When countries consider changing their taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. policies, sometimes they choose to make broad reforms and other times more narrowly targeted reforms. Recently, the Polish government proposed to lower taxes on workers under the age of 26, and on August 1, the targeted tax cut for young citizens went into effect. Lawmakers hope that the policy can slow the emigration of young and skilled workers to Western European countries. However, the policy produces incentives that may counteract its primary long-term goal.

Under the new policy, individuals under 26 will effectively face a separate income tax system. Those earning below 85,528 zloty are exempt from the tax, and those earning 85,528 zloty or more will experience the same rates as individuals older than 26. (The current exchange rate between the U.S. dollar and the Polish zloty is $1=3.88 Polish zloty.) Those 26 and older will not face any changes.

|

Source: “Personal Income Tax (PIT),” Polish Investment & Trade Agency, https://www.paih.gov.pl/polish_law/taxation/pit. |

||

| Taxable Income (PLN) | Rate | Reduction (PLN) |

|---|---|---|

| 0 – 8000 | 18% | 1440 |

| 8000 – 13,000 | Between 1440 and 556.02 | |

| 13,000 – 85,528 | 556.02 | |

| 85,528 – 127,000 | 15,395.04 PLN + 32% of surplus over 85,528 | Between 556.02 and 0 |

| Over 127,000 | 0 |

|

Source: “Zerowy PIT dla młodych już od sierpnia 2019 r.,” Ministerstwo Finansów, https://www.gov.pl/web/finanse/zerowy-pit-dla-mlodych-juz-od-sierpnia-2019-r |

||

| Taxable Income (PLN) | Rate | Reduction (PLN) |

|---|---|---|

| 0 – 85,528 | 0% | |

| 85,528 – 127,000 | 32% of surplus over 85,528 | Between 556.02 and 0 |

| Over 127,000 | 0 | |

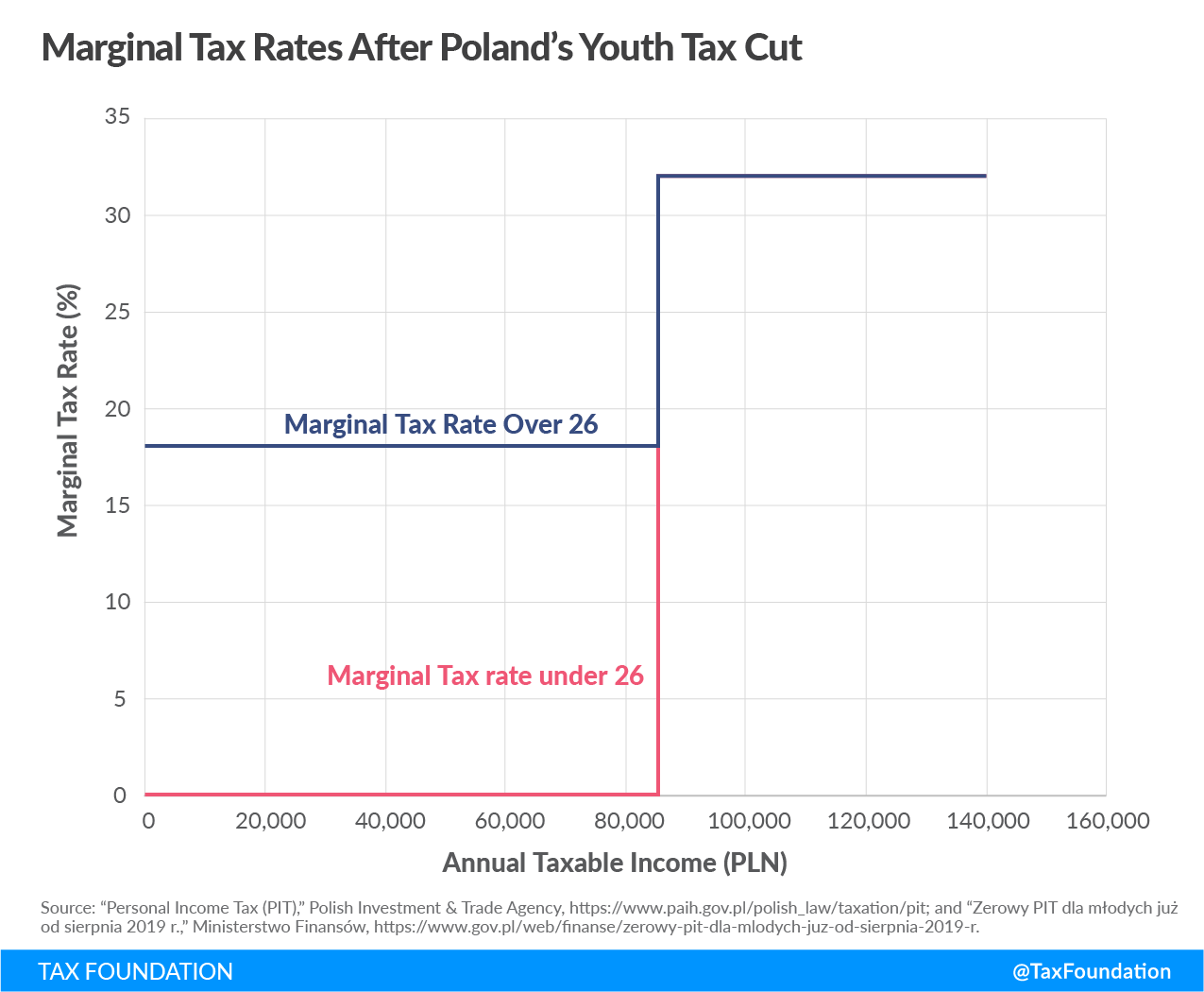

This tax cut might provide an adequate incentive for some young people to stay in Poland rather than seek employment abroad. However, the sharp transition into the standard rates creates perverse incentives for those who earn out or inevitably age out of qualifying for the tax break.

Those who age out of the tax cut would immediately experience a minimum 18 percentage-point increase in their marginal income tax rate. Individuals whose additional earnings would disqualify them from the tax cut would also face a high marginal tax rateThe marginal tax rate is the amount of additional tax paid for every additional dollar earned as income. The average tax rate is the total tax paid divided by total income earned. A 10 percent marginal tax rate means that 10 cents of every next dollar earned would be taken as tax. increase, as illustrated in the graph below. For example, an individual currently earning 85,528PLN (eligible for the tax cut) would face an increase in their marginal tax rate of 32 percentage points on their next zloty of income. Overall, depending on job prospects and tax burdens elsewhere, the policy can create an incentive to stay in Poland just until turning 26 or earning more than 85,528 PLN. Overall, the result is a guaranteed reduction in Poland’s tax base.

Poland ranked 33rd on our 2018 International Tax Competitiveness Index.

Instead of narrowly targeting tax cuts to distort behavior, Poland should work to create a more neutral and competitive tax system that can support the economic opportunity its young people desire and make Poland more friendly to business and workers. This policy, however, produces too many incentives that are counterproductive to the country’s long-term goals.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

Subscribe