South Dakota’s Initiated Measure 28 proposes something popular, common, and, particularly in South Dakota’s context, misguided. The measure, which attempts to exempt groceries from the sales taxA sales tax is levied on retail sales of goods and services and, ideally, should apply to all final consumption with few exemptions. Many governments exempt goods like groceries; base broadening, such as including groceries, could keep rates lower. A sales tax should exempt business-to-business transactions which, when taxed, cause tax pyramiding. , is ambiguously drafted, with the potential to exempt not only groceries but also cigarettes and other non-grocery products from sales and excise taxes. And in a state that forgoes income taxes and instead relies on an unusually broad-based sales taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. , carving up that base is no small thing, especially when (despite the popularity of grocery exemptions), the evidence suggests that grocery exemptions are an unusually poor way of providing tax relief to low-income households.

Initiated Measure 28, the Prohibit Food and Grocery Taxes Initiative, provides that “Notwithstanding any other provision of law, the state may not tax the sale of anything sold for human consumption, except alcoholic beverages and prepared food. Municipalities may continue to impose such taxes.”

Whether cigarettes and other tobacco products will be given tax-free status under the proposition is itself unclear and debates about this are ongoing. The text does not define, for example, “prepared food” or “human consumption.” Is a cigarette consumed, or does consumption mean only to eat or drink? Or are some tobacco products, like vapes and cigarettes, consumed while others, like chewing tobacco, are not consumed because they are not inhaled or swallowed? Of course, these are very specific questions, but they are exactly the types of questions that will arise as businesses and government officials respond to the measure. When other states have exempted groceries, they’ve spent considerably more than two sentences spelling out the policy details to avoid precisely these ambiguities.

South Dakota policymakers recently delivered on sales tax relief by cutting the sales tax rate from 4.5 to 4.2 percent, but that rate reduction is temporary, set to expire in mid-2027. Many lawmakers would like to see the reduction made permanent, if revenues allow.

A grocery exemption, though, is a different story, and may interfere with efforts to make the rate reduction permanent. Several key policymakers have come out against the measure, including the governor. Some—mostly Republicans—have also raised concerns about the proposal’s vague language and potential consequences, while many Democratic legislators support the proposal, as they believe this exemption would lead to more progressivity in an otherwise regressive sales tax.

That belief—that a grocery exemption is progressive—is widely shared by members of both parties and has been a driving force in the exemption of groceries from sales tax bases across the country. It is simple, straightforward—and wrong.

Even assuming the measure only exempts groceries, it will reduce state revenues by an estimated $102.4 million a year—about 4 percent of the state’s general fund revenues. This does not include the $57.5 million the state raises from tobacco excise taxes, nor the amount that tobacco sales currently generate in general sales tax revenue.

The recent, temporary sales tax rate reduction also costs about $100 million a year. Exempting groceries, even if the state can afford to do so under current revenue forecasts, reduces the capacity to make that rate reduction permanent, or to expand upon it.

For those concerned about progressivity, then, the question becomes this: which helps low-income households more, (1) retaining or maybe even building upon the recent rate reduction, or (2) excluding groceries from the base?

Unlike some policy questions, this one has an empirical answer: low-income households benefit more from the lower rate than from the grocery exemption.

How can that be, given that low-income households consume a greater share of their income, and spend more on groceries as a percentage of income than do higher earners? It’s simple: under federal law, states are already prevented from applying sales tax to purchases made with SNAP or WIC benefits. And while these benefits don’t cover all the grocery expenses of low-income households, they cover a fair bit—enough that the remaining, taxed groceries they purchase represent a lower share of their income than do the groceries purchased by higher earners. Meanwhile, they’re spending much of their remaining income on other purchases that are taxable. A lower rate on everything delivers more benefits to these households than an exemption for groceries which are, for them, already partially exempt. (If you want to see the calculations on this, click here.)

And if it doesn’t help low-income households, is it worth carving up the tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. ?

The sales tax is a relatively economically efficient tax. Particularly to the extent that it falls on final consumption, it does far less economic harm than income taxes, which South Dakota notably avoids. Income taxes fall on labor and investment—and whatever you tax, you get less of. Far better, economically speaking, to tax consumption instead; it creates significantly fewer distortions.

