Fiscal Fact No. 201

This week, President Obama will cap off the White House forum on jobs and the economy with a trip to Allentown, Pennsylvania. There he will focus attention on the challenges workers are facing during these tough economic times.

Alas, the President will be misinterpreting the miseries on display in Allentown. The real lesson should be that bad taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. policy can cripple a state’s economy, and no amount of federal stimulus money can undo the damage. Pennsylvania’s job losses did not start with the most recent recessionA recession is a significant and sustained decline in the economy. Typically, a recession lasts longer than six months, but recovery from a recession can take a few years.. Indeed, the out-migration of taxpayers began more than 15 years ago in large measure because Pennsylvania’s tax system is unremittingly hostile to business.

Tax Burden: Taxes consume 11.2 percent of the state’s income, which gives Pennsylvania the 11th highest state and local tax burden in the nation.

Business Tax Climate: Pennsylvania ranks 27th on the Tax Foundation’s 2010 State Business Tax Climate Index which measures the business-friendliness of each state’s tax system. Of the five major components of this index, Pennsylvania’s corporate system ranks 37th and its property/wealth taxA wealth tax is imposed on an individual’s net wealth, or the market value of their total owned assets minus liabilities. A wealth tax can be narrowly or widely defined, and depending on the definition of wealth, the base for a wealth tax can vary. system ranks 42nd. The only bright spot in the state’s tax climate is its individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source system which ranks 13th overall.

Corporate Tax Rates: Pennsylvania’s 9.99 percent corporate tax rate is the second-highest statutory rate among the 50 states; only Iowa’s 12 percent rate is higher. However, when federal deductibility is accounted for, Pennsylvania’s rate is the highest in the nation. If Pennsylvania were a nation, it would have the highest overall corporate tax rate in the world at 41.5 percent (federal plus state, accounting for the state-local deduction).

Capital Taxes on Businesses: In addition to paying the highest corporate tax rate in the nation, Pennsylvania businesses also pay one of the highest capital stock taxes in the nation at 0.290 percent. Pennsylvania is also among only 10 states to impose an intangible property taxA property tax is primarily levied on immovable property like land and buildings, as well as on tangible personal property that is movable, like vehicles and equipment. Property taxes are the single largest source of state and local revenue in the U.S. and help fund schools, roads, police, and other services. on businesses.

Estate Taxes: Pennsylvania is one of 16 states to have decoupled from the phase-out of the federal estate taxAn estate tax is imposed on the net value of an individual’s taxable estate, after any exclusions or credits, at the time of death. The tax is paid by the estate itself before assets are distributed to heirs., which means it still imposes its own estate tax. It is also one of only four states to have both an estate tax and an inheritance taxAn inheritance tax is levied upon the value of inherited assets received by a beneficiary after a decedent’s death. Not to be confused with estate taxes, which are paid by the decedent’s estate based on the size of the total estate before assets are distributed, inheritance taxes are paid by the recipient or heir based on the value of the bequest received..

It is not surprising, therefore, that Pennsylvania has been losing businesses and people to more tax-friendly states. As Tax Foundation analysis of IRS migration data indicates, this out-migration is not only impacting Pennsylvania’s population, it is also impacting the state’s tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates..

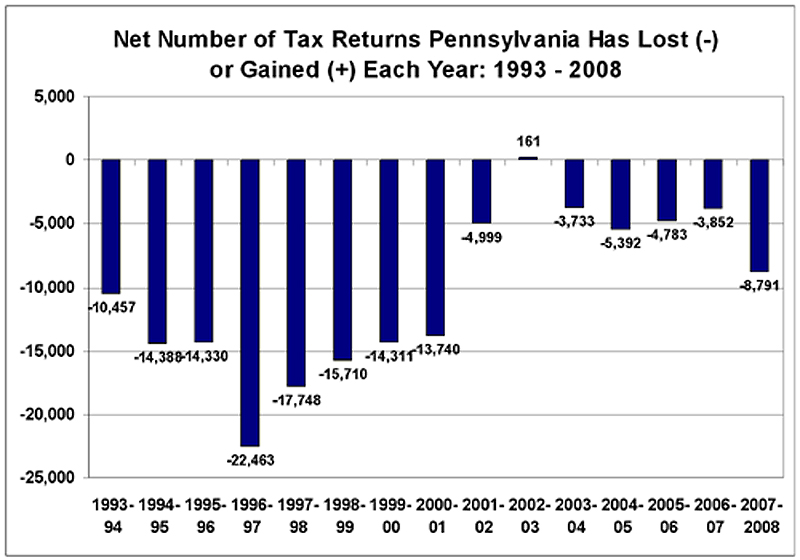

Chart 1 shows the net number of tax returns Pennsylvania lost or gained between 1993 and 2008. In every year but one, 2002 to 2003, the state saw more taxpayers leave the state than move into it. Clearly, the largest losses occurred between 1993 and 2000, an average of more than 15,000 per year. Since then, the state has been losing an average of nearly 3,800 taxpayers per year on net.

