Key Findings

- 100 percent bonus depreciation allows firms an immediate tax deductionA tax deduction allows taxpayers to subtract certain deductible expenses and other items to reduce how much of their income is taxed, which reduces how much tax they owe. For individuals, some deductions are available to all taxpayers, while others are reserved only for taxpayers who itemize. For businesses, most business expenses are fully and immediately deductible in the year they occur, but ot for investments in qualifying short-lived assets. The phaseout of 100 percent bonus depreciationBonus depreciation allows firms to deduct a larger portion of certain “short-lived” investments in new or improved technology, equipment, or buildings in the first year. Allowing businesses to write off more investments partially alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs., scheduled to take place after the end of 2022, will increase the after-taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. cost of investment in the United States.

- Preventing the phaseout and making 100 percent bonus depreciation a permanent feature of the U.S. tax code is crucial in the effort to increase business investment and create better opportunities for workers. Research indicates past instances of bonus depreciation have boosted capital accumulation and employment opportunities.

- Permanent 100 percent bonus depreciation would increase long-run economic output by 0.4 percent, the capital stock by 0.7 percent, and employment by 73,000 full-time equivalent jobs. Over the 10-year budget window, permanent bonus depreciation would reduce federal revenue by $400 billion.

- A permanent expansion of 100 percent bonus depreciation would support business investment, capital formation, and economic output over the long term while creating more opportunities for workers.

Table of Contents

- Introduction

- Background

- 100 Percent Bonus Depreciation and The Tax Cuts and Jobs Act

- Capital Investment and Workers

- Take-up and the Issue of NOLs

- Interactions with Global Minimum Tax and the Inflation Reduction Act

- Interactions with Limitation on Net Business Interest Expense

- Economic, Revenue, and Distributional Impact of Permanent 100 Percent Bonus Depreciation

- Conclusion

Introduction

Capital investment is critical for economic growth, and ultimately, capital investment benefits workers. Capital ranges from the simple, such as a hammer, to the complex, such as a semiconductor foundry. In general, more capital leads to more opportunities for workers. The existing U.S. tax code, however, is biased against capital investment and the bias is scheduled to worsen over the next decade.

The phaseout of 100 percent bonus depreciation, scheduled to take place after the end of 2022, will increase the cost of investment in the United States. Allowing the phaseout to occur will discourage otherwise productive domestic investment, creating an impediment to productivity-enhancing investment and opportunities for businesses and workers in the United States. Preventing the phaseout and making 100 percent bonus depreciation a permanent feature of the U.S. tax code is crucial in the effort to increase business investment and create better opportunities for workers.

In the following sections, we discuss the importance of 100 percent bonus depreciation for investment and employment, as well as interaction issues with other features of the tax code. Then we use the Tax Foundation General Equilibrium Model to estimate the economic, revenue, and distributional effects of permanent 100 percent bonus depreciation.

Background

Businesses determine their profits by subtracting costs from revenue. But for the purposes of calculating taxable income, the tax code does not treat capital costs the same as other ordinary business costs such as paying utility bills or workers’ wages. Instead, depreciationDepreciation is a measurement of the “useful life” of a business asset, such as machinery or a factory, to determine the multiyear period over which the cost of that asset can be deducted from taxable income. Instead of allowing businesses to deduct the cost of investments immediately (i.e., full expensing), depreciation requires deductions to be taken over time, reducing their value and disco schedules specify how different types of assets can be deducted over time.

For example, if a business purchases a $100 piece of manufacturing equipment, it will deduct the cost of the equipment in nominal terms over its assigned recovery period. If deductions are not permitted immediately, inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spendin and the time value of money erode the value of the deductions for the equipment in real terms over time. The present value of depreciation deductions, discounted to reflect inflation and a real rate of return, affects the cost of capital and thus affects investment decisions.[1]