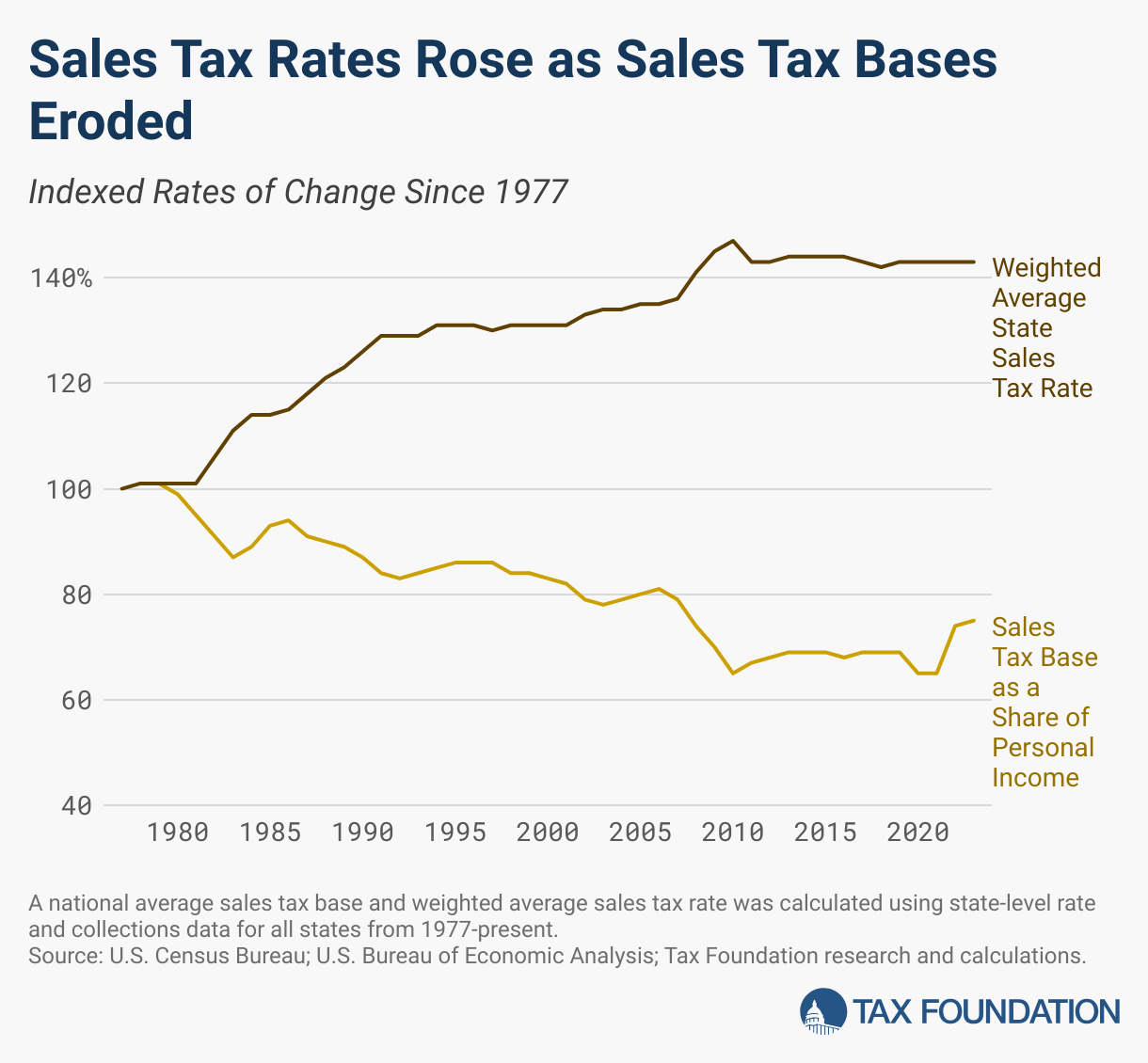

But every time new exemptions are added, new distortions are created, and more pressure is put on the tax base that remains. This requires higher rates than would be necessary if a broader base were maintained, or even forces lawmakers to adopt new taxes to offset revenue losses from the sales tax. Across the country, policymakers have been chipping away at sales tax bases for years, and rates have risen to compensate.

Better a 4.2 percent rate with groceries in the base than 4.5 percent without—or, if South Dakota lawmakers find that they can afford both, then by definition it could also afford a rate of about 3.9 percent with groceries in the base. Especially for a state that relies so heavily on the sales tax as a source of revenue—and where most people want to keep it that way—a broad base and a low rate is crucial.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe