Wealth Taxes in Europe, 2020

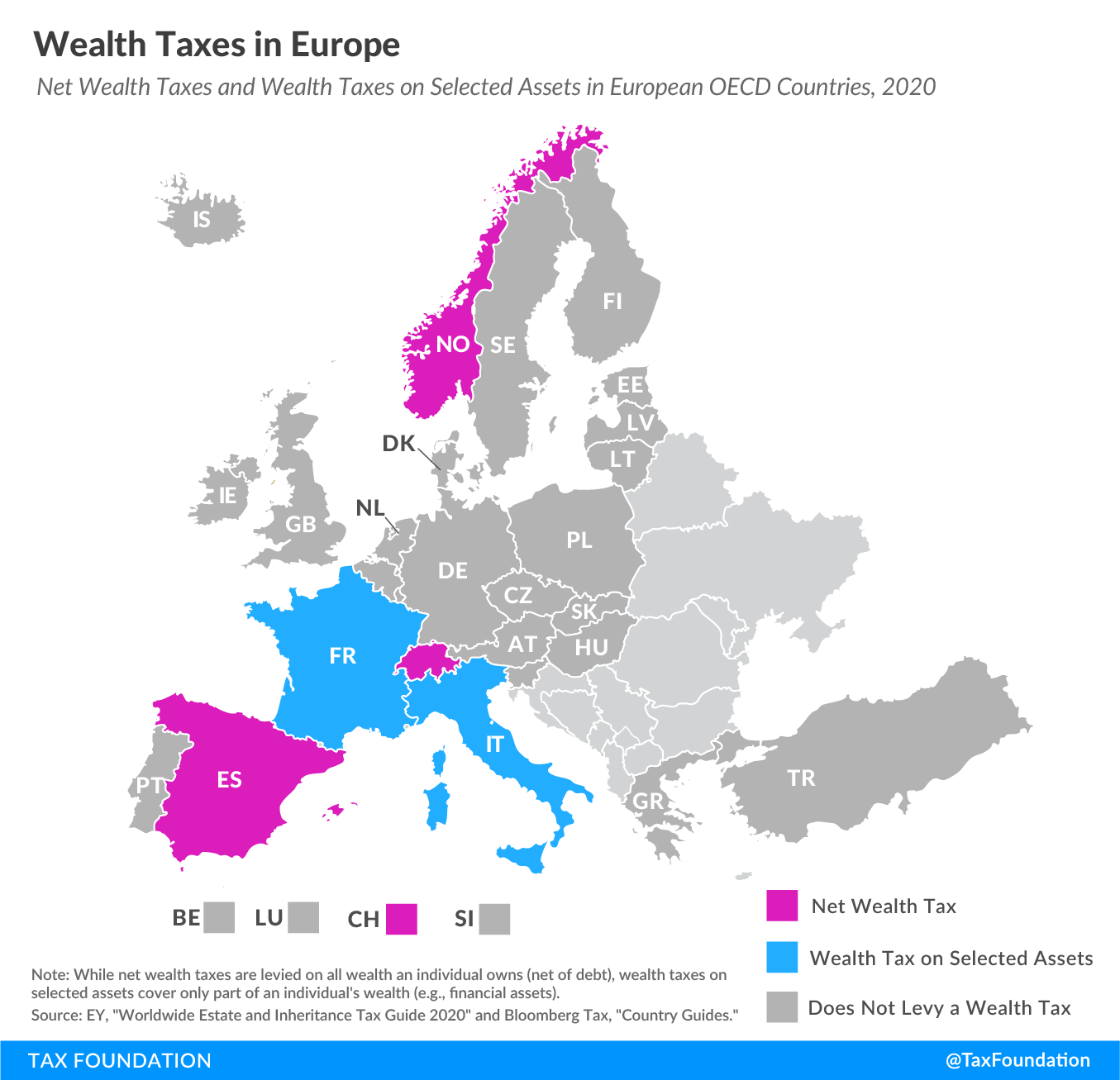

3 min readBy:Net wealth taxes are recurrent taxes on an individual’s wealth, net of debt. The concept of a net wealth taxA wealth tax is imposed on an individual’s net wealth, or the market value of their total owned assets minus liabilities. A wealth tax can be narrowly or widely defined, and depending on the definition of wealth, the base for a wealth tax can vary. is similar to a real property taxA property tax is primarily levied on immovable property like land and buildings, as well as on tangible personal property that is movable, like vehicles and equipment. Property taxes are the single largest source of state and local revenue in the U.S. and help fund schools, roads, police, and other services.. But instead of only taxing real estate, it covers all wealth an individual owns. As today’s map shows, only three European countries covered levy a net wealth tax, namely Norway, Spain, and Switzerland. France and Italy levy wealth taxes on selected assets but not on an individual’s net wealth per se.

Net Wealth Taxes

Norway levies a net wealth tax of 0.85 percent on individuals’ wealth stocks exceeding NOK1.5 million (€152,000 or US $170,000), with 0.7 percent going to municipalities and 0.15 percent to the central government. Norway’s net wealth tax dates to 1892. Under COVID-19-related measures, individual business owners and shareholders who realize a loss in 2020 are eligible for a one-year deferred payment of the wealth tax.

Spain’s net wealth tax is a progressive tax ranging from 0.2 percent to 3.75 percent on wealth stocks above €700,000 ($784,000; lower in some regions), with rates varying substantially across Spain’s autonomous regions (Madrid offers a 100 percent relief). Spanish residents are subject to the taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. on a worldwide basis while nonresidents pay the tax only on assets located in Spain.

Switzerland levies its net wealth tax at the cantonal level and covers worldwide assets (except real estate and permanent establishments located abroad). The tax rates and allowances vary significantly across cantons. The Swiss net wealth tax was first implemented in 1840.

Wealth Taxes on Selected Assets