Delayed deductions discourage businesses from making capital investments because they are unable to fully recover their costs. The Modified Accelerated Cost Recovery System (MACRS) details recovery periods of 3, 5, 7, 10, 20, 27.5, and 39 years depending on the type of property purchased. Since 2001, short-lived investment (recovery period of 20 years or less) has been eligible for different iterations of temporary bonus depreciation, which allows a certain percentage of the capital cost to be deducted in the first year and the remaining percentage to be deducted according to its regular recovery period (see Table 1).

| Act | Depreciation Percentage* | Effective Dates |

|---|---|---|

| Job Creation and Worker Assistance Act of 2002 | 30% | Sept. 12, 2001 – Dec. 31, 2004 |

| Jobs and Growth Tax Relief Reconciliation Act | 50% | May 5, 2003 – Jan. 1, 2006 |

| Economic Stimulus Act of 2008 | 50% | 2008 |

| American Recovery and Reinvestment Act of 2009 | 50% | 2009 |

| Small Business Jobs Act of 2010 | 50% | 2010 |

| Tax Relief, Unemployment Compensation Reauthorization, and Job Creation Act of 2010 | 100% | Sept. 9, 2010 – Dec. 31, 2011 |

| Tax Relief, Unemployment Compensation Reauthorization, and Job Creation Act of 2010 | 50% | 2012 |

| American Taxpayer Relief Act of 2012 | 50% | 2013 |

| Tax Increase Prevention Act of 2014 | 50% | 2014 |

| Protecting Americans from Tax Hikes Act of 2015 | 50% | 2015 – 2017 |

| Protecting Americans from Tax Hikes Act of 2015 | 40% | 2018 |

| Protecting Americans from Tax Hikes Act of 2015 | 30% | 2019 |

| Tax Cuts and Jobs Act | 100% | Sept. 27, 2017 – Dec. 31, 2022 |

| Tax Cuts and Jobs Act | 80% | 2023 |

| Tax Cuts and Jobs Act | 60% | 2024 |

| Tax Cuts and Jobs Act | 40% | 2025 |

| Tax Cuts and Jobs Act | 20% | 2026 |

|

Note: Policies in italics did not go into effect and instead were superseded by subsequent legislation. Source: Congressional Research Service, “The Section 179 and Section 168(k) Expensing Allowances: Current Law and Economic Effects,” Updated May 1, 2018, https://crsreports.congress.gov/product/pdf/RL/RL31852. *This percentage reflects the share of the eligible investment that companies are able to deduct in the first year. |

