Fiscal Fact No. 250

Introduction

On December 31, 2010, a decade’s worth of taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. code changes will expire. Most pundits have been predicting for months that Congress and the President would only permit the expiration of tax cuts for high-income people, but if election year politics create gridlock, the Internal Revenue Service will be ready to roll the clock back ten years.

Most of the changes will kick in because of the sunset provisions of the 2001 and 2003 laws, known popularly as the Bush tax cuts. But other, more recently enacted tax cuts—temporary tax provisions passed in early 2009 as part of the stimulus bill—are scheduled to expire at the same time. Both sets of changes would have substantial effects on low-income taxpayers.

While many people view the Bush tax cuts as targeted towards the wealthy, taxpayers across the entire income spectrum received a significant tax cut. It’s certainly true that wealthier taxpayers received a bigger cut as measured in dollars because they were paying higher taxes to begin with. However, a better measure of tax cuts is the percentage change in after-tax incomeAfter-tax income is the net amount of income available to invest, save, or consume after federal, state, and withholding taxes have been applied—your disposable income. Companies and, to a lesser extent, individuals, make economic decisions in light of how they can best maximize their earnings., which reflects tangible lifestyle benefits and is intuitively understood.

Comparing changes in after-tax income shows that the benefits of the tax cuts were distributed much more equally along the income spectrum because the Bush tax cuts included a number of provisions targeted specifically at low-income people. Moreover, low-income taxpayers also benefitted from some temporary stimulus measures enacted in 2009 that are also set to expire at the end of this year: an expansion of the earned income tax creditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income rather than the taxpayer’s tax bill directly. (EITC) and the child tax credit, as well as expanded credits for college education.

The various tax proposals made by the parties in Washington all extend most of these low-income tax cuts. However, the current Congress has shown itself to be unusually susceptible to gridlock. No vote will occur before the midterm elections, and although both parties plan to address the matter during a lame duck session after the election, there’s no certainty of legislative agreement then, either. Therefore, the threat of automatic, full expiration of all these cuts is quite real, and with that in mind, it is worth considering what effect such a scenario would have on low-income taxpayers, as well as the differences between the various proposals to extend most of the tax cuts.

Expiring Provisions Important to Low-Income Workers

Earned Income Tax Credit

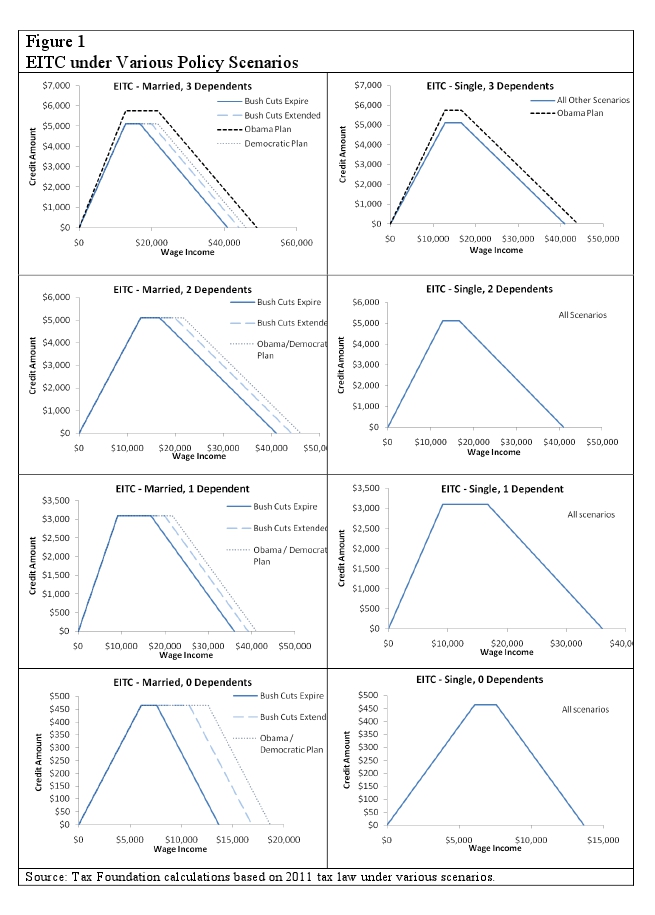

The EITC is a sizeable tax credit for the working poor, designed as an anti-poverty measure. Workers with wage income within a certain range and limited investment income are eligible. The credit is also “refundable,” which means that workers whose tax liability has been reduced to zero before the credit receive the value of the credit in the form of a check. Technically, those checks are not refunded tax payments; in the U.S. Budget, these payments count as government expenditures similar to transfer programs like TANF (i.e., the traditional “welfare” program). For many recipients, the credit amount exceeds their income tax liability considerably.

