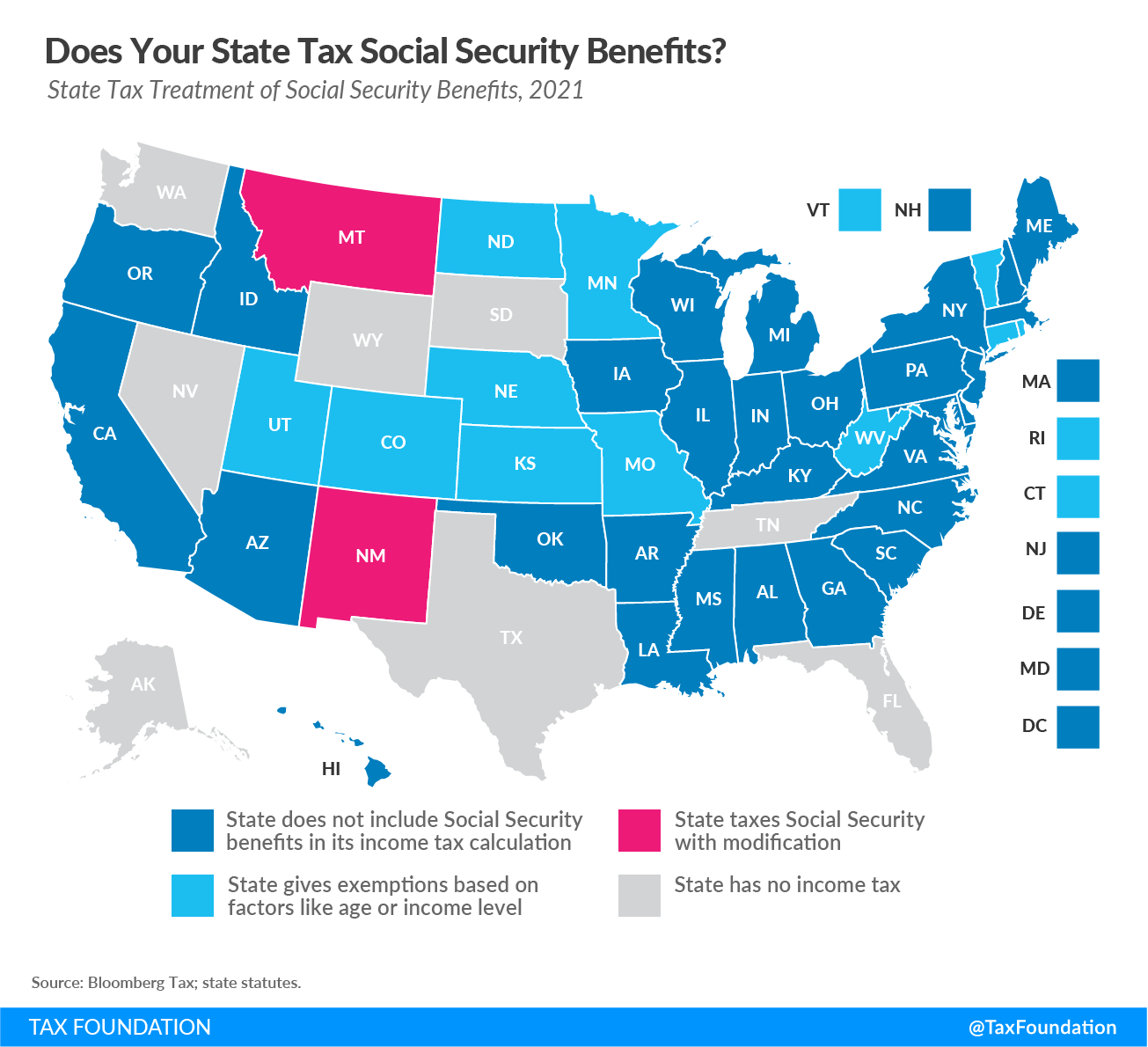

Thirteen states tax Social Security benefits, a matter of significant interest to retirees. Each of these states has its own approach to determining what share of benefits is subject to taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. , though these provisions can be grouped together into a few broad categories. Today’s map illustrates these approaches.

