I am Scott Hodge, president of the TaxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. Foundation. Thank you for the opportunity to speak to you today about how comprehensive tax reform can boost America’s long-term economic growth and improve our global competitiveness.

Founded in 1937, the Tax Foundation is the nation’s oldest non-partisan, non-profit organization dedicated to promoting economically sound tax policy at all levels of government.

We are guided by the immutable principles of economically sound tax policy which say that: Taxes should be neutral to economic decision making, they should be simple, transparent, stable, and they should promote economic growth.

In other words, the ideal tax system should do only one thing—raise a sufficient amount of revenues to fund government activities with the least amount of harm to the economy.

By all accounts, the U.S. tax system is far from that ideal.

Introduction

The U.S. tax system is in desperate need of simplification and reform. Over the past two decades, lawmakers have increasingly asked the tax code to direct all manner of social and economic objectives, such as encouraging people to buy hybrid vehicles, turn corn into gasoline, save more for retirement, purchase health insurance, buy a home, replace the home’s windows, adopt children, put them in daycare, take care of Grandma, buy bonds, spend more on research, purchase school supplies, go to college, invest in historic buildings, and the list goes on.

The relentless growth of credits and deductions over the past 20 years has not only knocked half of all American households off the tax rolls, it has made the IRS a super-agency, engaged in policies as unrelated as delivering welfare benefits to subsidizing the manufacture of energy efficient refrigerators. I would argue that were we starting from scratch, these would not be the functions we would want a tax collection agency to perform.

Ironically, but perhaps not surprisingly, the sectors suffering the biggest financial crises today—health care, housing, and state and local governments—all receive the most subsidies through the tax code. The cure for what ails these parties is to be weaned off the tax code, not given more subsidies through such things as the First Time Homebuyer’s Credit, Premium Assistance credits, or more tax free bonds.

While tax cuts will always curry more favor with voters than creating new spending programs, Washington needs to call a truce to using the tax code for social or economic goals. Indeed, the tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. has become so narrow that trying to accomplish more social goals via the tax code is like pushing on a string.

Washington can actually do more for the American people by doing less. The solution lies in fundamental tax reform—as has been suggested by parties as diverse as Chairman Ryan and President Obama’s National Commission on Fiscal Responsibility and Reform, chaired by Erskine Bowles and Alan Simpson. As many studies have shown, Americans could be taxed at lower rates—and the government could raise the same amount of revenue—if the majority of tax expenditures were eliminated.

That said, the primary goal of fundamental tax reform should not be raising more money for government. The primary goal should be improving the nation’s long-term economic growth and lifting American’s living standards.

Path breaking research by economists at the OECD suggests that the U.S. corporate and individual tax systems are a major detriment to our nation’s long-term economic growth. In a major study analyzing the impact of various taxes on long-term economic growth, they determined that high corporate and personal income tax rates are the most harmful taxes for long-term economic growth, followed by consumption taxes and property taxes.

Unfortunately, as many of you many know, the U.S. has the 2nd highest corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. rate among industrialized nations and, this may surprise you, the U.S. has the most progressive personal income tax systems among industrialized nations.

The economic evidence suggests that cutting our corporate and personal income tax rates while broadening the tax base would greatly improve the nation’s prospects for long-term GDP growth while helping to restore Uncle Sam’s fiscal health. More importantly, these measures will lead to higher wages and better living standards for American citizens. And that should be the number one priority of any tax policy.

Let’s consider corporate and individual tax reform one at a time.

Corporate Tax Reform Can Improve U.S. Competitiveness and Living Standards

When it comes to corporate taxes, the U.S. has a Neiman Marcus tax system while the rest of the world has moved toward a Walmart model of corporate taxation. In contrast to our high-rate, narrow base, and worldwide model of corporate taxations, the basic tenets of this new model are lower tax rates, a broader base, and the exemption of foreign earnings.