||

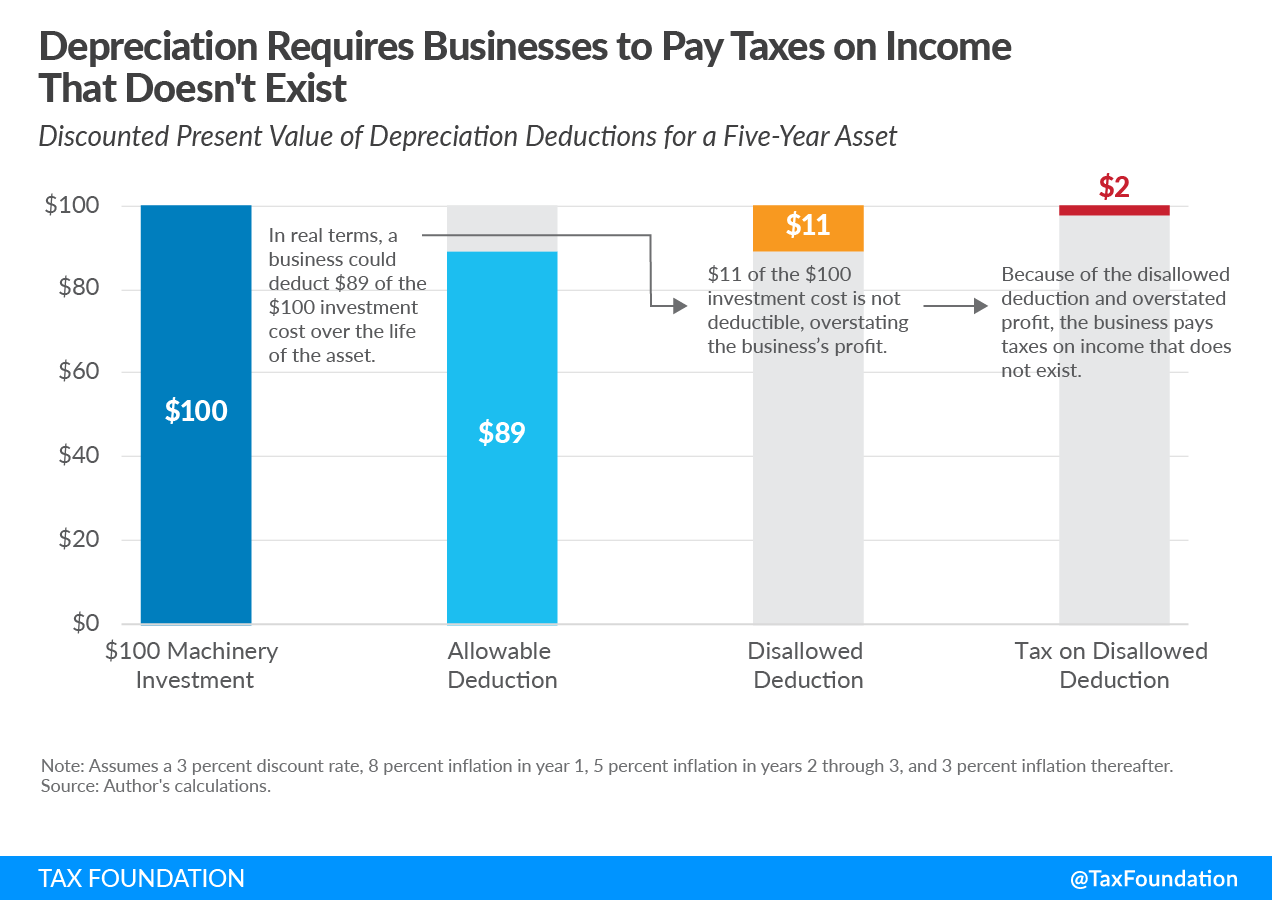

Figure 1 illustrates the erosion in the value of depreciation deductions and the resulting higher tax burden for a five-year asset, such as semiconductor manufacturing equipment, under MACRS without bonus depreciation. Because a business is prevented from deducting the full $100 in real terms, its tax bill is artificially higher and the after-tax cost of making the investment is higher. At a higher after-tax cost, fewer investment opportunities are viable.

100 Percent Bonus Depreciation and The Tax Cuts and Jobs Act

The 2017 tax law (Tax Cuts and Jobs Act, or TCJA) permitted a 100 percent bonus depreciation deduction for assets with useful lives of 20 years or less. Bonus depreciation, however, was enacted on a temporary basis and is scheduled to drop by 20 percentage points per year beginning in 2023 until it fully phases out after the end of 2026.

The pending 100 percent bonus depreciation phaseout contributes to an uncertain tax policy landscape, as businesses cannot count on whether the policy will be extended and in what form an extension might occur—and uncertainty is not an ideal situation for encouraging business investment.

The 100 percent bonus depreciation phaseout will also increase the after-tax cost of domestic investment, thereby discouraging otherwise productive investments from occurring. Failure to provide expensing on a permanent basis limits the economic benefit of expensing because the cost of capital again rises when the policy expires, and it may further induce timing shifts rather than level increases in investment.[2]

Capital Investment and Workers

Studies indicate bonus depreciation policies boost capital investment and employment levels and may raise wages (though the long-term wage effects have thus far been mixed, likely due to the temporary nature of the policy).

