New Guidance on State Aid Under the CARES Act

The U.S. Department of the Treasury recently issued new guidance on allowable expenses using the $150 billion in state aid provided under the CARES Act, a point on which there has been considerable confusion.

3 min read

Senate Passes Additional Funding for Small Business Relief, But Questions Remain on the Deductibility of PPP Expenses

The sooner federal policymakers or regulators clarify tax questions about the Paycheck Protection Program (PPP), the more certainty firms will have when they accept the economic relief to keep their businesses afloat.

3 min read

Keeping it Simple: Approaching the Next Stage of Coronavirus Tax Policy

When businesses and taxpayers look to the government for relief, it is paramount that lawmakers do their best to craft transparent and coherent legislation that is the least confusing for all.

4 min read

Tax Policy After Coronavirus: Clearing a Path to Economic Recovery

Governments at all levels must work to remove the tax policy barriers that stand in the way of economic recovery and long-term prosperity following the COVID-19 crisis. Our new guide outlines several comprehensive options that policymakers can take at the federal and state levels.

26 min read

States Should Be Allowed to Levy Sales Taxes on Internet Access

On July 1, sales taxes levied on internet access in six states—Hawaii, New Mexico, Ohio, South Dakota, Texas, and Wisconsin—will become illegal under the provisions of the Permanent Internet Tax Freedom Act (PITFA)

4 min read

A Review of Net Operating Loss Tax Provisions in the CARES Act and Next Steps for Phase 4 Relief

In addition to providing economic relief to individuals and loans to businesses struggling during the coronavirus crisis, the CARES Act changed several tax provisions to increase liquidity to ensure firms survive a large decline in cash flow.

7 min read

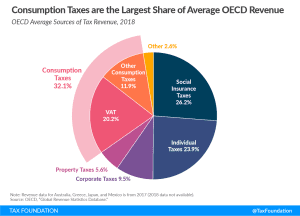

New OECD Study: Consumption Tax Revenues during Economic Downturns

Compared to other tax revenue sources, consumption tax revenue as a share of GDP tends to be relatively stable over time, even during economic downturns.

2 min read

Is Now the Time for a $100 billion Tax Increase?

Seemingly unconcerned about how the digital project could impact the economy at this crisis moment, officials at the OECD recently released a statement boasting that they are continuing to work “full steam” on their global digital tax project.

5 min read

April 10th Afternoon State Tax Update

California extends tax filing and payment deadline to July 31 for a broad spectrum of business taxes as Virginia keeps May 1st tax filing deadline.

5 min read