In just the past four years alone, 75 countries have cut their corporate tax rates to make themselves more competitive. And, reports the OECD, “there has been a gradual movement of countries moving from a credit [worldwide] to an exemption [territorial] system, at least in part because of the competitive edge that this can give to their resident multinational firms.”[1]

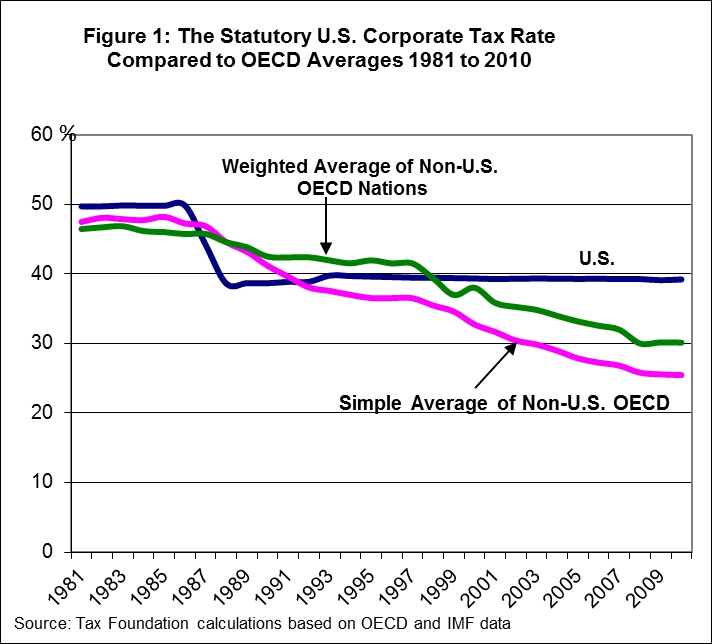

The U.S. remains far behind on both of these trends. Not only do we have the second-highest overall corporate tax rate among the leading industrialized nations at over 39 percent—only Japan has a higher overall rate—but we are one of the few remaining countries to tax on a worldwide basis.

Our largest trading partners—Canada, Great Britain, and Japan—have already taken steps to make themselves more competitive. For example, Great Britain lowered its corporate tax rate on April 1st of this year, from 28 percent to 26 percent as a first step toward the goal of having a 23 percent rate in 2014. On January 1st, Canada lowered its federal corporate tax rate from 18 percent to 16.5 percent. Next year the rate will fall to 15 percent. Japan was scheduled to cut its overall corporate rate by 5 percent until the tragic earthquake derailed the government’s legislative agenda. Japan’s move would have left the U.S. with the highest overall corporate tax rate in the industrialized world.

As important as are differences in tax rates, however, all three of these countries have effectively moved toward a territorial or exemption form of taxing the foreign profits of their multination firms. Indeed, of the 34 OECD member nations, 26 have either a full territorial system or exempt at least 95 percent of foreign earnings from repatriationTax repatriation is the process by which multinational companies bring overseas earnings back to the home country. Prior to the 2017 Tax Cuts and Jobs Act (TCJA), the U.S. tax code created major disincentives for U.S. companies to repatriate their earnings. Changes from the TCJA eliminate these disincentives. taxes. The U.S. remains the only country in the OECD with a world-wide system and a corporate rate above 30 percent.

While some critics charge that U.S. corporations pay far less than the statutory tax rate because of the plethora of credits and deductions, a review of IRS data shows that the effective U.S. tax rate for all corporations averaged 26 percent between 1994[2] and 2008. The effective U.S. tax rate varied across years, ranging from 27.5 percent in 1999 to 22.8 percent in 2008.[3]

However, these figures only account for U.S. income taxes paid on domestic profits and repatriated foreign earnings. When foreign taxes are included—U.S. corporations pay $100 billion annually in income taxes to other governments on their foreign profits—the overall tax rate on large multinationals is close to the U.S. statutory rate of 35 percent. Averaged for all corporations, the overall effective corporate tax rate is between 32.1 and 33 percent.

The benefits of making our corporate tax system on-par with the rest of the world’s systems cannot be understated.

Here are just a few of the benefits of corporate tax reform:

Cutting the U.S. corporate tax rate will help put the country on a long-term growth path. Economists at the OECD determined that the “corporate income tax is the most harmful tax for long-term economic growth” (emphasis added), not only because it increases the cost of domestic investment, but also because capital is the most mobile factor in the global economy, and thus the most sensitive to high tax rates.

Indeed, the report found that “Corporate income taxes appear to have a particularly negative impact on GDP per capita.” [4] Lowering statutory corporate tax rates, they determined, “can lead to particularly large productivity gains in firms that are dynamic and profitable, i.e. those that can make the largest contribution to GDP growth.”[5] OECD economists speculate that this could be because these are the firms that rely most heavily on retained earnings to finances their growth.[6] Higher taxes mean fewer retained earnings, which means less growth.