Economists Christopher House and Matthew D. Shapiro found sharp differences in investment for assets that qualified for the 2002 and 2003 rounds of temporary bonus depreciation: capital that benefited substantially from the policy saw sharp increases in investment, which they estimate may have increased output by roughly 0.1 percent to 0.2 percent and increased employment by roughly 100,000 to 200,000 jobs.[3] Economists Eric Zwick and James Mahon analyzed data from more than 120,000 firms across bonus depreciation episodes between 2001 to 2004 and 2008 to 2010. They found bonus depreciation raised investment in eligible capital relative to ineligible capital by 10.4 percent in the first episode and by 16.9 percent in the second episode, with small firms responding more than large firms.[4]

Economists Daniel G. Garrett, Eric Ohrn, and Juan Carlos Suarez Serrato measured the effect of exposure to bonus depreciation on employment, total earnings, and earnings-per-worker from 2002 through 2012 to study the effects on local labor markets.[5] From implementation of bonus depreciation in 2002 through its first expiration in 2005, places with larger decreases in investment costs experienced relative increases in employment, which tapered from 2005 through 2007 when bonus depreciation expired, and then stabilized from 2009 through 2012 after bonus depreciation was again implemented. Overall, the estimates indicate an increase of 6.24 million jobs at an estimated fiscal cost of $20,000 to $50,000 per job.

The estimated effects on earnings and earnings-per-worker, however, were mixed. Earnings initially rose, but gains began to dissipate after 2005 (when expensing first expired) and disappeared by 2008, while no effect was found on average earnings-per-worker. Accordingly, they find that while accelerated depreciation does not always benefit workers, “local labor markets with more exposure to the policy experience a large and stable increase in employment. These same markets experience a short-run increase in total earnings, but no increase in the average earnings-per-worker.” The authors also note, “as we consider how the policy may affect earnings…it is useful to recall that bonus depreciation evolved over time and that expectations over its persistence may influence its effects on local labor markets.”

New research from E. Mark Curtis, Daniel G. Garrett, Eric C. Ohrn, Kevin A. Roberts, and Juan Carlos Suárez Serrato compares firms that receive the most benefits from bonus depreciation to firms that receive less benefits from bonus depreciation to study the relationship between capital investment and labor demand. Covering the period from 1997 through 2011, they found firms respond to bonus depreciation by increasing their capital stock and employment. Specifically, by 2011 they find a relative increase in overall capital, concentrated in equipment, of 7.8 percent, and a relative increase in employment of 9.5 percent—gains among production workers were more pronounced, at 11.5 percent. They do not find an increase in plant-level total factor productivity but do find an increase in plant output.

Zooming in on workforce composition, the authors “find that bonus led to a relative increase in the shares of young, less educated, women, Black, and Hispanic workers. …While workers benefit from the availability of additional jobs, which are more likely to be filled by otherwise disadvantaged workers, the policy does not significantly increase average earnings.” In other words, the authors did not find an increase in the average level of earnings, largely because the expansion in employment opportunities was concentrated at the lower end of the earnings spectrum. The authors note their results mean capital and production workers are complementary inputs in modern manufacturing.

Take-up and the Issue of Net Operating Loss (NOL) Provisions

In 2017, when 50 percent bonus depreciation was in effect, the Joint Committee on Taxation (JCT) estimated just 43.8 percent of assets eligible for bonus depreciation benefited from the provision—in other words, 56.2 percent of eligible property did not benefit from bonus depreciation.[6] The report explains low depreciation usage rates are typically associated with three factors: taxpayers in net operating loss (NOL) positions, taxpayers with NOL or credit carryforwards, and multinationals where fully utilizing bonus depreciation would result in a domestic NOL position. Treasury Department research covering older episodes of bonus depreciation from 2002 through 2014 indicates bonus depreciation take-up rates of 50 to 70 percent for C corporations, finding bonus depreciation use was limited by firms in a loss position and by firms with NOL carryforwards.[7]

Empirical research indicates tax losses reduce the incentive of firms to respond to tax changes.[8] Specifically looking at bonus depreciation, research suggests the positive effect of bonus depreciation on investment is concentrated exclusively among taxable firms—even though firms without positive taxable incomeTaxable income is the amount of income subject to tax, after deductions and exemptions. Taxable income differs from—and is less than—gross income. can carry forward deductions, they must wait to receive the tax benefits from such carryforwards, which weakens the investment incentives considerably.[9] The inability to immediately use a full deduction and instead needing to wait to take it in the future thus results in similar issues to delayed depreciation deductions.