The EITC is probably one of the most complicated provisions of the tax code due to its “plateau” shape. The value of the credit rises as wage income increases until it reaches an amount at which a larger dollar amount of assistance is deemed unnecessary—this is the edge of the plateau. For several thousands of dollars of additional wage income, the credit is constant. When the worker reaches an income level at which the maximum credit is considered unnecessary, he has reached the far end of the plateau, and the credit starts to decline. When wage income increases beyond another threshold, the credit falls to zero. The exact shape of this plateau depends on both filing status and the number of dependents on the return.

Prior to the Bush tax cuts, the credit amounts were the same for both single and married filers. This was one component of the “marriage penaltyA marriage penalty is when a household’s overall tax bill increases due to a couple marrying and filing taxes jointly. A marriage penalty typically occurs when two individuals with similar incomes marry; this is true for both high- and low-income couples.,” because if two single EITC recipients married, their combined income would often be enough to make them ineligible to receive the credit. The Bush cuts mitigated this by lengthening the plateau—that is, by increasing the income threshold at which the credit starts to phase out for married filers.

The 2009 stimulus bill expanded the EITC further in two ways. In the same way Bush had, Obama increased the phase-out threshold for married filers. Secondly, the stimulus bill added a new, more generous EITC category for tax returns claiming three or more dependent children. Previously, a family with two children could get the largest credit, and the birth of a third child did not increase it.

The current Republican proposal is to extend all of the Bush tax cuts without extending any stimulus bill provisions. Congressional Democrats extend both the Bush EITC expansion and some of the stimulus provisions. They include the additional marriage penalty relief, but not the new EITC category for three children. Obama’s budget proposal goes the furthest, including even the three-children EITC category.

Child Tax Credit

Prior to the Bush tax cuts of 2001 and 2003, most taxpayers could receive a tax credit worth $500 for each qualifying child they claimed as a dependent. This credit benefits low- and middle-income people because it starts to phase out once income exceeds a certain threshold ($110,000 for couples, $75,000 for single parents). The Bush tax cuts doubled the credit amount to $1,000 per child.

While the credit was refundable prior to the Bush tax cuts, the refund (that is, the amount that the credit reduced the filer’s income tax burden below zero) was capped by the amount of payroll taxes paid, and only applied to returns with three or more children. The Bush tax cuts eliminated the three-child requirement and changed the law so that the cap no longer depended on payroll taxes but instead was set at 15 percent of the worker’s income in excess of $12,800. The 2009 stimulus bill lowered this threshold to $3,000, expanding the refundable credit further. Both the Obama budget proposal and the congressional Democrats’ plan would extend this lower threshold into 2011.

|

Table 1 |

||||

|

If Bush Cuts Expire |

If Bush Cuts Are Extended |

If Obama Budget Adopted |

If Cong. Democrats’ Plan Adopted |

|

|

Credit Amount |

$500 per child |

$1,000 per child |

$1,000 per child |

$1,000 per child |

|

Refundable Cap |

Payroll taxes paid |

15% of AGI over $12,800 |

15% of AGI over $3,000 |

15% of AGI over $3,000 |

Making-Work-Pay Credit

The broadest tax-cutting measure in the 2009 stimulus bill was the introduction of a new, refundable tax creditA refundable tax credit can be used to generate a federal tax refund larger than the amount of tax paid throughout the year. In other words, a refundable tax credit creates the possibility of a negative federal tax liability. An example of a refundable tax credit is the Earned Income Tax Credit (EITC). called the making-work-pay credit, equal to 6.2 percent of the taxpayer’s wage income, up to a maximum of $400 ($800 for joint returns). The credit phases out as income rises above $75,000 (or $150,000 for joint married returns), so this is a provision that benefits low- and middle-income people. The credit is set to expire at the end of 2010, and aside from Obama’s budget proposal, none of the plans currently under consideration calls for extending this credit into 2011.