France abolished its net wealth tax in 2018 and replaced it that year with a real estate wealth tax. French tax residents whose net worldwide real estate assets are valued at or above €1.3 million ($1.5 million) are subject to the tax, as well as non-French tax residents whose net real estate assets located in France are valued at or above €1.3 million. Depending on the net value of the real estate assets, the tax rate is as much as 1.5 percent.

Italy taxes financial assets held abroad without Italian intermediaries by individual resident taxpayers at 0.2 percent. In addition, real estate properties held abroad by Italian tax residents are taxed at 0.76 percent.

| Country | ISO-2 | Net Wealth Tax | Wealth Tax on Certain Assets |

|---|---|---|---|

| Austria | AT | ||

| Belgium | BE | ||

| Czech Republic | CZ | ||

| Denmark | DK | ||

| Estonia | EE | ||

| Finland | FI | ||

| France | FR | Yes | |

| Germany | DE | ||

| Greece | GR | ||

| Hungary | HU | ||

| Iceland | IS | ||

| Ireland | IE | ||

| Italy | IT | Yes | |

| Latvia | LV | ||

| Lithuania | LT | ||

| Luxembourg | LU | ||

| Netherlands | NL | ||

| Norway | NO | Yes | |

| Poland | PL | ||

| Portugal | PT | ||

| Slovakia | SK | ||

| Slovenia | SI | ||

| Spain | ES | Yes | |

| Sweden | SE | ||

| Switzerland | CH | Yes | |

| Turkey | TR | ||

| United Kingdom | GB | ||

|

Note: While net wealth taxes are levied on all wealth an individual owns (net of debt), wealth taxes on selected assets cover only part of an individual’s wealth (e.g., financial assets). Source: EY, “Worldwide Estate and Inheritance Tax Guide 2020″ and Bloomberg Tax, “Country Guides.” |

|||

Taxes make more sense with us in your inbox.

Subscribe to our newsletter for tax insights that cut through the noise—and make sense of it.

Sign UpAbout the Author

Elke Asen

Policy Analyst

Elke Asen was a Policy Analyst with the Tax Foundation’s Center for Global Tax Policy, focusing on international tax issues and tax policy in Europe. Prior to joining the Tax Foundation, Elke interned with the EU Delegation in Washington, D.C., the German Development Agency, and a social startup in Munich, Germany. She holds a BS in Economics from Ludwig Maximilian University of Munich.