Tax Foundation estimates of the economic, revenue, and distributional effects of changes to bonus depreciation incorporate estimated take-up rates based on depreciation deductions taken from 2007 through 2013 by industry and asset type using IRS and Bureau of Economic Analysis (BEA) data.

Interactions with Global Minimum Tax and the Inflation Reduction Act

In 2021, more than 130 nations agreed to a template for adjusting how large multinational companies are taxed. Part of the agreement is a global minimum tax of 15 percent. The minimum tax base is unique in that it relies on financial accounting standards more than standard tax rules. The rules interact with capital investment in two ways, and even if the U.S. does not adopt the rules, other countries will be able to apply the minimum tax calculations to profits in the U.S.

First, 100 percent bonus depreciation makes it more likely that a corporation is subject to the global minimum tax. However, accelerated depreciation does not necessarily trigger minimum tax liability. This is because deferred tax liabilities are valued at the 15 percent minimum tax rate and counted as current tax liability.[10] As a result, credits and other tax benefits can easily push minimum tax liability below 15 percent.

In the case where a business has an effective tax rate (as measured by the global minimum tax rules) below 15 percent, it might not fully benefit from immediately deducting the cost of investment.

Another part of the minimum tax rules could protect the business, though. Even if a business has a low effective tax rate, the rules contain a carveout for a portion of profits based on tangible assets (like buildings, machinery, and equipment). The carveout is 5 percent of the value of the assets (a separate 5 percent carveout applies for payroll costs).

If a business is making significant capital investments, it could lower its effective tax rate below 15 percent (depending on eligibility for other credits or incentives); however, if the profits are smaller than the value of the carveout, then the minimum tax top-up would not apply.

Because the impact depends on details relevant to individual businesses, the tax incentives and credits they are eligible for and claim, and their existing tangible assets, the potential overall impact on business investment is not estimated in this paper.

The global minimum tax is separate and distinct from the new corporate alternative minimum tax enacted as part of the Inflation Reduction Act (IRA), which has no direct impact on bonus depreciation as all accelerated depreciation is explicitly carved out. However, to the extent the IRA increases corporate tax liabilities it may increase the take-up rate of bonus depreciation, an effect not included in the estimates in this paper.

Interactions with Limitation on Net Business Interest Expense

Under current law, businesses that pay interest on loans can deduct the amount of interest paid as a business expense on their tax returns. The 2017 tax reform limited the deductibility of interest expenses to 30 percent of a business’s earnings before interest, taxes, depreciation, and amortization (EBITDA). Starting in 2022, interest deductibility is further limited to 30 percent of a business’s earnings before interest and taxes (EBIT).

As a result of switching to EBIT, the threshold for hitting the limitation on interest deductibility will become lower (30 percent of a narrower income concept), and businesses that invest more could be at greater risk of hitting the threshold, as the accompanying table illustrates.

| EBITDA Policy | EBIT Policy | |

|---|---|---|

| A. Sales | $120 | $120 |

| B. Cost of goods sold | $50 | $50 |

| C. Interest expense | $30 | $30 |

| D. Depreciation and amortization | $20 | $20 |

| E. Taxes paid | $5 | $5 |

| F. Taxable income without interest limitation(A – B – C – D – E) | $15 | $15 |

| G. Tax before interest limit | $3.15 | $3.15 |

| H. Adjusted taxable income (ATI) under EBITDA Policy (F + C + D + E) or EBIT Policy (F + C + E) | $70 | $50 |

| I. 30 percent of ATI (30% * H) | $21 | $15 |

| J. Interest expense added back (C – I) | $9 | $15 |

| K. Final taxable income (F + J) | $24 | $30 |

| L. Tax (K * 21%) | $5.04 | $6.30 |

|

Source: Based on Kyle Pomerleau, “The Treatment of Business Interest Expense in the TCJA,” TaxNotes, May 27, 2021, https://www.taxnotes.com/tax-notes-today-federal/depreciation-amortization-and-depletion/treatment-business-interest-expense-tcja/2021/05/27/59p13 |

