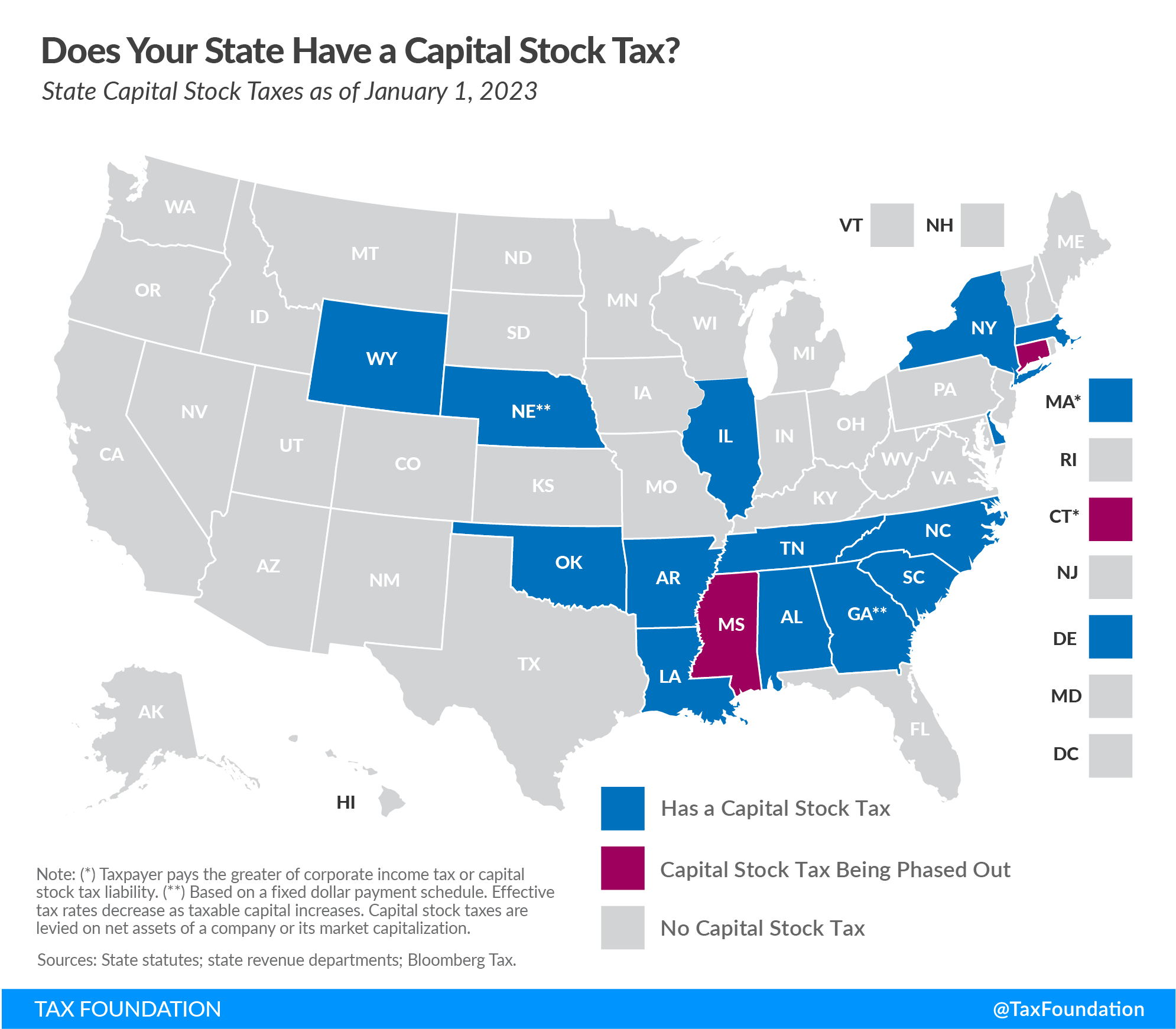

A capital stock tax is imposed on a business’s net worth (or accumulated wealth). Capital stock taxes differ from corporate income taxes which are levied on a business’s net income (or profit). Capital stock taxes penalize investment and requires businesses to pay regardless of whether they make a profit in a given year, or ever. A capital stock tax is often referred to as a franchise tax, although some states use that term for different types of taxes, as well.

Who Is Subject to These Taxes?

Capital stock taxes are usually, but not always, levied on C corporations—different states have different laws regarding the types of businesses that fall under a capital stock tax.

While exact formulas and methodologies vary from state to state, of the 16 states that have them, capital stock taxes are usually levied on a firm’s net assets, with rates ranging from a low of 0.02 percent in Wyoming to a high of 0.3 percent in Arkansas. Among the states that levy a capital stock tax, half place a cap on the maximum liability a business may be required to pay, while the other half do not.

Regardless of which entities are subject to capital stock taxes, or the formulas used to levy them, the effect is the same: they disincentivize capital accumulation.

Impact of These Taxes

As a form of corporate wealth taxation, capital stock taxes bear many of the inefficient hallmarks of an individual wealth tax, but with additional implications for the economy.

“Capital stock,” which this tax targets, includes the value of all the physical components a firm uses to generate its goods or services, minus the firm’s debt. Capital stock taxes are levied regardless of whether a business makes a profit, making them especially onerous to new businesses that have yet to turn a profit, industries with low profit margins, and to all businesses during times of economic downturn.

Taxing a company based on its net worth penalizes the firm for making additional capital investments. This disincentive results in firms that underproduce and operate below their full potentials. Purchasing additional equipment, or replacing old equipment, becomes more costly—both in terms of tax liability and tax compliance costs. Without additional capital investment, fewer workers are hired, and those that are employed are less productive. Since productivity directly influences wages, underproducing workers are also unable to realize their full earning potential. In short, the unintended consequences of capital stock taxation can have a limiting effect on the state’s economy.

Over the last 10 years, lawmakers have grown to realize the problems with capital stock taxes. As a result, four states have completely repealed their franchise taxes, and two more are in the process of phasing them out.

Federal capital stock taxes were eliminated beginning January 1, 2016.

Stay updated on the latest educational resources.

Level-up your tax knowledge with free educational resources—primers, glossary terms, videos, and more—delivered monthly.

Subscribe