Cutting the corporate tax rate will lead to higher wages and living standards. In a world in which capital is extremely mobile but workers are not, most studies find that workers bear 45 percent to 75 percent of the economic burden of corporate taxes. In one such study, an economist at the Federal Reserve Bank of Kansas City used cross-country data to study the effect of corporate taxes and their interaction on the gross wages of workers. She found that “labor’s burden is more than four times the magnitude of the corporate tax revenue collected in the U.S.”[7]

According to her model, a one percentage point increase in the average corporate tax rate decreases annual gross wages by 0.9 percent. Translated to U.S. corporate tax collections and wages, this means that a $10.4 billion increase in corporate tax collections would lower overall wages by $43.5 billion.[8]

The overwhelming body of economic evidence suggests that cutting the U.S. corporate tax rate will benefit U.S. workers through higher wages, which translate into higher living standards.

Cutting the corporate tax rate will boost entrepreneurship, investment and productivity. Studies show that the corporate income tax hinders entrepreneurship, risk, and investment. Indeed, a study by Jens Arnold and Cyrille Schwellnus supports the notion that corporate taxes are “success taxes” which “fall disproportionately on firms that are contributing positively to aggregate productivity growth.”[9]

Perhaps a worrisome sign for the U.S., they found that firms in relatively profitable industries “have disproportionately lower productivity growth rates in countries with high statutory corporate tax rates.”[10] The corporate tax has the biggest impact on firms that are on the way up as opposed to those that have plateaued or are on the way down. In other words, companies that are “in the process of catching up with the technological frontier are particularly affected by corporate taxes.”[11]

A key factor for the health of the overall economy is the extent in which investment leads to new technology which, in turn, improves productivity. But, “high corporate taxes may reduce incentives for productivity-enhancing innovations by reducing their post-tax returns.”[12] Thus, if U.S. lawmakers want to increase the amount of innovation in the country, a good first step would be to cut the corporate tax rate.

Moving to a territorial system will eliminate the “lock-out” effect. A significant amount of economic research has shown that the willingness of multinational firms to bring home foreign profits is highly sensitive to the level of repatriation tax rates. A 2007 study by Foley et al., found that repatriation tax burdens induce firms to hold more cash abroad.[13] They determined that “the median firm facing above average [repatriation] rates holds 47% of its cash abroad, but the median firm facing below average rates holds only 26% of its cash abroad. This figure suggests that repatriation tax burdens increase foreign cash holdings relative to domestic cash holdings.”[14] It should be no surprise, thus, that by most accounts U.S. multinational firms are holding as much as $1 trillion in foreign earnings abroad, in part because of the high toll charge to bring the money back to the U.S.

But in a finding that should particularly worry U.S. lawmakers, Foley et al. found that “technology intensive firms appear to be particularly sensitive to repatriation tax burdens,” as well as those with “strong growth opportunities,” and those with high levels of R&D expenditures.[15] Thus, the “new economy” firms that contribute substantially to economic growth are those that are the most dissuaded from reinvesting their foreign profits back into the U.S.

Individual Tax Reform Can Boost Entrepreneurship, Productivity and Growth

President Obama has consistently called for higher tax rates on upper-income taxpayers. But the economic evidence suggests that this would be very detrimental to the country’s long-term economic growth. Indeed, OECD economists determined that high personal income taxes are second only to corporate income taxes in their harmful effects on long-term economic growth. And it will shock many Americans to learn that we already have the most progressive income tax burden among the leading industrialized nations.

What that means is that the top 10 percent of U.S. taxpayers pay a larger share of the income tax burden than do their counterparts in any other industrialized country, including traditionally “high-tax” countries such as France, Italy, and Sweden.[16] Meanwhile, because of the generosity of such preferences as the EITC and child credit, low-income Americans have the lowest income tax burden of any OECD nation.

Indeed, the study reports that while most countries rely more on cash transfers than taxes to redistribute income, the U.S. stands out as “achieving greater redistribution through the tax system than through cash transfers.”[17] Remarkably, the most recent IRS data for 2009 indicates that nearly 59 million tax filers—42 percent of all filers—had no income tax liability because of the credits and deductions in the tax code.