||

In some cases, as explained by American Enterprise Institute’s Kyle Pomerleau, the EBIT-based restriction may cause a net loss of interest deductions for some businesses with equity-financed investments.[11] Specifically, in cases in which a business is subject to the cap when undertaking an equity-financed investment (resulting in a loss in the ability to deduct interest payments when the investment is made) but does not expect to be subject to the cap in the future, the business would have to carry its disallowed deduction forward, eroding its real value. If, however, the business expects to be subject to the cap in future years, the earnings from the new equity-financed investment would increase its earnings in future years, offsetting some or all of the initial loss in its interest deductions in present value terms.

Thus, the EBIT cap potentially interacts with depreciation allowances, including bonus depreciation, to the detriment of certain firms. While the limitation is intended, at least in part, to reduce the tax code’s bias in favor of debt-financed investment,[12] the recent switch from EBITDA to EBIT can create disadvantages for companies undertaking domestic investment. It also diverges from international norms; for instance, most OECD countries limit their interest based on EBITDA, not EBIT.[13]

The potential macroeconomic impact of interactions between depreciation deductions and the EBIT cap is not modeled in this paper; however, the macroeconomic impact of switching from EBITDA to EBIT is relatively small compared to the impact of allowing bonus depreciation to expire.[14]

Economic, Revenue, and Distributional Impact of Permanent 100 Percent Bonus Depreciation

Using the Tax Foundation General Equilibrium Model, we estimate making 100 percent bonus depreciation permanent would expand long-run economic output by 0.4 percent, the capital stock by 0.7 percent, wages by 0.3 percent, and employment by 73,000 full-time equivalent jobs.

| GDP | +0.4% |

| GNP | +0.3% |

| Capital Stock | +0.7% |

| Wages | +0.3% |

| Full-time Equivalent Employment | +73,000 |

|

Source: Tax Foundation General Equilibrium Model, August 2022. |

|

Over the 10-year budget window from 2023 through 2032, we estimate permanent bonus depreciation would reduce federal revenue by about $400 billion on a conventional basis. The cost of permanence would continue to fall outside the budget window as the transitional costs fade. On a dynamic basis, accounting for increased economic output and higher income and payroll tax receipts, the cost of the policy falls to $296 billion over the 10-year window. The cost would fall outside the budget window, as can be seen in the declining revenue pattern toward the end of the budget window.

| 2023 | 2024 | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2023-2032 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Conventional | -$19.8 | -$35.5 | -$47.4 | -$56.9 | -$65.8 | -$50.2 | -$39.6 | -$32.5 | -$27.8 | -$24.7 | -$400.3 |

| Dynamic | -$19.6 | -$35.0 | -$43.9 | -$50.3 | -$55.4 | -$37.7 | -$25.5 | -$15.9 | -$9.1 | -$4.1 | -$296.0 |

Making 100 percent bonus depreciation permanent would have different impacts across industries. For example, we find that the agriculture & utilities, real estate, information, and transportation and warehousing sectors would have the largest reduction in corporate tax liabilities as a portion of income in 2023 and 2032. Administrative services, accommodation and food services, and professional services would also substantively benefit from making 100 percent bonus depreciation permanent.

| Industry | Change in Tax Liabilities as a Portion of Income, 2023 | Change in Tax Liabilities as a Portion of Income, 2032 |

|---|---|---|

| Agriculture & Utilities | -24.8% | -42.4% |

| Real estate and rental/leasing | -19.7% | -17.0% |

| Information | -14.9% | -29.8% |

| Transportation and warehousing | -14.0% | -11.7% |

| Administrative services | -6.8% | -4.8% |

| Accommodation and food services | -5.8% | -5.3% |

| Professional, scientific, and technical services | -5.6% | -7.0% |

| Wholesale trade | -5.0% | -3.7% |

| Retail trade | -3.9% | -3.4% |

| Mining | -3.8% | -2.4% |

| Finance and insurance | -3.3% | -1.9% |

| Construction | -2.3% | -1.2% |

| Manufacturing | -2.0% | -2.0% |

| Miscellaneous services | -1.9% | -1.8% |

|

Note: The two columns display the change in tax liabilities as a portion of income for firms in each industry when making permanent 100 percent bonus depreciation in 2023 and 2032. The industry breakout follows the NAICS major industries used in the Corporate Tax model. The industry estimates do not include pass-through firms such as partnerships or sole proprietorships. Source: Tax Foundation Corporate Tax Model, August 2022. |

