Thomas Locher

Summer Global Intern

Thomas Locher was a 2021 summer intern with the Tax Foundation’s Center for Global Tax Policy.

Latest Work

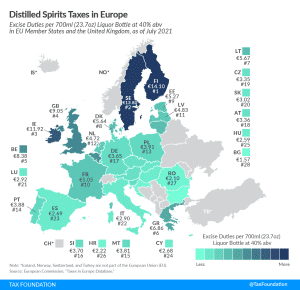

Distilled Spirits Taxes in Europe, 2021

The highest excise duties are applied in Finland, Sweden, and Ireland, where the rates for a standard-size bottle of liquor are €14.10 ($16.08), €13.80 ($15.73), and €11.92 ($13.59), respectively.

3 min read

Four Revenue Scores on Options to Change U.S. International Tax Rules

Changes to international tax rules are likely on the way, and it is therefore important for lawmakers to understand how various reform options would impact U.S. tax burdens on multinational companies. Moreover, policymakers should also recognize the need for prudent policies that do not put U.S.-based multinationals at a competitive disadvantage or severely curtail investment and hiring.

9 min read

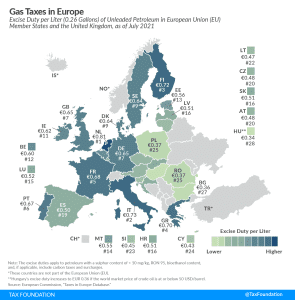

Gas Taxes in Europe, 2021

5 min read

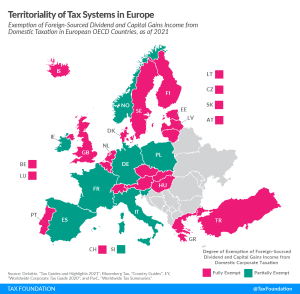

Territoriality of Tax Systems in Europe

19 European OECD countries employ a fully territorial tax system, exempting all foreign-sourced dividend and capital gains income from domestic taxation. No European OECD country operates a worldwide tax system.

3 min read

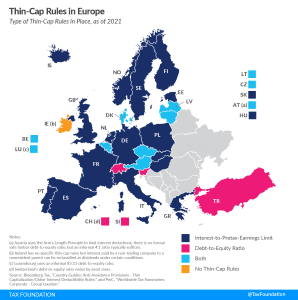

Thin-Cap Rules in Europe

To discourage this form of international debt shifting, many countries have implemented so-called thin-capitalization rules (thin-cap rules), which limit the amount of interest a multinational business can deduct for tax purposes.

5 min read

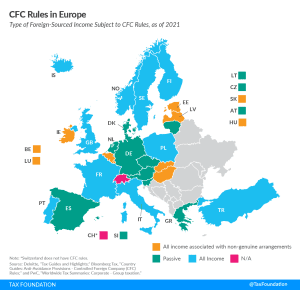

CFC Rules in Europe

To prevent businesses from minimizing their tax liability by taking advantage of cross-country differences, countries have implemented various anti-tax avoidance measures, such as the so-called Controlled Foreign Corporation (CFC) rules.

5 min read

Anti-Base Erosion Provisions and Territorial Tax Systems in OECD Countries

From a policy perspective it is appropriate to combat base erosion and profit shifting, but policymakers need to keep in mind the need for simplicity to avoid increasing the compliance burden on taxpayers and administrative burdens on tax authorities.

68 min read

Exploring How Remote Work Could Impact the Way Countries Tax Individuals

A question for policymakers to consider is how this new era of worker mobility will impact the fiscal landscape, and what changes must be made to address resulting revenue and compliance concerns.

6 min read

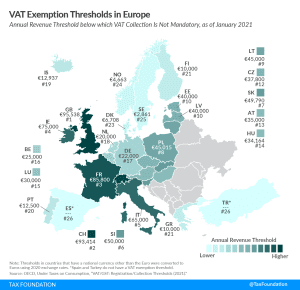

VAT Exemption Thresholds in Europe

To reduce tax compliance and administrative costs, most countries have VAT exemption thresholds: If a business is below a certain annual revenue threshold, it is not required to participate in the VAT system.

2 min read

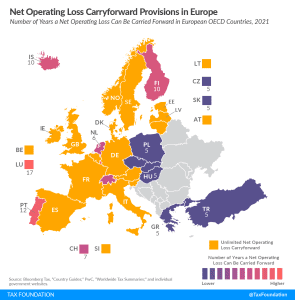

Net Operating Loss Carryforward and Carryback Provisions in Europe, 2021

Many companies have investment projects with different risk profiles and operate in industries that fluctuate greatly with the business cycle. Carryover provisions help businesses “smooth” their risk and income, making the tax code more neutral across investments and over time.

7 min read

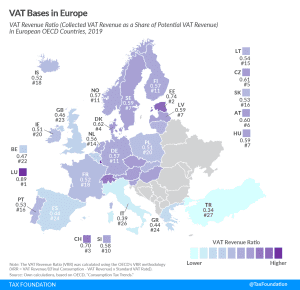

VAT Bases in Europe

As economic activity resumes and the task of accounting for the deficits incurred in navigating the crisis of the past year becomes the focus of fiscal policy deliberations, a greater reliance on VAT could be an important tool in ensuring fiscal stability going forward. Countries should use this as an opportunity to improve VAT systems by re-examining carveouts in the form of exemptions and reduced rates.

2 min read

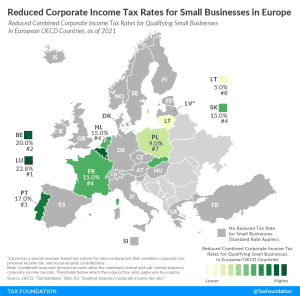

Reduced Corporate Income Tax Rates for Small Businesses in Europe

Corporate income taxes are commonly levied as a flat rate on business profits. However, some countries provide reduced corporate income tax rates for small businesses. Out of 27 European OECD countries covered in today’s map, eight levy a reduced corporate tax rate on businesses that have revenues or profits below a certain threshold.

3 min read