Education Credits

There are several ways taxpayers who pay college tuition expenses can reduce their income tax liabilities. Lower-income taxpayers are better off claiming an education credit instead of deducting expenses. At higher incomes, it is usually more advantageous to deduct tuition expenses from gross incomeFor individuals, gross income is the total of all income received from any source before taxes or deductions. It includes wages, salaries, tips, interest, dividends, capital gains, rental income, alimony, pensions, and other forms of income. For businesses, gross income (or gross profit) is the sum of total receipts or sales minus the cost of goods sold (COGS)—the direct costs of producing goods, because like many other tax credits, education credits phase out once income rises above a defined threshold.

The best-known education credit was the Hope credit and was worth up to $1,800 per student, determined according to a formula that depended on total tuition expenses. The 2009 stimulus bill essentially replaced the Hope credit with the new American Opportunity credit (AOC), which has a much higher phase-out threshold, so it benefits most middle- and upper-middle-income taxpayers as well. It is worth more, too, up to $2,500 per student. Additionally, the new credit is partially refundable, whereas the Hope credit was limited by the amount of total income tax owed. The AOC will expire at the end of 2010, and Obama’s budget proposal is the only tax plan that calls for its extension into 2011.

|

Table 2 |

||||

|

Hope Credit If Bush Cuts Expire |

Hope Credit |

American Opportunity Credit* If Obama Budget Adopted |

Hope Credit |

|

|

Max Credit Amount |

$1,800 |

$1,800 |

$2,500 |

$1,800 |

|

Refundable? |

No |

No |

Up to 40% |

No |

|

* Under President Obama’s Budget, the Hope credit would still exist in law, but taxpayers would only be allowed to take either the Hope credit or the new American Opportunity credit, the latter being more generous in almost all circumstances. |

10-Percent Tax Bracket

The biggest single tax cut among all the provisions in the Bush tax cuts was the introduction of a new low tax rate on the first $6,000 in income ($8,500 in 2011 dollars). Previously, taxable incomeTaxable income is the amount of income subject to tax, after deductions and exemptions. Taxable income differs from—and is less than—gross income. up to $27,950 ($34,500 in 2011 dollars) fell into the 15-percent bracket. The Bush cuts split this bracket into two, and set a rate of 10 percent on the lowest bracket. This provision affected all taxpayers; even billionaires saw a small savings because their first $6,000 in income was taxed at the lower rate. However, the change had the biggest effect on low-income earners from a percentage standpoint. This new tax bracket, along with the rest of the Bush tax cuts, is set to expire next year. All the current proposals call for extending this provision. Only if the Bush tax cuts expire on schedule with no legislative intervention would the 10-percent bracket disappear.

Standard DeductionThe standard deduction reduces a taxpayer’s taxable income by a set amount determined by the government. Taxpayers who take the standard deduction cannot also itemize their deductions; it serves as an alternative. Marriage Penalty

Taxpayers are allowed to subtract a variety of expenses from their taxable income, saving quite a bit on their federal tax returns: interest on loans, state-local tax payments, charitable gifts—the list goes on and on. The process of claiming these deductions is called itemizing, and because low-income people don’t have many of these expenses, itemizing mainly helps higher-income taxpayers. However, for lower-income taxpayers, a “standard” deduction is available. It acts as a proxy for itemized deductions.

Prior to the Bush tax cuts, the standard deduction for married joint returns was less than twice the standard deduction for single returns. This was another component of the “marriage penalty,” because two newly married filers who had previously both claimed the single standard deduction found that their new combined deduction was less than the sum of their individual deductions. The Bush tax cuts changed the law so that the standard deduction for married joint returns was exactly twice the deduction for single returns.

Percentage Change in Take-Home Income for Various Taxpayers

To demonstrate the effects of the expiring provisions, consider the change in after-tax income for two lower-income tax returns (see Table 3). A family of four with $40,000 in income will see its after-tax income rise between 6.8 percent and 9.8 percent if tax cuts are extended, depending on which version becomes law. A single-parent family of three with $20,000 in income would see similar gains: between 4.4 percent and 9.7 percent gains in after-tax income.