||

It is important to note, however, that the economic boost from making 100 percent bonus depreciation permanent comes from the change in incentives to invest moving forward and not from an improvement in firms’ cash position due to a decline in tax liabilities driven by 100 percent bonus depreciation.

Distributionally, by the end of the budget window, permanent 100 percent bonus depreciation would increase after-tax income by 0.2 percent on average on a conventional basis. The top 1 percent of taxpayers would see a higher increase of about 0.3 percent. On a long-run dynamic basis, factoring in increased economic output, after-tax incomeAfter-tax income is the net amount of income available to invest, save, or consume after federal, state, and withholding taxes have been applied—your disposable income. Companies and, to a lesser extent, individuals, make economic decisions in light of how they can best maximize their earnings. would increase by 0.4 percent overall, and by a similar amount in each income quintile.

| Conventional, 2023 | Conventional, 2032 | Dynamic, Long-run | |

|---|---|---|---|

| 0% – 20.0 | 0.1% | 0.1% | 0.4% |

| 20.0% – 40.0 | 0.0% | 0.1% | 0.4% |

| 40.0% – 60.0 | 0.1% | 0.1% | 0.4% |

| 60.0% – 80.0 | 0.1% | 0.1% | 0.3% |

| 80.0% – 100 | 0.2% | 0.2% | 0.4% |

| 80.0% – 90.0 | 0.1% | 0.1% | 0.4% |

| 90.0% – 95.0 | 0.1% | 0.1% | 0.4% |

| 95.0% – 99.0 | 0.2% | 0.2% | 0.4% |

| 99.0% – 100 | 0.4% | 0.3% | 0.5% |

| Total | 0.1% | 0.2% | 0.4% |

|

Source: Tax Foundation General Equilibrium Model, August 2022. |

|||

Conclusion

The phaseout of 100 percent bonus depreciation, scheduled to take place after the end of 2022, will increase the after-tax cost of investment in the United States. Preventing the phaseout and making 100 percent bonus depreciation a permanent feature of the U.S. tax code is crucial in the effort to increase business investment and create better opportunities for workers.

Research indicates past instances of bonus depreciation have boosted capital accumulation and employment, especially among disadvantaged workers. Our modeling indicates making 100 percent bonus depreciation a permanent feature of the U.S. tax code would increase long-run economic output by 0.4 percent, the capital stock by 0.7 percent, and employment by 73,000 full-time equivalent jobs. On a permanent basis, 100 percent bonus depreciation would support business investment, capital formation, and economic output over the long term while creating more opportunities for workers.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

SubscribeMethodology

Tax Foundation’s General Equilibrium Model computes tax items related to investment and cost recoveryCost recovery refers to how the tax system permits businesses to recover the cost of investments through depreciation or amortization. Depreciation and amortization deductions affect taxable income, effective tax rates, and investment decisions.. Using historical investment since 1960 across 95 asset types and 14 major industry groups, as well as current and historical cost recovery rules for each asset type, the model calculates tax depreciation deductions, amortization of intangible assets, and the research credit for each year.

The calculations capture the effects of detailed policy changes for capital cost recovery: changes to depreciation rules, such as the method or class life; rates; and eligibility. The most recent update in the corporate capital model can simulate the take-up of bonus depreciation; eligibility and use of section 179 expensing; expensing and amortization of intellectual property investment; and rules of the regular and alternative research tax credits.

