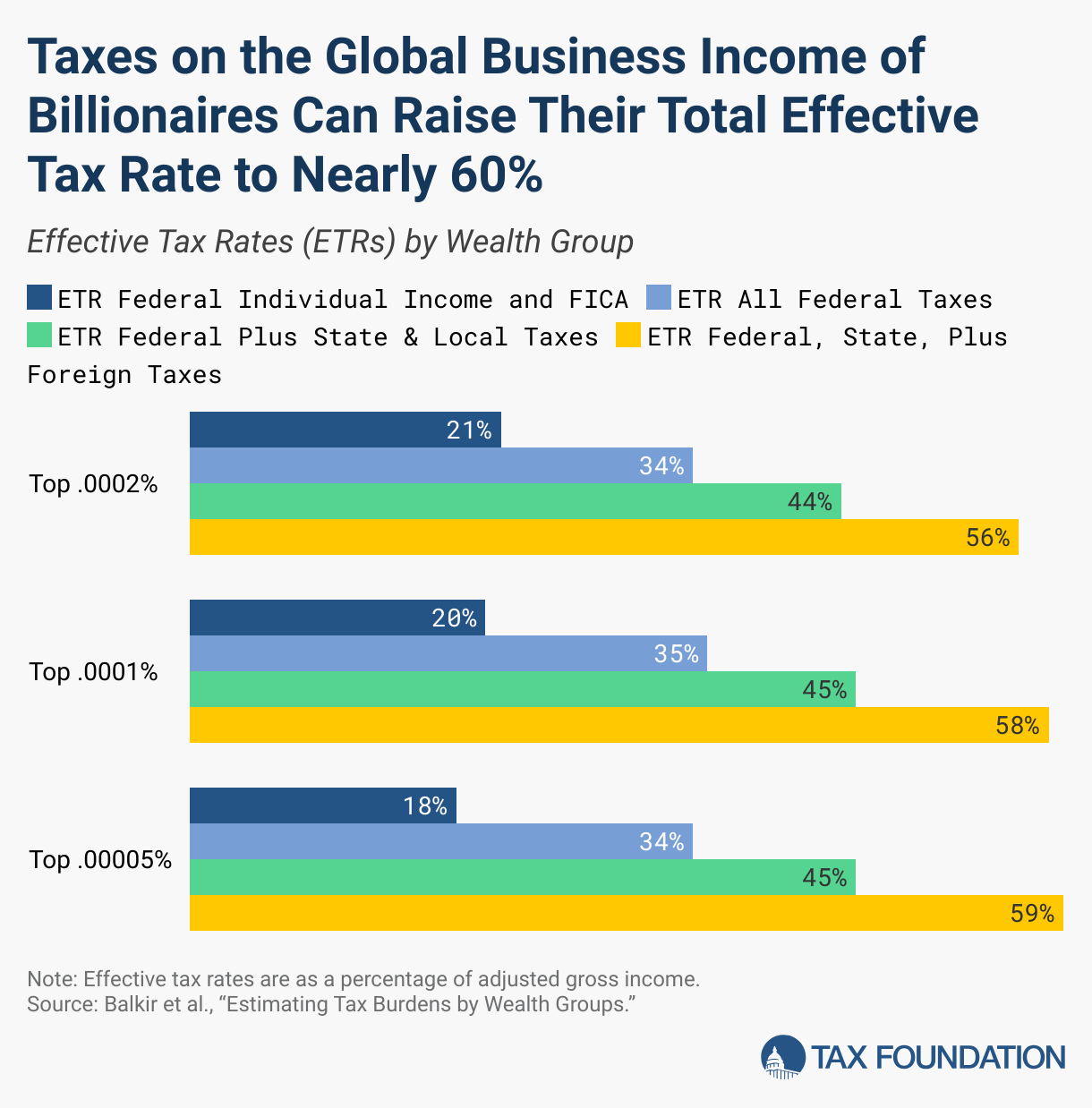

The study separately estimated the tax burden for three sample groups within the “Fortunate 400,” nicknamed for the 400 wealthiest individual taxpayers. The first group represents the top 0.0002 percent, composed of 367 tax units with an average AGI of about $173 million and average wealth of about $8.0 billion. The next group is the top 0.0001 percent, representing 184 tax units with an average AGI of about $245 million and average wealth of nearly $13 billion. The last group is the top 0.00005 percent, representing just 92 tax units with an average AGI of about $345 million and average wealth of about $20.8 billion.

The substantial global interests of the super-rich require them to pay individual income taxes as well as the corporate income taxes they owe to foreign tax authorities. The combined impact of multiple layers of taxes owed to multiple levels of government raises their effective tax rates to exceptionally high levels.

As Figure 2 illustrates, for the top 0.0002 percent of wealthy tax units, federal income and payroll taxes amount to 21 percent of their AGI. Although 21 percent is a lower effective tax rate than the average of all tax units, it represents an average tax bill of $36.8 million. The federal income and payroll tax effective tax rates for the two richest income groups are 20 percent (an average of $49 million) and 18 percent (an average of $62 million), respectively.

Their federal effective tax rates jump to as high as 35 percent when corporate income and estate taxes are included, then jump again to as high as 44 to 45 percent when state and local taxes are added.

Surprisingly, Treasury finds that the corporate income taxes they pay to foreign jurisdictions nearly equals the corporate income taxes they pay to the US Treasury. For example, Treasury estimates that the average tax unit in the top 0.0002 percent pays $19.8 million in US federal corporate income taxes and $17.6 million in foreign corporate income taxes. Similarly, the richest 0.00005 percent were estimated to pay $51.5 million in US corporate income taxes and $45.8 million in foreign corporate income taxes.

All told, we can see that when foreign taxes are added to their US tax burden, the effective tax rates for the wealthiest Americans rise to nearly 60 percent. Thus, focusing on the US tax burden does not tell the whole story of the taxes the super-wealthy pay in total.

The Treasury study was no doubt commissioned to demonstrate that wealthy Americans pay a relatively small amount of income taxes compared to their total wealth. But most governments, foreign and domestic, tax people and businesses on their income and not their wealth.

By that measure, the Treasury report clearly shows that tax systems at every level—federal, state and local, and foreign—tend to be very progressive, requiring the rich to pay super-amounts of taxes.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe