All Related Articles

What’s up with Being GILTI?

The Tax Cuts and Jobs Act made significant changes to the way U.S. multinationals’ foreign profits are taxed. GILTI, or “Global Intangible Low Tax Income,” was introduced as an outbound anti-base erosion provision.

5 min read

What Happens When Everyone is GILTI?

Secretary Mnuchin, Finance Minister Le Maire, and other tax policy leaders should encourage the OECD and their own research staff to perform serious economic analysis on the alternatives for changing international tax rules before moving forward. It would be quite unfortunate for the world to learn the wrong lessons from U.S. tax reform.

3 min read

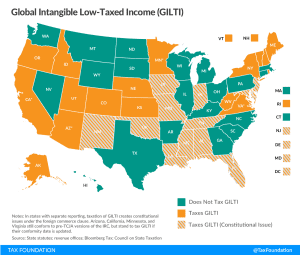

GILTI Minds: Why Some States Want to Tax International Income—And Why They Shouldn’t

The new federal tax on Global Intangible Low-Taxed Income (GILTI) is something of a misnomer: it’s certainly global and it’s definitely income, but the rest of it is, at best, an approximation. It’s not exclusively levied on low-taxed income, nor just on the economic returns from intangible property. So what is GILTI, why might states tax it, and what’s the problem with that?

8 min readToward a State of Conformity: State Tax Codes a Year After Federal Tax Reform

States incorporate provisions of the federal tax code into their own codes in varying degrees, meaning that federal tax reform has implications for state revenue beyond any broader economic effects of tax reform.

73 min read

A Hybrid Approach: The Treatment of Foreign Profits under the Tax Cuts and Jobs Act

The Tax Cuts and Jobs Act moved the U.S. toward more of a territorial corporate tax system used by most other OECD countries. However, the U.S. law contains key differences in the treatment of foreign profits.

24 min read