Thirty-seven states and D.C. either have no income tax (AK, FL, NV, SD, TN, TX, WA, WY) or do not include Social Security benefits in their calculation for taxable income (AL, AZ, AR, CA, DE, DC, GA, HI, ID, IL, IN, IA, KY, LA, ME, MD, MA, MI, MS, NH, NJ, NY, NC, OH, OK, OR, PA, SC, VA, WI).

New Mexico includes all Social Security benefits in the taxable incomeTaxable income is the amount of income subject to tax, after deductions and exemptions. Taxable income differs from—and is less than—gross income. base, though the state provides a deduction that reduces the taxability of all retirement income.

Utah taxes Social Security benefits but uses tax credits to eliminate liability for beneficiaries with less than $30,000 (single filers) or $50,000 (joint filers), with credits phasing out at 2.5 cents for each dollar above these thresholds. Until this year, Utah’s credits mirrored the federal tax code, where the taxable portion of Social Security income depends on two factors: a taxpayer’s filing status and the size of their “combined income” (adjusted gross incomeFor individuals, gross income is the total of all income received from any source before taxes or deductions. It includes wages, salaries, tips, interest, dividends, capital gains, rental income, alimony, pensions, and other forms of income. For businesses, gross income (or gross profit) is the sum of total receipts or sales minus the cost of goods sold (COGS)—the direct costs of producing goods, including inventory and certain labor costs. + nontaxable interest + half of Social Security benefits). Under federal law—and Utah law prior to the enactment of HB 86—thresholds were $25,000 and $32,000 respectively.

Additionally, several states reduce the level of taxation applied to Social Security benefits depending on factors like age or income level:

Colorado allows taxpayers to subtract some of their Social Security income (as well as pension income) as long as they are age 55 or older, under the “pension and annuity subtraction.”

Connecticut excludes Social Security benefits from income calculations for any taxpayer with less than $75,000 (single filers) or $100,000 (filing jointly) in adjusted gross income (AGI).

Kansas provides an exemption for such benefits for any taxpayer whose AGI is $75,000, regardless of filing status.

Minnesota provides a graduated system of Social Security subtractions which kick in if someone’s provisional income is below $81,180 (single filer) or $103,930 (filing jointly).

Missouri allows a 100 percent Social Security exemption as long as the taxpayer is 62 or older and has less than $85,000 (single filer) or $100,000 (filing jointly) in annual income.

Nebraska allows single filers with $43,000 in AGI or less ($58,000 married filing jointly) to subtract their Social Security income. If their income is over that threshold, the state follows the federal treatment.

North Dakota allows taxpayers to deduct taxable Social Security benefits if their AGI is less than $50,000 (single filer) or $100,000 (filing jointly).

Rhode Island allows a modification for taxpayers who have reached full retirement age as defined by the Social Security Administration and have a federal AGI of under $81,900 (single filer) or $102,400 (filing jointly).

Vermont provides a graduated system of Social Security exemptions which kick in if a taxpayer’s income is below $34,000 (single filer) or $44,000 (filing jointly).

While Montana and West Virginia do not have age or income stipulations, their approaches to such taxes still warrant attention.

In Montana, which does not have age or income stipulations, some Social Security benefits may be taxable, and the state advises taxpayers to fill out a worksheet to determine how the state taxable amount differs from the federally taxable amount.

West Virginia passed a law in 2019 to begin phasing out taxes on Social Security for those with incomes not exceeding $50,000 (single filers) or $100,000 (married filing jointly). Beginning in tax year 2020, the state exempted 35 percent of benefits for qualifying taxpayers. As of 2021, that amount increased to 65 percent, and in 2022, the benefits will be completely exempt for those taxpayers.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe