The Earned Income Tax Credit (EITC) is a refundable tax credit targeted at low-income working families. The credit offsets tax liability, the total amount of tax debt owed by an individual, corporation, or other entity to a taxing authority like the Internal Revenue Service (IRS), and can even generate a refund, with earned income credit amounts calculated on the basis of income and number of children.

How Does the Earned Income Credit (EITC) Work?

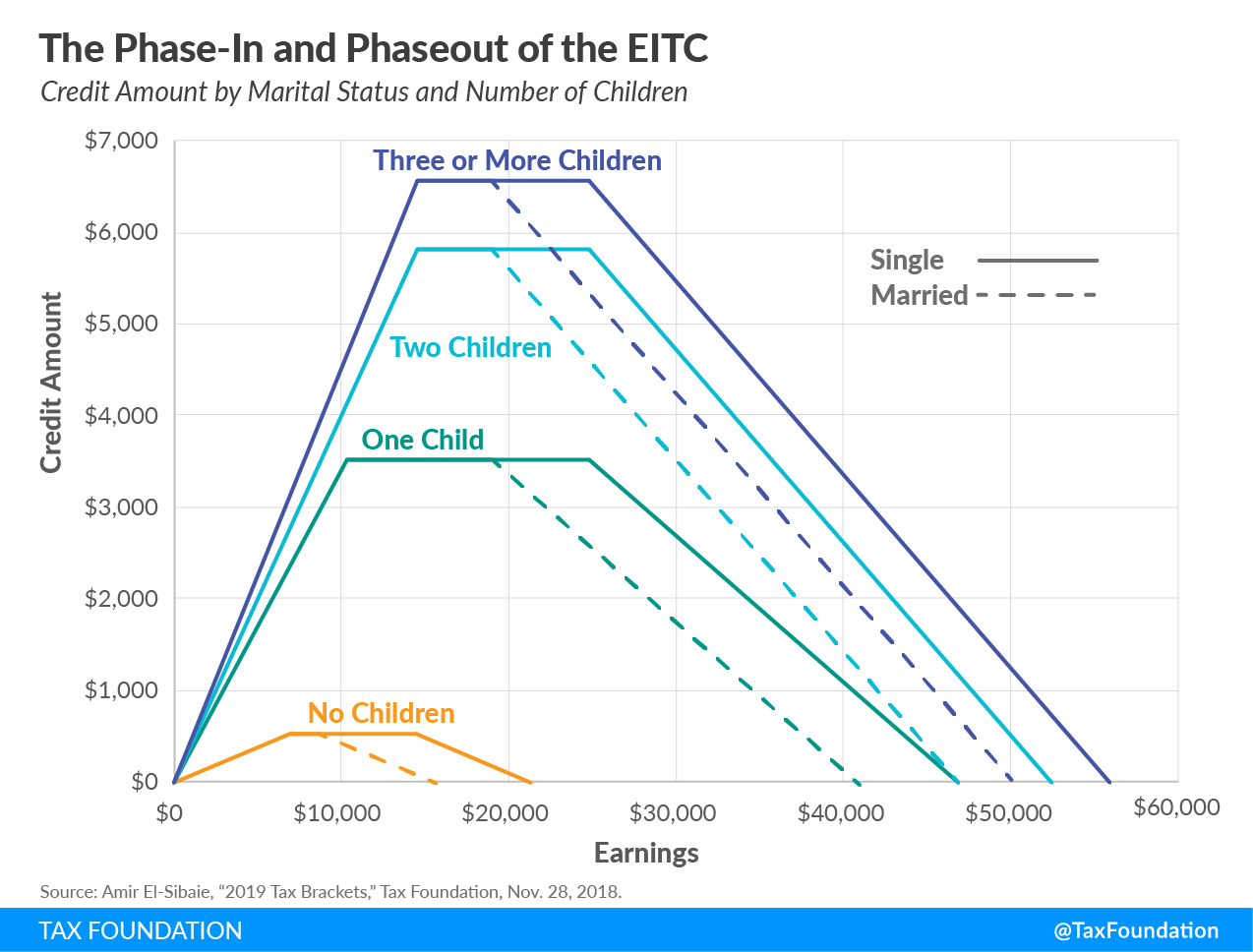

The value of the Earned Income Tax Credit (EITC) is a fixed percentage of a household’s earned income until the credit reaches its maximum. The EITC stays at its maximum value as a household’s earned income continues to increase, until earnings reach a phaseout threshold, above which the credit drops by a fixed percentage for each additional dollar of income over the phaseout threshold. The EITC is a fully refundable credit at the federal level; some, but not all, states with EITCs make their own provisions refundable as well.

The EITC’s rates and thresholds depend on a household’s filing status and number of children. Under current law, households with no children are eligible for a relatively small EITC, with a phase-in rate of 7.65 percent and a maximum credit of $503.

History of the Earned Income Credit

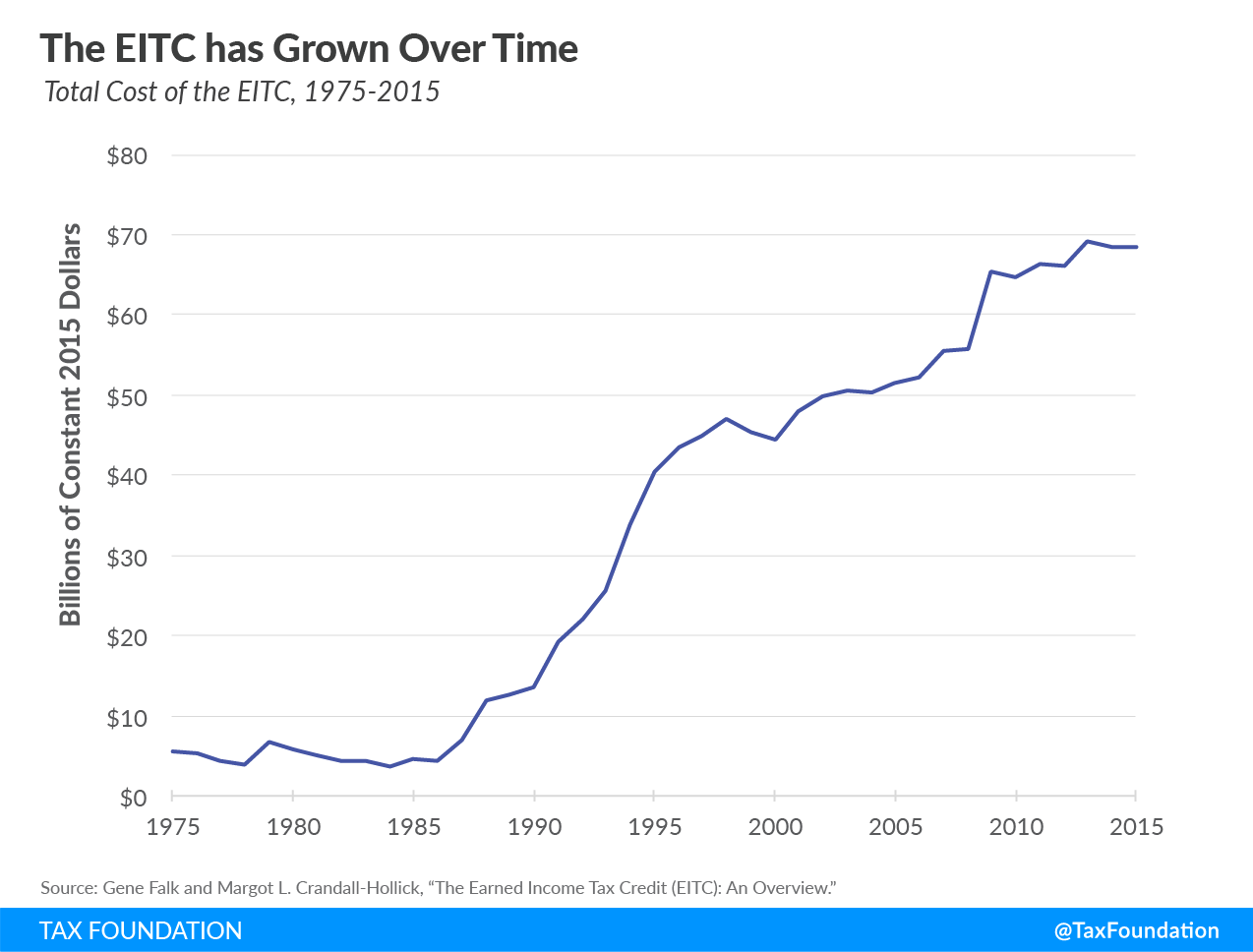

The EITC was enacted in 1975 as a temporary credit to help low-income workers with children. It was made permanent by Congress in 1978 and has since been expanded several times. The Protecting Americans from Tax Hikes (PATH) Act of 2015 made the most recent expansion of the EITC permanent.

As the following Figure illustrates, the EITC has grown considerably since its inception, from $5.5 billion in 1975 in constant 2015 dollars to $68.5 billion in 2015. Its cost rose dramatically in 1990, 1993, 2001, and 2009, years in which Congress expanded the program.

Strengths and Weaknesses

The Earned Income Tax Credit’s primary strengths are that it is well-targeted towards low-income workers and that it promotes entrance into the workforce. On the other hand, the Earned Income Tax Credit is complicated, has a high error rate, discourages work past a certain income threshold, imposes a marriage penalty, and creates disparity between workers with and without children.

Stay updated on the latest educational resources.

Level-up your tax knowledge with free educational resources—primers, glossary terms, videos, and more—delivered monthly.

Subscribe