| Table 3 Effects of Various Proposals on Sample Low-Income Tax Returns Tax Year 2011 |

||||

| Married Couple, 2 Dependent Children, $40K Income | ||||

| Tax Calculation | If Bush Cuts Expire | If Bush Cuts Are Extended | If Obama Budget Adopted | If Cong. Democrats’ Plan Adopted |

| Pre-Tax Income | $40,000.00 | $40,000.00 | $40,000.00 | $40,000.00 |

| Taxable Income | $15,550.00 | $13,600.00 | $13,600.00 | $13,600.00 |

| Tax Before Credits | $2,333.00 | $1,360.00 | $1,360.00 | $1,360.00 |

| Child Tax Credit | -$1,000.00 | -$2,000.00 | -$2,000.00 | -$2,000.00 |

| Making Work Pay | $0.00 | $0.00 | -$800.00 | $0.00 |

| EITC | -$203.00 | -$873.00 | -$1,256.00 | -$1,256.00 |

| Total Income Tax | $1,130.00 | -$1,513.00 | -$2,696.00 | -$1,896.00 |

| After-Tax Income | $38,870.00 | $41,513.00 | $42,696.00 | $41,896.00 |

| Change in After-Tax Income | 0% (baseline) | 6.8% | 9.8% | 7.8% |

| Single parent, 2 Dependent Children, $20K Income | ||||

| Tax Calculation | If Bush Cuts Expire | If Bush Cuts Are Extended | If Obama Budget Adopted | If Cong. Democrats’ Plan Adopted |

| Pre-Tax Income | $20,000.00 | $20,000.00 | $20,000.00 | $20,000.00 |

| Taxable Income | $400.00 | $400.00 | $400.00 | $400.00 |

| Tax Before Credits | $60.00 | $40.00 | $40.00 | $40.00 |

| Child Tax Credit | -$60.00 | -$1,120.00 | -$2,000.00 | -$2,000.00 |

| Making Work Pay | $0.00 | $0.00 | -$400.00 | $0.00 |

| EITC | -$4,415.00 | -$4,415.00 | -$4,415.00 | -$4,415.00 |

| Total Income Tax | -$4,415.00 | -$5,495.00 | -$6,775.00 | -$6,375.00 |

| After-Tax Income | $24,415.00 | $25,495.00 | $26,775.00 | $26,375.00 |

| Change in After-Tax Income | 0% (baseline) | 4.4% | 9.7% | 8.0% |

For comparison, let us consider an example on the opposite end of the income spectrum (see Table 4). A family of four with $1 million in income would see its after-tax income rise as much as 6.7 percent or drop as much as 1.3 percent, depending on which version of extension becomes law.

If the Republican version of extension—full extension of the Bush-era laws but not the credits included in 2009’s stimulus bill—becomes law, the two tax returns whose after-tax income would increase the most in 2011 are the low-income, two-parent family (6.8 percent) and the high-income family (6.7 percent).

If the Obama budget or the congressional Democrats’ plan becomes law, a substantial additional benefit from stimulus provisions for low-income families would bump up the gains in after-tax income of both low-income tax returns: to as much as 9.7 percent for the single-parent family of three and 9.8 percent for the low-earning family of four.

| Table 4 Effects of Various Proposals on a Sample High-Income Tax Return Tax Year 2011 |

||||

| Married Couple, 2 Dependent Children, $1 Million in Income | ||||

| Tax Calculation | If Bush Cuts Expire | If Bush Cuts Are Extended | If Obama Budget Adopted | If Congressional Democrats’ Plan Adopted |

| Pre-Tax Income | $1,000,000 | $1,000,000 | $1,000,000 | $1,000,000 |

| Taxable Income* | $844,914 | $805,200 | $842,376 | $842,376 |

| Tax Before Credits | $298,646 | $251,692 | $307,473 | $290,331 |

| Tax Credits (all) | $0 | $0 | $0 | $0 |

| Total Income Tax | $298,646 | $251,692 | $307,743 | $290,331 |

| After-Tax Income | $701,354 | $748,308 | $692,257 | $709,669 |

| Change in After-Tax Income | 0% (baseline) | 6.70% | -1.30% | 1.20% |

| *We assume itemized deductions equal to 18 percent of adjusted gross income. |

In summary, low-income and high-income families alike have significant tax payments at stake over the next two months.

About these Numbers

These calculations are based on the Tax Foundation’s projected 2011 tax bracket levels, which are calculated by the IRS according to inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spendin statistics from the Bureau of Labor Statistics (BLS). While the IRS has not officially released tax bracketsA tax bracket is the range of incomes taxed at given rates, which typically differ depending on filing status. In a progressive individual or corporate income tax system, rates rise as income increases. There are seven federal individual income tax brackets; the federal corporate income tax system is flat. for 2011 due to uncertainty about tax law changes, we use their formula to calculate bracket levels for many possible policy scenarios.

Note: To plug in your own example to see how a hypothetical family of your choosing, would fair under these alternative policy scenarios (as opposed to our three chosen examples above), visit the Tax Foundaton’s MyTaxBurden.org calculator.

Share this article