The model draws on detailed fixed asset investment data from the Bureau of Economic Analysis, with an adjustment to reflect differential growth rates of investment by corporations compared to other businesses. To reconcile the data with depreciation deductions reported by the IRS (using slightly different industry definitions and only C corporations), we jointly scale the data and calibrate the bonus depreciation take-up rates by industry and by type of business (domestic vs. foreign owned), to target IRS depreciation deductions for each year from 2007-2013.

When simulating the revenue and economic effects of 100 percent bonus depreciation, the take-up rate for the non-corporate sector is derived using data from the Treasury Department and is calibrated against the data derived from the corporate tax model.[15]

[1] Lawrence H. Summers, “Investment Incentives and the Discounting of Depreciation Allowances,” in Martin S. Feldstein, The Effects of Taxation on Capital Accumulation (Chicago: University of Chicago Press, 1987), https://www.nber.org/system/files/chapters/c11352/c11352.pdf.

[2] See discussion in Kyle Pomerleau, “Economic and Budgetary Impact of Temporary Expensing,” Tax Foundation, Oct. 4, 2017, https://www.taxfoundation.org/economic-budgetary-impact-temporary-expensing/.

[3] Christopher House and Matthew D. Shapiro, “Temporary Investment Tax Incentives: Theory with Evidence from Bonus Depreciation,” National Bureau of Economic Research, September 2006, https://www.nber.org/system/files/working_papers/w12514/w12514.pdf.

[4] Eric Zwick and James Mahon, “Tax Policy and Heterogenous Investment Behavior,” American Economic Review 107:1, January 2017, https://www.aeaweb.org/articles?id=10.1257/aer.20140855.

[5] Dan G. Garrett, Eric Ohrn, and Juan Carlos Suárez Serrato, “Tax Policy and Local Labor Market Behavior,” American Economic Review: Insights 2:1, March 2020, https://pubs.aeaweb.org/doi/pdfplus/10.1257/aeri.20190041.

[6] The Joint Committee on Taxation, “Tax Incentives for Domestic Manufacturing,” Mar. 12, 2021, https://www.jct.gov/CMSPages/GetFile.aspx?guid=668fcf5a-30fc-4628-a65a-71c9fbdc90ac.

[7] John Kitchen and Matthew Knittel, “Business Use of Section 179 Expensing and Bonus Depreciation, 2002-2014,” The Department of the Treasury, October 2016, https://home.treasury.gov/system/files/131/wp-110.pdf.

[8] See discussion in Eric Zwick and James Mahon, “Tax Policy and Heterogenous Investment Behavior,” National Bureau of Economic Research, January 2016, https://www.nber.org/system/files/working_papers/w21876/w21876.pdf.

[9] Eric Zwick and James Mahon, “Tax Policy and Heterogenous Investment Behavior.”

[10] For more detail on the global minimum tax, see Daniel Bunn, “Accounting for the Global Minimum Tax,” Tax Foundation, Mar. 16, 2022, https://www.taxfoundation.org/global-minimum-tax-model-rules/.

[11] Kyle Pomerleau, “The Treatment of Business Interest Expense in the TCJA,” Tax Notes, May 27, 2021, https://www.taxnotes.com/tax-notes-today-federal/depreciation-amortization-and-depletion/treatment-business-interest-expense-tcja/2021/05/27/59p13.

[12] For more about the issue of interest deductibility and reforms to address the debt-equity bias, see Alan Cole, “Interest Deductibility – Issues and Reforms,” Tax Foundation, May 4, 2017, https://www.taxfoundation.org/interest-deductibility/.

[13] Kyle Pomerleau, Daniel Bunn, and Thomas Locher, “Anti-Base Erosion Provisions and Territorial Tax Systems in OECD Countries,” Tax Foundation, July 7, 2021, https://www.taxfoundation.org/anti-base-erosion-territorial-tax-systems/#Interest.

[14] Kyle Pomerleau, “The treatment of business interest expense, the trilogy,” Tax Notes Federal, May 24, 2021, https://www.aei.org/articles/the-treatment-of-business-interest-expense-the-trilogy/.

[15] Kitchen and Knittel, “Business Use of Section 179 Expensing and Bonus Depreciation, 2002-2014.”

Share this article