With deference to Warren Buffett, the share of the income tax burden borne by America’s wealthiest taxpayers has been growing steadily for more than two decades. Figure 2 compares the share of income taxes paid by the top 1 percent of taxpayers to the share paid by the bottom 90 percent of taxpayers.

The chart shows that, as of 2008, the top 1 percent of taxpayers paid 38 percent of all income taxes, while the bottom 90 percent of taxpayers paid just 30 percent of the income tax burden. By any measure, this is the sign of a very progressive taxA progressive tax is one where the average tax burden increases with income. High-income families pay a disproportionate share of the tax burden, while low- and middle-income taxpayers shoulder a relatively small tax burden. system.

What are the harmful effects of progressivity? The economic evidence is quite clear that there is a “non-trivial tradeoff between tax policies that enhance GDP per-capita and equity.”[18] Meaning, the more we try to make an income tax system progressive, the more we undermine the factors that contribute most to economic growth—investment, risk taking, entrepreneurship, and productivity.

Individual Tax Reform Must Go Hand-in-Hand with Corporate Reform. It may surprise people to learn that the corporate tax system is no longer the primary tool for which we tax businesses in America. As Figure 4 below shows, more business income is currently taxed under the individual tax system than under the traditional corporate income tax system. It is also interesting to note that for the first time in the history of the tax code the top corporate tax rate and the top individual rate are the same (35 percent). These are key reasons why the individual and corporate tax systems should be reformed together. The neutrality principle dictates that the tax code not bias the way corporate and non-corporate businesses are taxed.

There has been a tremendous growth in “flow-through” private businesses such as sole proprietors, S-corporations, LLCs, and partnerships over the past thirty years. Between 1980 and 2007, for example, the number of sole proprietors grew from 8.9 million to more than 23 million, and the number of S-corporations and partnerships (which include LLCs) grew at a faster rate from 1.9 million to more than 7 million. There are now three and one-half times as many pass-through firms as traditional C-corporations.[19]

America’s “rich” are our successful entrepreneurs and business owners. While some people dismiss the effect of high tax rates on business by citing the fact that only 2 or 3 percent of business owners pay tax in the top two brackets, the more economically relevant question is how much business income is earned by those in the top tax brackets.

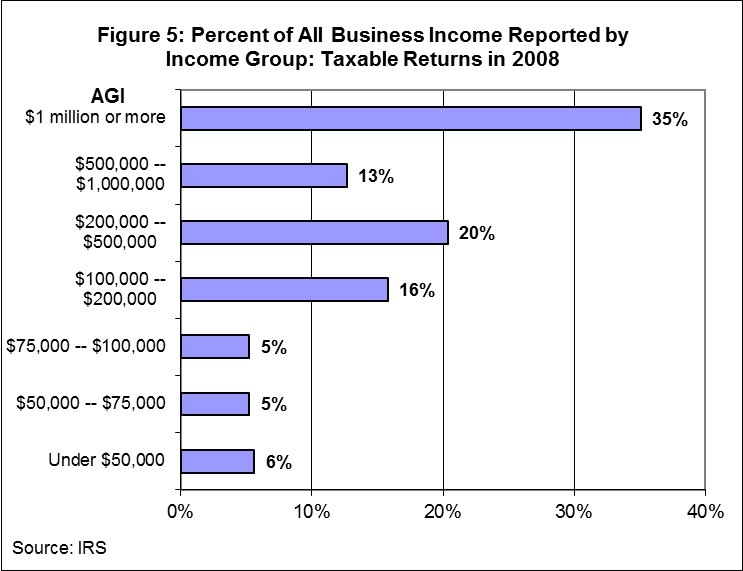

While there are millions of small businesses in America, Figure 5 shows that only about 16 percent of all private business income is earned by taxpayers with adjusted gross incomeFor individuals, gross income is the total pre-tax earnings from wages, tips, investments, interest, and other forms of income and is also referred to as “gross pay.” For businesses, gross income is total revenue minus cost of goods sold and is also known as “gross profit” or “gross margin.” (AGI) below $100,000. Another 16 percent of private business income is earned by taxpayers with AGI between $100,000 and $200,000.

However, fully 68 percent of private business income is earned by taxpayers with AGI above $200,000—the target range of President Obama’s proposed tax rate increases. Some 35 percent of all private business income is earned by taxpayers with AGIs above $1 million.