Chart 1

But as Chart 2 shows, the loss of taxpayers also means that the state is losing their incomes to other states which, in turn, means that the state’s economy and tax base are shrinking. Between 1993 and 2008, Pennsylvania lost on-net $9.7 billion in adjusted gross incomeFor individuals, gross income is the total of all income received from any source before taxes or deductions. It includes wages, salaries, tips, interest, dividends, capital gains, rental income, alimony, pensions, and other forms of income. For businesses, gross income (or gross profit) is the sum of total receipts or sales minus the cost of goods sold (COGS)—the direct costs of producing goods to outmigration. Even in the 2002-2003 period, where the state gained slightly more taxpayers than it lost, it still lost AGI overall because the people who left the state earned more than the new people who entered the state.

Chart 2

Recent Census data gives us an insight into who is moving into Pennsylvania compared to who is moving out. First, it is interesting to note that in contrast to the IRS data that shows a net outflow of tax returns, the Census data for 2007 to 2008 shows a net inflow of roughly 9,500 new people moving into the state.

One reason IRS and Census data frequently don’t match is that a single tax return may represent one person, a married couple, or an entire family. So it is possible that the tax returns moving into the state have more dependents than the tax returns moving out of the state. Another reason IRS and Census data don’t match is that Census data accounts for people who don’t file a tax return, including college-aged students and retirees.

The migration figures by age show that Pennsylvania is gaining young people (under age 19) and young families (ages 25 to 44) and retirees over age 65. But the state is losing college graduates (ages 20 to 24) and people in their peak earnings years (ages 45 to 64).

But the real warning signs for the state are seen in the education and income figures. Pennsylvania is gaining people who have little or no income and less than a college degree (college students mainly) but losing people at all other income levels and those who have a college degree or better.

|

Pennsylvania |

People Moving into Pennsylvania |

People Moving out of Pennsylvania |

Net # People Moving into Pennsylvania from 2007 to 2008 |

Ratio of People Coming to Going |

|

Total |

237,766 |

228,246 |

9,520 |

1.04 |

|

By Age Group |

||||

|

Under 18 |

41,701 |

39,716 |

1,985 |

1.05 |

|

Aged 18-19 |

30,565 |

20,335 |

10,230 |

1.5 |

|

Aged 20-24 |

41,584 |

43,785 |

-2,201 |

0.95 |

|

Aged 25-34 |

52,600 |

48,765 |

3,835 |

1.08 |

|

Aged 35-44 |

30,168 |

27,344 |

2,824 |

1.1 |

|

Aged 45-54 |

17,052 |

20,753 |

-3,701 |

0.82 |

|

Aged 55-64 |

10,270 |

14,011 |

-3,741 |

0.73 |

|

Aged 65+ |

13,826 |

13,537 |

289 |

1.02 |

|

By Educational Attainment |

||||

|

Less than H.S. Diploma |

14,183 |

10,113 |

4,070 |

1.4 |

|

High School Graduate |

28,698 |

27,337 |

1,361 |

1.05 |

|

Some college or Associates degree |

29,350 |

30,399 |

-1,049 |

0.97 |

|

Bachelor’s Degree |

29,796 |

31,629 |

-1,833 |

0.94 |

|

Graduate or Professional Degree |

21,889 |

24,932 |

-3,043 |

0.88 |

|

By Individual Income |

||||

|

No Income |

26,976 |

18,761 |

8,215 |

1.44 |

|

$1-$9,999 |

61,112 |

51,265 |

9,847 |

1.19 |

|

$10,000-$24,999 |

40,585 |

42,911 |

-2,326 |

0.95 |

|

$25,000-$49,999 |

39,043 |

43,165 |

-4,122 |

0.9 |

|

$50,000-$74,999 |

17,476 |

18,362 |

-886 |

0.95 |

|

$75,000+ |

16,471 |

19,110 |

-2,639 |

0.86 |

|

Source: Tax Foundation, based on Census data |

Conclusion

There are many reasons behind the migration of Americans between states, and taxes are just one. But taxes can clearly create a hostile environment for business investment and job creation and Pennsylvania appears to be a prime example of that.

It would be easy to blame “the weak economy” for the hard times that have befallen the people of Allentown and the state of Pennsylvania. But the migration of taxpayers and their incomes out of the state has been going on for more than 15 years and the one constant has been the state’s tax system. These trends will likely continue long after the national economy recovers unless state lawmakers overhaul their business tax system.

Share this article