Another way of looking at the distribution of business income is to see how many taxpayers at the highest tax brackets have business income. According to Tax Policy Center estimates, more than 74 percent of tax filers in the highest tax bracketA tax bracket is the range of incomes taxed at given rates, which typically differ depending on filing status. In a progressive individual or corporate income tax system, rates rise as income increases. There are seven federal individual income tax brackets; the federal corporate income tax system is flat. report business income, compare to 20 percent of those at the lowest bracket. As Table 1 below indicates, more than 40 percent of private business income is earned by taxpayers paying the top marginal rate.

While these high-income business owners may be relatively few in number, the data makes it very clear that increasing top individual tax rates would directly impact America’s successful private business owners and entrepreneurs.

|

Table 1: Distribution of Business Income by Statutory Marginal Tax Rate, 2011 |

|||||

|

Statutory Marginal Income Tax Rate |

Number of Tax Units Reporting Business Income (Thousands) |

Percent of Total Reporting Business Income |

Percent of Bracket Reporting Business Income |

Amount of Positive Business Income (Billions) |

Percent of Total |

|

Non-filers |

981 |

2.7 |

4.9 |

$ 3.1 |

0.3 |

|

0 |

9,201 |

25.5 |

31.4 |

$ 59.5 |

6.2 |

|

10 |

4,951 |

13.7 |

19.9 |

$ 45.9 |

4.8 |

|

15 |

10,777 |

29.9 |

21.7 |

$ 113.1 |

11.8 |

|

25 |

6,180 |

17.2 |

26.2 |

$ 114.2 |

11.9 |

|

26 (AMT) |

932 |

2.6 |

46.8 |

$ 37.5 |

3.9 |

|

28 (Regular) |

1,082 |

3.0 |

36.4 |

$ 48.6 |

5.0 |

|

28 (AMT) |

1,028 |

2.9 |

59.7 |

$ 113.5 |

11.8 |

|

36 |

272 |

0.8 |

65.7 |

$ 39.0 |

4.0 |

|

39.6 |

622 |

1.7 |

74.2 |

$ 388.2 |

40.3 |

|

All |

36,026 |

100.0 |

23.2 |

$ 962.5 |

100.0 |

|

Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-5). |

Cutting Individual Tax Rates Can Boost Productivity and Economic Growth. After extensive study of the impact of tax reforms on economic growth across the largest capitalist nations, OECD researchers determined that “a reduction in the top marginal [individual] tax rate is found to raise productivity in industries with potentially high rates of enterprise creation. Thus reducing top marginal tax rates may help to enhance economy-wide productivity in OECD countries with a large share of such industries…”[20]

Indeed, OECD researchers find that lower tax rates and higher productivity gains translate into higher economic growth:

For example, consider the average OECD country in 2004, which had an average personal income tax rate of 14.3% and a marginal income tax rate of 26.5%. If the marginal tax rateThe marginal tax rate is the amount of additional tax paid for every additional dollar earned as income. The average tax rate is the total tax paid divided by total income earned. A 10 percent marginal tax rate means that 10 cents of every next dollar earned would be taken as tax. were to decrease by 5 percentage points in this situation, thus decreasing the progressivity of income taxes, the estimated increase in GDP per capita in the long run would be around 1%.[21]

With our large entrepreneurial and non-corporate sector, such studies suggest that the U.S. could see substantial productivity and GDP gains from lower personal income tax rates.

Tax reform will also reduce complexity and dead-weight costs to the economy. In its 2010 Annual Report to Congress, the National Taxpayer Advocate identified tax complexity as the most serious problem facing taxpayers and the IRS, and urged lawmakers to simplify the system.[22] It is estimated that tax compliance costs taxpayers an estimate $163 billion each year. The corporate tax system alone costs American businesses about $40 billion per year—roughly equal to the cost of hiring 800,000 workers at $50,000 each.

According to a recent Tax Foundation study, the “deadweight” costs, or excess burden, of the current individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source of tax revenue in the U.S. is not inconsequential, amounting to roughly 11 to 15 percent of total income tax revenues. This means that in the course of raising roughly $1 trillion in revenue through the individual income tax, an additional burden of $110 to $150 billion is imposed on taxpayers and the economy.[23]

One of the other ways that tax reform can lead to greater economic growth is by liberating taxpayers, businesses, and investors from these burdensome compliance and deadweight costs.

Conclusion

The U.S. tax system is in desperate need of simplification and reform. To be sure, with the deficit now topping $1.5 trillion, many lawmakers may look at eliminating tax “loopholes” and simplifying the tax code as an opportunity to raise more revenues. But increasing the share of the economy going to tax collections should not be the primary goal of tax reform. The primary goal should be to promote long-term economic growth and better living standards for the American people. If the byproduct of increased economic growth is more tax revenues, then that is a win-win.

But there is a real tension in the U.S. between the desire for a simpler tax code and one that insures fairness and equity. To be sure, tax reform that broadens the base while lowering marginal tax rates could create the appearance of giving “tax cuts for the rich,” an anathema to many.

As we move forward to overhaul the tax system, I suggest that we develop a new way of thinking about equity in the tax code. We should strive to build consensus around these basic concepts:

• An equitable tax system should be free of most credits or deductions and not micromanage individual or business behavior.

• An equitable tax system should apply a single, flat rate on most everyone equally. That way, every citizen pays at least something toward the basic cost of government.

• An equitable tax code should be simple—which would save all of us time, money and headache and would save the economy the deadweight loss of the current system.

• An equitable tax code should have dramatically lower rates than we have today—in the mid-20s by most accounts—and the government could still raise the same amount of revenues.

I believe that such a tax code would actually generate a more predictable and stable revenue stream to fund government programs as opposed to the roller coaster revenues we have today.

And, most importantly, such a tax code would be conducive to long-term economic growth, which is one of the keys to fixing the long-term fiscal crisis facing the country.

Thank you, I’m happy to answer any questions you may have.

[1] Tax Policy Reform and Economic Growth, OECD Tax Policy Studies, No. 20, OECD Publishing (2010), p. 138.

[2] This is the year the top corporate tax rate was raised from 34 percent to 35 percent.

[3] William McBride, “Beyond the Headlines: What Do Corporations Pay in Income Tax?” Tax Foundation Special Report No. 194, September 2011, p. 2.

[4] Asa Johansson, Christopher Heady, Jens Arnold, Bert Brys and Laura Vartia, “Tax and Economic Growth,” Organization for Economic Cooperation and Development, OECD Economics Working Paper No. 620., July 11, 2008. p. 43.

[6] Tax Policy Reform and Economic Growth, OECD Tax Policy Studies, No. 20, OECD Publishing (2010), p. 135.

[7] R. Alison Felix, “Passing the Burden: Corporate Tax IncidenceTax incidence is a measure of who ultimately pays a tax, either directly or through the tax burden. This burden can be split between buyers and consumers, or different groups in the economy. in Open Economies,” October 2007, p. 2.

[9] Jens Arnold and Cyrille Schwellnus, “Do Corporate Taxes Reduce Productivity and Investment at the Firm Level? Cross-Country Evidence for the Amadeus Dataset,” CEPII, Working Paper No. 2008 – 19, September 2008, p. 31. The concept of “success taxes” was first suggested by Gentry and Hubbard (2004).

[10] Arnold and Schwellnus, p. 4.

[13] C. Fritz Foley, Jay C. Hartzell, Sheridan Titman, Garry Twite, “Why Do Firms Hold So Much Cash? A Tax-Based Explanation,” February 2007, p. 3.

[16] “Growing Unequal? Income Distribution and Poverty in OECD Countries,” Organization for Economic Cooperation and Development, 2008. p. 112. http://dx.doi.org/10.1787/422013187855. Here income taxes refer to both personal and social insurance taxes.

[18] Tax Policy Reform and Economic Growth, p. 22.

[19] Scott A. Hodge, “Over One-Third of New Tax Revenue Would Come from Business Income if High-Income Personal Tax Cuts Expire,” Tax Foundation Special Report No. 185, September 2010, p. 4.

[20] “Tax and Economic Growth,” p. 9.

[22] National Taxpayer Advocate’s 2010 Annual Report to Congress.

http://www.irs.gov/advocate/article/0,,id=233846,00.html

[23] Robert C. Carroll, “The Excess Burden of Taxes and the Economic Cost of High Tax Rates,” Tax Foundation Special Report No. 170, August 14, 2009.

Share